Taxation Law: Capital Gains, Fringe Benefits, and Property

VerifiedAdded on 2020/04/01

|9

|1815

|35

Report

AI Summary

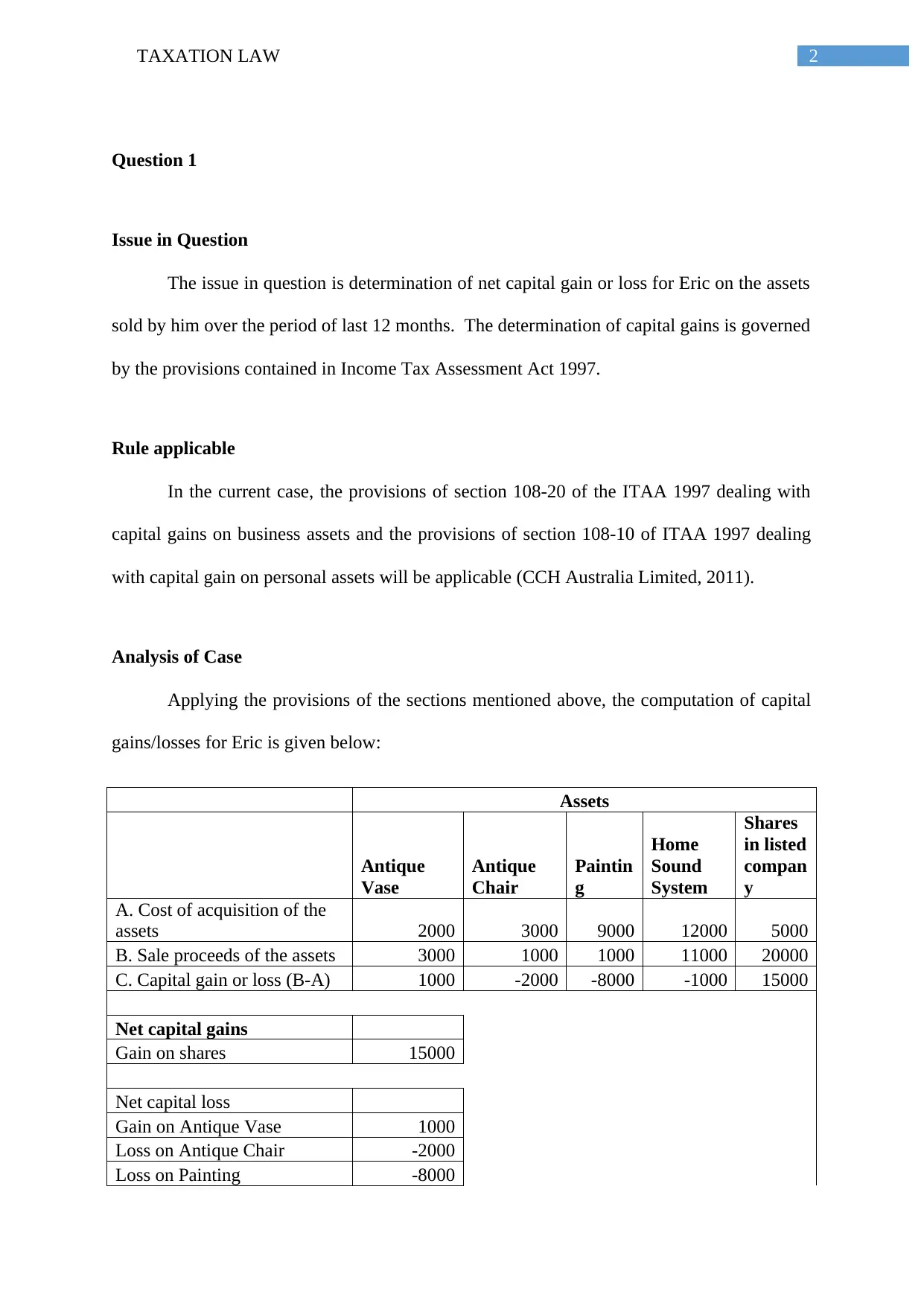

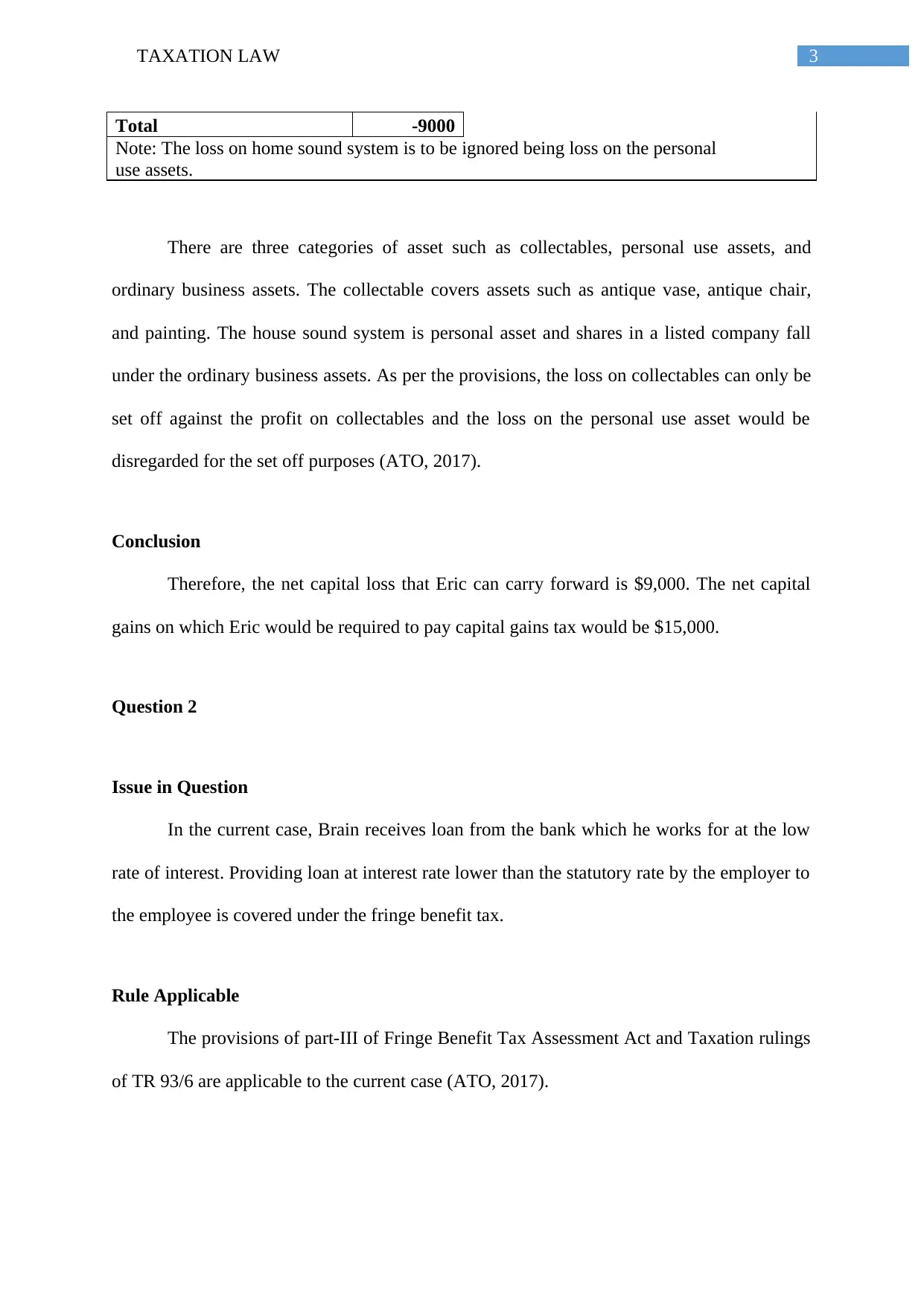

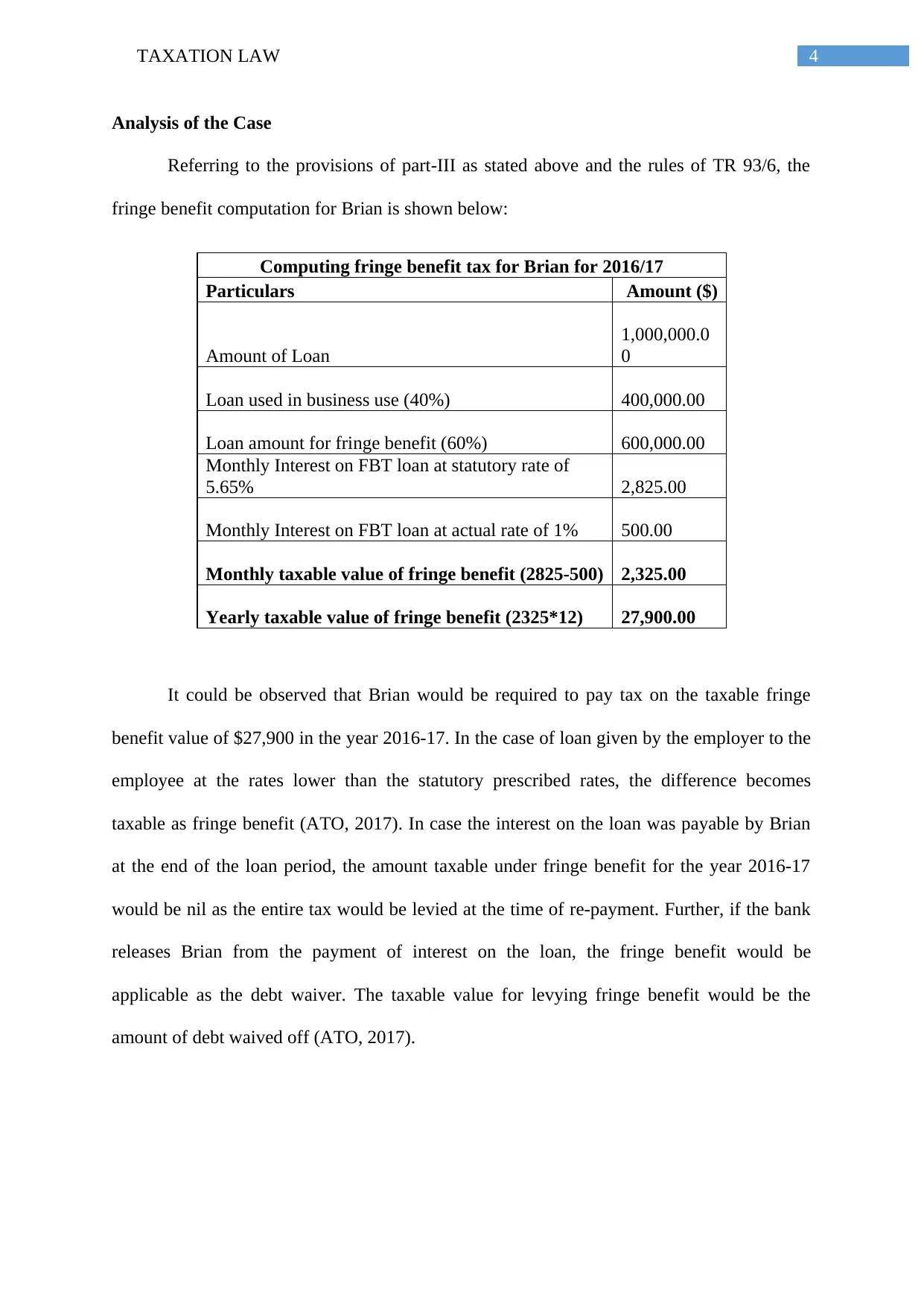

This report provides an analysis of several key areas within Australian taxation law. It begins by addressing the determination of net capital gains or losses, examining the application of the Income Tax Assessment Act 1997 to various assets, including collectables, personal use assets, and business assets. The report then delves into fringe benefit tax (FBT), specifically concerning loans provided by employers to employees at below-market interest rates, calculating the taxable value of the fringe benefit. Furthermore, the report explores the taxation of jointly owned rental properties, analyzing how profits and losses are distributed among co-owners, referencing relevant taxation rulings and case law. It also touches upon the principle of tax avoidance as established in IRC v Duke of Westminster. Finally, the report examines the tax implications of selling felled timber from a land owner's property, determining whether the proceeds constitute taxable income under primary production rules. The analysis incorporates relevant sections of the Income Tax Assessment Act and relevant taxation rulings, providing a comprehensive overview of the topics covered.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.