HA3042 - Tax Law: Analyzing Income, FBT, and Capital Gains Scenario

VerifiedAdded on 2024/06/03

|14

|2514

|392

Case Study

AI Summary

This case study provides a detailed analysis of various Australian tax law scenarios. It begins by examining whether certain payments qualify as income from personal exertion, considering scenarios where the story was initially written for personal satisfaction. The study then calculates the taxable value of a car fringe benefit using the statutory formula. Furthermore, it explores the effect of a loan provided to a family member on the parent's assessable income, determining taxability based on arm's length principles. Finally, the study analyzes the net capital gain or loss resulting from the sale of a property, considering different scenarios such as selling to a daughter or if the property was owned by a company. Desklib offers more solved assignments for students.

HA3042

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction..........................................................................................................................................2

QUESTION 1: Discuss Whether or not the three payments are income from personal exertion.

Would your answer differ if she wrote the story for her own satisfaction and only decided to sell

it later?..............................................................................................................................................3

QUESTION 2: Calculate the taxable value of the car fringe benefit using the statutory formula..5

QUESTION 3: Discuss the effect on the assessable income of the parent........................................7

QUESTION 4:......................................................................................................................................8

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

2

Introduction..........................................................................................................................................2

QUESTION 1: Discuss Whether or not the three payments are income from personal exertion.

Would your answer differ if she wrote the story for her own satisfaction and only decided to sell

it later?..............................................................................................................................................3

QUESTION 2: Calculate the taxable value of the car fringe benefit using the statutory formula..5

QUESTION 3: Discuss the effect on the assessable income of the parent........................................7

QUESTION 4:......................................................................................................................................8

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

2

Introduction

In this report, it discusses the Australian tax laws according to different scenarios. This report

includes the different scenarios that are in first situation, it analyses the income of individual and

on that income tax is to be calculated. In second scenario, it discusses the benefits of FBT with

their calculation. The third situation deals with the loan amount, which is given to the family

members and calculates the assessable income with their impacts. In fourth scenario, it analyses

the amount of net capital gain and net capital loss.

3

In this report, it discusses the Australian tax laws according to different scenarios. This report

includes the different scenarios that are in first situation, it analyses the income of individual and

on that income tax is to be calculated. In second scenario, it discusses the benefits of FBT with

their calculation. The third situation deals with the loan amount, which is given to the family

members and calculates the assessable income with their impacts. In fourth scenario, it analyses

the amount of net capital gain and net capital loss.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1: Discuss Whether or not the three payments are income from personal

exertion. Would your answer differ if she wrote the story for her own satisfaction and only

decided to sell it later?

Facts of the case: This case is related to the Australian tax laws. The facts of the case are in

which a Hilary is a climber and the other party that is Daily Terror newspaper offers

$10,000. Hilary accepts this offer and writes the story and assigns the title, interest, right in

the copyright for $10,000. The daily terror newspaper published the story and Hilary

receives money for that. After writing the story she sells manuscript at $5000 to Mitchell

library and photographs for that she received $2000.

Law: According to the Australian tax laws, personal income is the income that can be

produced by the efforts or personal skills of individuals. According to the section 6 of

Income Tax Assessment Act, 1936 personal exertion or income includes the wages,

commissions, fees bonus, superannuation allowance, and retirement benefits. It can also be

asserted that any gratuities and allowances collected and any services provided by the

business can be run by the tax payer (ACCOUNTING, 2017).

Analysis:

From the above facts, it can be asserted that the Hilary wrote a story without the help of the

writer which depicts that she accepts the offers according to the terms and conditions and

also receive the payment. By this observation, it can be determined that it is the income

from personal exertion and it can be assesses as the ordinary income. It can also be

determined that for a taxpayer, who is holder of copyright they have to identify that whether

the copyright is income or capital asset in case of taxation. It can be stated that if the if the

holder is the writer or artist then in that case the copyright is treated as the taxable ordinary

income and in case if the individual is not a writer or artist then it will be recognized as the

capital assets(Stewart, 2017).

In the above case, the Hilary receives the money from the sale of manuscript to the Mitchell

library and receives the $5,000 and $2000 form the photographs of mountaineering. This

4

exertion. Would your answer differ if she wrote the story for her own satisfaction and only

decided to sell it later?

Facts of the case: This case is related to the Australian tax laws. The facts of the case are in

which a Hilary is a climber and the other party that is Daily Terror newspaper offers

$10,000. Hilary accepts this offer and writes the story and assigns the title, interest, right in

the copyright for $10,000. The daily terror newspaper published the story and Hilary

receives money for that. After writing the story she sells manuscript at $5000 to Mitchell

library and photographs for that she received $2000.

Law: According to the Australian tax laws, personal income is the income that can be

produced by the efforts or personal skills of individuals. According to the section 6 of

Income Tax Assessment Act, 1936 personal exertion or income includes the wages,

commissions, fees bonus, superannuation allowance, and retirement benefits. It can also be

asserted that any gratuities and allowances collected and any services provided by the

business can be run by the tax payer (ACCOUNTING, 2017).

Analysis:

From the above facts, it can be asserted that the Hilary wrote a story without the help of the

writer which depicts that she accepts the offers according to the terms and conditions and

also receive the payment. By this observation, it can be determined that it is the income

from personal exertion and it can be assesses as the ordinary income. It can also be

determined that for a taxpayer, who is holder of copyright they have to identify that whether

the copyright is income or capital asset in case of taxation. It can be stated that if the if the

holder is the writer or artist then in that case the copyright is treated as the taxable ordinary

income and in case if the individual is not a writer or artist then it will be recognized as the

capital assets(Stewart, 2017).

In the above case, the Hilary receives the money from the sale of manuscript to the Mitchell

library and receives the $5,000 and $2000 form the photographs of mountaineering. This

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

can be recognized as the ordinary income and it will be taxable as the income forms the

capital gains. From this it can be asserted that she did not have to pay any tax as per the

ordinary income taxation law.

In the second case, Hilary wrote the story for her satisfaction, after writing it she decided

that she will sell it later on. This is the situation of capital gains. Capital gains can be

defined as the profit that can be received after selling the property or investment. In this

case, Hilary sells her life story after sometimes so it can be recognized as the capital gain.

From the above analysis it can be determined that the in first case the income received from

the story is recognized as the ordinary taxable income and income received from the

manuscript and photograph can be recognized as the capital income(Siriwardane, 2018).

5

capital gains. From this it can be asserted that she did not have to pay any tax as per the

ordinary income taxation law.

In the second case, Hilary wrote the story for her satisfaction, after writing it she decided

that she will sell it later on. This is the situation of capital gains. Capital gains can be

defined as the profit that can be received after selling the property or investment. In this

case, Hilary sells her life story after sometimes so it can be recognized as the capital gain.

From the above analysis it can be determined that the in first case the income received from

the story is recognized as the ordinary taxable income and income received from the

manuscript and photograph can be recognized as the capital income(Siriwardane, 2018).

5

QUESTION 2: Calculate the taxable value of the car fringe benefit using the statutory

formula.

To calculate the taxable value, it is necessary to know the term of fringe Benefits tax. Fringe

benefits tax is the amount of tax payable that can be paid by employers for the benefits paid

to the employee in relation to wages or salary. The fringe benefits tax can be calculated on

the taxable value. The fringe benefits can be offered to the employee so that they work in

better manner. An employee may receive benefits in form of car, loans, payment of private

expenses (Jones, 2017).

FBT can be calculated by two methods that is :

Statutory method.

Operating cost method.

Statutory method:

Taxable value= [A*B*C/D]-E

A= It depicts the value of car.

B= Denotes the percentage value.

C= It denotes the number of days in the case of used car.

D= Number of days in FBT year.

E= Contribution of employee.

In the above scenario, the Eric is the employer and he provides the FBT to his employees. A

benefit of car is provided to the employee and that car can be used for the 183 days during

the financial year. The car travelled around the 16,000 km and Eric purchased it for at

$50,000. The employee spends around $1000 for the running of car(Stewart, 2017).

6

formula.

To calculate the taxable value, it is necessary to know the term of fringe Benefits tax. Fringe

benefits tax is the amount of tax payable that can be paid by employers for the benefits paid

to the employee in relation to wages or salary. The fringe benefits tax can be calculated on

the taxable value. The fringe benefits can be offered to the employee so that they work in

better manner. An employee may receive benefits in form of car, loans, payment of private

expenses (Jones, 2017).

FBT can be calculated by two methods that is :

Statutory method.

Operating cost method.

Statutory method:

Taxable value= [A*B*C/D]-E

A= It depicts the value of car.

B= Denotes the percentage value.

C= It denotes the number of days in the case of used car.

D= Number of days in FBT year.

E= Contribution of employee.

In the above scenario, the Eric is the employer and he provides the FBT to his employees. A

benefit of car is provided to the employee and that car can be used for the 183 days during

the financial year. The car travelled around the 16,000 km and Eric purchased it for at

$50,000. The employee spends around $1000 for the running of car(Stewart, 2017).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

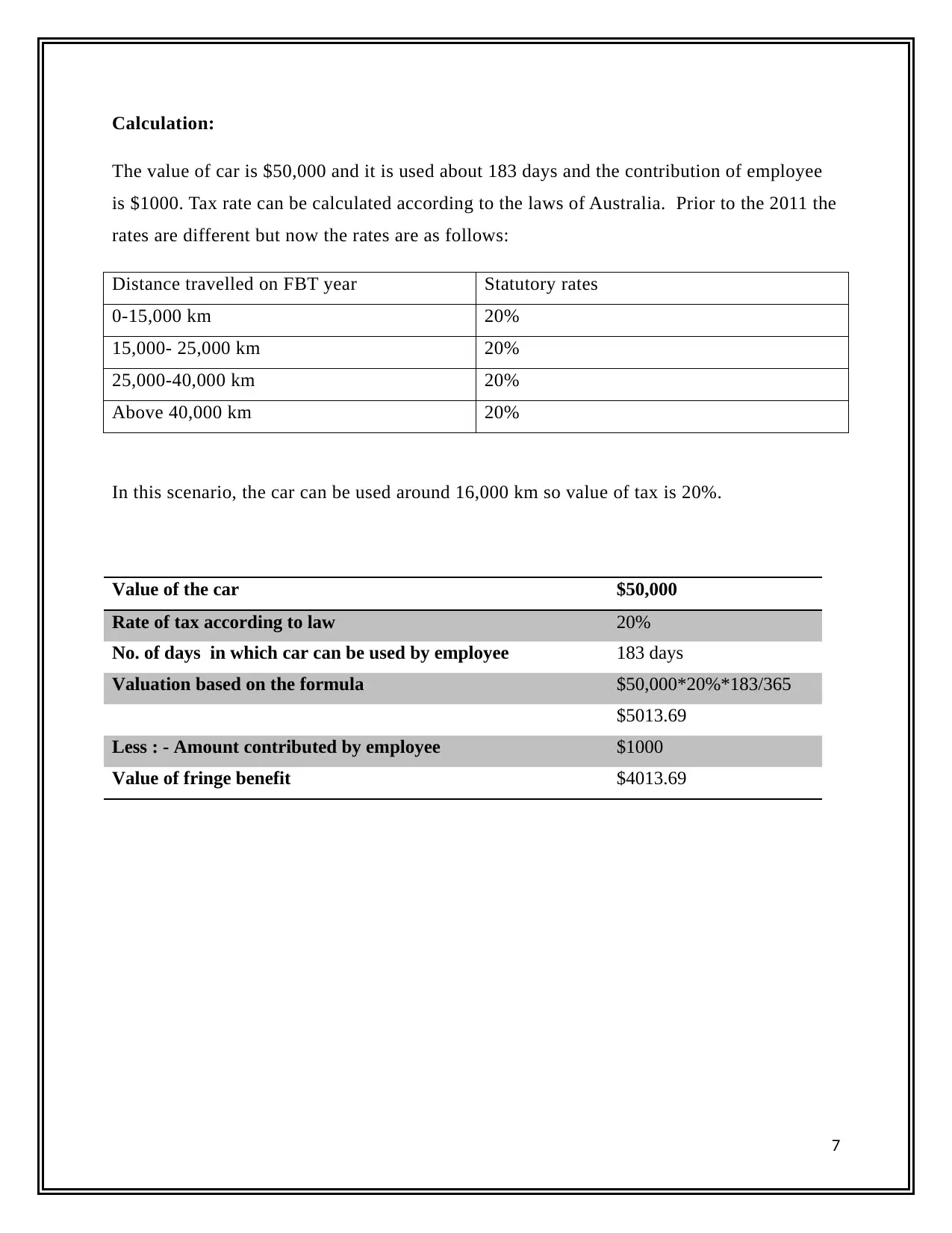

Calculation:

The value of car is $50,000 and it is used about 183 days and the contribution of employee

is $1000. Tax rate can be calculated according to the laws of Australia. Prior to the 2011 the

rates are different but now the rates are as follows:

Distance travelled on FBT year Statutory rates

0-15,000 km 20%

15,000- 25,000 km 20%

25,000-40,000 km 20%

Above 40,000 km 20%

In this scenario, the car can be used around 16,000 km so value of tax is 20%.

Value of the car $50,000

Rate of tax according to law 20%

No. of days in which car can be used by employee 183 days

Valuation based on the formula $50,000*20%*183/365

$5013.69

Less : - Amount contributed by employee $1000

Value of fringe benefit $4013.69

7

The value of car is $50,000 and it is used about 183 days and the contribution of employee

is $1000. Tax rate can be calculated according to the laws of Australia. Prior to the 2011 the

rates are different but now the rates are as follows:

Distance travelled on FBT year Statutory rates

0-15,000 km 20%

15,000- 25,000 km 20%

25,000-40,000 km 20%

Above 40,000 km 20%

In this scenario, the car can be used around 16,000 km so value of tax is 20%.

Value of the car $50,000

Rate of tax according to law 20%

No. of days in which car can be used by employee 183 days

Valuation based on the formula $50,000*20%*183/365

$5013.69

Less : - Amount contributed by employee $1000

Value of fringe benefit $4013.69

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3: Discuss the effect on the assessable income of the parent.

Facts of the case: In this scenario, client is the parents who provide money to their son as the

loan. The agreement was made orally that the son will repay $ 50,000 at the end of five years.

There was no agreement between the parties regarding the loan and security. Apart from that the

client tell to her son to not to pay interest, but still amount was paid by the son that can be equal

to the 5% on the borrowed amount.

Analysis:

In order to identify the taxability of loan that was granted to the family members or relative, it is

necessary to understand the transaction and their operation that is their price. In case, if the loan

is carried at the non-arm length then it should be considered as the assessable income.

According to section 295-550 of ITAA 11997, the loan which is recognized as the non-arm’s

length income that is taxable and that can be included in the assessable income of tax payer

(Jones, 2017).

In the given scenario, it can be determined that client provide the loan to son without any

interest, so it cannot be treated as the income. The son does not have any right to pay interest as

he is not legally bound to pay the interest to mother as he does not legally bound to pay the

interest and they did not have any written agreement regarding the interest.

The son paid interest amount to their mother. He pay the interest at the rate of 5% p.a , so the

total amount of interest for two years that is $4000 and that can be given to the client that is

(mother). The client received the amount of interest that is $4000 without the right, so in this

case it is asserted that it is not ordinary income. As per the provision of taxation law, the tax can

be charged when the amount of income exceeds the limit. In this scenario, the interest received

by mother is less that’s why it is not charged as the tax(Jacob, 2018).

8

Facts of the case: In this scenario, client is the parents who provide money to their son as the

loan. The agreement was made orally that the son will repay $ 50,000 at the end of five years.

There was no agreement between the parties regarding the loan and security. Apart from that the

client tell to her son to not to pay interest, but still amount was paid by the son that can be equal

to the 5% on the borrowed amount.

Analysis:

In order to identify the taxability of loan that was granted to the family members or relative, it is

necessary to understand the transaction and their operation that is their price. In case, if the loan

is carried at the non-arm length then it should be considered as the assessable income.

According to section 295-550 of ITAA 11997, the loan which is recognized as the non-arm’s

length income that is taxable and that can be included in the assessable income of tax payer

(Jones, 2017).

In the given scenario, it can be determined that client provide the loan to son without any

interest, so it cannot be treated as the income. The son does not have any right to pay interest as

he is not legally bound to pay the interest to mother as he does not legally bound to pay the

interest and they did not have any written agreement regarding the interest.

The son paid interest amount to their mother. He pay the interest at the rate of 5% p.a , so the

total amount of interest for two years that is $4000 and that can be given to the client that is

(mother). The client received the amount of interest that is $4000 without the right, so in this

case it is asserted that it is not ordinary income. As per the provision of taxation law, the tax can

be charged when the amount of income exceeds the limit. In this scenario, the interest received

by mother is less that’s why it is not charged as the tax(Jacob, 2018).

8

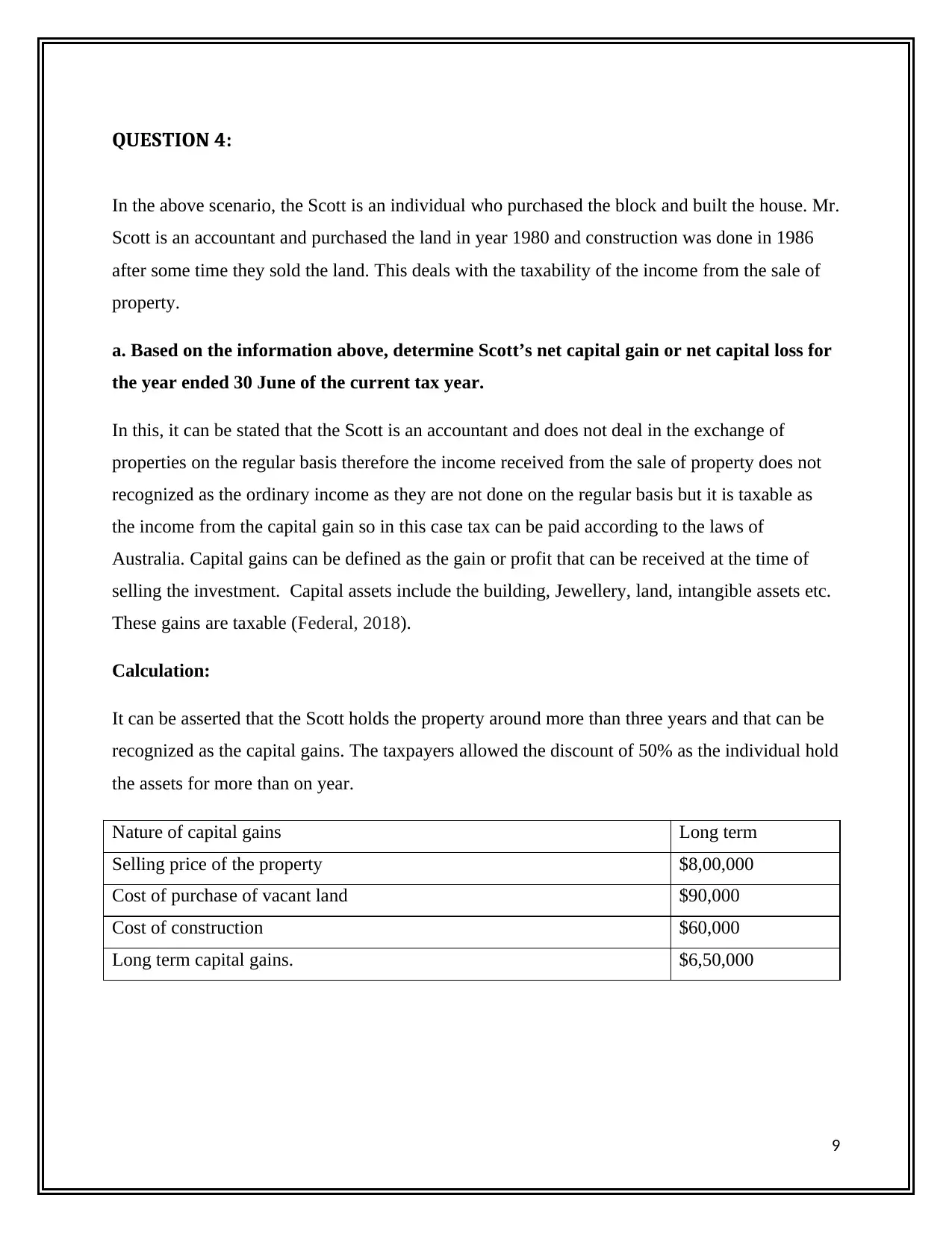

QUESTION 4:

In the above scenario, the Scott is an individual who purchased the block and built the house. Mr.

Scott is an accountant and purchased the land in year 1980 and construction was done in 1986

after some time they sold the land. This deals with the taxability of the income from the sale of

property.

a. Based on the information above, determine Scott’s net capital gain or net capital loss for

the year ended 30 June of the current tax year.

In this, it can be stated that the Scott is an accountant and does not deal in the exchange of

properties on the regular basis therefore the income received from the sale of property does not

recognized as the ordinary income as they are not done on the regular basis but it is taxable as

the income from the capital gain so in this case tax can be paid according to the laws of

Australia. Capital gains can be defined as the gain or profit that can be received at the time of

selling the investment. Capital assets include the building, Jewellery, land, intangible assets etc.

These gains are taxable (Federal, 2018).

Calculation:

It can be asserted that the Scott holds the property around more than three years and that can be

recognized as the capital gains. The taxpayers allowed the discount of 50% as the individual hold

the assets for more than on year.

Nature of capital gains Long term

Selling price of the property $8,00,000

Cost of purchase of vacant land $90,000

Cost of construction $60,000

Long term capital gains. $6,50,000

9

In the above scenario, the Scott is an individual who purchased the block and built the house. Mr.

Scott is an accountant and purchased the land in year 1980 and construction was done in 1986

after some time they sold the land. This deals with the taxability of the income from the sale of

property.

a. Based on the information above, determine Scott’s net capital gain or net capital loss for

the year ended 30 June of the current tax year.

In this, it can be stated that the Scott is an accountant and does not deal in the exchange of

properties on the regular basis therefore the income received from the sale of property does not

recognized as the ordinary income as they are not done on the regular basis but it is taxable as

the income from the capital gain so in this case tax can be paid according to the laws of

Australia. Capital gains can be defined as the gain or profit that can be received at the time of

selling the investment. Capital assets include the building, Jewellery, land, intangible assets etc.

These gains are taxable (Federal, 2018).

Calculation:

It can be asserted that the Scott holds the property around more than three years and that can be

recognized as the capital gains. The taxpayers allowed the discount of 50% as the individual hold

the assets for more than on year.

Nature of capital gains Long term

Selling price of the property $8,00,000

Cost of purchase of vacant land $90,000

Cost of construction $60,000

Long term capital gains. $6,50,000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

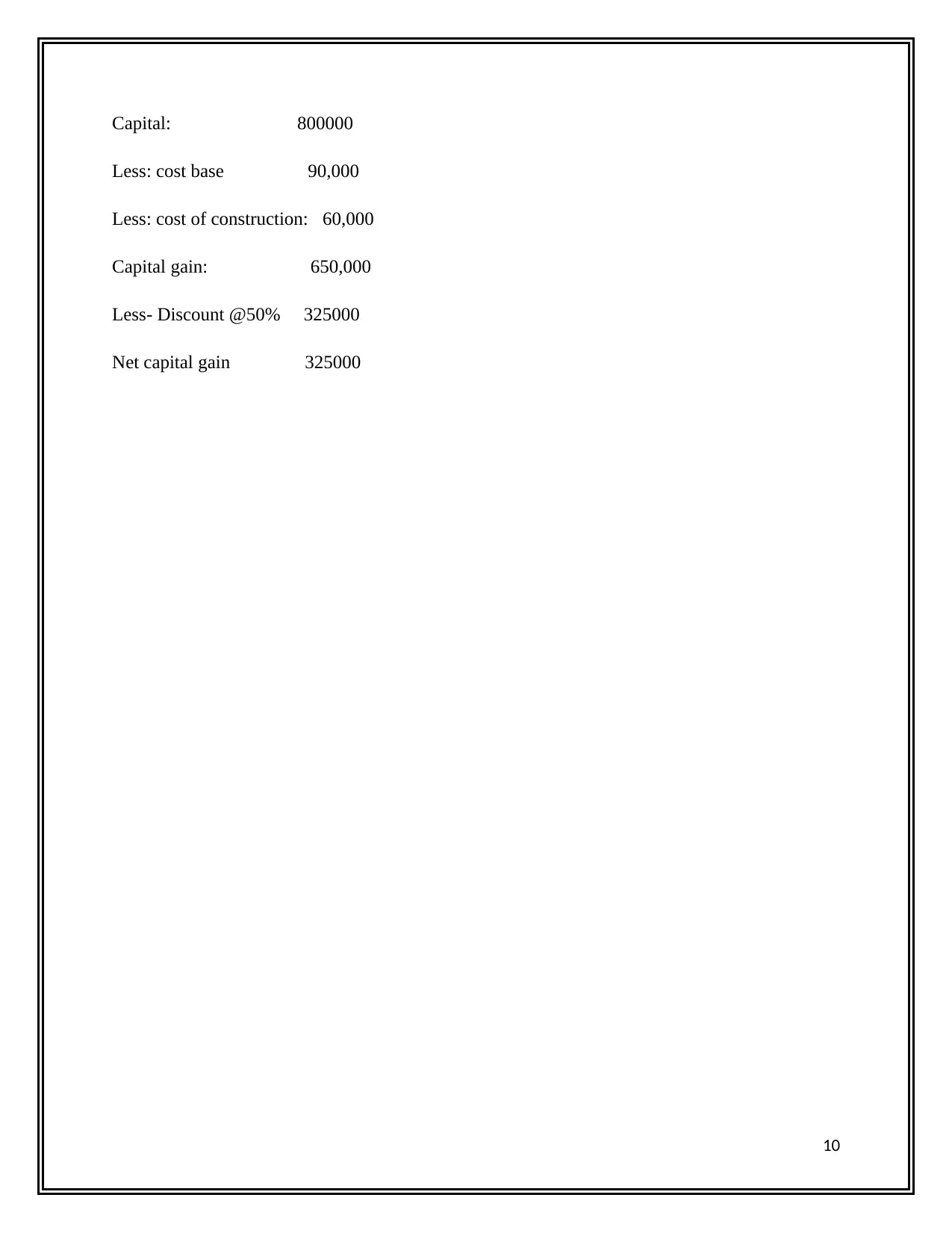

Capital: 800000

Less: cost base 90,000

Less: cost of construction: 60,000

Capital gain: 650,000

Less- Discount @50% 325000

Net capital gain 325000

10

Less: cost base 90,000

Less: cost of construction: 60,000

Capital gain: 650,000

Less- Discount @50% 325000

Net capital gain 325000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b. How would your answer to (a) differ if Scott sold the property to his daughter for $

200,000?

If the Scott sold the property to his daughter, there will be no of capital gains as the capital has

do not arise in case of inheritance and gifts. It can be stated that if the property is disposed and if

it is given without receiving any amount of interest then in that case, it will be recognized as the

capital and that can be equal to the market value . If the property is sold to the members of

family then in that case the sale can be recognized on the market value at the date of disposal.

In the above scenario, the Scott sell the property to her daughter and that costs to $200000 and

the total cost of property is $800000 and that amount is recognized as the capital. The net capital

is same as (a) that is 325000 and it is not different (Edge, 2017).

11

200,000?

If the Scott sold the property to his daughter, there will be no of capital gains as the capital has

do not arise in case of inheritance and gifts. It can be stated that if the property is disposed and if

it is given without receiving any amount of interest then in that case, it will be recognized as the

capital and that can be equal to the market value . If the property is sold to the members of

family then in that case the sale can be recognized on the market value at the date of disposal.

In the above scenario, the Scott sell the property to her daughter and that costs to $200000 and

the total cost of property is $800000 and that amount is recognized as the capital. The net capital

is same as (a) that is 325000 and it is not different (Edge, 2017).

11

c. How would your answer to (a) differ if the owner of the property was a company instead

of an individual?

In this fact, if the owner is a company then it depends on the facts and circumstances that

whether the company is engaged in the real estate or not. In this case, if firm engaged in the real

estate then in that case income from transfer of property that will be taxable as the normal

income otherwise it is taxable income from the capital gains. There is another aspect on that it

can be stated s that it is different as there is 50% discount on the capital gain and that cannot be

allowed to the company, it can be allowed to the individual(Biasin and Quaranta, 2018).

12

of an individual?

In this fact, if the owner is a company then it depends on the facts and circumstances that

whether the company is engaged in the real estate or not. In this case, if firm engaged in the real

estate then in that case income from transfer of property that will be taxable as the normal

income otherwise it is taxable income from the capital gains. There is another aspect on that it

can be stated s that it is different as there is 50% discount on the capital gain and that cannot be

allowed to the company, it can be allowed to the individual(Biasin and Quaranta, 2018).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.