Taxation Law Utilization: GST Act and Big Bank Analysis

VerifiedAdded on 2020/03/23

|10

|663

|272

Homework Assignment

AI Summary

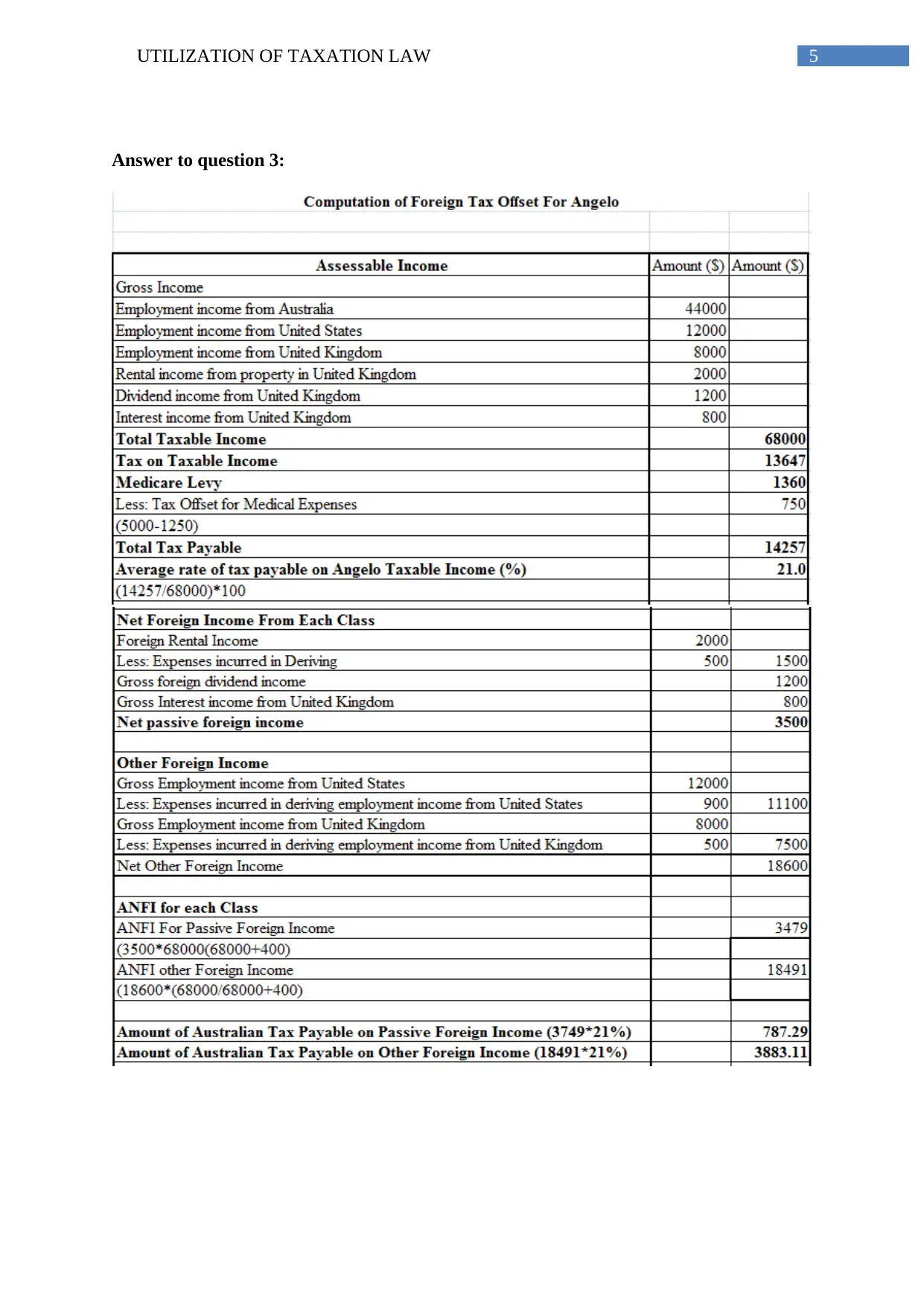

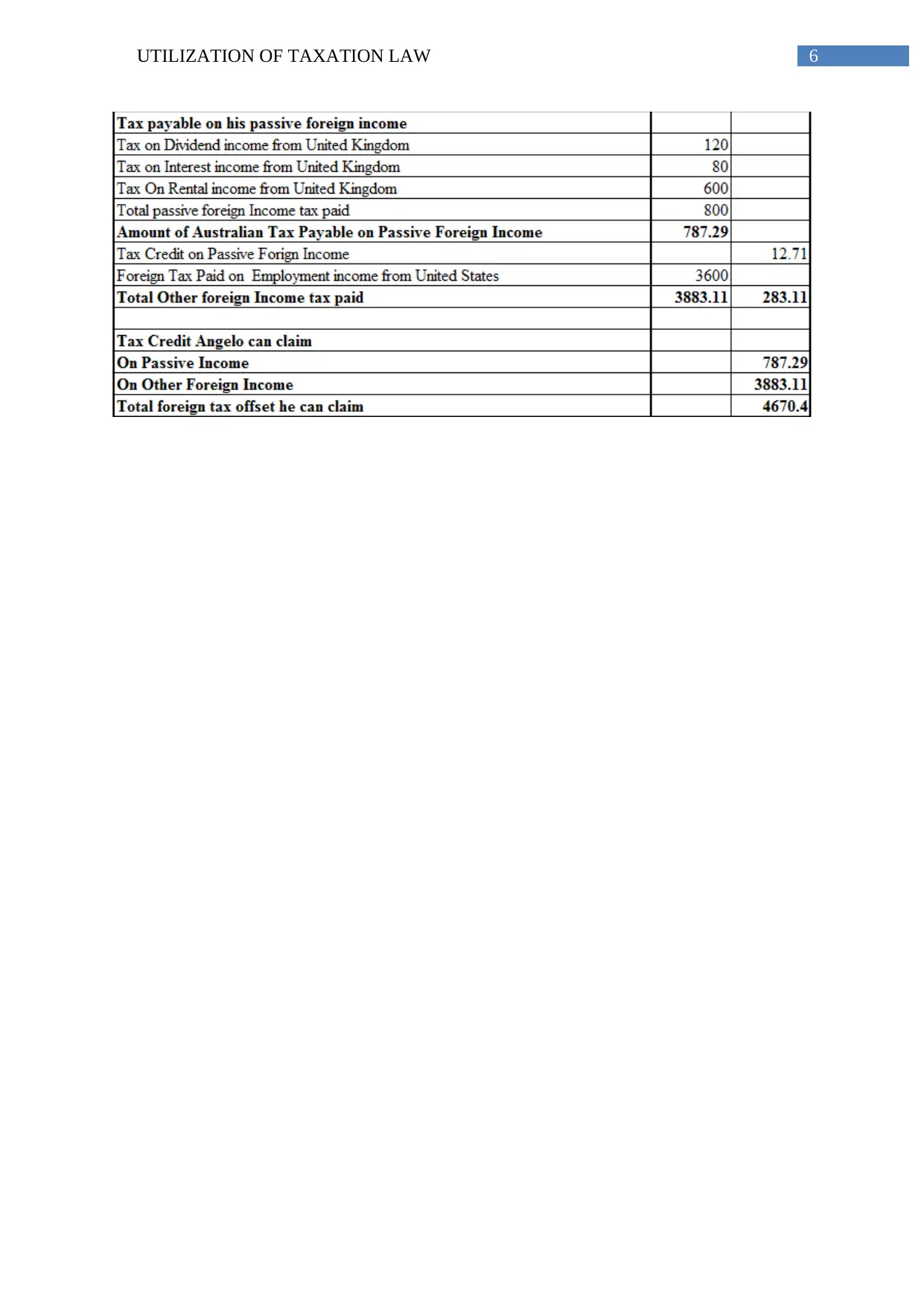

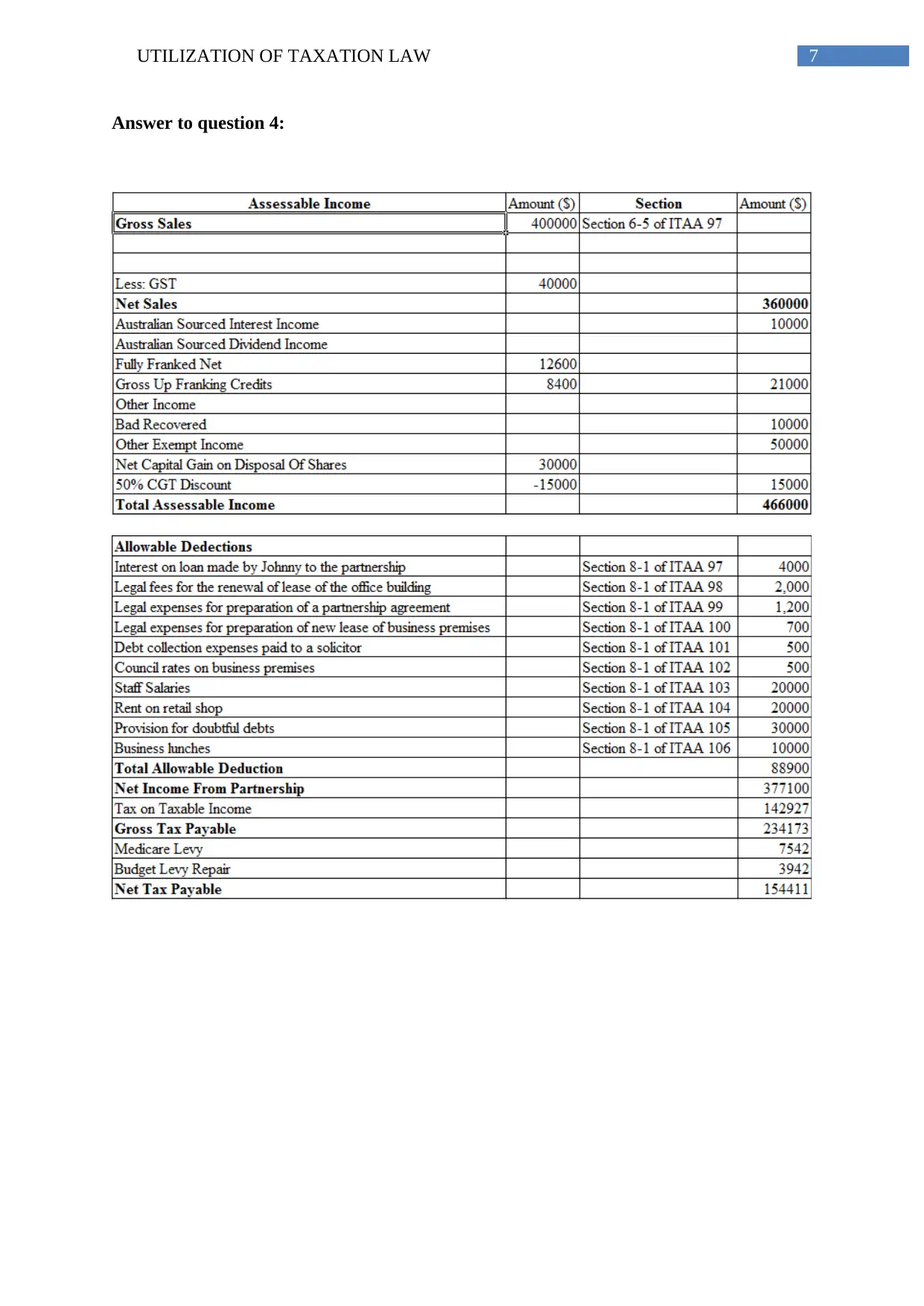

This assignment analyzes the application of taxation law, specifically focusing on the Goods and Services Tax (GST) Act 1999 and its implications for Big Bank Ltd. The assignment addresses the issue of input tax credit eligibility concerning advertising expenses incurred by the bank. It references relevant legal frameworks, including paragraphs 11-5 and 15-5, subsection 15-25, and the Goods and Service taxation ruling of GSTR 2006/3, along with the case of Ronpibon Tin NL v. FC of T. The analysis determines whether Big Bank Ltd is eligible to claim an input tax credit for the GST applied to its advertising expenditures, concluding that, based on the provided information and relevant legal precedents, the company is indeed eligible to claim the input tax credit. The assignment also includes references to legal databases and academic publications related to taxation law and GST.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.