Taxation Project: Australian Residency and Tax Liability Analysis

VerifiedAdded on 2020/10/22

|9

|2495

|349

Project

AI Summary

This taxation project delves into the intricacies of Australian tax law, focusing on the determination of an individual's residency status and its subsequent impact on tax liability. The project examines various residency tests, including the resides test, domicile test, and 183-day test, to ascertain whether an individual qualifies as an Australian resident. It then analyzes the assessability of different income sources, such as salary, interest, and rental income, earned both domestically and internationally. Furthermore, the project explores the calculation of taxable income, incorporating deductions for expenses related to business operations and superannuation contributions. The project culminates in the calculation of net tax payable, considering various tax provisions and rates applicable to different income brackets. It emphasizes the importance of understanding tax treaties and the implications of treating income-generating activities as a business versus a hobby, providing valuable insights into tax planning and compliance.

Taxation Project

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Analysing residential status of individual for tax purpose calculation of tax liability as per

the residency status......................................................................................................................1

2. Advising assessability of various incomes earned from the British publisher........................2

TASK 2............................................................................................................................................3

Calculating minimum taxable income and net tax payable or refundable amount for the year

ended 30 June 2019.....................................................................................................................3

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Analysing residential status of individual for tax purpose calculation of tax liability as per

the residency status......................................................................................................................1

2. Advising assessability of various incomes earned from the British publisher........................2

TASK 2............................................................................................................................................3

Calculating minimum taxable income and net tax payable or refundable amount for the year

ended 30 June 2019.....................................................................................................................3

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

The term taxation refers to a major source of revenue of government. It levies upon each

individual person including individuals and entities of the country. They need to pay a certain

sum to the government on the basis of profit or income generated by them. The present study

shows calculation of tax liability of the individual on the basis of residence status. It provides

information about accessibility of various receipts as per taxation law. Further, the study also

shows calculation of tax liability of an individual using various taxation provisions. The

calculation of tax liability is being based on numerous provisions relating to deduction,

exemption, etc.

TASK 1

1. Analysing residential status of individual for tax purpose calculation of tax liability as per the

residency status.

Residency status of individual

As per income tax rulings issued by the Australian Taxation OfficeBefore

determining the taxation liability of any individual, it is necessary to determine the residency

status first, as levy of tax varies as per the residential status of the individual (Eslak, 2015). The

Australian government has provided various requirements on the basis of which residential status

of an individual can be determined.

The Australian government provides some tests that needs to be fulfilled by an

individuals for considering themselves as ordinary residence of Australia. These tests can be

analysed as under:

Resides test: If an individual is born in Australia or his parents are born in Australia, the

individual would be termed as Australian ordinary resident (Ngo and et.al., 2019). Any of the the

individual who does not satisfy the terms of resides test, would be needed to satisfy other tests.

Domicile test: Domicile test says that if any individual has purchased any home for

permanent residential purpose, the individual will said to be an ordinary resident for

taxation purpose.

183 days test: Further, as per ITAA 1997 rules relating to the 183 days tests, in case,

any individual has resided at least 183 days during a specific time period, the individual

would be treated as resident of Australia for tax purposes.

1

The term taxation refers to a major source of revenue of government. It levies upon each

individual person including individuals and entities of the country. They need to pay a certain

sum to the government on the basis of profit or income generated by them. The present study

shows calculation of tax liability of the individual on the basis of residence status. It provides

information about accessibility of various receipts as per taxation law. Further, the study also

shows calculation of tax liability of an individual using various taxation provisions. The

calculation of tax liability is being based on numerous provisions relating to deduction,

exemption, etc.

TASK 1

1. Analysing residential status of individual for tax purpose calculation of tax liability as per the

residency status.

Residency status of individual

As per income tax rulings issued by the Australian Taxation OfficeBefore

determining the taxation liability of any individual, it is necessary to determine the residency

status first, as levy of tax varies as per the residential status of the individual (Eslak, 2015). The

Australian government has provided various requirements on the basis of which residential status

of an individual can be determined.

The Australian government provides some tests that needs to be fulfilled by an

individuals for considering themselves as ordinary residence of Australia. These tests can be

analysed as under:

Resides test: If an individual is born in Australia or his parents are born in Australia, the

individual would be termed as Australian ordinary resident (Ngo and et.al., 2019). Any of the the

individual who does not satisfy the terms of resides test, would be needed to satisfy other tests.

Domicile test: Domicile test says that if any individual has purchased any home for

permanent residential purpose, the individual will said to be an ordinary resident for

taxation purpose.

183 days test: Further, as per ITAA 1997 rules relating to the 183 days tests, in case,

any individual has resided at least 183 days during a specific time period, the individual

would be treated as resident of Australia for tax purposes.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Superannuation test: Moreover, if the individual; does not satisfies any of the above

test. But is working as an employee of any government service agencies of Australia

(Sadiq, 2019), the individual would need to pay tax as resident of Australia.

In the present scenario, as Dr. Scott Piner stayed in Australia till 22nd January 2019, he

fulfills the 183 days for the year ending on June 2019. Further, he also satisfies the domicile test.

Therefore, Dr. Scott Piner can be termed as a resident of Australia for the taxation purpose.

Further, being an Australian resident, Piner will need to pay tax on each income earned

by him in the Australia. Therefore, he will need to pay tax on the amount of salary received from

the hospital in Australia, interest from the Australian term deposit, rental income from the

property situated in Melbourne will be taxable in the Australia.

Further, as per the common rule of taxation law, as the tax is usually paid in the country

in which the income has been generated. Therefore, taxation of foreign income can attract the

double taxation over an income. In this regard, the Australian government has signed agreement

and treaty with 40 countries. In order to this, the foreign income generated from those countries

would not be taxable in Australia.

Moreover, as Belgium is one of those country with whom Australian Government have

signed their treaties (Perl and Burke, 2018). In this regard, it can be analysed that all the income

generated by Piner from Belgium including salaries, interest, payment from publishers, etc.

would be taxable in Australia. Although, the amount equal to the tax paid by them in Australia

can be claimed by him.

Although, being an Australian resident, the Piler will need to disclose each income

earned by him during a specific time period.

2. Advising assessability of various incomes earned from the British publisher

As per ITAA 1936, An Australian resident needs to pay tax on the worldwide income. In

this regard, income earned from both domestic and foreign source would be taxable in the

Australia for resident individuals. Although, income generated from the countries with which

Australia has signed treaty, falls under the liability of paying tax in Australia. Although, the

individual has right to gain input tax credit equal to the amount of tax paid by them in those

countries (Woellner and et.al., 2016). In addition, each income must be disclosed in the

Australian taxation return by the Australian ordinary resident. In this order, Dr. Scott Piner,

being an Australian resident, will be liable to pay tax on the income earned by him in the

2

test. But is working as an employee of any government service agencies of Australia

(Sadiq, 2019), the individual would need to pay tax as resident of Australia.

In the present scenario, as Dr. Scott Piner stayed in Australia till 22nd January 2019, he

fulfills the 183 days for the year ending on June 2019. Further, he also satisfies the domicile test.

Therefore, Dr. Scott Piner can be termed as a resident of Australia for the taxation purpose.

Further, being an Australian resident, Piner will need to pay tax on each income earned

by him in the Australia. Therefore, he will need to pay tax on the amount of salary received from

the hospital in Australia, interest from the Australian term deposit, rental income from the

property situated in Melbourne will be taxable in the Australia.

Further, as per the common rule of taxation law, as the tax is usually paid in the country

in which the income has been generated. Therefore, taxation of foreign income can attract the

double taxation over an income. In this regard, the Australian government has signed agreement

and treaty with 40 countries. In order to this, the foreign income generated from those countries

would not be taxable in Australia.

Moreover, as Belgium is one of those country with whom Australian Government have

signed their treaties (Perl and Burke, 2018). In this regard, it can be analysed that all the income

generated by Piner from Belgium including salaries, interest, payment from publishers, etc.

would be taxable in Australia. Although, the amount equal to the tax paid by them in Australia

can be claimed by him.

Although, being an Australian resident, the Piler will need to disclose each income

earned by him during a specific time period.

2. Advising assessability of various incomes earned from the British publisher

As per ITAA 1936, An Australian resident needs to pay tax on the worldwide income. In

this regard, income earned from both domestic and foreign source would be taxable in the

Australia for resident individuals. Although, income generated from the countries with which

Australia has signed treaty, falls under the liability of paying tax in Australia. Although, the

individual has right to gain input tax credit equal to the amount of tax paid by them in those

countries (Woellner and et.al., 2016). In addition, each income must be disclosed in the

Australian taxation return by the Australian ordinary resident. In this order, Dr. Scott Piner,

being an Australian resident, will be liable to pay tax on the income earned by him in the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Belgium. Further, he will have a right to get input tax credit upto the amount of tax that would be

paid by him in Belgium.

As per the provisions of Australian taxation law of ITAA 1997, expenses incurred for

operation of business are able to be claimed as deduction while calculating the tax amount to be

paid. Although, for getting the deduction, it is important that income against which the expense

has been incurred, must be liable for the payment of tax. In addition, income tax rulings issued

by the Australian Taxation Office Expenses against any exempted income cannot be claimed

for deduction. In addition, all those incomes on which tax has already been deducted by te

taxation authorities at the time of generation of the income, would be able to claim exemptions

while calculating the tax liability of the business.

Further, as Dr. Scott Piner will get payment from the publishers against his writing, it

would be covered under the business rather than hobby. Therefore, Piner will need to pay tax on

the income generated from the writing business. Further, as income earned from writing are

taxable incomes, the expenses incurred for the operation of the business would be deductible

while calculating the tax liability. In addition, as the income generated through publishing book

would be taxable in Australia, all the expenses incurred regarding book including Airfares,

computer hiring expenses, etc. would be assessable in Australia. Moreover, being operating

expenses, Piner would be able to get the deduction against these expenses as well.

In this regard, it can be advised to Dr. Scott Piner that he can open a business of writing

book in Belgium (Kennedy and et.al., 2017). Although, income generated from the business

would be taxable in both Beligium as well as Australia, but due to treaty signed between

Australia and Belgium, he would get credit equal to the amount of tax paid by him in the

Belgium.

In this regard, the double taxation would be eliminated. Furthermore, all the expenses

incurred by him for publishing book and for other operating activities of the business will be able

to claim as deduction against the income generated by the business as per the Australian taxation

law. All these benefits could not be get by him if he treats writing as his hobby. In order to it,

Dr, Scott Piner can be advised to treat the writing as his business rather than hobby.

3

paid by him in Belgium.

As per the provisions of Australian taxation law of ITAA 1997, expenses incurred for

operation of business are able to be claimed as deduction while calculating the tax amount to be

paid. Although, for getting the deduction, it is important that income against which the expense

has been incurred, must be liable for the payment of tax. In addition, income tax rulings issued

by the Australian Taxation Office Expenses against any exempted income cannot be claimed

for deduction. In addition, all those incomes on which tax has already been deducted by te

taxation authorities at the time of generation of the income, would be able to claim exemptions

while calculating the tax liability of the business.

Further, as Dr. Scott Piner will get payment from the publishers against his writing, it

would be covered under the business rather than hobby. Therefore, Piner will need to pay tax on

the income generated from the writing business. Further, as income earned from writing are

taxable incomes, the expenses incurred for the operation of the business would be deductible

while calculating the tax liability. In addition, as the income generated through publishing book

would be taxable in Australia, all the expenses incurred regarding book including Airfares,

computer hiring expenses, etc. would be assessable in Australia. Moreover, being operating

expenses, Piner would be able to get the deduction against these expenses as well.

In this regard, it can be advised to Dr. Scott Piner that he can open a business of writing

book in Belgium (Kennedy and et.al., 2017). Although, income generated from the business

would be taxable in both Beligium as well as Australia, but due to treaty signed between

Australia and Belgium, he would get credit equal to the amount of tax paid by him in the

Belgium.

In this regard, the double taxation would be eliminated. Furthermore, all the expenses

incurred by him for publishing book and for other operating activities of the business will be able

to claim as deduction against the income generated by the business as per the Australian taxation

law. All these benefits could not be get by him if he treats writing as his hobby. In order to it,

Dr, Scott Piner can be advised to treat the writing as his business rather than hobby.

3

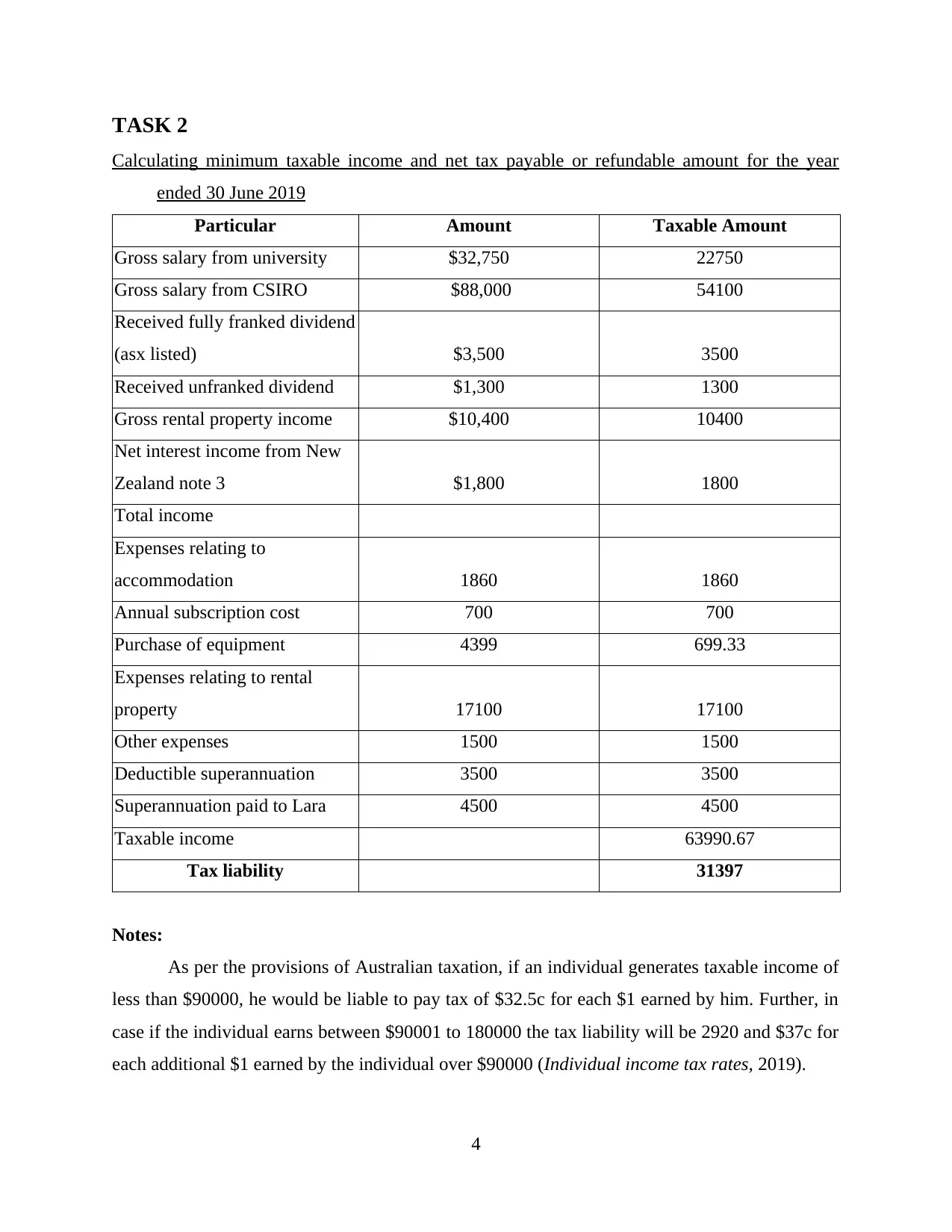

TASK 2

Calculating minimum taxable income and net tax payable or refundable amount for the year

ended 30 June 2019

Particular Amount Taxable Amount

Gross salary from university $32,750 22750

Gross salary from CSIRO $88,000 54100

Received fully franked dividend

(asx listed) $3,500 3500

Received unfranked dividend $1,300 1300

Gross rental property income $10,400 10400

Net interest income from New

Zealand note 3 $1,800 1800

Total income

Expenses relating to

accommodation 1860 1860

Annual subscription cost 700 700

Purchase of equipment 4399 699.33

Expenses relating to rental

property 17100 17100

Other expenses 1500 1500

Deductible superannuation 3500 3500

Superannuation paid to Lara 4500 4500

Taxable income 63990.67

Tax liability 31397

Notes:

As per the provisions of Australian taxation, if an individual generates taxable income of

less than $90000, he would be liable to pay tax of $32.5c for each $1 earned by him. Further, in

case if the individual earns between $90001 to 180000 the tax liability will be 2920 and $37c for

each additional $1 earned by the individual over $90000 (Individual income tax rates, 2019).

4

Calculating minimum taxable income and net tax payable or refundable amount for the year

ended 30 June 2019

Particular Amount Taxable Amount

Gross salary from university $32,750 22750

Gross salary from CSIRO $88,000 54100

Received fully franked dividend

(asx listed) $3,500 3500

Received unfranked dividend $1,300 1300

Gross rental property income $10,400 10400

Net interest income from New

Zealand note 3 $1,800 1800

Total income

Expenses relating to

accommodation 1860 1860

Annual subscription cost 700 700

Purchase of equipment 4399 699.33

Expenses relating to rental

property 17100 17100

Other expenses 1500 1500

Deductible superannuation 3500 3500

Superannuation paid to Lara 4500 4500

Taxable income 63990.67

Tax liability 31397

Notes:

As per the provisions of Australian taxation, if an individual generates taxable income of

less than $90000, he would be liable to pay tax of $32.5c for each $1 earned by him. Further, in

case if the individual earns between $90001 to 180000 the tax liability will be 2920 and $37c for

each additional $1 earned by the individual over $90000 (Individual income tax rates, 2019).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition, if the individual’s taxable income comes over $180001, he would need to pay

tax of 62550 and additional 45c for each additional $1earned by him.

In the present case, as Income of Mr. Max falls between 90001 to 180000, he would

need to pay the tax of $29250 and additional 37c for each additional $1 earned by him during the

specific taxation period.

For the purpose of calculating taxable income, all the incomes against which the PAYG

Tax has been deducted, will not be taken into consideration while calculating the taxable income

of Max. further, as superannuation contribution is allowed as deduction against the taxable

income of an assesse, while calculating the taxable income of max, the amount will be deducted

from the taxable income.

In case, any equipment or asset is hold by a business organization, it can claim deduction

equal to the amount of depreciation for the specific time period. Further, in case, the asset or the

equipment is partially hold by the company, the amount of depreciation equal to the portion of

asset used for the business purpose would be able to claim as deduction (Sharkey and Murray

2016) in this order, Max can claim deduction for asset equal to the amount of asset used for the

business purpose for the business purpose during the year.

In addition, in case if interest amount is earned by any business entity on which the tax

has already been deducted, the amount by the taxation authorities at the time of getting interest

can be claimed as deduction in the calculation of amount of tax to be paid.

In this order, while considering all the above taxation provisions and clauses, relating to

tax liability of the business organization, tax amount to be paid by Max is being calculated.

Further, with the help of interpretation of the tax calculation of Mr. Max, it canbe interpret that,

after claiming all the deductions and exemptions available to Max, the taxable amount comes to

$63990.67. in this order Max falls in the slab of $90001 to 180000. While calculating the taxable

amount to be paid by Max, it can be interpreted that Max will need to pay tax of $31397 for the

year ended on June 2019.

CONCLUSION

From the analysis of the above taxation project, it can be concluded that residency status

of an individual plays a vital role in determination of tax liability of an individual. The overall

calculation of the taxable income of individual depends upon the residential status of the

5

tax of 62550 and additional 45c for each additional $1earned by him.

In the present case, as Income of Mr. Max falls between 90001 to 180000, he would

need to pay the tax of $29250 and additional 37c for each additional $1 earned by him during the

specific taxation period.

For the purpose of calculating taxable income, all the incomes against which the PAYG

Tax has been deducted, will not be taken into consideration while calculating the taxable income

of Max. further, as superannuation contribution is allowed as deduction against the taxable

income of an assesse, while calculating the taxable income of max, the amount will be deducted

from the taxable income.

In case, any equipment or asset is hold by a business organization, it can claim deduction

equal to the amount of depreciation for the specific time period. Further, in case, the asset or the

equipment is partially hold by the company, the amount of depreciation equal to the portion of

asset used for the business purpose would be able to claim as deduction (Sharkey and Murray

2016) in this order, Max can claim deduction for asset equal to the amount of asset used for the

business purpose for the business purpose during the year.

In addition, in case if interest amount is earned by any business entity on which the tax

has already been deducted, the amount by the taxation authorities at the time of getting interest

can be claimed as deduction in the calculation of amount of tax to be paid.

In this order, while considering all the above taxation provisions and clauses, relating to

tax liability of the business organization, tax amount to be paid by Max is being calculated.

Further, with the help of interpretation of the tax calculation of Mr. Max, it canbe interpret that,

after claiming all the deductions and exemptions available to Max, the taxable amount comes to

$63990.67. in this order Max falls in the slab of $90001 to 180000. While calculating the taxable

amount to be paid by Max, it can be interpreted that Max will need to pay tax of $31397 for the

year ended on June 2019.

CONCLUSION

From the analysis of the above taxation project, it can be concluded that residency status

of an individual plays a vital role in determination of tax liability of an individual. The overall

calculation of the taxable income of individual depends upon the residential status of the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

individual. A residence of Australia needs to fulfill any one of the residency test provided by the

Government of Australia.

Moreover, it has been concluded that if a person generates income from any activity, it

would be relate as a business rather than hobby for the taxation purpose in Australian taxation

system. all the operating expenses incurred for running of a business can be claimed as deduction

in the Australian taxation system.

Further the study has also concluded that there are numerous taxation provisions

regarding taxability of various incomes and expenses of the company on the basis of which

taxability of any income or deductibility of any expenses incurred by the business is being

decided.

6

Government of Australia.

Moreover, it has been concluded that if a person generates income from any activity, it

would be relate as a business rather than hobby for the taxation purpose in Australian taxation

system. all the operating expenses incurred for running of a business can be claimed as deduction

in the Australian taxation system.

Further the study has also concluded that there are numerous taxation provisions

regarding taxability of various incomes and expenses of the company on the basis of which

taxability of any income or deductibility of any expenses incurred by the business is being

decided.

6

REFERENCES

Books and Journals

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian taxation:

beware the fine balance of social psychological and rule of law principles. Austl. Tax

F. .31. p.63.

Kennedy, T. and et.al., 2017. Does income inequality hinder economic growth? New evidence

using Australian taxation statistics. Economic Modelling. 65. pp.119-128.

Woellner, R. and et.al., 2016. Australian Taxation Law 2016. OUP Catalogue.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Perl, A. and Burke, M.I., 2018. Does institutional entrenchment shape instrument adjustment?:

Assessing instrument constituency influences on American and Australian motor fuel

taxation. Policy and Society. 37(1). pp.90-107.

Ngo, A and et.al., 2019. Analysis of Gender Differences in the Impact of Taxation and Taxation

Structure on Cigarette Consumption in 17 ITC Countries. International journal of

environmental research and public health. 16(7). p.1275.

Eslake, S., 2015, September. Reforming the Australian taxation system: a principled approach. In

address to the Australian Financial Review's Tax Forum Summit (Vol. 22).

Online

Individual income tax rates. 2019 [Online] Available through:

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>

7

Books and Journals

Sharkey, N. and Murray, I., 2016. Reinventing administrative leadership in Australian taxation:

beware the fine balance of social psychological and rule of law principles. Austl. Tax

F. .31. p.63.

Kennedy, T. and et.al., 2017. Does income inequality hinder economic growth? New evidence

using Australian taxation statistics. Economic Modelling. 65. pp.119-128.

Woellner, R. and et.al., 2016. Australian Taxation Law 2016. OUP Catalogue.

Sadiq, K., 2019. Australian Taxation Law Cases 2019. Thomson Reuters.

Perl, A. and Burke, M.I., 2018. Does institutional entrenchment shape instrument adjustment?:

Assessing instrument constituency influences on American and Australian motor fuel

taxation. Policy and Society. 37(1). pp.90-107.

Ngo, A and et.al., 2019. Analysis of Gender Differences in the Impact of Taxation and Taxation

Structure on Cigarette Consumption in 17 ITC Countries. International journal of

environmental research and public health. 16(7). p.1275.

Eslake, S., 2015, September. Reforming the Australian taxation system: a principled approach. In

address to the Australian Financial Review's Tax Forum Summit (Vol. 22).

Online

Individual income tax rates. 2019 [Online] Available through:

<https://www.ato.gov.au/Rates/Individual-income-tax-rates/>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.