Taxation Law Report: Income Tax, Deductions, Capital Gains, and Losses

VerifiedAdded on 2020/10/22

|10

|3038

|487

Report

AI Summary

This report provides an in-depth analysis of Australian taxation law, addressing key aspects such as income tax, deductions, and capital gains. It examines the tax treatment of lottery winnings, detailing whether these are taxable under personal income or subject to capital gains tax upon investment and sale. The report also includes a calculation of taxable income for a business, considering sales, purchases, and expenses to determine net profit or loss, and the implications for tax deductions. Furthermore, it explores the legal principle established in IRC v Duke of Westminster [1936] AC 1, discussing its relevance in the Australian context of tax avoidance and evasion. Finally, the report investigates the allocation of losses in a rental property scenario, outlining the rules for determining capital gains or losses upon sale, and how these are treated for tax purposes. The report concludes with a summary of key findings and implications of Australian taxation law.

TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determination of treatment of annual payment of annuity.........................................................1

QUESTION 2...................................................................................................................................2

Calculation of taxable income of Corner Pharmacy...................................................................2

QUESTION 3...................................................................................................................................3

Principle established in IRC v Duke of Westminster [1936] AC 1: and its relevancy in

Australia .....................................................................................................................................3

QUESTION 4...................................................................................................................................5

Treatment for allocation of losses and determination of capital gain/loss..................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determination of treatment of annual payment of annuity.........................................................1

QUESTION 2...................................................................................................................................2

Calculation of taxable income of Corner Pharmacy...................................................................2

QUESTION 3...................................................................................................................................3

Principle established in IRC v Duke of Westminster [1936] AC 1: and its relevancy in

Australia .....................................................................................................................................3

QUESTION 4...................................................................................................................................5

Treatment for allocation of losses and determination of capital gain/loss..................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

An important source of revenue for government of a country is from taxation income.

Tax in a nation is charged on sales of goods and services, income earned by individual citizens

and international business and trade transactions. For charging tax on income of individuals in

Australia act had been enacted and as per the provisions of that act incomes added and

deductions are made to ascertain total taxable income. In the present report taxation of incomes

from lotteries, deductions from income for tax purposes etc. are discussed. Along with this

principle established under IRC v Duke of Westminster [1936] AC 1 and its relevance in present

era in Australia is presented.

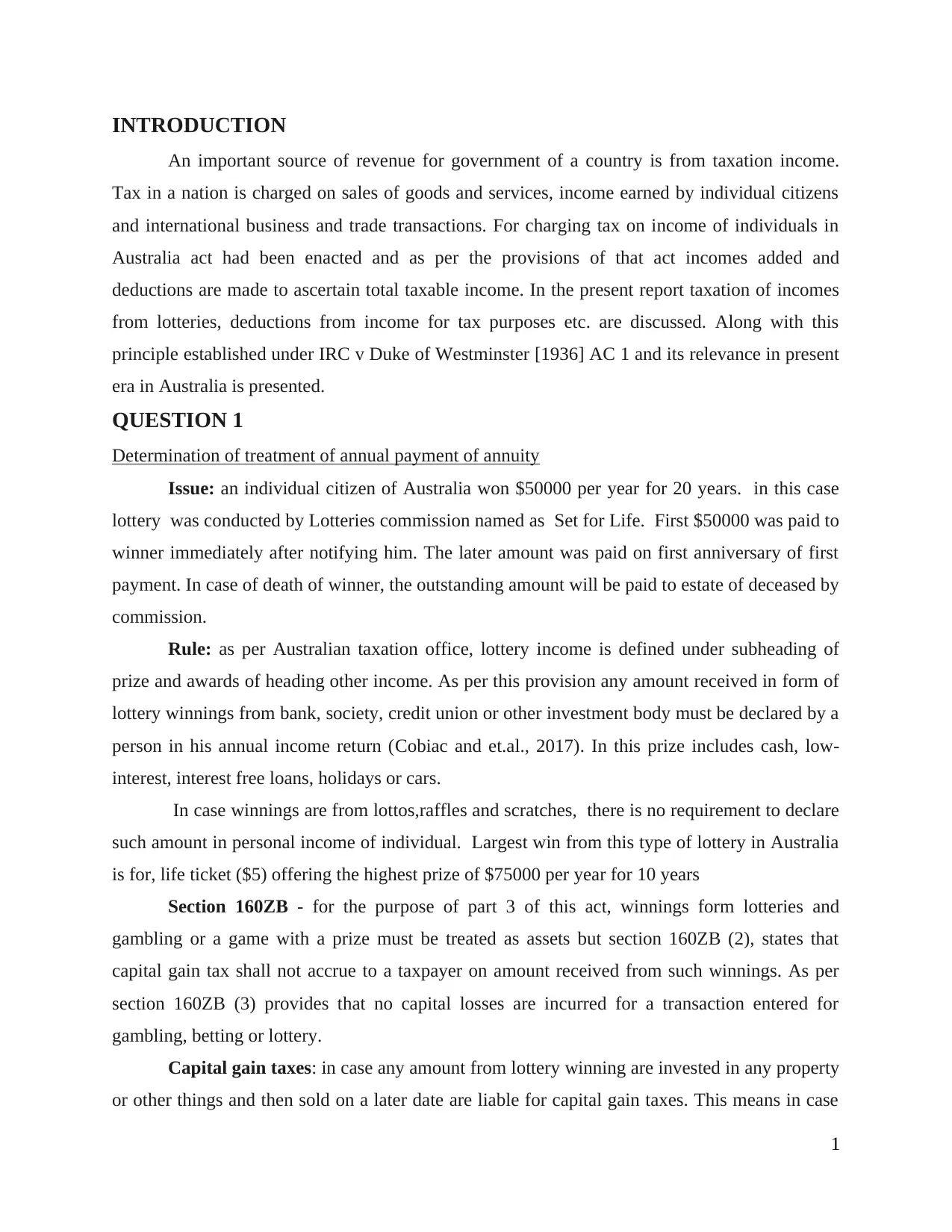

QUESTION 1

Determination of treatment of annual payment of annuity

Issue: an individual citizen of Australia won $50000 per year for 20 years. in this case

lottery was conducted by Lotteries commission named as Set for Life. First $50000 was paid to

winner immediately after notifying him. The later amount was paid on first anniversary of first

payment. In case of death of winner, the outstanding amount will be paid to estate of deceased by

commission.

Rule: as per Australian taxation office, lottery income is defined under subheading of

prize and awards of heading other income. As per this provision any amount received in form of

lottery winnings from bank, society, credit union or other investment body must be declared by a

person in his annual income return (Cobiac and et.al., 2017). In this prize includes cash, low-

interest, interest free loans, holidays or cars.

In case winnings are from lottos,raffles and scratches, there is no requirement to declare

such amount in personal income of individual. Largest win from this type of lottery in Australia

is for, life ticket ($5) offering the highest prize of $75000 per year for 10 years

Section 160ZB - for the purpose of part 3 of this act, winnings form lotteries and

gambling or a game with a prize must be treated as assets but section 160ZB (2), states that

capital gain tax shall not accrue to a taxpayer on amount received from such winnings. As per

section 160ZB (3) provides that no capital losses are incurred for a transaction entered for

gambling, betting or lottery.

Capital gain taxes: in case any amount from lottery winning are invested in any property

or other things and then sold on a later date are liable for capital gain taxes. This means in case

1

An important source of revenue for government of a country is from taxation income.

Tax in a nation is charged on sales of goods and services, income earned by individual citizens

and international business and trade transactions. For charging tax on income of individuals in

Australia act had been enacted and as per the provisions of that act incomes added and

deductions are made to ascertain total taxable income. In the present report taxation of incomes

from lotteries, deductions from income for tax purposes etc. are discussed. Along with this

principle established under IRC v Duke of Westminster [1936] AC 1 and its relevance in present

era in Australia is presented.

QUESTION 1

Determination of treatment of annual payment of annuity

Issue: an individual citizen of Australia won $50000 per year for 20 years. in this case

lottery was conducted by Lotteries commission named as Set for Life. First $50000 was paid to

winner immediately after notifying him. The later amount was paid on first anniversary of first

payment. In case of death of winner, the outstanding amount will be paid to estate of deceased by

commission.

Rule: as per Australian taxation office, lottery income is defined under subheading of

prize and awards of heading other income. As per this provision any amount received in form of

lottery winnings from bank, society, credit union or other investment body must be declared by a

person in his annual income return (Cobiac and et.al., 2017). In this prize includes cash, low-

interest, interest free loans, holidays or cars.

In case winnings are from lottos,raffles and scratches, there is no requirement to declare

such amount in personal income of individual. Largest win from this type of lottery in Australia

is for, life ticket ($5) offering the highest prize of $75000 per year for 10 years

Section 160ZB - for the purpose of part 3 of this act, winnings form lotteries and

gambling or a game with a prize must be treated as assets but section 160ZB (2), states that

capital gain tax shall not accrue to a taxpayer on amount received from such winnings. As per

section 160ZB (3) provides that no capital losses are incurred for a transaction entered for

gambling, betting or lottery.

Capital gain taxes: in case any amount from lottery winning are invested in any property

or other things and then sold on a later date are liable for capital gain taxes. This means in case

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

some amount of lottery winning is invested in a purchase of a property, and is sold after few

years then gain on sale of such possessions is taxable under capital gain tax with a concessional

rate. For winnings from lotteries, 50% deduction of tax amount is given.

Taxation on Amount transferred to estate of deceased: as per Australian taxation

office, deceased estate of a person that on one is nominated as his/her legal heirs (McGee,

Devos and Benk, 2016). In such cases lottery winnings are submitted in estate of deceased

person and then distributed among legal inheritor as per the law by relevant authorities. There is

no inheritance or estate tax in Australia.

Application: with application of above section 160ZB (2) it can be stated that $50000

earned by a person is entirely non-taxable. Neither amount received in first year nor subsequent

amount are taxable. In case amount recorded in books is more than received from lottery, then

per section 160ZB (3). individual have not suffered any capital losses

Conclusion: in Australia, lottery winnings are not subject to taxation under personal

income. This can be concluded $50000 received for first time and then earned subsequently for

20 years is not chargeable to tax and cannot be treated as personal income of individual. In case

person who won the lottery dies remaining amount is transferred to his estate and that amount is

also not chargeable to tax as per taxation law of Australia.

QUESTION 2

Calculation of taxable income of Corner Pharmacy

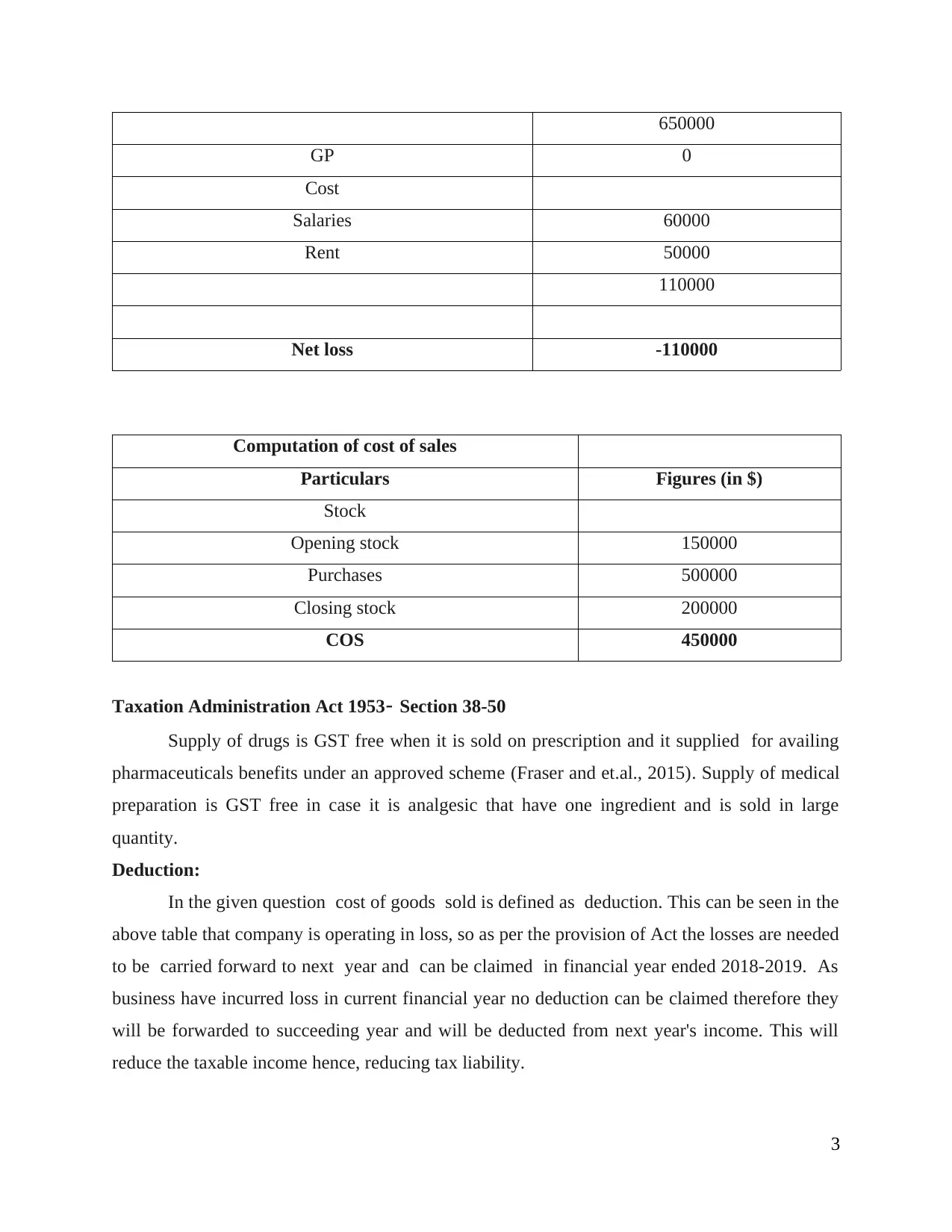

Particulars Figures (in $)

Total Sales

Cash Sales 300000

Credit Card Sales 150000

450000

Closing Stock 200000

650000

Less:

opening stock 150000

Purchases 500000

2

years then gain on sale of such possessions is taxable under capital gain tax with a concessional

rate. For winnings from lotteries, 50% deduction of tax amount is given.

Taxation on Amount transferred to estate of deceased: as per Australian taxation

office, deceased estate of a person that on one is nominated as his/her legal heirs (McGee,

Devos and Benk, 2016). In such cases lottery winnings are submitted in estate of deceased

person and then distributed among legal inheritor as per the law by relevant authorities. There is

no inheritance or estate tax in Australia.

Application: with application of above section 160ZB (2) it can be stated that $50000

earned by a person is entirely non-taxable. Neither amount received in first year nor subsequent

amount are taxable. In case amount recorded in books is more than received from lottery, then

per section 160ZB (3). individual have not suffered any capital losses

Conclusion: in Australia, lottery winnings are not subject to taxation under personal

income. This can be concluded $50000 received for first time and then earned subsequently for

20 years is not chargeable to tax and cannot be treated as personal income of individual. In case

person who won the lottery dies remaining amount is transferred to his estate and that amount is

also not chargeable to tax as per taxation law of Australia.

QUESTION 2

Calculation of taxable income of Corner Pharmacy

Particulars Figures (in $)

Total Sales

Cash Sales 300000

Credit Card Sales 150000

450000

Closing Stock 200000

650000

Less:

opening stock 150000

Purchases 500000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

650000

GP 0

Cost

Salaries 60000

Rent 50000

110000

Net loss -110000

Computation of cost of sales

Particulars Figures (in $)

Stock

Opening stock 150000

Purchases 500000

Closing stock 200000

COS 450000

Taxation Administration Act 1953- Section 38-50

Supply of drugs is GST free when it is sold on prescription and it supplied for availing

pharmaceuticals benefits under an approved scheme (Fraser and et.al., 2015). Supply of medical

preparation is GST free in case it is analgesic that have one ingredient and is sold in large

quantity.

Deduction:

In the given question cost of goods sold is defined as deduction. This can be seen in the

above table that company is operating in loss, so as per the provision of Act the losses are needed

to be carried forward to next year and can be claimed in financial year ended 2018-2019. As

business have incurred loss in current financial year no deduction can be claimed therefore they

will be forwarded to succeeding year and will be deducted from next year's income. This will

reduce the taxable income hence, reducing tax liability.

3

GP 0

Cost

Salaries 60000

Rent 50000

110000

Net loss -110000

Computation of cost of sales

Particulars Figures (in $)

Stock

Opening stock 150000

Purchases 500000

Closing stock 200000

COS 450000

Taxation Administration Act 1953- Section 38-50

Supply of drugs is GST free when it is sold on prescription and it supplied for availing

pharmaceuticals benefits under an approved scheme (Fraser and et.al., 2015). Supply of medical

preparation is GST free in case it is analgesic that have one ingredient and is sold in large

quantity.

Deduction:

In the given question cost of goods sold is defined as deduction. This can be seen in the

above table that company is operating in loss, so as per the provision of Act the losses are needed

to be carried forward to next year and can be claimed in financial year ended 2018-2019. As

business have incurred loss in current financial year no deduction can be claimed therefore they

will be forwarded to succeeding year and will be deducted from next year's income. This will

reduce the taxable income hence, reducing tax liability.

3

QUESTION 3

Principle established in IRC v Duke of Westminster [1936] AC 1: and its relevancy in Australia

IRC v Duke of Westminster [1936] AC 1:

In this case Duke who lived in Westminster paid his gardener on week basis and then he

enters in an agreement with him and stopped paying wages and agreed on a condition to pay him

lump sum amount:.

The principle which was given in this case was by Lord Tomin,

Principle of tax avoidance:

According to him, “every person who arranges his income and taxation matter in such a

way and in accordance with suitable law acts which attract less tax liability, he is entitled to the

same (Saad, 2014). If the person gets success in getting an order from the court which held this

act correct and secures the result under justice law, then he cannot be compelled to pay increased

tax. The inappreciativeness of Indian revenue commissioner or fellow taxpayer about

genuineness of act of the person does not matter.”

It was held that action of Duke was right and his contention was correct as he had done it

under tax planning. Grander was still getting the payment but duke gained benefit of tax as the

decision passed at that time reduced his tax liability of surtax.

This was a clear case of tax avoidance but was granted decision under act of tax planning. So this

was seen in this case that tax avoidance was given a green signal and duke had to pay less

surcharges on payment of wages to his gardener.

Relevancy of principle of tax avoidance in Australia:

With time principles and rules in this field have been evolved and in present time there is

a whole new legislation that governs tax avoidance and principle rules out in case of duke has

faded away. The Australian taxation office have developed tax avoidance schemes to eliminate

and protect tax evasion.

The principle laid down in case of duke v IRC cannot be held to correct. with time rules

have been changed. this principle cannot be applied and referred to and used by people to hold

their action of tax avoidance, as correct. This ruling in case was held by supreme court due to

contention and thoughts of judge Tomine thought the decree passed in lower court was not

legally correct.

4

Principle established in IRC v Duke of Westminster [1936] AC 1: and its relevancy in Australia

IRC v Duke of Westminster [1936] AC 1:

In this case Duke who lived in Westminster paid his gardener on week basis and then he

enters in an agreement with him and stopped paying wages and agreed on a condition to pay him

lump sum amount:.

The principle which was given in this case was by Lord Tomin,

Principle of tax avoidance:

According to him, “every person who arranges his income and taxation matter in such a

way and in accordance with suitable law acts which attract less tax liability, he is entitled to the

same (Saad, 2014). If the person gets success in getting an order from the court which held this

act correct and secures the result under justice law, then he cannot be compelled to pay increased

tax. The inappreciativeness of Indian revenue commissioner or fellow taxpayer about

genuineness of act of the person does not matter.”

It was held that action of Duke was right and his contention was correct as he had done it

under tax planning. Grander was still getting the payment but duke gained benefit of tax as the

decision passed at that time reduced his tax liability of surtax.

This was a clear case of tax avoidance but was granted decision under act of tax planning. So this

was seen in this case that tax avoidance was given a green signal and duke had to pay less

surcharges on payment of wages to his gardener.

Relevancy of principle of tax avoidance in Australia:

With time principles and rules in this field have been evolved and in present time there is

a whole new legislation that governs tax avoidance and principle rules out in case of duke has

faded away. The Australian taxation office have developed tax avoidance schemes to eliminate

and protect tax evasion.

The principle laid down in case of duke v IRC cannot be held to correct. with time rules

have been changed. this principle cannot be applied and referred to and used by people to hold

their action of tax avoidance, as correct. This ruling in case was held by supreme court due to

contention and thoughts of judge Tomine thought the decree passed in lower court was not

legally correct.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The principles stated in tax avoidance scheme are as under: Each year, tax system has been

made promoted to be more aggressive to taxpayers and these arrangements are:

reducing taxable income of an individual

increase in deduction against income

to entirely eliminate tax avoidance

The transaction in tax avoidance are recognised in wrong or different category which can be

classified as:

wrong classification of revenues as capital

incorrect use of concessional tax rates

illegal release of funds before maturity to avoid tax liability

to trigger movement of fund through many entities to minimise tax payable

In Australia no one can refer ruling passed in this case to make their contention of tax

evasion right, as this is act which is considered illegal and unlawful according to Australian

taxation office.

With this it can be concluded that principle established in case of IRC v Duke do not

have much relevance in present times as in that case the act of Duke was of tax avoidance which

was declared as tax planning through order of court. Further it can be interpreted that in this era

tax avoidance is treated as unlawful and illegal act on behalf of a tax payer. With proper planning

a tax payee can plan out his taxable income and claim deductions which is relevant and true to

their facts. An act in which a person tries to avoid tax through illegal and incorrect classification

of transactions and multiple transfers of income is considered as tax avoidance/evasion.

QUESTION 4

Treatment for allocation of losses and determination of capital gain/loss

Issue: this is a case rated with a couple Joseph who is an accountant and his wife Jane

who is a housewife. A sum is borrowed by both of them to buy a rental property as joint tenants.

For this a written agreement was executed between both of them and it was agreed that profits

will be shared as 80% by wife and 20% by husband. In case any losses are incurred will be

suffered 100% by Joseph only. Now, a situation arises that a loss of $40000 was incurred in last

year from that property.

5

made promoted to be more aggressive to taxpayers and these arrangements are:

reducing taxable income of an individual

increase in deduction against income

to entirely eliminate tax avoidance

The transaction in tax avoidance are recognised in wrong or different category which can be

classified as:

wrong classification of revenues as capital

incorrect use of concessional tax rates

illegal release of funds before maturity to avoid tax liability

to trigger movement of fund through many entities to minimise tax payable

In Australia no one can refer ruling passed in this case to make their contention of tax

evasion right, as this is act which is considered illegal and unlawful according to Australian

taxation office.

With this it can be concluded that principle established in case of IRC v Duke do not

have much relevance in present times as in that case the act of Duke was of tax avoidance which

was declared as tax planning through order of court. Further it can be interpreted that in this era

tax avoidance is treated as unlawful and illegal act on behalf of a tax payer. With proper planning

a tax payee can plan out his taxable income and claim deductions which is relevant and true to

their facts. An act in which a person tries to avoid tax through illegal and incorrect classification

of transactions and multiple transfers of income is considered as tax avoidance/evasion.

QUESTION 4

Treatment for allocation of losses and determination of capital gain/loss

Issue: this is a case rated with a couple Joseph who is an accountant and his wife Jane

who is a housewife. A sum is borrowed by both of them to buy a rental property as joint tenants.

For this a written agreement was executed between both of them and it was agreed that profits

will be shared as 80% by wife and 20% by husband. In case any losses are incurred will be

suffered 100% by Joseph only. Now, a situation arises that a loss of $40000 was incurred in last

year from that property.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rule:

Residential rental property:

In case investment in rental property is done, one must keep all records right from the

starting of such tenancy. All expenses which can be claimed as deductions and which cannot

must be determined and rental income must be declared in the individual tax return. In case of

income from such rental property, will be reflected in personal income of individual (Evans,

Minas and Lim, 2015).

Deduction which can be claimed:

fees for management of real estate

advertisement for tenancy

insurance

interest on loan taken for such rental property

depreciation on assets on that property

Deduction which cannot be claimed:

expenses incurred for personal use of rental property

bill paid for utilities by tenant

cost incurred for purchase or sale of such rental house

borrowing costs

Allocation of loss for purpose of taxation:

Losses incurred on rental property are treated as capital losses and set off from the capital

gains earned which can be accumulated, of same year or in case there is no increase such loss

will be carried forward till such property is disposed.

Capital gain of losses on sale of rental property:

Capital gain or capital loss can be defined as difference between what is the cost incurred

on possessing and improving the property (cost base) and what is received when rental holding is

sold. The amount which are claimed as deduction are not included in cost of acquisition or cost

base. While determination of capital gain or loss, specified capital expenses are included in the

cost base such as expenses done for title search, conveyancing to - from property, valuation fees

and stamp duty (Residence, 2018). This inclusion of expenses in cost will reduce the amount of

capital gain and hence decreasing amount in capital tax gain payable on sale of rental property.

Cost base of rental property:

6

Residential rental property:

In case investment in rental property is done, one must keep all records right from the

starting of such tenancy. All expenses which can be claimed as deductions and which cannot

must be determined and rental income must be declared in the individual tax return. In case of

income from such rental property, will be reflected in personal income of individual (Evans,

Minas and Lim, 2015).

Deduction which can be claimed:

fees for management of real estate

advertisement for tenancy

insurance

interest on loan taken for such rental property

depreciation on assets on that property

Deduction which cannot be claimed:

expenses incurred for personal use of rental property

bill paid for utilities by tenant

cost incurred for purchase or sale of such rental house

borrowing costs

Allocation of loss for purpose of taxation:

Losses incurred on rental property are treated as capital losses and set off from the capital

gains earned which can be accumulated, of same year or in case there is no increase such loss

will be carried forward till such property is disposed.

Capital gain of losses on sale of rental property:

Capital gain or capital loss can be defined as difference between what is the cost incurred

on possessing and improving the property (cost base) and what is received when rental holding is

sold. The amount which are claimed as deduction are not included in cost of acquisition or cost

base. While determination of capital gain or loss, specified capital expenses are included in the

cost base such as expenses done for title search, conveyancing to - from property, valuation fees

and stamp duty (Residence, 2018). This inclusion of expenses in cost will reduce the amount of

capital gain and hence decreasing amount in capital tax gain payable on sale of rental property.

Cost base of rental property:

6

This is sum of purchase cost of property along with expenditure associated with holding

and sale of such property (Information on residency for tax purposes, 2018). This includes

stamp duty, fees to brokers, loan application charges, legal expenses and capital improvement

outlays. In case property is held after 19th September 1985 and owned for more than 12 months’

capital gain taxes are subject to a deduction of 50%.

Assumption:

In this case it is not clearly mentioned about the sources of loss of $40000 in previous

year. It is assumed that losses are not form difference between income and expense of rental

house. As in the second part of question it is clearly mentioned that 'if property is sold', but

amount is huge so loss of $40000 is considered as capital loss for this case. It is assumed house is

purchased after 19th September 1985, and held in possession for more than 12 months.

Application:

In this case losses for previous year can be defied as; a difference of rental income for

the whole previous year i.e. nil and expenses incurred on property in form of maintenance and

partial repayment of borrowed money for house. The expenses also include interested amount

paid on such borrowings. As in given case study loss of $40000 was incurred in previous year,

which is treated as capital loss, will be set off against accumulated profits for that period of time.

Nothing is mentioned about gains in previous year, hence losses will be carried forward to next

year.

Conclusion:

Sale of house at profit: in case rental house is sold at a price which is more than cost

base that will be considered as capital gain. The selling price of house must be more than cost of

acquisition and expenses incurred for taking possession and maintenance of rental house. In this

case capital-losses of previous year will be set off against capital gain of this period arises on

sale of property and are liable for a 50 % deduction for capital gain taxation.

Sale of house for loss: in case, sales price of property is less than the cost of acquisition

then it is a situation of capital loss. In this present scenario, no tax is payable as there are no

losses, hence no tax ability. Accumulate losses will increase as current years’ losses and

previous year losses of $40000 will be added up.

7

and sale of such property (Information on residency for tax purposes, 2018). This includes

stamp duty, fees to brokers, loan application charges, legal expenses and capital improvement

outlays. In case property is held after 19th September 1985 and owned for more than 12 months’

capital gain taxes are subject to a deduction of 50%.

Assumption:

In this case it is not clearly mentioned about the sources of loss of $40000 in previous

year. It is assumed that losses are not form difference between income and expense of rental

house. As in the second part of question it is clearly mentioned that 'if property is sold', but

amount is huge so loss of $40000 is considered as capital loss for this case. It is assumed house is

purchased after 19th September 1985, and held in possession for more than 12 months.

Application:

In this case losses for previous year can be defied as; a difference of rental income for

the whole previous year i.e. nil and expenses incurred on property in form of maintenance and

partial repayment of borrowed money for house. The expenses also include interested amount

paid on such borrowings. As in given case study loss of $40000 was incurred in previous year,

which is treated as capital loss, will be set off against accumulated profits for that period of time.

Nothing is mentioned about gains in previous year, hence losses will be carried forward to next

year.

Conclusion:

Sale of house at profit: in case rental house is sold at a price which is more than cost

base that will be considered as capital gain. The selling price of house must be more than cost of

acquisition and expenses incurred for taking possession and maintenance of rental house. In this

case capital-losses of previous year will be set off against capital gain of this period arises on

sale of property and are liable for a 50 % deduction for capital gain taxation.

Sale of house for loss: in case, sales price of property is less than the cost of acquisition

then it is a situation of capital loss. In this present scenario, no tax is payable as there are no

losses, hence no tax ability. Accumulate losses will increase as current years’ losses and

previous year losses of $40000 will be added up.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

From the above report. it can be concluded that lottery winning in Australia are not

chargeable to tax. The amount won by a person from lottery is not included in his/her personal

income. Further, it is also analysed that on such income there is no capital gain or loss, hence on

taxation in this respect as well. Taxable income of Corner pharmacy is calculated on accrual

basis. Ruling passed in law suit of IRC v Duke held tax avoidance right, but with time this

principle lost its legal validity. For case of Joseph and Jane it can be concluded that previous year

financial loss are capital losses. In case house was sold at a price more than cost of acquisition

there is capital gain from which capital losses was deducted and balance is charged against

capital gain tax. In case its sale at loss, accumulated capital loss amount would increase.

8

From the above report. it can be concluded that lottery winning in Australia are not

chargeable to tax. The amount won by a person from lottery is not included in his/her personal

income. Further, it is also analysed that on such income there is no capital gain or loss, hence on

taxation in this respect as well. Taxable income of Corner pharmacy is calculated on accrual

basis. Ruling passed in law suit of IRC v Duke held tax avoidance right, but with time this

principle lost its legal validity. For case of Joseph and Jane it can be concluded that previous year

financial loss are capital losses. In case house was sold at a price more than cost of acquisition

there is capital gain from which capital losses was deducted and balance is charged against

capital gain tax. In case its sale at loss, accumulated capital loss amount would increase.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.