Taxation Law Assignment: Analysis of Tax Laws, University Name

VerifiedAdded on 2019/10/31

|11

|1815

|283

Homework Assignment

AI Summary

This taxation law assignment provides detailed answers to five key questions. The first question addresses the issue of capital gains and losses, determining whether losses from personal use assets and collectibles can be offset against gains. The second question focuses on Fringe Benefit Tax (FBT) related to interest payments on loans. The third question examines partnership losses from rental properties and how they should be shared between partners. The fourth question discusses tax avoidance, referencing the IRC v Duke of Westminster case. Finally, the fifth question deals with assessable income derived from timber tending, considering whether the sale of timber constitutes assessable income under the ITAA 1997 and relevant tax rulings. The assignment solution provides a thorough analysis of each issue, citing relevant legislation, applications, and conclusions.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.........................................................................................................................................2

Legislation:.................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislations:...............................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Issue:..........................................................................................................................................7

Legislations:...............................................................................................................................7

Applications:..............................................................................................................................7

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.........................................................................................................................................2

Legislation:.................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Legislations:...............................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Legislation:.................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Issue:..........................................................................................................................................7

Legislations:...............................................................................................................................7

Applications:..............................................................................................................................7

2TAXATION LAW

Conclusion:................................................................................................................................8

Reference List:...........................................................................................................................9

Conclusion:................................................................................................................................8

Reference List:...........................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

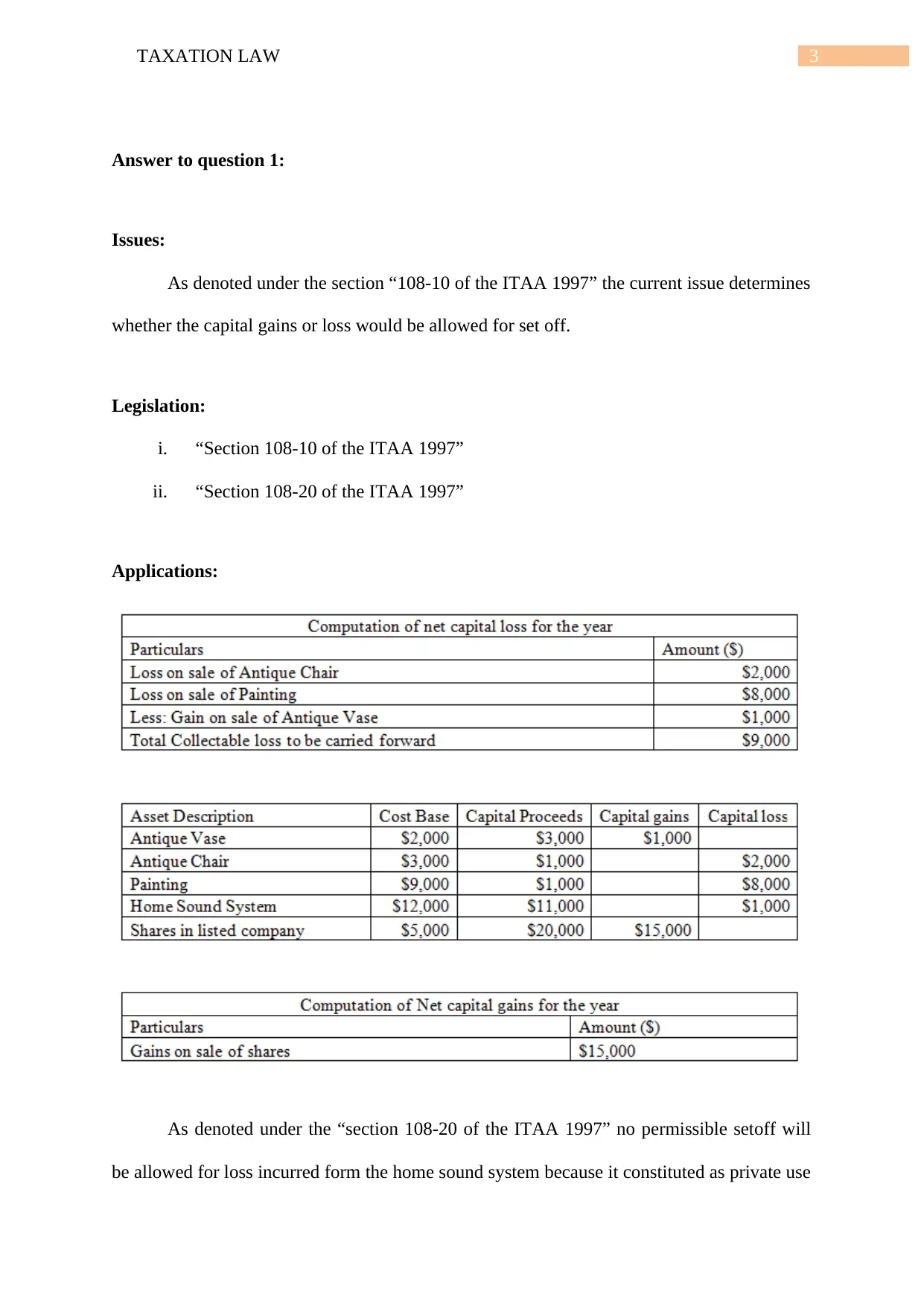

Answer to question 1:

Issues:

As denoted under the section “108-10 of the ITAA 1997” the current issue determines

whether the capital gains or loss would be allowed for set off.

Legislation:

i. “Section 108-10 of the ITAA 1997”

ii. “Section 108-20 of the ITAA 1997”

Applications:

As denoted under the “section 108-20 of the ITAA 1997” no permissible setoff will

be allowed for loss incurred form the home sound system because it constituted as private use

Answer to question 1:

Issues:

As denoted under the section “108-10 of the ITAA 1997” the current issue determines

whether the capital gains or loss would be allowed for set off.

Legislation:

i. “Section 108-10 of the ITAA 1997”

ii. “Section 108-20 of the ITAA 1997”

Applications:

As denoted under the “section 108-20 of the ITAA 1997” no permissible setoff will

be allowed for loss incurred form the home sound system because it constituted as private use

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

asset (Barkoczy et al. 2016). In compliance with the “section 108-10 of the ITAA” collectible

loss will not be allowed for set off against the gains that is made on sale of shares. Eric will

only be able to offset the collectibles against the gains that is derived under “section 108-10

of the ITAA 1997”.

Conclusion:

As denoted from the scenario Eric has will not be permitted to set off the loss for the

personal use asset and has derived gains from the disposal of ordinary assets.

Answer to question 2:

Issue:

The question deals about the determination of the FBT for payment of interest at the

end of the loan period.

Legislations:

i. “Taxation Ruling TR 93/6”

ii. “FBT Act 1986”

Applications:

Computation of Fringe Benefit Tax

asset (Barkoczy et al. 2016). In compliance with the “section 108-10 of the ITAA” collectible

loss will not be allowed for set off against the gains that is made on sale of shares. Eric will

only be able to offset the collectibles against the gains that is derived under “section 108-10

of the ITAA 1997”.

Conclusion:

As denoted from the scenario Eric has will not be permitted to set off the loss for the

personal use asset and has derived gains from the disposal of ordinary assets.

Answer to question 2:

Issue:

The question deals about the determination of the FBT for payment of interest at the

end of the loan period.

Legislations:

i. “Taxation Ruling TR 93/6”

ii. “FBT Act 1986”

Applications:

Computation of Fringe Benefit Tax

5TAXATION LAW

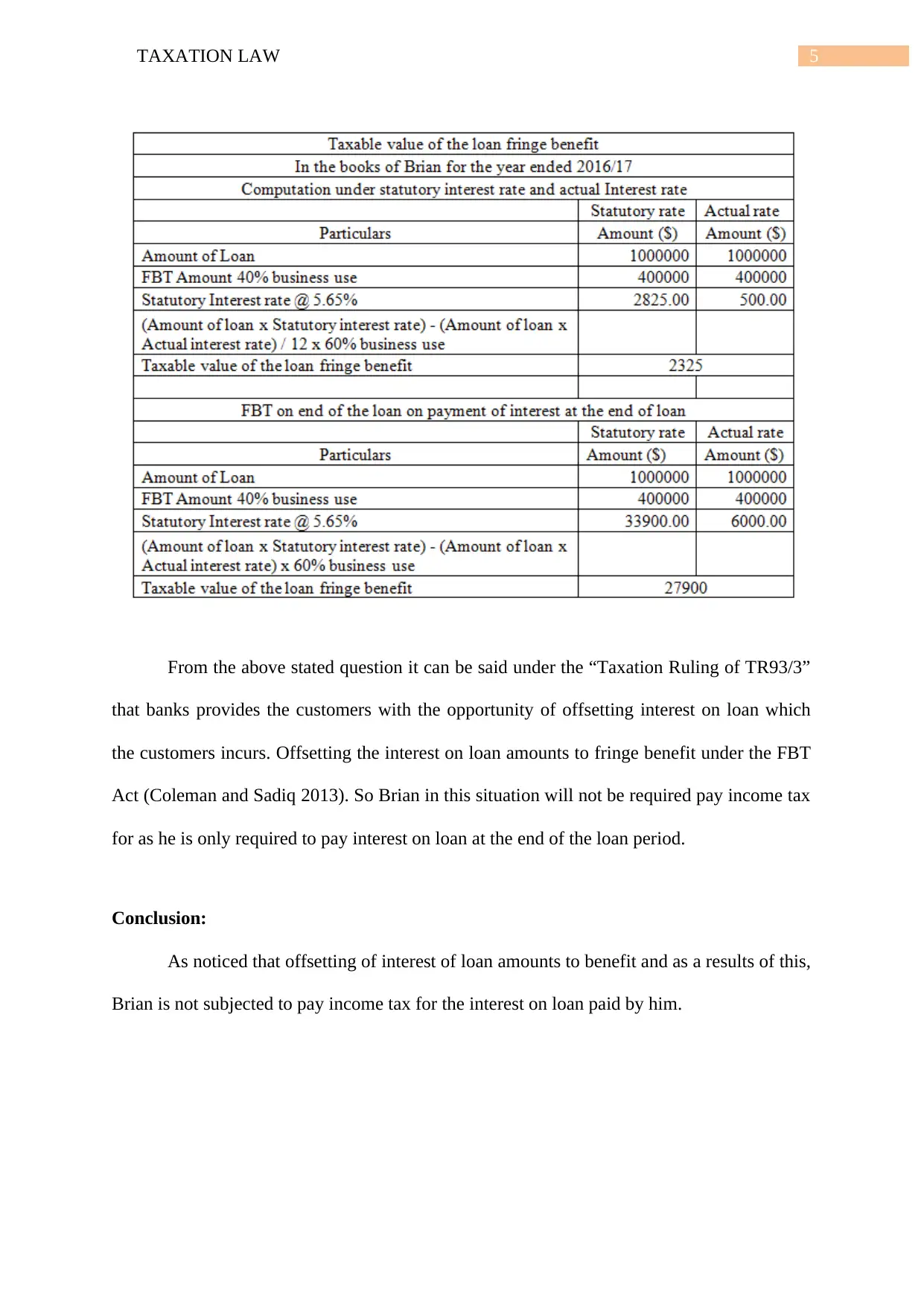

From the above stated question it can be said under the “Taxation Ruling of TR93/3”

that banks provides the customers with the opportunity of offsetting interest on loan which

the customers incurs. Offsetting the interest on loan amounts to fringe benefit under the FBT

Act (Coleman and Sadiq 2013). So Brian in this situation will not be required pay income tax

for as he is only required to pay interest on loan at the end of the loan period.

Conclusion:

As noticed that offsetting of interest of loan amounts to benefit and as a results of this,

Brian is not subjected to pay income tax for the interest on loan paid by him.

From the above stated question it can be said under the “Taxation Ruling of TR93/3”

that banks provides the customers with the opportunity of offsetting interest on loan which

the customers incurs. Offsetting the interest on loan amounts to fringe benefit under the FBT

Act (Coleman and Sadiq 2013). So Brian in this situation will not be required pay income tax

for as he is only required to pay interest on loan at the end of the loan period.

Conclusion:

As noticed that offsetting of interest of loan amounts to benefit and as a results of this,

Brian is not subjected to pay income tax for the interest on loan paid by him.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 3:

Issue:

This issue deals with the partnership loss from the rental property suffered by the taxpayer.

Legislation:

i. “FC of T v McDonald (1987)”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation Rulings of TR 93/23”

Application:

As noticed that Jack and Jill entered into a partnership of rental property where it was

stated that Jack will be getting 10% of the profit and Jill will be getting 90% of the profit

from the rental property. The partnership agreement between Jack and Jill contained that Jack

will have shoulder the entire amount of loss from the rental property. The “Taxation ruling

TR 93/23” gives explanation that co-ownership of rental property will be accounted for

income tax but will it is not a partnership under the general law (Harris et al. 2013).

Therefore, as per the explanation of the “Taxation Ruling of TR 92/32”, Jack and Jill being

husband and wife will not be considered partners under the General Law (Morgan, Mortimer

and Pinto 2013). This is because the joint-ownership of rental property between then do not

have any effect regarding the sharing of profit and loss. From the observation it is asserted

that joint ownership between Jack and Jill represents “joint owner or tenants in common”.

An argument can be put forward with reference to judgement of the court in case of

“FC of T v McDonald (1987)” where the Mr McDonald sought to advance the income of his

wife where he indemnified Mrs McDonald from any kind of loss (Nethercott et al. 2016). As

Answer to question 3:

Issue:

This issue deals with the partnership loss from the rental property suffered by the taxpayer.

Legislation:

i. “FC of T v McDonald (1987)”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation Rulings of TR 93/23”

Application:

As noticed that Jack and Jill entered into a partnership of rental property where it was

stated that Jack will be getting 10% of the profit and Jill will be getting 90% of the profit

from the rental property. The partnership agreement between Jack and Jill contained that Jack

will have shoulder the entire amount of loss from the rental property. The “Taxation ruling

TR 93/23” gives explanation that co-ownership of rental property will be accounted for

income tax but will it is not a partnership under the general law (Harris et al. 2013).

Therefore, as per the explanation of the “Taxation Ruling of TR 92/32”, Jack and Jill being

husband and wife will not be considered partners under the General Law (Morgan, Mortimer

and Pinto 2013). This is because the joint-ownership of rental property between then do not

have any effect regarding the sharing of profit and loss. From the observation it is asserted

that joint ownership between Jack and Jill represents “joint owner or tenants in common”.

An argument can be put forward with reference to judgement of the court in case of

“FC of T v McDonald (1987)” where the Mr McDonald sought to advance the income of his

wife where he indemnified Mrs McDonald from any kind of loss (Nethercott et al. 2016). As

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

observed from the situation of Jack and Jill it can be said the occurrence of loss must be

shared among them equally. As rightly put forward under section 51 that no losses can be

deducted by virtue of the contract created.

In contrary to the situation if Jack and Jill decides to sell the property then the cost

base and lowered amount of cost base of the rental property should be accounted in

determining the assessable income. Since Jack and Jill being the joint owners, any capital

gain or loss should be identified in harmony with the title of interest.

Conclusion:

As observed that Jack and Jill are not partners in terms of the general law and they

must share profit and loss equally in respect of the “section 51”.

Answer to question 4:

Arguably, IRC v Duke of Westminster (1936) is cited repeatedly whenever there

occurs a tax avoidance. The IRC v Duke of Westminster (1936) defines that every

individual has the right of ordering for their tax affairs and the tax assignment must be made

in such a way that taxes are lower than it would have actually been (Sadiq 2016). It can be

stated that the ruling of IRC v Duke of Westminster (1936) is regarded as the material of

appeal where it noticed that taxpayers have been avoiding tax by creating a complicated

structure. The court have followed more restrictive approach by citing the case of “WT

Ramsay v IRC”. The objective comprised of removing the false pre-arranged transactions by

imposing tax on business activities (Woellner et al. 2014).

On assigning the principles in the modern Australia, it can be defined that individual

taxpayers are allowed to structure their business agreements for the purpose of cutting their

tax liability. However this must be done within the purview of legal structure of the act.

observed from the situation of Jack and Jill it can be said the occurrence of loss must be

shared among them equally. As rightly put forward under section 51 that no losses can be

deducted by virtue of the contract created.

In contrary to the situation if Jack and Jill decides to sell the property then the cost

base and lowered amount of cost base of the rental property should be accounted in

determining the assessable income. Since Jack and Jill being the joint owners, any capital

gain or loss should be identified in harmony with the title of interest.

Conclusion:

As observed that Jack and Jill are not partners in terms of the general law and they

must share profit and loss equally in respect of the “section 51”.

Answer to question 4:

Arguably, IRC v Duke of Westminster (1936) is cited repeatedly whenever there

occurs a tax avoidance. The IRC v Duke of Westminster (1936) defines that every

individual has the right of ordering for their tax affairs and the tax assignment must be made

in such a way that taxes are lower than it would have actually been (Sadiq 2016). It can be

stated that the ruling of IRC v Duke of Westminster (1936) is regarded as the material of

appeal where it noticed that taxpayers have been avoiding tax by creating a complicated

structure. The court have followed more restrictive approach by citing the case of “WT

Ramsay v IRC”. The objective comprised of removing the false pre-arranged transactions by

imposing tax on business activities (Woellner et al. 2014).

On assigning the principles in the modern Australia, it can be defined that individual

taxpayers are allowed to structure their business agreements for the purpose of cutting their

tax liability. However this must be done within the purview of legal structure of the act.

8TAXATION LAW

Answer to question 5:

Issue:

The matter deals with assessable income derived from tending of timber in respect of

“section 6 (1) of the ITAA 1997” as primary producer.

Legislations:

a. “Taxation Rulings of TR 95/6”

b. “Section 6 (1) of the ITAA 1936”

c. “Subsection 36 (1)”

d. “Section 26 (f)”

e. “McCauley v FC of T (1944)”

Applications:

As observed that Bill has a large land where there are large number of pine trees. Bill

at first wanted to use the land for sheep grazing but latter accepted the offer of logging

company when the company made an offer of paying Bill $1000 for 100 meters of timber the

company can take from his land. As noticed in “Taxation Ruling of TR 95/6” selling of

timber is an assessable income barring from the fact that that a person is involved in the

forestry activity (Woellner et al. 2014). An individual will be treated as primary producer

under “Section 6 (1) of the ITAA 1936” for indulging in forestry activity. Arguably Bill is

regarded as primary producer under “section 6 (1) of the ITAA 1936” for engaging in tending

of pine trees in his own land and despite not planting the trees in his own land, selling of

timber would accounted as assessable income (Morgan, Mortimer and Pinto 2013). With

respect to “subsection 36 (1)” despite the fact that sale of timber was regarded as taxable

income, trees are viewed as fragment of business assets.

Answer to question 5:

Issue:

The matter deals with assessable income derived from tending of timber in respect of

“section 6 (1) of the ITAA 1997” as primary producer.

Legislations:

a. “Taxation Rulings of TR 95/6”

b. “Section 6 (1) of the ITAA 1936”

c. “Subsection 36 (1)”

d. “Section 26 (f)”

e. “McCauley v FC of T (1944)”

Applications:

As observed that Bill has a large land where there are large number of pine trees. Bill

at first wanted to use the land for sheep grazing but latter accepted the offer of logging

company when the company made an offer of paying Bill $1000 for 100 meters of timber the

company can take from his land. As noticed in “Taxation Ruling of TR 95/6” selling of

timber is an assessable income barring from the fact that that a person is involved in the

forestry activity (Woellner et al. 2014). An individual will be treated as primary producer

under “Section 6 (1) of the ITAA 1936” for indulging in forestry activity. Arguably Bill is

regarded as primary producer under “section 6 (1) of the ITAA 1936” for engaging in tending

of pine trees in his own land and despite not planting the trees in his own land, selling of

timber would accounted as assessable income (Morgan, Mortimer and Pinto 2013). With

respect to “subsection 36 (1)” despite the fact that sale of timber was regarded as taxable

income, trees are viewed as fragment of business assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

In contrary to the situation, if a lump sum of $50,000 is paid to Bill by grating the

right to the timber company to take as much as timber they want from his land then such

lump sum would be treated as royalties. As stated in “section 26 (f)” receipt of royalties by

selling timber from the land where the taxpayer is the owners is observed as assessable

income (Nethercott et al. 2016). This income is taxable during the year in which it is earned

from tending of timber. Denoting the judgment of court in “McCauley v FC of T (1944)” sum

received by granting the right of felling timber constitute royalties under “section 26 (f)”

(Coleman and Sadiq 2013). Henceforth, sum received from giving way the rights of cutting

timber characterises royalties and is taxable under “section 26 (f) of the ITAA 1997”.

Conclusion:

The discussion is concluded by defining that Bill attracts tax liability for selling

timber and the receipt of royalties would be assessable under section “26 (f) of the ITAA

1997”.

In contrary to the situation, if a lump sum of $50,000 is paid to Bill by grating the

right to the timber company to take as much as timber they want from his land then such

lump sum would be treated as royalties. As stated in “section 26 (f)” receipt of royalties by

selling timber from the land where the taxpayer is the owners is observed as assessable

income (Nethercott et al. 2016). This income is taxable during the year in which it is earned

from tending of timber. Denoting the judgment of court in “McCauley v FC of T (1944)” sum

received by granting the right of felling timber constitute royalties under “section 26 (f)”

(Coleman and Sadiq 2013). Henceforth, sum received from giving way the rights of cutting

timber characterises royalties and is taxable under “section 26 (f) of the ITAA 1997”.

Conclusion:

The discussion is concluded by defining that Bill attracts tax liability for selling

timber and the receipt of royalties would be assessable under section “26 (f) of the ITAA

1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G. (2016). Foundations Student Tax

Pack 3 2016. South Melbourne: Oxford University Press Australia & New Zealand.

Coleman, C. and Sadiq, K. (n.d.). Principles of taxation law 2013.

Harris, J., Graw, S., Gilders, F., Kenny, P. and Van der Waarden, N. (n.d.). 2013 Theory and

law in the regulation of business.

Morgan, A., Mortimer, C. and Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Nethercott, L., Devos, K., Gonzaga, L. and Richardson, G. (2016). Australian taxation study

manual. Melbourne: Oxford University Press.

Sadiq, K. (2016). Principles of Taxation Law 2016. Pyrmont: Law Book Co of Australasia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. (n.d.). 2014 Australian

taxation law.

Reference List:

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G. (2016). Foundations Student Tax

Pack 3 2016. South Melbourne: Oxford University Press Australia & New Zealand.

Coleman, C. and Sadiq, K. (n.d.). Principles of taxation law 2013.

Harris, J., Graw, S., Gilders, F., Kenny, P. and Van der Waarden, N. (n.d.). 2013 Theory and

law in the regulation of business.

Morgan, A., Mortimer, C. and Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Nethercott, L., Devos, K., Gonzaga, L. and Richardson, G. (2016). Australian taxation study

manual. Melbourne: Oxford University Press.

Sadiq, K. (2016). Principles of Taxation Law 2016. Pyrmont: Law Book Co of Australasia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. (n.d.). 2014 Australian

taxation law.

1 out of 11

Related Documents

![Taxation Law Analysis Assignment - [University Name]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2F237a5b831ee046ecb975c30288c0819d.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.