Taxation Law Assignment: Applying Tax Law to Real-World Scenarios

VerifiedAdded on 2019/11/25

|13

|2249

|159

Homework Assignment

AI Summary

This assignment solution addresses several key areas of taxation law. The first question examines net capital gains or losses under ITAA 1997, analyzing the tax implications of asset sales. Question 2 focuses on Fringe Benefit Tax (FBT) under the FBT Act 1986, specifically concerning interest offset arrangements. Question 3 explores the assessable position of losses from rental property, considering co-ownership and relevant tax rulings. The fourth question discusses tax avoidance principles, referencing the IRC v Duke of Westminster case. Finally, question 5 analyzes the taxation of income generated from timber sales, considering primary production and relevant legislation. The assignment provides detailed explanations, legal references, and conclusions for each scenario.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................7

Issues:.........................................................................................................................................7

Laws:..........................................................................................................................................7

Application:................................................................................................................................8

Table of Contents

Answer to question 1:.................................................................................................................2

Issue:..........................................................................................................................................2

Laws:..........................................................................................................................................2

Applications:..............................................................................................................................2

Conclusion:................................................................................................................................3

Answer to question 2:.................................................................................................................3

Issue:..........................................................................................................................................3

Laws:..........................................................................................................................................3

Applications:..............................................................................................................................3

Conclusion:................................................................................................................................4

Answer to question 3:.................................................................................................................5

Issue:..........................................................................................................................................5

Laws:..........................................................................................................................................5

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................7

Issues:.........................................................................................................................................7

Laws:..........................................................................................................................................7

Application:................................................................................................................................8

2TAXATION LAW

Conclusion:................................................................................................................................9

Reference List:.........................................................................................................................10

Conclusion:................................................................................................................................9

Reference List:.........................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

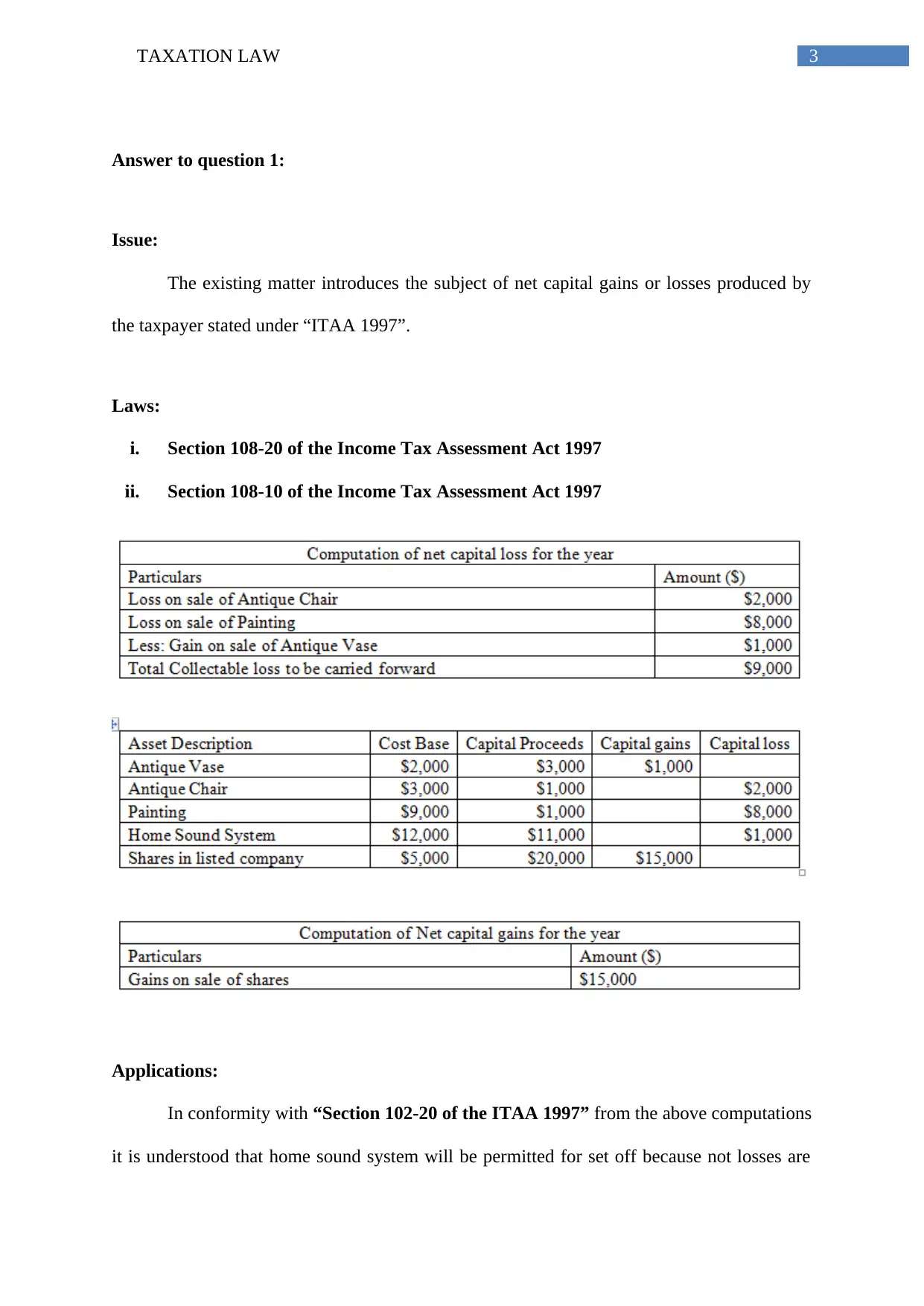

Answer to question 1:

Issue:

The existing matter introduces the subject of net capital gains or losses produced by

the taxpayer stated under “ITAA 1997”.

Laws:

i. Section 108-20 of the Income Tax Assessment Act 1997

ii. Section 108-10 of the Income Tax Assessment Act 1997

Applications:

In conformity with “Section 102-20 of the ITAA 1997” from the above computations

it is understood that home sound system will be permitted for set off because not losses are

Answer to question 1:

Issue:

The existing matter introduces the subject of net capital gains or losses produced by

the taxpayer stated under “ITAA 1997”.

Laws:

i. Section 108-20 of the Income Tax Assessment Act 1997

ii. Section 108-10 of the Income Tax Assessment Act 1997

Applications:

In conformity with “Section 102-20 of the ITAA 1997” from the above computations

it is understood that home sound system will be permitted for set off because not losses are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

allowed to be carried forward on the sale of personal asset (Kenny 2013). As defined under

“Section 108-10 of the ITAA 1997” losses in the form of collectable will not be permitted

for set off against the ordinary gains derived from the sale of shares and it is only eligible for

offset against the collectible gains stated under the “Section 108-10 of the ITAA 1997”

(Newman, S., 2016). As Eric generated profit from the sale of ordinary asset with no present

year ordinary capital, the net amount of capital gains for Eric stands $15,000.

Conclusion:

It can concluded that no kind of loss is permitted for offset from the asset that are of

personal use. Therefore, Eric only gains from the disposal of ordinary assets.

Answer to question 2:

Issue:

The issue introduces the matter of assessment of FBT of the taxpayer stated under the

“FBT Act 1986” (James 2016).

Laws:

i. Taxation rulings of TR 93/6

ii. Fringe Benefit Tax Assessment Act 1986

Applications:

Calculation of Fringe Benefit Tax

allowed to be carried forward on the sale of personal asset (Kenny 2013). As defined under

“Section 108-10 of the ITAA 1997” losses in the form of collectable will not be permitted

for set off against the ordinary gains derived from the sale of shares and it is only eligible for

offset against the collectible gains stated under the “Section 108-10 of the ITAA 1997”

(Newman, S., 2016). As Eric generated profit from the sale of ordinary asset with no present

year ordinary capital, the net amount of capital gains for Eric stands $15,000.

Conclusion:

It can concluded that no kind of loss is permitted for offset from the asset that are of

personal use. Therefore, Eric only gains from the disposal of ordinary assets.

Answer to question 2:

Issue:

The issue introduces the matter of assessment of FBT of the taxpayer stated under the

“FBT Act 1986” (James 2016).

Laws:

i. Taxation rulings of TR 93/6

ii. Fringe Benefit Tax Assessment Act 1986

Applications:

Calculation of Fringe Benefit Tax

5TAXATION LAW

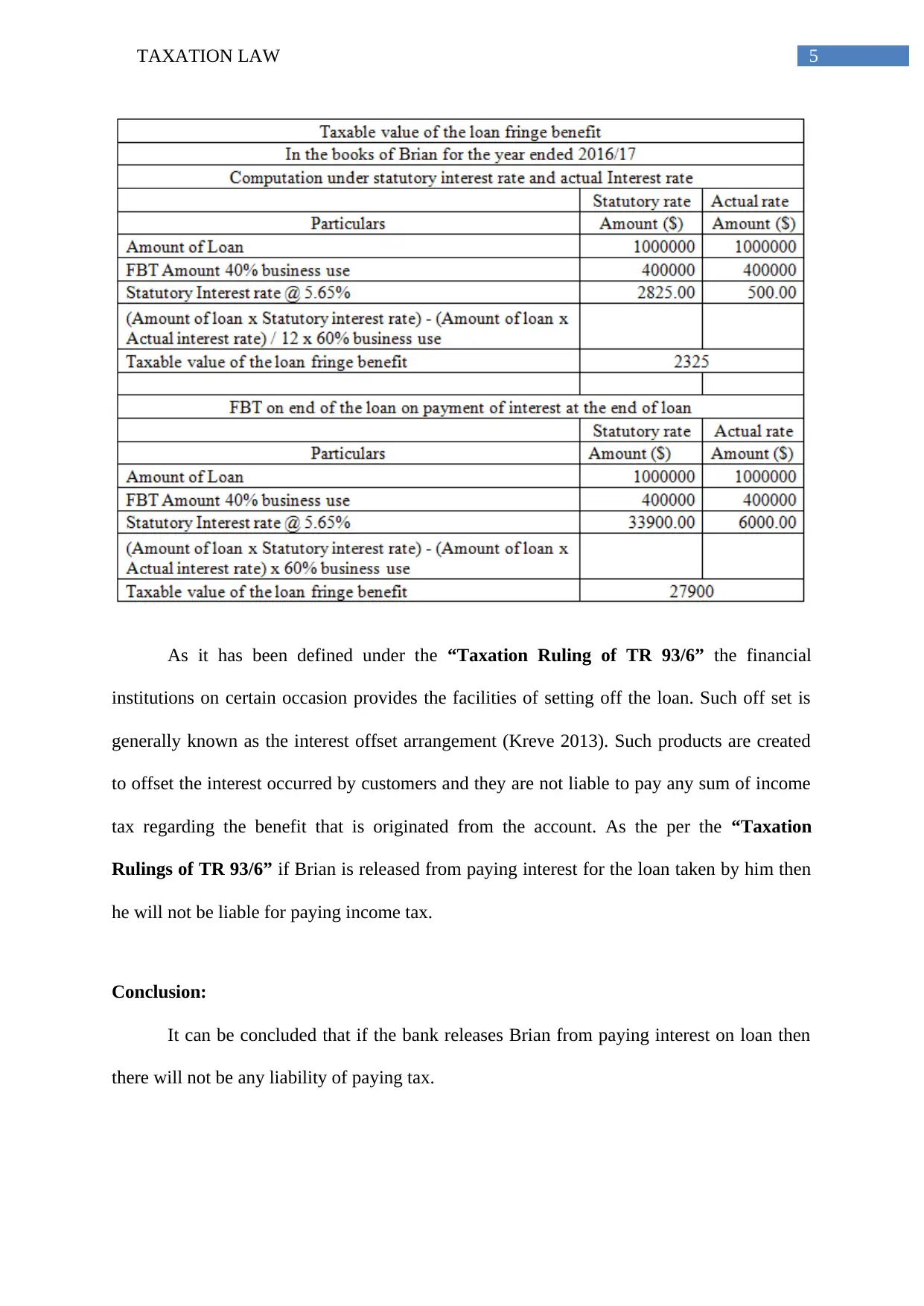

As it has been defined under the “Taxation Ruling of TR 93/6” the financial

institutions on certain occasion provides the facilities of setting off the loan. Such off set is

generally known as the interest offset arrangement (Kreve 2013). Such products are created

to offset the interest occurred by customers and they are not liable to pay any sum of income

tax regarding the benefit that is originated from the account. As the per the “Taxation

Rulings of TR 93/6” if Brian is released from paying interest for the loan taken by him then

he will not be liable for paying income tax.

Conclusion:

It can be concluded that if the bank releases Brian from paying interest on loan then

there will not be any liability of paying tax.

As it has been defined under the “Taxation Ruling of TR 93/6” the financial

institutions on certain occasion provides the facilities of setting off the loan. Such off set is

generally known as the interest offset arrangement (Kreve 2013). Such products are created

to offset the interest occurred by customers and they are not liable to pay any sum of income

tax regarding the benefit that is originated from the account. As the per the “Taxation

Rulings of TR 93/6” if Brian is released from paying interest for the loan taken by him then

he will not be liable for paying income tax.

Conclusion:

It can be concluded that if the bank releases Brian from paying interest on loan then

there will not be any liability of paying tax.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to question 3:

Issue:

The issue brings forward the matter of determining assessable position of loss that

Jack and Jill suffered from the rental property.

Laws:

i. Section 51 of the ITAA 1997

ii. Taxation rulings of TR 93/32

iii. F.C. of T. v McDonald (1987) 18 ATR 957

Application:

As it has been found from the existing situation that Jack and Jill entered in a business

of rental property and were joint tenant. Jack was entitled to only 10% of the profit and Jill

being entitled to 90% of the profit from rental property. However, the agreement between

them contained clause that on sustaining loss Jack will be accountable of shouldering 100%

of the loss from the rental property. The “taxation ruling of 93/32” brings forward the

assessment of division of net profit or loss derived from the rental property amid the co-

owners (Barton 2013).

The ruling defines the Co-ownership of the partnership for taxation purpose however

it does not constitute partnership under the general law unless the ownership comprises of

carrying of the business activities. In reference to the “Taxation Ruling of 93/32” it can be

defined that the co-ownership between Jack and Jill represents partnership for the purpose of

taxation but it could not be treated as partnership under the general law (Anderson, Dickfos

and Brown 2016).

Answer to question 3:

Issue:

The issue brings forward the matter of determining assessable position of loss that

Jack and Jill suffered from the rental property.

Laws:

i. Section 51 of the ITAA 1997

ii. Taxation rulings of TR 93/32

iii. F.C. of T. v McDonald (1987) 18 ATR 957

Application:

As it has been found from the existing situation that Jack and Jill entered in a business

of rental property and were joint tenant. Jack was entitled to only 10% of the profit and Jill

being entitled to 90% of the profit from rental property. However, the agreement between

them contained clause that on sustaining loss Jack will be accountable of shouldering 100%

of the loss from the rental property. The “taxation ruling of 93/32” brings forward the

assessment of division of net profit or loss derived from the rental property amid the co-

owners (Barton 2013).

The ruling defines the Co-ownership of the partnership for taxation purpose however

it does not constitute partnership under the general law unless the ownership comprises of

carrying of the business activities. In reference to the “Taxation Ruling of 93/32” it can be

defined that the co-ownership between Jack and Jill represents partnership for the purpose of

taxation but it could not be treated as partnership under the general law (Anderson, Dickfos

and Brown 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Citing the reference of “F.C. of T. v McDonald (1987) 18 ATR 957” where the

taxpayer were husband and wife and legally owned two strata units as joint tenants (Morgan,

Mortimer and Pinto 2013). The agreement contained that 25% of the profits were attributable

to Mr McDonald and Mrs McDonald would be entitled to 75% of the profit with the entire

amount of loss being borne by Mr McDonald.

The question introduces the issue whether the loss derived from the operations was

wholly occurred by the taxpayer or among each of the taxpayer and his spouse occurred half

of the sum of loss. There was not provision of deductibility of loss (Barkoczy et al. 2016). It

is understood that was no partnership as per the general law and only a relationship of co-

ownership existed between them. Being the joint owners under the law, the loss sustained by

them must be uniformly shared among with respondents are under obligation of deducting

half of the loss sustained (Milton 2013). Therefore, Jack and Jill are required to share loss

equally for taxation purpose and no deductions will be allowed in terms of their agreement.

The reason behind this is that distribution of loss was willingly made by Jack as the domestic

arrangement of advancing the income of his wife because section 51 does not gives

permission of deductions in terms of the agreement made.

Additionally, if Jack and Jill decides to sell the property, the cost base and the

lowered cost base of the rental property must be included in their amount paid by them. Since

Jack and Jill are the joint owners of the property capital gains and loss shall be accounted

with the ownership of the interest of property.

Conclusion:

It can be concluded that no such partnership existed under the general and the losses

must be shared equally among Jack and Jill.

Citing the reference of “F.C. of T. v McDonald (1987) 18 ATR 957” where the

taxpayer were husband and wife and legally owned two strata units as joint tenants (Morgan,

Mortimer and Pinto 2013). The agreement contained that 25% of the profits were attributable

to Mr McDonald and Mrs McDonald would be entitled to 75% of the profit with the entire

amount of loss being borne by Mr McDonald.

The question introduces the issue whether the loss derived from the operations was

wholly occurred by the taxpayer or among each of the taxpayer and his spouse occurred half

of the sum of loss. There was not provision of deductibility of loss (Barkoczy et al. 2016). It

is understood that was no partnership as per the general law and only a relationship of co-

ownership existed between them. Being the joint owners under the law, the loss sustained by

them must be uniformly shared among with respondents are under obligation of deducting

half of the loss sustained (Milton 2013). Therefore, Jack and Jill are required to share loss

equally for taxation purpose and no deductions will be allowed in terms of their agreement.

The reason behind this is that distribution of loss was willingly made by Jack as the domestic

arrangement of advancing the income of his wife because section 51 does not gives

permission of deductions in terms of the agreement made.

Additionally, if Jack and Jill decides to sell the property, the cost base and the

lowered cost base of the rental property must be included in their amount paid by them. Since

Jack and Jill are the joint owners of the property capital gains and loss shall be accounted

with the ownership of the interest of property.

Conclusion:

It can be concluded that no such partnership existed under the general and the losses

must be shared equally among Jack and Jill.

8TAXATION LAW

Answer to question 4:

In IRC v Duke of Westminster [1936] AC it has been constantly stated during the

event of tax avoidance (Woellner 2013). The case bought forward the belief that every person

is allowed to order for his affairs in such a manner that the assignment of tax that is made is

in accordance of the act and it is less then it would have else been. Even if has been taken

into the considerations that this ruling was pleasing for others in seeking tax avoidance by

legally creating a multifaceted structure, it has been destabilized from the succeeding cases

where the courts have looked into the entire contract.

As an example “WT Ramsay v. IRC” it was observed that court adopted more

restrictive method (Barkoczy 2016). It was found that if a person has pre-arranged artificial

steps that did not served any kind of business objective rather than saving tax, the corrective

approach was to levy duty to the degree of transaction entirely.

In the current age if the principle is applied in Australia, the taxpayers can attain

success where they could not be forced to pay additional sum of tax (Saad 2014). It provides

that the companies and taxpayers to design their monetary transaction so they can reduce

their tax liabilities inside the constitution of the law.

Answer to question 5:

Issues:

This issue is introduces the subject of whether the income generated from selling of

timber shall be regarded as taxable proceeds under “subsection 6 (1) of the ITAA 1936”.

Laws:

i. Subsection 6 (1) of the ITAA 1936

Answer to question 4:

In IRC v Duke of Westminster [1936] AC it has been constantly stated during the

event of tax avoidance (Woellner 2013). The case bought forward the belief that every person

is allowed to order for his affairs in such a manner that the assignment of tax that is made is

in accordance of the act and it is less then it would have else been. Even if has been taken

into the considerations that this ruling was pleasing for others in seeking tax avoidance by

legally creating a multifaceted structure, it has been destabilized from the succeeding cases

where the courts have looked into the entire contract.

As an example “WT Ramsay v. IRC” it was observed that court adopted more

restrictive method (Barkoczy 2016). It was found that if a person has pre-arranged artificial

steps that did not served any kind of business objective rather than saving tax, the corrective

approach was to levy duty to the degree of transaction entirely.

In the current age if the principle is applied in Australia, the taxpayers can attain

success where they could not be forced to pay additional sum of tax (Saad 2014). It provides

that the companies and taxpayers to design their monetary transaction so they can reduce

their tax liabilities inside the constitution of the law.

Answer to question 5:

Issues:

This issue is introduces the subject of whether the income generated from selling of

timber shall be regarded as taxable proceeds under “subsection 6 (1) of the ITAA 1936”.

Laws:

i. Subsection 6 (1) of the ITAA 1936

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

ii. McCauley v F C of T (1944)

Application:

As understood from the study that Bill being the owner of land having large amount

of pine trees was approached by a logging unit which was willing to pay $1000 for every 100

meters of timber that the company take from his land. The “Taxation ruling of TR 95/6”

defines the taxation consequences resulting from the activities of primary producer and

forestry (Braithwaite 2017). The ruling is applicable to the person that are engaged in forest

operations and also on those that indulged in the forest operation of selling timber. Receipts

from such activities would be treated as assessable income whether the taxpayer was engaged

in the activities of the forestry.

As per “Subsection 6 (1) of ITAA 1997” primary production includes planting or

tending or trees in a plantation which is intended for felling. Bill, in conformity with the

“Subsection 6 (1) of the ITAA 1936” Bill will be viewed as primary producer because he

has been engaged in the activities of felling of trees in a plantation which he owned

(Woellner et al. 2016). Bill is the owner of large land however he did not planted the trees on

that land but the income derived from felling of trees will be considered for taxation.

Disposal of standing timber that is not planted by the taxpayer and felled with the objective of

selling with receipts derived from such sale would be treated as taxable income.

Simultaneously, if Bill was merely paid a lump sum of $50,000 by giving the right to

logging company of removing the necessary sum of timber such kind of receipts would be

treated as “Royalties”. In respect of section 26 (f) receiving “Royalties” from the tending of

timber will be treated as taxable income during the year in which trees were tended (Robin

2017). Citing the reference of “McCauley v F C of T (1944)” payments that is received by

ii. McCauley v F C of T (1944)

Application:

As understood from the study that Bill being the owner of land having large amount

of pine trees was approached by a logging unit which was willing to pay $1000 for every 100

meters of timber that the company take from his land. The “Taxation ruling of TR 95/6”

defines the taxation consequences resulting from the activities of primary producer and

forestry (Braithwaite 2017). The ruling is applicable to the person that are engaged in forest

operations and also on those that indulged in the forest operation of selling timber. Receipts

from such activities would be treated as assessable income whether the taxpayer was engaged

in the activities of the forestry.

As per “Subsection 6 (1) of ITAA 1997” primary production includes planting or

tending or trees in a plantation which is intended for felling. Bill, in conformity with the

“Subsection 6 (1) of the ITAA 1936” Bill will be viewed as primary producer because he

has been engaged in the activities of felling of trees in a plantation which he owned

(Woellner et al. 2016). Bill is the owner of large land however he did not planted the trees on

that land but the income derived from felling of trees will be considered for taxation.

Disposal of standing timber that is not planted by the taxpayer and felled with the objective of

selling with receipts derived from such sale would be treated as taxable income.

Simultaneously, if Bill was merely paid a lump sum of $50,000 by giving the right to

logging company of removing the necessary sum of timber such kind of receipts would be

treated as “Royalties”. In respect of section 26 (f) receiving “Royalties” from the tending of

timber will be treated as taxable income during the year in which trees were tended (Robin

2017). Citing the reference of “McCauley v F C of T (1944)” payments that is received by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

guarantor or the right of removing the trees is based on the right of removing the timber.

Hence, the sum received by him from royalty would be considered as taxable income.

Conclusion:

It can be concluded that tending of timber and selling the same is taxable income and

such receipts will be liable for taxation.

guarantor or the right of removing the trees is based on the right of removing the timber.

Hence, the sum received by him from royalty would be considered as taxable income.

Conclusion:

It can be concluded that tending of timber and selling the same is taxable income and

such receipts will be liable for taxation.

11TAXATION LAW

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G., 2016. Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Barton, (2013). Management of the Australian Taxation Office's property portfolio. ACT:

Australian National Audit Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), pp.345-362.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Milton, (2013). The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Morgan, A., Mortimer, C. and Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Newman, S., 2016. The new CGT withholding regime: More than meets the eye. Proctor,

The, 36(5), p.18.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Reference List:

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Barkoczy, S., Nethercott, L., Devos, K. and Richardson, G., 2016. Foundations Student Tax

Pack 3 2016. Oxford University Press Australia & New Zealand.

Barton, (2013). Management of the Australian Taxation Office's property portfolio. ACT:

Australian National Audit Office.

Braithwaite, V. ed., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

James, K., 2016. The Australian Taxation Office perspective on work-related travel expense

deductions for academics. International Journal of Critical Accounting, 8(5-6), pp.345-362.

Kenny, P. (2013). Australian tax 2013. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2013). Australian taxation law cases 2013. Pyrmont, N.S.W.: Thomson Reuters.

Milton, (2013). The taxpayers' guide 2013 & 2014. Qld.: Wrightbooks.

Morgan, A., Mortimer, C. and Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Newman, S., 2016. The new CGT withholding regime: More than meets the eye. Proctor,

The, 36(5), p.18.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.