Taxation Law Report: Analysis of Tax Deductions and Credits

VerifiedAdded on 2020/04/01

|14

|2819

|31

Report

AI Summary

This taxation law report provides a comprehensive analysis of various tax-related issues. It begins by examining the deductibility of expenses related to transporting machinery, asset revaluation, winding-up costs, and legal expenses under Section 8-1 of the ITAA 1997, supported by relevant case law and rulings. The report then analyzes GST input credits for a company's advertising expenditure, calculating the eligible amount based on the nature of the expenses. Next, it delves into the calculation of foreign tax offset under Subdivision 717A, determining the limit of the offset. Finally, the report presents a statement calculating the income from a partnership, including revenue, various incomes, and eligible deductions, to arrive at the gross total income and net income after deductions. The report offers a detailed breakdown of each component, including the application of relevant tax laws and regulations.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Taxation Law

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................6

Answer to Question No 3...........................................................................................................8

Answer to Question No 4.........................................................................................................10

Reference List and Bibliography.............................................................................................12

TAXATION LAW

Table of Contents

Answer to Question No 1...........................................................................................................2

Answer to Question No 2...........................................................................................................6

Answer to Question No 3...........................................................................................................8

Answer to Question No 4.........................................................................................................10

Reference List and Bibliography.............................................................................................12

2

TAXATION LAW

Answer to Question No 1

Issue I

From the active situation of transporting a machinery from one location to the other,

the expenses and the cost that the company may incur can be taken as a deductions that are

non-allowable in accordance to the “Section 8-1 of the ITAA 1997”.

The laws that are applicable to this issue are

“Section 8-1 of the ITAA 1997 “British Insulated and Helsby Cables”

The use of the laws can be applicable as it is pertinent from the current scenario that

transporting the machinery from one location to the other requires the use of a certain cost

and it can be explained that no tolerable deductions would be allowable with respect to

“Section 8-1 of the ITAA 1997” . In order to compute the depreciation, transporting the

machinery into a new location can be explained that it associates cost that finally leads to the

rise in the machinery cost. It has been indicated in the “British Insulated & Helsby Cables”

various kinds of expenses and cost that is acquired during the time of the movement

represents a benefit that is beneficial in nature for the firm by transporting the machine to the

new location. With respect to the “Taxation Ruling TD 93/126” fitting of the machine and

initiating the functions of the organization leads to the involvement of the cost for the shifting

of the machine in a new location and sustainably creating a section of the profit1. It must be

cited that the associated cost in shifting the machine to the new arena may not be regarded as

the deductions that are allowable.

1 Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue (2016).

TAXATION LAW

Answer to Question No 1

Issue I

From the active situation of transporting a machinery from one location to the other,

the expenses and the cost that the company may incur can be taken as a deductions that are

non-allowable in accordance to the “Section 8-1 of the ITAA 1997”.

The laws that are applicable to this issue are

“Section 8-1 of the ITAA 1997 “British Insulated and Helsby Cables”

The use of the laws can be applicable as it is pertinent from the current scenario that

transporting the machinery from one location to the other requires the use of a certain cost

and it can be explained that no tolerable deductions would be allowable with respect to

“Section 8-1 of the ITAA 1997” . In order to compute the depreciation, transporting the

machinery into a new location can be explained that it associates cost that finally leads to the

rise in the machinery cost. It has been indicated in the “British Insulated & Helsby Cables”

various kinds of expenses and cost that is acquired during the time of the movement

represents a benefit that is beneficial in nature for the firm by transporting the machine to the

new location. With respect to the “Taxation Ruling TD 93/126” fitting of the machine and

initiating the functions of the organization leads to the involvement of the cost for the shifting

of the machine in a new location and sustainably creating a section of the profit1. It must be

cited that the associated cost in shifting the machine to the new arena may not be regarded as

the deductions that are allowable.

1 Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

With regards to the “Section 8-1 of the ITAA 1997”, it can be said that expense of

shifting the machine will not be granted as substructions as it has been considered as a capital

expenditure.

Issue II

This problem brings forth the query about whether asset revaluation impacts insurance

coverage, which would form a segment of the permissible deductions with respect to

“Section 8-1 of ITAA 1997”. The laws that applicable to this scenario involve:

“Section 8-1 of the ITAA 1997”

It can be considered that the cost that is generated from the asset revaluation in order

to have an impact on the insurance coverage may be regarded as the deductions that are

permissible and this is connected directly with the fixed assets. During the time of evaluating

the deductible characteristics of the expenditure, it is mandatory to ensure such occurrence of

the expenditure during the asset revaluation outcomes within the earning producing capacity

or it can be simply incurred to safeguard the asset2. If this condition provides a conditional

benefit to the firm or it is in nature recurring then it would be granted as permissible

deductions provided in “Section 8-1 of the ITAA 1997”.

Hence, it can be explained that the insurance coverage cost will be considered as

subtractions that would be allowable in “Section 8-1 of the ITAA 1997” as it has a persistent

element of the expenditure.

2 Bell, Stephen, and Andrew Hindmoor. "The structural power of business and the power of

ideas: The strange case of the Australian mining tax." New Political Economy 19, no. 3

(2014): 470-486.

TAXATION LAW

With regards to the “Section 8-1 of the ITAA 1997”, it can be said that expense of

shifting the machine will not be granted as substructions as it has been considered as a capital

expenditure.

Issue II

This problem brings forth the query about whether asset revaluation impacts insurance

coverage, which would form a segment of the permissible deductions with respect to

“Section 8-1 of ITAA 1997”. The laws that applicable to this scenario involve:

“Section 8-1 of the ITAA 1997”

It can be considered that the cost that is generated from the asset revaluation in order

to have an impact on the insurance coverage may be regarded as the deductions that are

permissible and this is connected directly with the fixed assets. During the time of evaluating

the deductible characteristics of the expenditure, it is mandatory to ensure such occurrence of

the expenditure during the asset revaluation outcomes within the earning producing capacity

or it can be simply incurred to safeguard the asset2. If this condition provides a conditional

benefit to the firm or it is in nature recurring then it would be granted as permissible

deductions provided in “Section 8-1 of the ITAA 1997”.

Hence, it can be explained that the insurance coverage cost will be considered as

subtractions that would be allowable in “Section 8-1 of the ITAA 1997” as it has a persistent

element of the expenditure.

2 Bell, Stephen, and Andrew Hindmoor. "The structural power of business and the power of

ideas: The strange case of the Australian mining tax." New Political Economy 19, no. 3

(2014): 470-486.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

Issue III

This problem has highlighted the subject about whether or not the winding up cost of

an organization will be treated as permissible with respect to “Section 8-1 of the ITAA

1997”. The laws that are associated with this issue involve:

“FC of T v Snowden and Wilson Pty Ltd (1958)” “Section 8-1 of the ITAA 1997

This problem has highlighted the issue that cost or the expenditure that is associated

while binding up the operations of the business have been undertaken in the activities of the

business and will thus would not be granted as deductions with respect to the “Section 8-1 of

the ITAA 1997”. As explained in the “Taxation Ruling of ID 2004/367” the legal expense

that is accounted is granted as deductions that are permissible3. This is due to the fact that the

taxpayer has incurred the expenditure during the time undertaking the activities of the

business with the help of which the individual generates their income. With this respect, a

case can be highlighted of “FC of T v Snowden and Wilson Pty Ltd 1958” in which the legal

expenses for conflicting the petition of winding up even though reaching the eligibility of

positive appendages will not be regarded as subtractions that are granted as they have the

capability of capital and goes within the structure of the business4.

3 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

4 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

TAXATION LAW

Issue III

This problem has highlighted the subject about whether or not the winding up cost of

an organization will be treated as permissible with respect to “Section 8-1 of the ITAA

1997”. The laws that are associated with this issue involve:

“FC of T v Snowden and Wilson Pty Ltd (1958)” “Section 8-1 of the ITAA 1997

This problem has highlighted the issue that cost or the expenditure that is associated

while binding up the operations of the business have been undertaken in the activities of the

business and will thus would not be granted as deductions with respect to the “Section 8-1 of

the ITAA 1997”. As explained in the “Taxation Ruling of ID 2004/367” the legal expense

that is accounted is granted as deductions that are permissible3. This is due to the fact that the

taxpayer has incurred the expenditure during the time undertaking the activities of the

business with the help of which the individual generates their income. With this respect, a

case can be highlighted of “FC of T v Snowden and Wilson Pty Ltd 1958” in which the legal

expenses for conflicting the petition of winding up even though reaching the eligibility of

positive appendages will not be regarded as subtractions that are granted as they have the

capability of capital and goes within the structure of the business4.

3 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

4 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

5

TAXATION LAW

It can therefore be said that the expenditure that is taken place for conflicting winding up

petition would not be granted as permissible deductions with respect to “Section 8-1 of the

ITAA 1997”.

Issue IV

This problem brings in the issue of the legal expenditure that arises from the solicitor services

for several functions related to the business of their client can be regarded as permissible

deductions under “Section 8-1 of the ITAA 1997”. The laws applicable involve:

“Section 8-1 of the ITAA 1997”

With respect to the situation that has been explained above, the matter brings forth the

query that whether the legal expense incurred by an individual in relation to their expenses

related to the business can be considered for any sort of deductions that are permissible in

“Section 8-1 of the ITAA 1997” . If the taxpayer has incurred any legal cost that is not

associated to the business then it will be treated as deductions that are non-permissible5. With

respect to the context provided, it can be concluded that any expenditure that is legal paid by

the taxpayer would be permitted as allowable subtractions as they form a segment of the

business and it is taken place in giving out the income that is assessable to the taxpayer.

It can be explained that the legal expenditure gained from the functions of the

business would be permitted in the deduction form with respect to “Section 8-1 of the ITAA

1997”6.

5 Doran, Christopher M., Joshua M. Byrnes, Linda J. Cobiac, Brian Vandenberg, and Theo

Vos. "Estimated impacts of alternative Australian alcohol taxation structures on consumption,

public health and government revenues." Med J Aust 199, no. 9 (2013): 619-622.

TAXATION LAW

It can therefore be said that the expenditure that is taken place for conflicting winding up

petition would not be granted as permissible deductions with respect to “Section 8-1 of the

ITAA 1997”.

Issue IV

This problem brings in the issue of the legal expenditure that arises from the solicitor services

for several functions related to the business of their client can be regarded as permissible

deductions under “Section 8-1 of the ITAA 1997”. The laws applicable involve:

“Section 8-1 of the ITAA 1997”

With respect to the situation that has been explained above, the matter brings forth the

query that whether the legal expense incurred by an individual in relation to their expenses

related to the business can be considered for any sort of deductions that are permissible in

“Section 8-1 of the ITAA 1997” . If the taxpayer has incurred any legal cost that is not

associated to the business then it will be treated as deductions that are non-permissible5. With

respect to the context provided, it can be concluded that any expenditure that is legal paid by

the taxpayer would be permitted as allowable subtractions as they form a segment of the

business and it is taken place in giving out the income that is assessable to the taxpayer.

It can be explained that the legal expenditure gained from the functions of the

business would be permitted in the deduction form with respect to “Section 8-1 of the ITAA

1997”6.

5 Doran, Christopher M., Joshua M. Byrnes, Linda J. Cobiac, Brian Vandenberg, and Theo

Vos. "Estimated impacts of alternative Australian alcohol taxation structures on consumption,

public health and government revenues." Med J Aust 199, no. 9 (2013): 619-622.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

Answer to Question No 2

The purchase undertaken by any firm is liable for GST input credit if suitable

documents that are associated to these kinds of transactions are kept accurately. According to

the GST Act of 1999, any firm functioning in the market in order to earn profit have the

authority to undertake input credits for the payment of the GST that associates buying of

assets and materials.

Big Bank Ltd have incurred $1,650,000 that is inclusive of GST on the expenditure

related to advertisement. The bank is under the consideration to make sure that the

advertisement expenditure will be granted as input credits and not as expenditure as the value

is inclusive of GST.

There are various rules that are applicable as with respect to Chapter 2 of the GST Act

1999, it explains that a firm will be granted to undertake the input tax credit of GST on these

expenditures that are incurred by an organization during the general course of the business in

case such expenditures are GST inclusive.

Big Bank Ltd provides services that related to finance to the general population and

operates from over more than 50 branches all over the nation. Its headquarters is situated on a

10 building. Presently, the bank has incorporated home content and insurance products in the

market other than giving out advances and keeping storages of the deposit of the individuals.

Due to the intention of advertisement, the bank has stored a budget of sum $1,650,000 from

which $550,000 is committed for advertisement of loan and home products out of which just

2% of the aggregate income of the bank is created. The remaining value of $1,100,000 is for

6 Grubert, Harry, and Rosanne Altshuler. "Shifting the Burden of taxation from the Corporate

to the perSonal level and getting the Corporate tax rate down to 15 perCent." (2016).

TAXATION LAW

Answer to Question No 2

The purchase undertaken by any firm is liable for GST input credit if suitable

documents that are associated to these kinds of transactions are kept accurately. According to

the GST Act of 1999, any firm functioning in the market in order to earn profit have the

authority to undertake input credits for the payment of the GST that associates buying of

assets and materials.

Big Bank Ltd have incurred $1,650,000 that is inclusive of GST on the expenditure

related to advertisement. The bank is under the consideration to make sure that the

advertisement expenditure will be granted as input credits and not as expenditure as the value

is inclusive of GST.

There are various rules that are applicable as with respect to Chapter 2 of the GST Act

1999, it explains that a firm will be granted to undertake the input tax credit of GST on these

expenditures that are incurred by an organization during the general course of the business in

case such expenditures are GST inclusive.

Big Bank Ltd provides services that related to finance to the general population and

operates from over more than 50 branches all over the nation. Its headquarters is situated on a

10 building. Presently, the bank has incorporated home content and insurance products in the

market other than giving out advances and keeping storages of the deposit of the individuals.

Due to the intention of advertisement, the bank has stored a budget of sum $1,650,000 from

which $550,000 is committed for advertisement of loan and home products out of which just

2% of the aggregate income of the bank is created. The remaining value of $1,100,000 is for

6 Grubert, Harry, and Rosanne Altshuler. "Shifting the Burden of taxation from the Corporate

to the perSonal level and getting the Corporate tax rate down to 15 perCent." (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

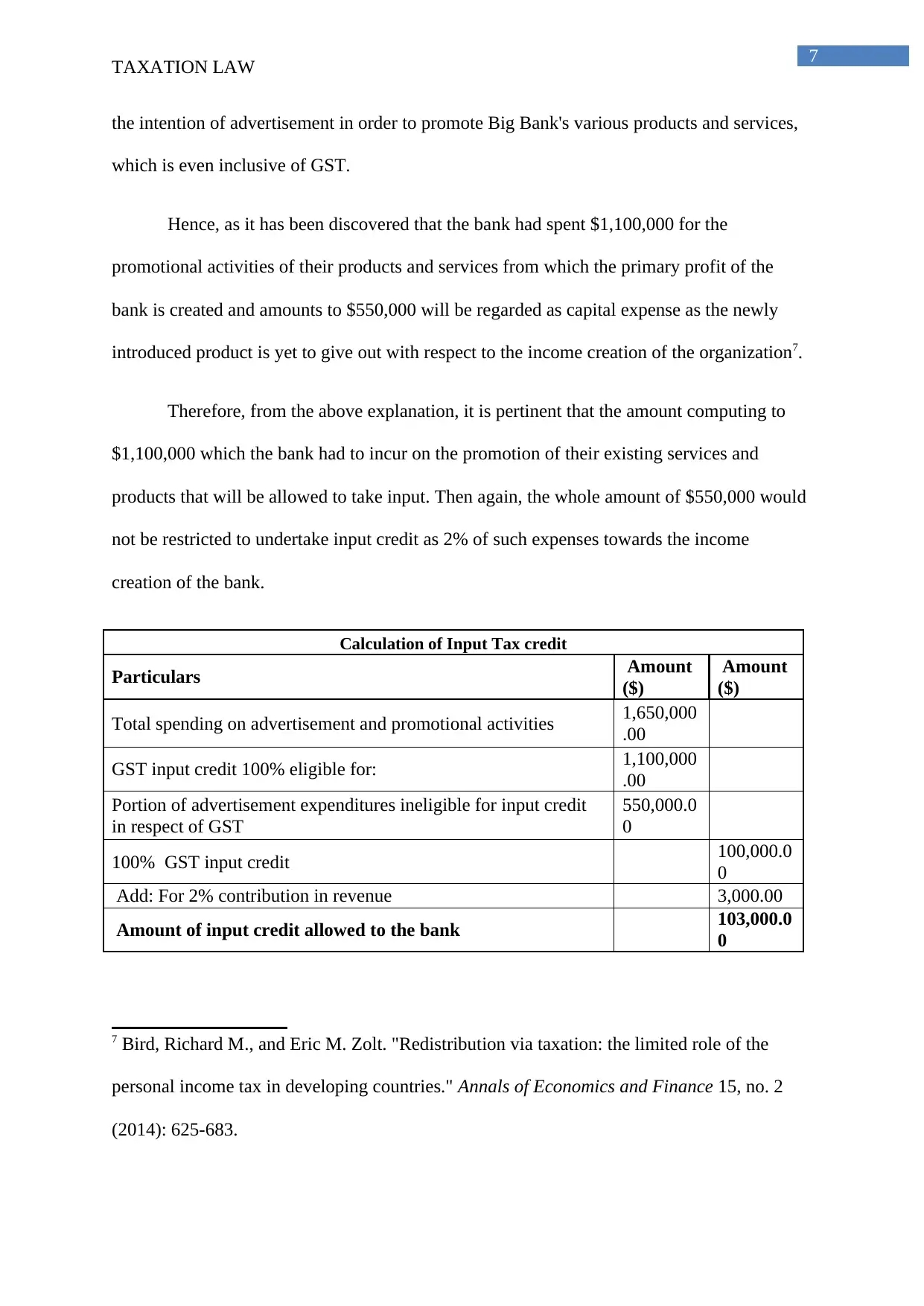

the intention of advertisement in order to promote Big Bank's various products and services,

which is even inclusive of GST.

Hence, as it has been discovered that the bank had spent $1,100,000 for the

promotional activities of their products and services from which the primary profit of the

bank is created and amounts to $550,000 will be regarded as capital expense as the newly

introduced product is yet to give out with respect to the income creation of the organization7.

Therefore, from the above explanation, it is pertinent that the amount computing to

$1,100,000 which the bank had to incur on the promotion of their existing services and

products that will be allowed to take input. Then again, the whole amount of $550,000 would

not be restricted to undertake input credit as 2% of such expenses towards the income

creation of the bank.

Calculation of Input Tax credit

Particulars Amount

($)

Amount

($)

Total spending on advertisement and promotional activities 1,650,000

.00

GST input credit 100% eligible for: 1,100,000

.00

Portion of advertisement expenditures ineligible for input credit

in respect of GST

550,000.0

0

100% GST input credit 100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.0

0

7 Bird, Richard M., and Eric M. Zolt. "Redistribution via taxation: the limited role of the

personal income tax in developing countries." Annals of Economics and Finance 15, no. 2

(2014): 625-683.

TAXATION LAW

the intention of advertisement in order to promote Big Bank's various products and services,

which is even inclusive of GST.

Hence, as it has been discovered that the bank had spent $1,100,000 for the

promotional activities of their products and services from which the primary profit of the

bank is created and amounts to $550,000 will be regarded as capital expense as the newly

introduced product is yet to give out with respect to the income creation of the organization7.

Therefore, from the above explanation, it is pertinent that the amount computing to

$1,100,000 which the bank had to incur on the promotion of their existing services and

products that will be allowed to take input. Then again, the whole amount of $550,000 would

not be restricted to undertake input credit as 2% of such expenses towards the income

creation of the bank.

Calculation of Input Tax credit

Particulars Amount

($)

Amount

($)

Total spending on advertisement and promotional activities 1,650,000

.00

GST input credit 100% eligible for: 1,100,000

.00

Portion of advertisement expenditures ineligible for input credit

in respect of GST

550,000.0

0

100% GST input credit 100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.0

0

7 Bird, Richard M., and Eric M. Zolt. "Redistribution via taxation: the limited role of the

personal income tax in developing countries." Annals of Economics and Finance 15, no. 2

(2014): 625-683.

8

TAXATION LAW

Table 1: Input tax credit

(Source: Created by Author)

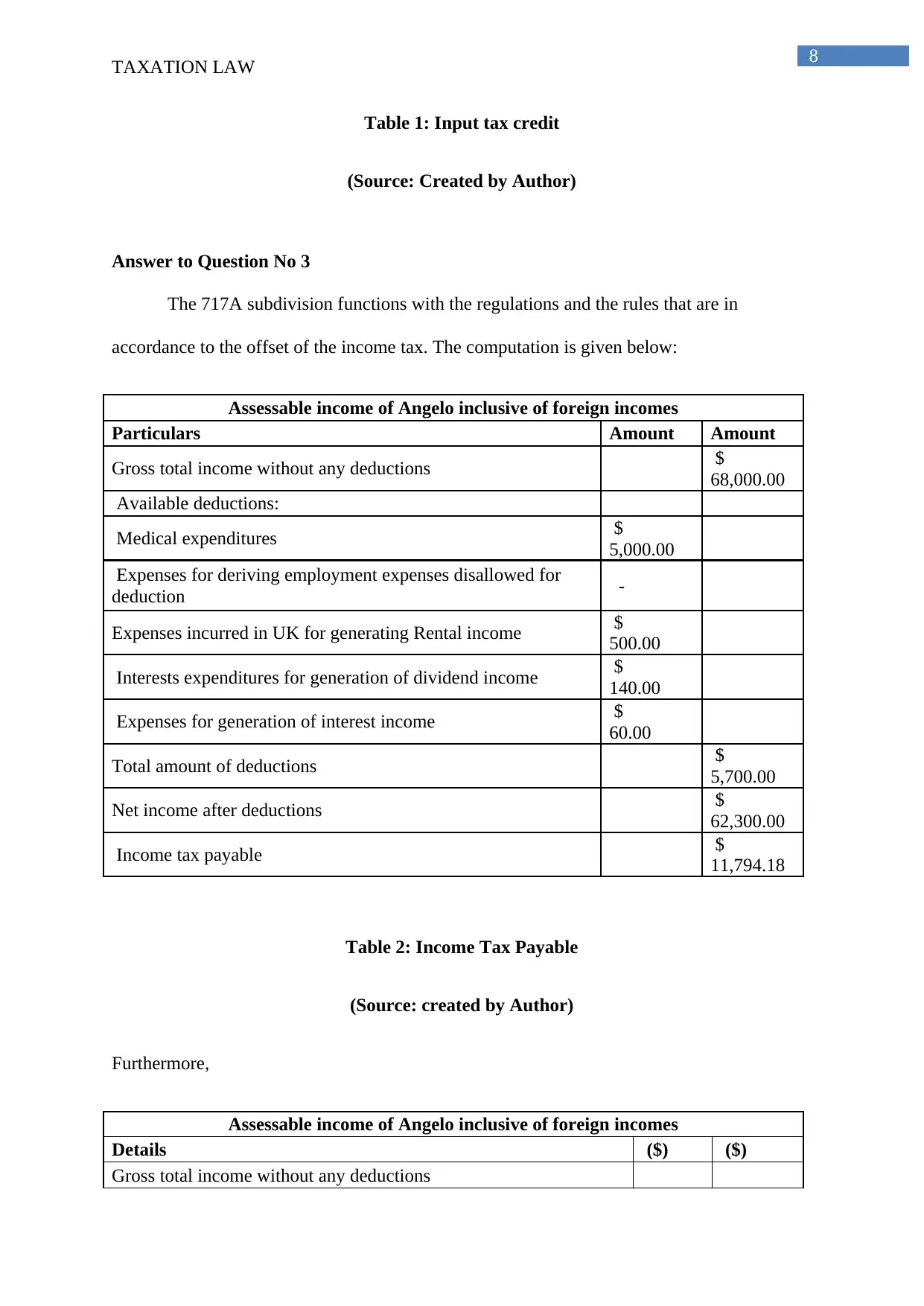

Answer to Question No 3

The 717A subdivision functions with the regulations and the rules that are in

accordance to the offset of the income tax. The computation is given below:

Assessable income of Angelo inclusive of foreign incomes

Particulars Amount Amount

Gross total income without any deductions $

68,000.00

Available deductions:

Medical expenditures $

5,000.00

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income $

500.00

Interests expenditures for generation of dividend income $

140.00

Expenses for generation of interest income $

60.00

Total amount of deductions $

5,700.00

Net income after deductions $

62,300.00

Income tax payable $

11,794.18

Table 2: Income Tax Payable

(Source: created by Author)

Furthermore,

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

TAXATION LAW

Table 1: Input tax credit

(Source: Created by Author)

Answer to Question No 3

The 717A subdivision functions with the regulations and the rules that are in

accordance to the offset of the income tax. The computation is given below:

Assessable income of Angelo inclusive of foreign incomes

Particulars Amount Amount

Gross total income without any deductions $

68,000.00

Available deductions:

Medical expenditures $

5,000.00

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income $

500.00

Interests expenditures for generation of dividend income $

140.00

Expenses for generation of interest income $

60.00

Total amount of deductions $

5,700.00

Net income after deductions $

62,300.00

Income tax payable $

11,794.18

Table 2: Income Tax Payable

(Source: created by Author)

Furthermore,

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION LAW

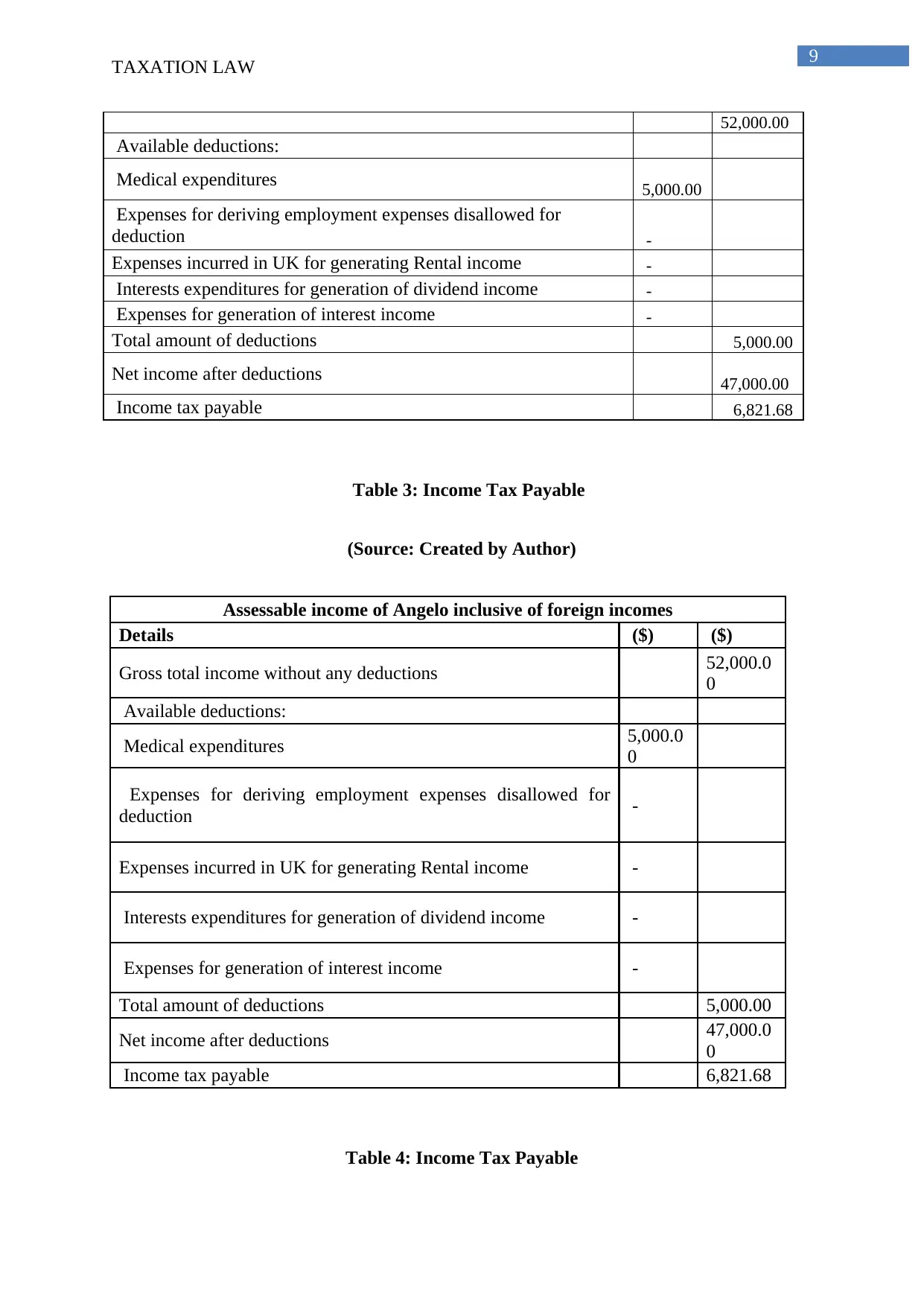

52,000.00

Available deductions:

Medical expenditures 5,000.00

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions 47,000.00

Income tax payable 6,821.68

Table 3: Income Tax Payable

(Source: Created by Author)

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions 52,000.0

0

Available deductions:

Medical expenditures 5,000.0

0

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions 47,000.0

0

Income tax payable 6,821.68

Table 4: Income Tax Payable

TAXATION LAW

52,000.00

Available deductions:

Medical expenditures 5,000.00

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions 47,000.00

Income tax payable 6,821.68

Table 3: Income Tax Payable

(Source: Created by Author)

Assessable income of Angelo inclusive of foreign incomes

Details ($) ($)

Gross total income without any deductions 52,000.0

0

Available deductions:

Medical expenditures 5,000.0

0

Expenses for deriving employment expenses disallowed for

deduction -

Expenses incurred in UK for generating Rental income -

Interests expenditures for generation of dividend income -

Expenses for generation of interest income -

Total amount of deductions 5,000.00

Net income after deductions 47,000.0

0

Income tax payable 6,821.68

Table 4: Income Tax Payable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

(Source: Created by Author)

The offset of the foreign tax is computed by subtracting the income tax amount that is

payable with respect to the first option from the income tax that can be paid from the second

option. Hence, the income tax limit has been (11794.18-6821.68) = $4972.50. It is observed

that the value of offset of the foreign tax is higher than amount paid for foreign tax. Hence,

the limit of foreign tax offset has been $4400.

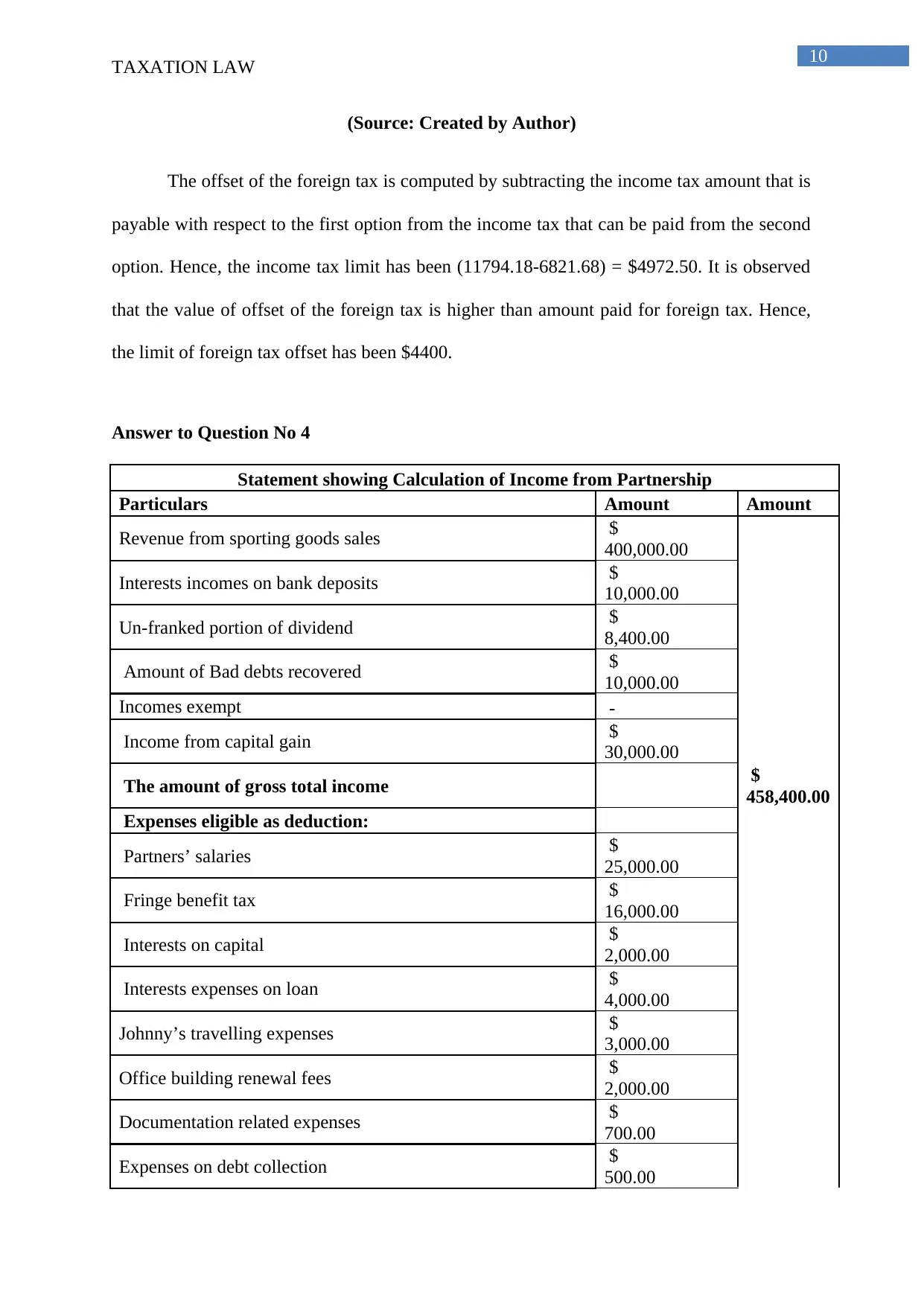

Answer to Question No 4

Statement showing Calculation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $

400,000.00

Interests incomes on bank deposits $

10,000.00

Un-franked portion of dividend $

8,400.00

Amount of Bad debts recovered $

10,000.00

Incomes exempt -

Income from capital gain $

30,000.00

The amount of gross total income $

458,400.00

Expenses eligible as deduction:

Partners’ salaries $

25,000.00

Fringe benefit tax $

16,000.00

Interests on capital $

2,000.00

Interests expenses on loan $

4,000.00

Johnny’s travelling expenses $

3,000.00

Office building renewal fees $

2,000.00

Documentation related expenses $

700.00

Expenses on debt collection $

500.00

TAXATION LAW

(Source: Created by Author)

The offset of the foreign tax is computed by subtracting the income tax amount that is

payable with respect to the first option from the income tax that can be paid from the second

option. Hence, the income tax limit has been (11794.18-6821.68) = $4972.50. It is observed

that the value of offset of the foreign tax is higher than amount paid for foreign tax. Hence,

the limit of foreign tax offset has been $4400.

Answer to Question No 4

Statement showing Calculation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $

400,000.00

Interests incomes on bank deposits $

10,000.00

Un-franked portion of dividend $

8,400.00

Amount of Bad debts recovered $

10,000.00

Incomes exempt -

Income from capital gain $

30,000.00

The amount of gross total income $

458,400.00

Expenses eligible as deduction:

Partners’ salaries $

25,000.00

Fringe benefit tax $

16,000.00

Interests on capital $

2,000.00

Interests expenses on loan $

4,000.00

Johnny’s travelling expenses $

3,000.00

Office building renewal fees $

2,000.00

Documentation related expenses $

700.00

Expenses on debt collection $

500.00

11

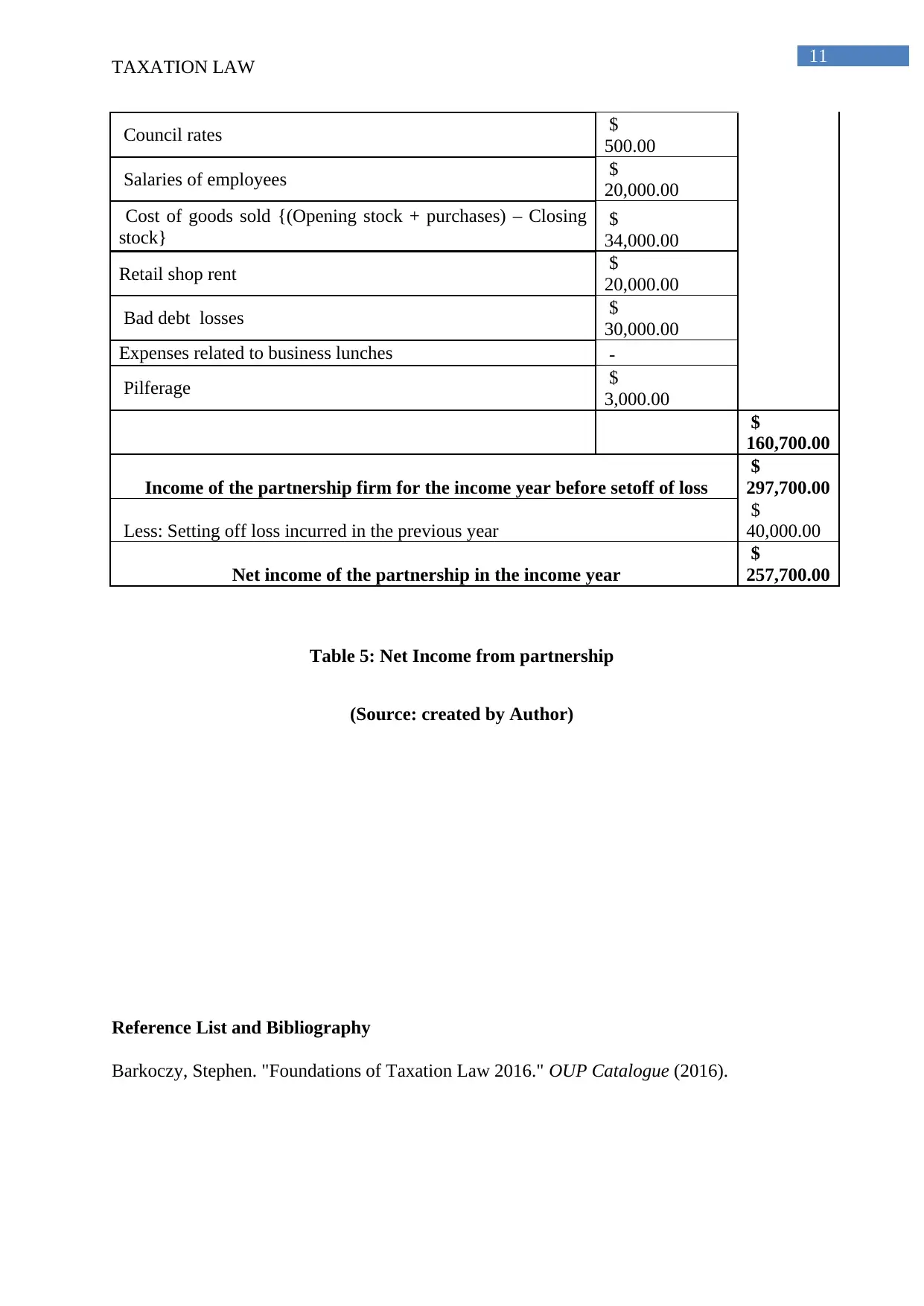

TAXATION LAW

Council rates $

500.00

Salaries of employees $

20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock} $

34,000.00

Retail shop rent $

20,000.00

Bad debt losses $

30,000.00

Expenses related to business lunches -

Pilferage $

3,000.00

$

160,700.00

Income of the partnership firm for the income year before setoff of loss

$

297,700.00

Less: Setting off loss incurred in the previous year

$

40,000.00

Net income of the partnership in the income year

$

257,700.00

Table 5: Net Income from partnership

(Source: created by Author)

Reference List and Bibliography

Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue (2016).

TAXATION LAW

Council rates $

500.00

Salaries of employees $

20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock} $

34,000.00

Retail shop rent $

20,000.00

Bad debt losses $

30,000.00

Expenses related to business lunches -

Pilferage $

3,000.00

$

160,700.00

Income of the partnership firm for the income year before setoff of loss

$

297,700.00

Less: Setting off loss incurred in the previous year

$

40,000.00

Net income of the partnership in the income year

$

257,700.00

Table 5: Net Income from partnership

(Source: created by Author)

Reference List and Bibliography

Barkoczy, Stephen. "Foundations of Taxation Law 2016." OUP Catalogue (2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.