Taxation Law Assignment: Income, Capital Gains, and Tax Avoidance

VerifiedAdded on 2020/04/07

|10

|1671

|60

Homework Assignment

AI Summary

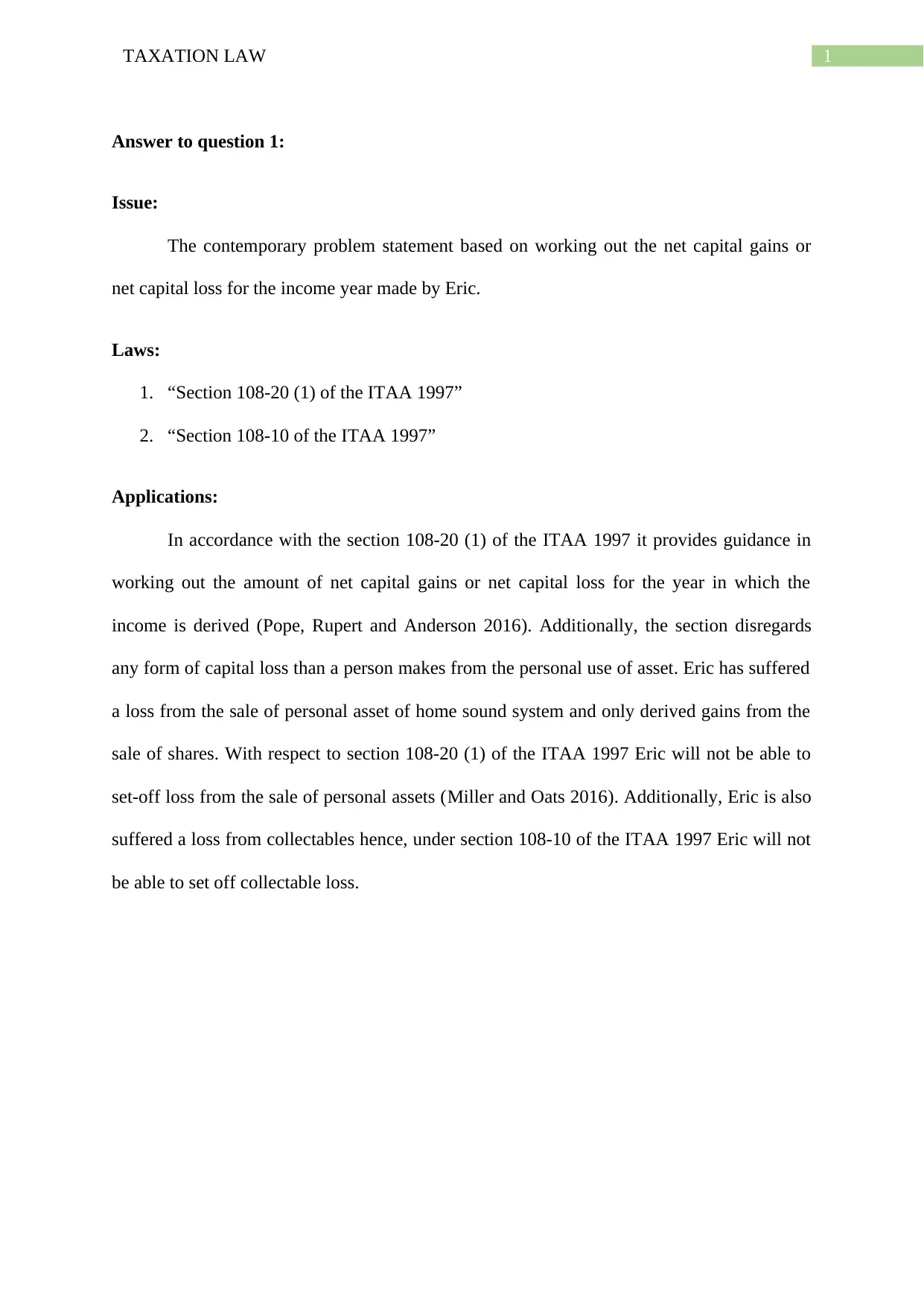

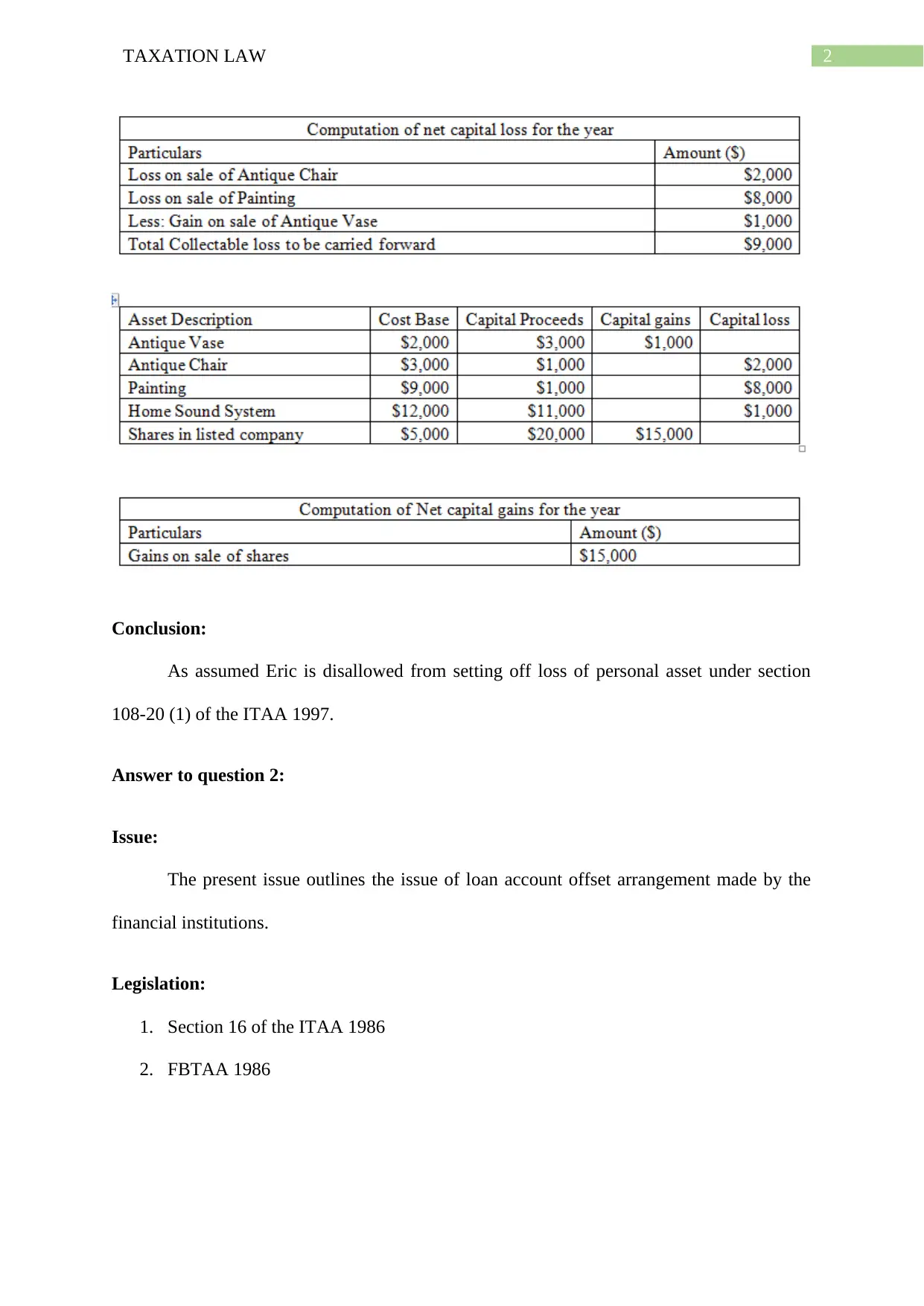

This taxation law assignment delves into several key areas of tax law. It begins by examining the calculation of net capital gains or losses, specifically addressing the tax implications for an individual, Eric, who has both capital gains from shares and losses from personal assets. The assignment then explores the issue of loan account offset arrangements by financial institutions and how these arrangements may constitute fringe benefits. It further analyzes the division of net income or loss from a rental property between co-owners, Jack and Jill, considering the application of relevant tax rulings. The assignment also discusses tax avoidance strategies, referencing the case of IRC v Duke of Westminster and WT Ramsay v. IRC, and their implications in the Australian context. Finally, it examines the taxation of income derived from the sale of timber by a primary producer, Bill, considering relevant legislation and case law, including FC of T v McCauley (1944). The assignment provides detailed analysis and conclusions for each scenario, supported by relevant legislation and case law.

1 out of 10

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.