BULAW3731 Taxation Law: Uber and Traditional Taxi Comparison

VerifiedAdded on 2022/11/13

|14

|3659

|351

Report

AI Summary

This report examines the taxation law surrounding the sharing economy, specifically comparing the business models and tax implications of Uber and traditional taxi services. It begins with an overview of the black and sharing economies, highlighting the challenges faced by governments and tax administrations. The report then delves into detailed analyses of the Uber and traditional taxi business models, identifying key differences that impact tax outcomes. These differences include regulatory frameworks, tax breaks, and the classification of workers. The study further explores tax consequences under existing Australian tax law, addressing issues like income tax, GST, and the potential for unfair competitive advantages. The report emphasizes the need for specific regulations within the sharing economy to ensure fair competition and adequate tax collection. The report concludes by summarizing the key findings and implications for the future of taxation in the digital age.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Introduction:...............................................................................................................................2

Overview of Black Economy:....................................................................................................2

Overview of sharing economy:..................................................................................................3

Sharing economy business model and traditional business model:...........................................4

Digital transportation business model (Uber):.......................................................................5

Traditional Taxation System (Taxi).......................................................................................7

Key differences between the two business models that effect taxation outcome:.....................8

Tax consequences under existing Australian tax law................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

Table of Contents

Introduction:...............................................................................................................................2

Overview of Black Economy:....................................................................................................2

Overview of sharing economy:..................................................................................................3

Sharing economy business model and traditional business model:...........................................4

Digital transportation business model (Uber):.......................................................................5

Traditional Taxation System (Taxi).......................................................................................7

Key differences between the two business models that effect taxation outcome:.....................8

Tax consequences under existing Australian tax law................................................................9

Conclusion:..............................................................................................................................10

References:...............................................................................................................................11

2TAXATION LAW

Introduction:

The business model of sharing economy has contributed to wide variety of economic,

social and legal issues. With the growth of this economy and wider market growth, the

pressure of government also increases to address as well as study the issue of sharing

economy to redress the rising distortion, while at the same time sustaining positive

innovation. An important concern of this report is whether the activities that are carried out

by the sharing economy agents are captured sufficiently (Demailly & Novel, 2014). The

present viewpoint is that there is lack of specific regulations in the sharing economy which is

further escalated by inadequate visibility of underlying activity, under-collection of tax from

under users and tax breaks provided to the platform results in unfair competitive advantage

over its counterparts under more strictly regulated traditional sectors.

The study also emphasis on the challenges that is faced by the governments and tax

administrations and how the rising concerns of the sharing economy is acknowledged inside

the national governments. The study would emphasis on the two business models namely the

digital mode and the traditional mode of business operations. An in depth analysis of Uber

and traditional Taxicabs business model will be studied in this report. Identification of

important differences will be addressed as well which effects the tax outcomes and would be

providing an explanation of the differences under the current Australian tax laws.

Overview of Black Economy:

Black economy is regarded as those segment of a nation’s economic activity which is

derived from the sources which falls out of the nation’s rules and regulations relating to trade

and commerce (Schor, 2016). The activities under the black economy can be either legal or

illegal and it is mainly reliant on the type of goods and services that are involved. People

generally operate under the black economy to trade illegal imports, avoid the taxes and

Introduction:

The business model of sharing economy has contributed to wide variety of economic,

social and legal issues. With the growth of this economy and wider market growth, the

pressure of government also increases to address as well as study the issue of sharing

economy to redress the rising distortion, while at the same time sustaining positive

innovation. An important concern of this report is whether the activities that are carried out

by the sharing economy agents are captured sufficiently (Demailly & Novel, 2014). The

present viewpoint is that there is lack of specific regulations in the sharing economy which is

further escalated by inadequate visibility of underlying activity, under-collection of tax from

under users and tax breaks provided to the platform results in unfair competitive advantage

over its counterparts under more strictly regulated traditional sectors.

The study also emphasis on the challenges that is faced by the governments and tax

administrations and how the rising concerns of the sharing economy is acknowledged inside

the national governments. The study would emphasis on the two business models namely the

digital mode and the traditional mode of business operations. An in depth analysis of Uber

and traditional Taxicabs business model will be studied in this report. Identification of

important differences will be addressed as well which effects the tax outcomes and would be

providing an explanation of the differences under the current Australian tax laws.

Overview of Black Economy:

Black economy is regarded as those segment of a nation’s economic activity which is

derived from the sources which falls out of the nation’s rules and regulations relating to trade

and commerce (Schor, 2016). The activities under the black economy can be either legal or

illegal and it is mainly reliant on the type of goods and services that are involved. People

generally operate under the black economy to trade illegal imports, avoid the taxes and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

regulations and skirt the price controls or rationing. Usually, black market originates when

the government restricts specific economic activities or services, either by making the

transactions illegal or by imposing tax on the items so much that it turns into a cost-

prohibitive. A black economy might originate to make the illegal goods and services

available or to make the expensive items available at a cheaper cost.

A large number of Australians have faith in an equal playing ground and believes that

it is not fair for the others to obtain a competitive advantage by purposely doing things wrong

(Beretta, 2017). The black economy is regularly altering its forms and it is largely supported

by the improper assumptions that taking part in the black economy is not lawbreaking. It

comprises of the employers improperly treating their workers by not paying what they must

get. Dishonest businesses are paying tax and superannuation so that they can undercut their

competitors. As a result, this creates pressure on the Australians that are doing their things in

a correct manner (Inman et al., 2015). Black economy is a difficult, multi-faceted incidence

that operates in work relation and financial or welfare system. The behaviour of black

economy generally comprises of the following;

a. Under-Reporting of wages

b. Bypassing the restrictions on visa

c. GST and tax fraud

d. Illegal phoenixing

e. Money laundering

Overview of sharing economy:

Sharing economy is referred as the economic activity performed through digital

platform where people share their assets or services in exchange of fee (Kathan et al., 2016).

If a person makes available some services or assets with the help of platform in exchange of

regulations and skirt the price controls or rationing. Usually, black market originates when

the government restricts specific economic activities or services, either by making the

transactions illegal or by imposing tax on the items so much that it turns into a cost-

prohibitive. A black economy might originate to make the illegal goods and services

available or to make the expensive items available at a cheaper cost.

A large number of Australians have faith in an equal playing ground and believes that

it is not fair for the others to obtain a competitive advantage by purposely doing things wrong

(Beretta, 2017). The black economy is regularly altering its forms and it is largely supported

by the improper assumptions that taking part in the black economy is not lawbreaking. It

comprises of the employers improperly treating their workers by not paying what they must

get. Dishonest businesses are paying tax and superannuation so that they can undercut their

competitors. As a result, this creates pressure on the Australians that are doing their things in

a correct manner (Inman et al., 2015). Black economy is a difficult, multi-faceted incidence

that operates in work relation and financial or welfare system. The behaviour of black

economy generally comprises of the following;

a. Under-Reporting of wages

b. Bypassing the restrictions on visa

c. GST and tax fraud

d. Illegal phoenixing

e. Money laundering

Overview of sharing economy:

Sharing economy is referred as the economic activity performed through digital

platform where people share their assets or services in exchange of fee (Kathan et al., 2016).

If a person makes available some services or assets with the help of platform in exchange of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

fee, then it becomes necessary to take into account how the goods and service tax and income

tax will be levied on those incomes.

Some of the popular activities of sharing activities

a. Providing ride-sourcing services in exchange of fare, through the platforms such as

the Uber or GoCatch

b. Renting out the room or the entire unit of the house based on short-term basis, through

digital platform such as Airbnb or Flipkey.

c. Sharing of the assets which includes the car, spaces for car parking, space for storage

or private belongings through digital platforms such as Toolmates or Quipmo.

The users in the sharing economy platforms monetises the capacity of surplus value

for assets or labour. For example, car or transportation services where users can rent out their

assets out owned by them and procure services on “as-needed”. Hence, the sharing economy

is entirely based on the idea of access over the ownership (Felländer et al. 2015). The effect

and use of sharing economy has significantly attained growth in the recent years in Australia

and other nations as well. This is largely due to the rising availability of access to internet

particularly through smart phones.

There are mainly end-users under this model which represents demand and supply for

the transactions which is later matched by using embedded search functionalities inside the

online platform (Mazhar & Méon, 2017). The participants under this economy provide their

professional services without entering in the formal contract arrangement with their clients.

Sharing economy business model and traditional business model:

Under the sharing economy, its activities are coordinated typically through the

applications that are running on the participant’s smartphones, which connect large number

of platform hosted by the operator. The platform acts as the intermediary among the

fee, then it becomes necessary to take into account how the goods and service tax and income

tax will be levied on those incomes.

Some of the popular activities of sharing activities

a. Providing ride-sourcing services in exchange of fare, through the platforms such as

the Uber or GoCatch

b. Renting out the room or the entire unit of the house based on short-term basis, through

digital platform such as Airbnb or Flipkey.

c. Sharing of the assets which includes the car, spaces for car parking, space for storage

or private belongings through digital platforms such as Toolmates or Quipmo.

The users in the sharing economy platforms monetises the capacity of surplus value

for assets or labour. For example, car or transportation services where users can rent out their

assets out owned by them and procure services on “as-needed”. Hence, the sharing economy

is entirely based on the idea of access over the ownership (Felländer et al. 2015). The effect

and use of sharing economy has significantly attained growth in the recent years in Australia

and other nations as well. This is largely due to the rising availability of access to internet

particularly through smart phones.

There are mainly end-users under this model which represents demand and supply for

the transactions which is later matched by using embedded search functionalities inside the

online platform (Mazhar & Méon, 2017). The participants under this economy provide their

professional services without entering in the formal contract arrangement with their clients.

Sharing economy business model and traditional business model:

Under the sharing economy, its activities are coordinated typically through the

applications that are running on the participant’s smartphones, which connect large number

of platform hosted by the operator. The platform acts as the intermediary among the

5TAXATION LAW

individual and participants that may use the platform as the contract for delivering some

services (Murillo et al., 2017). The intended operations of the sharing economy platforms are

that they do not employ any type of participants or own any control of the assets that are

shared over the platform. Instead, the platform looks forward to facilitate the creation of

arrangements among the peers. The platform is useful in providing a payment mechanism and

charges fees or commissions based on transaction basis.

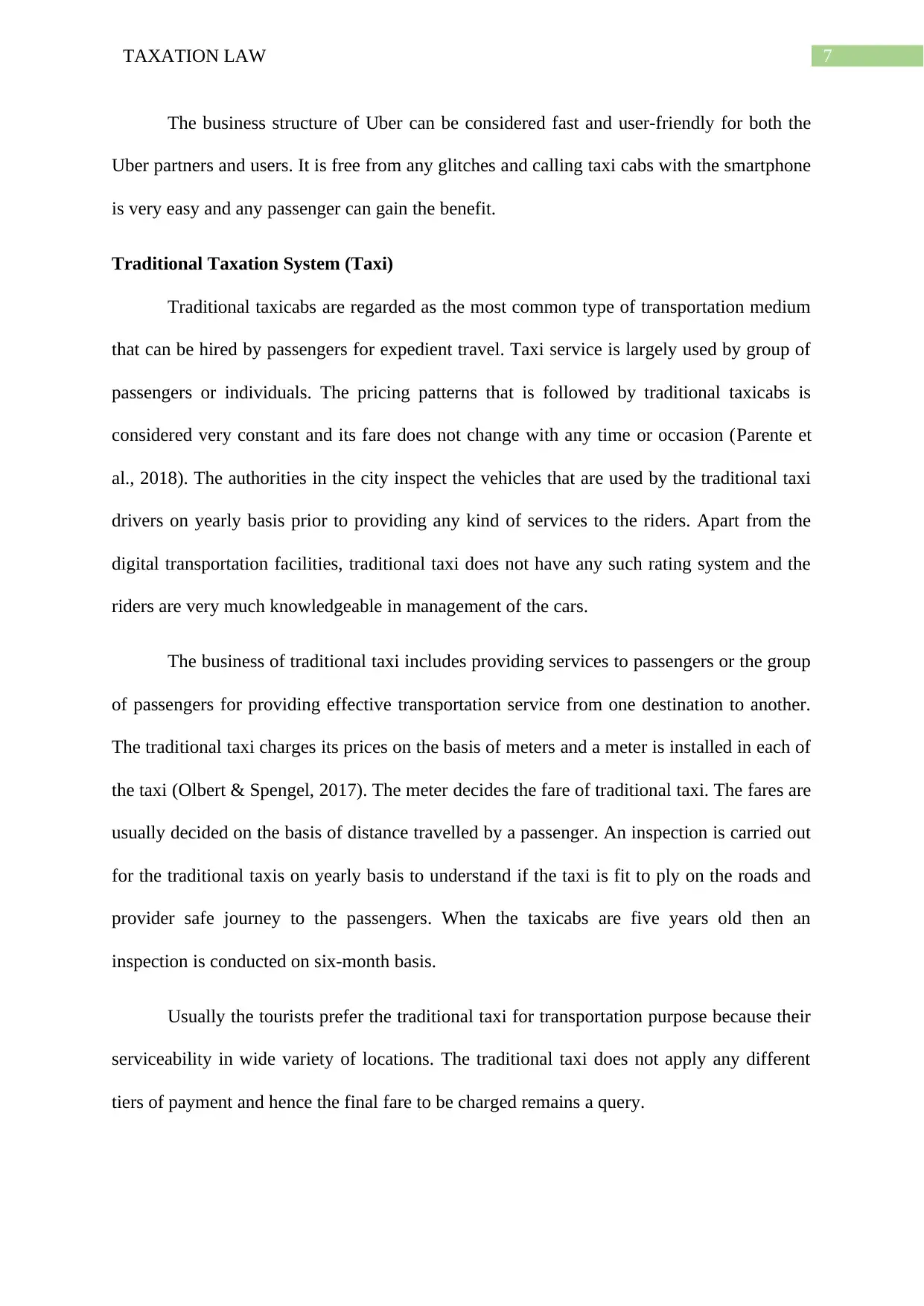

Digital transportation business model (Uber):

Uber is regarded as the transportation service which is based on demand and has

introduced a revolution in the taxi industry all through the world. The business model of Uber

is made up of possible people that only give tap on their smartphone and can have a cab

arrived on their location within the minimum possible time. As per the experts, Uber

produced $10 billion in revenues 2015 (Miller, 2016). The company is not a traditional

business model since it does not employ any taxi drivers on its own nor does it has any taxi of

its own. Uber essentially connects the passenger and taxi driver and take some portion of fee

as their share. The business model of Uber is give below;

Taxi Driver: For Uber anyone that has the driving license and car can apply for the Uber

driver any cities which is converted into Uber. Following the screening of the driver, he is

enlisted under the system of Uber and they are provided with Uber IPhone (Tauscher &

Kietzmann, 2017). This helps in providing a steady source of income for anyone without any

hazard or investment.

Passengers: Registered Uber users can download the app of Uber to their phones and if they

require taxi, they can avail the services through Uber application. The passengers can keep

track of their taxi on their phones when it approaches their pick up location. This services can

individual and participants that may use the platform as the contract for delivering some

services (Murillo et al., 2017). The intended operations of the sharing economy platforms are

that they do not employ any type of participants or own any control of the assets that are

shared over the platform. Instead, the platform looks forward to facilitate the creation of

arrangements among the peers. The platform is useful in providing a payment mechanism and

charges fees or commissions based on transaction basis.

Digital transportation business model (Uber):

Uber is regarded as the transportation service which is based on demand and has

introduced a revolution in the taxi industry all through the world. The business model of Uber

is made up of possible people that only give tap on their smartphone and can have a cab

arrived on their location within the minimum possible time. As per the experts, Uber

produced $10 billion in revenues 2015 (Miller, 2016). The company is not a traditional

business model since it does not employ any taxi drivers on its own nor does it has any taxi of

its own. Uber essentially connects the passenger and taxi driver and take some portion of fee

as their share. The business model of Uber is give below;

Taxi Driver: For Uber anyone that has the driving license and car can apply for the Uber

driver any cities which is converted into Uber. Following the screening of the driver, he is

enlisted under the system of Uber and they are provided with Uber IPhone (Tauscher &

Kietzmann, 2017). This helps in providing a steady source of income for anyone without any

hazard or investment.

Passengers: Registered Uber users can download the app of Uber to their phones and if they

require taxi, they can avail the services through Uber application. The passengers can keep

track of their taxi on their phones when it approaches their pick up location. This services can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

be convenient for the passengers, provides them with relatively low cost and comfortable

service.

Fare and Payment: Uber decides the taxi fares. Premium fare is charged during the peak

hours and flat rates are charged during the off peak hours. Passengers are required to pay with

the help of their credit cards and they do not have to pay cash to the drivers (Jin et al., 2018).

The fare is usually based on the type of car, distance and peak business hour. Payment is

secure since passengers only pay through the credit card by using the Uber application.

Dividing the Profits: Uber divides its fare, generally 80% to the driver while the rest 20 is

given to the Uber. Despite the pay cut of 20%, the taxi drivers are able to earn more than the

traditional taxi services. In some of the cities Uber has to reduce its percentage due to the

prevailing competition from other similar companies such as Haio and Lyft.

Figure 1: Uber business model

(Source: As Created by Author)

Taxi Driver Passengers

Fare Division of

Profits

be convenient for the passengers, provides them with relatively low cost and comfortable

service.

Fare and Payment: Uber decides the taxi fares. Premium fare is charged during the peak

hours and flat rates are charged during the off peak hours. Passengers are required to pay with

the help of their credit cards and they do not have to pay cash to the drivers (Jin et al., 2018).

The fare is usually based on the type of car, distance and peak business hour. Payment is

secure since passengers only pay through the credit card by using the Uber application.

Dividing the Profits: Uber divides its fare, generally 80% to the driver while the rest 20 is

given to the Uber. Despite the pay cut of 20%, the taxi drivers are able to earn more than the

traditional taxi services. In some of the cities Uber has to reduce its percentage due to the

prevailing competition from other similar companies such as Haio and Lyft.

Figure 1: Uber business model

(Source: As Created by Author)

Taxi Driver Passengers

Fare Division of

Profits

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The business structure of Uber can be considered fast and user-friendly for both the

Uber partners and users. It is free from any glitches and calling taxi cabs with the smartphone

is very easy and any passenger can gain the benefit.

Traditional Taxation System (Taxi)

Traditional taxicabs are regarded as the most common type of transportation medium

that can be hired by passengers for expedient travel. Taxi service is largely used by group of

passengers or individuals. The pricing patterns that is followed by traditional taxicabs is

considered very constant and its fare does not change with any time or occasion (Parente et

al., 2018). The authorities in the city inspect the vehicles that are used by the traditional taxi

drivers on yearly basis prior to providing any kind of services to the riders. Apart from the

digital transportation facilities, traditional taxi does not have any such rating system and the

riders are very much knowledgeable in management of the cars.

The business of traditional taxi includes providing services to passengers or the group

of passengers for providing effective transportation service from one destination to another.

The traditional taxi charges its prices on the basis of meters and a meter is installed in each of

the taxi (Olbert & Spengel, 2017). The meter decides the fare of traditional taxi. The fares are

usually decided on the basis of distance travelled by a passenger. An inspection is carried out

for the traditional taxis on yearly basis to understand if the taxi is fit to ply on the roads and

provider safe journey to the passengers. When the taxicabs are five years old then an

inspection is conducted on six-month basis.

Usually the tourists prefer the traditional taxi for transportation purpose because their

serviceability in wide variety of locations. The traditional taxi does not apply any different

tiers of payment and hence the final fare to be charged remains a query.

The business structure of Uber can be considered fast and user-friendly for both the

Uber partners and users. It is free from any glitches and calling taxi cabs with the smartphone

is very easy and any passenger can gain the benefit.

Traditional Taxation System (Taxi)

Traditional taxicabs are regarded as the most common type of transportation medium

that can be hired by passengers for expedient travel. Taxi service is largely used by group of

passengers or individuals. The pricing patterns that is followed by traditional taxicabs is

considered very constant and its fare does not change with any time or occasion (Parente et

al., 2018). The authorities in the city inspect the vehicles that are used by the traditional taxi

drivers on yearly basis prior to providing any kind of services to the riders. Apart from the

digital transportation facilities, traditional taxi does not have any such rating system and the

riders are very much knowledgeable in management of the cars.

The business of traditional taxi includes providing services to passengers or the group

of passengers for providing effective transportation service from one destination to another.

The traditional taxi charges its prices on the basis of meters and a meter is installed in each of

the taxi (Olbert & Spengel, 2017). The meter decides the fare of traditional taxi. The fares are

usually decided on the basis of distance travelled by a passenger. An inspection is carried out

for the traditional taxis on yearly basis to understand if the taxi is fit to ply on the roads and

provider safe journey to the passengers. When the taxicabs are five years old then an

inspection is conducted on six-month basis.

Usually the tourists prefer the traditional taxi for transportation purpose because their

serviceability in wide variety of locations. The traditional taxi does not apply any different

tiers of payment and hence the final fare to be charged remains a query.

8TAXATION LAW

Key differences between the two business models that effect taxation outcome:

An important difference between the two business models is that tax breaks are

provided to the platforms which contributes in unfair competitive advantage over the

competitors while there is a strict regulation is imposed on the traditional sectors. The car

sharing is perceived as very analogous to the traditional taxi services and certainly more

traditional competitors have witnessed a decline in their market share once the digital version

is entered into the scene (Constantiou et al., 2017). In addition to this, there is a risk risks that

laissez-affaire attitude to sharing economy sector and insufficient intervention of the

government to promote controlling consistency between the sharing and the traditional

economies may lead to converting the offerings of sharing economy in the formal economy

with the negative effect on the tax collections.

Another vital differences that can be taken into account regarding the digital

transportation system and traditional transportation system. Even though preventive measures

are taken by the government to make sure that the sharing economy stays inside the formal

domain the taxes which is applied to its activities might reduce the revenues and

simultaneously distorts the equal playing field between traditional and digital transportation

system (Wallsten, 2015). The most commonly observed things are that there is an insufficient

certainty in categorizing the activity that are performed by the end users for taxation purpose.

This results in under-tax that are carried out by the end users for taxation purpose. As a result,

the traditional business models are displaced within the digital transportation system leading

to additional depletion of tax revenues through lower generation of employment taxes. This

hits the purses of government in a substantial manner (Parente et al., 2018). For example, in

2016 as per the reports of Municipal transportation agency the demand for the traditional

taxicabs fell by 30% in Australia.

Key differences between the two business models that effect taxation outcome:

An important difference between the two business models is that tax breaks are

provided to the platforms which contributes in unfair competitive advantage over the

competitors while there is a strict regulation is imposed on the traditional sectors. The car

sharing is perceived as very analogous to the traditional taxi services and certainly more

traditional competitors have witnessed a decline in their market share once the digital version

is entered into the scene (Constantiou et al., 2017). In addition to this, there is a risk risks that

laissez-affaire attitude to sharing economy sector and insufficient intervention of the

government to promote controlling consistency between the sharing and the traditional

economies may lead to converting the offerings of sharing economy in the formal economy

with the negative effect on the tax collections.

Another vital differences that can be taken into account regarding the digital

transportation system and traditional transportation system. Even though preventive measures

are taken by the government to make sure that the sharing economy stays inside the formal

domain the taxes which is applied to its activities might reduce the revenues and

simultaneously distorts the equal playing field between traditional and digital transportation

system (Wallsten, 2015). The most commonly observed things are that there is an insufficient

certainty in categorizing the activity that are performed by the end users for taxation purpose.

This results in under-tax that are carried out by the end users for taxation purpose. As a result,

the traditional business models are displaced within the digital transportation system leading

to additional depletion of tax revenues through lower generation of employment taxes. This

hits the purses of government in a substantial manner (Parente et al., 2018). For example, in

2016 as per the reports of Municipal transportation agency the demand for the traditional

taxicabs fell by 30% in Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Revenues produced under the digital transportation system such as by Uber drivers

are generally not disclosed as compared to the traditional transportation system. According to

the survey of TNS approximately 15% of the Uber drivers operating under sharing economy

reported their revenues while more than 46% of drivers of sharing platform have not

disclosed their income and have stated that their income is not beyond the threshold limit

(Slee, 2017). While more 80% of the drivers operating under the traditional systems have

disclosed their income to ATO produced from the rented vehicles.

Tax consequences under existing Australian tax law

There are fears that sharing economy can reduce the tax revenues for the government.

This originates from the challenges that are faced by the tax administrations in assuring that

the service providers adhere with the tax obligations (Schor & Cansoy, 2019). There are

difficulties in recognizing the taxable earnings since there is a deficiency of information

regarding the services provider’s activities which will result in difficulties for the tax

administrations in recognizing the assessable income.

In the non-existence any obligations imposed on the platforms operators to disclose

information to tax authorities on service providers that are enrolled under the sharing

economy platform, there may be difficulties in detecting the income that is produced from the

service providers since it lacks the culture of compliance (Calo & Rosenblat, 2017). Without

any clear rules thee may be difficulty in ascertaining where taxes can be imposed.

It is also witnessed that there is income that are not disclosed by the service providers

and might remain unreported for taxation purpose if the platform operators do not provide

this information to the tax authorities (Cramer & Krueger, 2016). It has mainly argued that

the certain features of the sharing economy possess challenge in applying the tax obedience.

Revenues produced under the digital transportation system such as by Uber drivers

are generally not disclosed as compared to the traditional transportation system. According to

the survey of TNS approximately 15% of the Uber drivers operating under sharing economy

reported their revenues while more than 46% of drivers of sharing platform have not

disclosed their income and have stated that their income is not beyond the threshold limit

(Slee, 2017). While more 80% of the drivers operating under the traditional systems have

disclosed their income to ATO produced from the rented vehicles.

Tax consequences under existing Australian tax law

There are fears that sharing economy can reduce the tax revenues for the government.

This originates from the challenges that are faced by the tax administrations in assuring that

the service providers adhere with the tax obligations (Schor & Cansoy, 2019). There are

difficulties in recognizing the taxable earnings since there is a deficiency of information

regarding the services provider’s activities which will result in difficulties for the tax

administrations in recognizing the assessable income.

In the non-existence any obligations imposed on the platforms operators to disclose

information to tax authorities on service providers that are enrolled under the sharing

economy platform, there may be difficulties in detecting the income that is produced from the

service providers since it lacks the culture of compliance (Calo & Rosenblat, 2017). Without

any clear rules thee may be difficulty in ascertaining where taxes can be imposed.

It is also witnessed that there is income that are not disclosed by the service providers

and might remain unreported for taxation purpose if the platform operators do not provide

this information to the tax authorities (Cramer & Krueger, 2016). It has mainly argued that

the certain features of the sharing economy possess challenge in applying the tax obedience.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

To being with, due to its new sector, not all the participants are capable of

understanding the tax obligations and might face difficulty in declaring their income (Kooti et

al., 2017). This is mainly due to the fact that there may transformation from employment to

self-employment that may introduce confusion for the digital transportation partners as well

as for the governments on what can be taxable and what deductions can be permitted.

There several service providers that are new business and does not pays attention in

tracking their income and expenditure. They might also believe that this kind of income is

non-taxable and may not hence declare it. As held in “Uber B.V v FCT (2017)” the decision

which was given by law court was that services provided by Uber drivers will be treated

assessable under the meaning of “sec 144-5(1) of the GST Act 1999” (Frenken & Schor,

2017). The law court held that Uber partners should obtain a GST registration regardless of

their income.

Conclusion:

The digital economy makes use of idle excess capacity resources and provides a

significant case of forming a free market sustainability. Despite the benefits it produces

negative social trends. In respect of taxation, if the sharing economy is adequately captured

under the Australian tax code then there can be a reliable source of revenue for the

government. It is argued that traditional market segments which is replaced by sharing

economy is customarily demonstrating deficiency since the payment method evades the

official reporting procedure and undermines the tax base.

To being with, due to its new sector, not all the participants are capable of

understanding the tax obligations and might face difficulty in declaring their income (Kooti et

al., 2017). This is mainly due to the fact that there may transformation from employment to

self-employment that may introduce confusion for the digital transportation partners as well

as for the governments on what can be taxable and what deductions can be permitted.

There several service providers that are new business and does not pays attention in

tracking their income and expenditure. They might also believe that this kind of income is

non-taxable and may not hence declare it. As held in “Uber B.V v FCT (2017)” the decision

which was given by law court was that services provided by Uber drivers will be treated

assessable under the meaning of “sec 144-5(1) of the GST Act 1999” (Frenken & Schor,

2017). The law court held that Uber partners should obtain a GST registration regardless of

their income.

Conclusion:

The digital economy makes use of idle excess capacity resources and provides a

significant case of forming a free market sustainability. Despite the benefits it produces

negative social trends. In respect of taxation, if the sharing economy is adequately captured

under the Australian tax code then there can be a reliable source of revenue for the

government. It is argued that traditional market segments which is replaced by sharing

economy is customarily demonstrating deficiency since the payment method evades the

official reporting procedure and undermines the tax base.

11TAXATION LAW

References:

Beretta, G. (2017). Taxation of individuals in the sharing economy. Intertax, 45(1), 2-11.

Calo, R., & Rosenblat, A. (2017). The taking economy: Uber, information, and

power. Colum. L. Rev., 117, 1623.

Constantiou, I., Marton, A., & Tuunainen, V. K. (2017). Four Models of Sharing Economy

Platforms. MIS Quarterly Executive, 16(4).

Cramer, J., & Krueger, A. B. (2016). Disruptive change in the taxi business: The case of

Uber. American Economic Review, 106(5), 177-82.

Demailly, D., & Novel, A. S. (2014). The sharing economy: make it

sustainable. Studies, 3(14), 14-30.

Felländer, A., Ingram, C., & Teigland, R. (2015). Sharing economy. In Embracing Change

with Caution. Näringspolitiskt Forum Rapport (No. 11).

Frenken, K., & Schor, J. (2017). Putting the sharing economy into

perspective. Environmental Innovation and Societal Transitions, 23, 3-10.

Inman, R. P., McGuire, M., Oates, W. E., Pressman, J. L., & Reischauer, R. D.

(2015). Financing the New Federalism: Revenue Sharing, Conditional Grants and

Taxation. Routledge.

Jin, S. T., Kong, H., Wu, R., & Sui, D. Z. (2018). Ridesourcing, the sharing economy, and the

future of cities. Cities, 76, 96-104.

Kathan, W., Matzler, K., & Veider, V. (2016). The sharing economy: Your business model's

friend or foe?. Business Horizons, 59(6), 663-672.

References:

Beretta, G. (2017). Taxation of individuals in the sharing economy. Intertax, 45(1), 2-11.

Calo, R., & Rosenblat, A. (2017). The taking economy: Uber, information, and

power. Colum. L. Rev., 117, 1623.

Constantiou, I., Marton, A., & Tuunainen, V. K. (2017). Four Models of Sharing Economy

Platforms. MIS Quarterly Executive, 16(4).

Cramer, J., & Krueger, A. B. (2016). Disruptive change in the taxi business: The case of

Uber. American Economic Review, 106(5), 177-82.

Demailly, D., & Novel, A. S. (2014). The sharing economy: make it

sustainable. Studies, 3(14), 14-30.

Felländer, A., Ingram, C., & Teigland, R. (2015). Sharing economy. In Embracing Change

with Caution. Näringspolitiskt Forum Rapport (No. 11).

Frenken, K., & Schor, J. (2017). Putting the sharing economy into

perspective. Environmental Innovation and Societal Transitions, 23, 3-10.

Inman, R. P., McGuire, M., Oates, W. E., Pressman, J. L., & Reischauer, R. D.

(2015). Financing the New Federalism: Revenue Sharing, Conditional Grants and

Taxation. Routledge.

Jin, S. T., Kong, H., Wu, R., & Sui, D. Z. (2018). Ridesourcing, the sharing economy, and the

future of cities. Cities, 76, 96-104.

Kathan, W., Matzler, K., & Veider, V. (2016). The sharing economy: Your business model's

friend or foe?. Business Horizons, 59(6), 663-672.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.