HI6028 Taxation Theory, Practice & Law Assignment: Tax Liability & FBT

VerifiedAdded on 2022/11/30

|5

|1287

|323

Homework Assignment

AI Summary

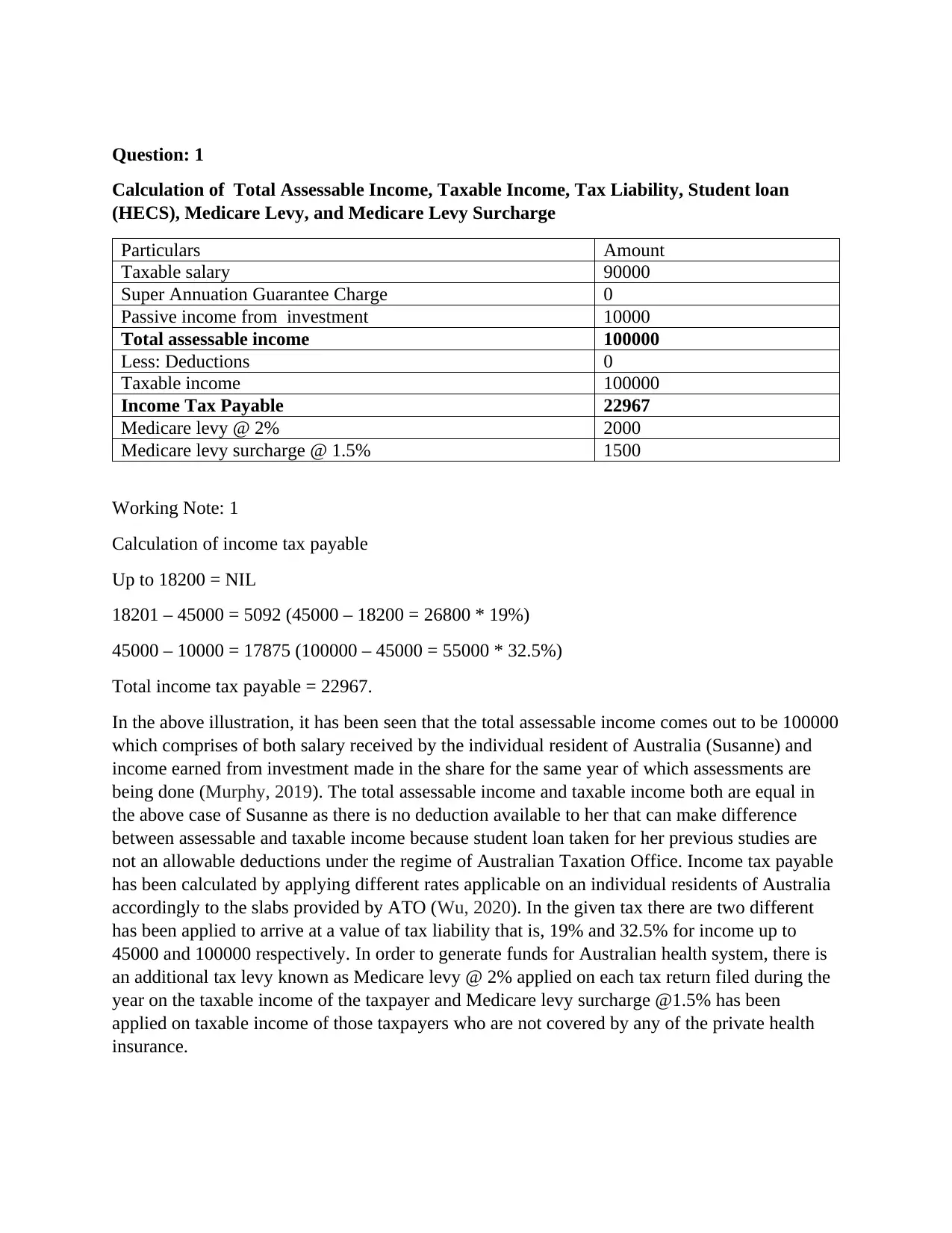

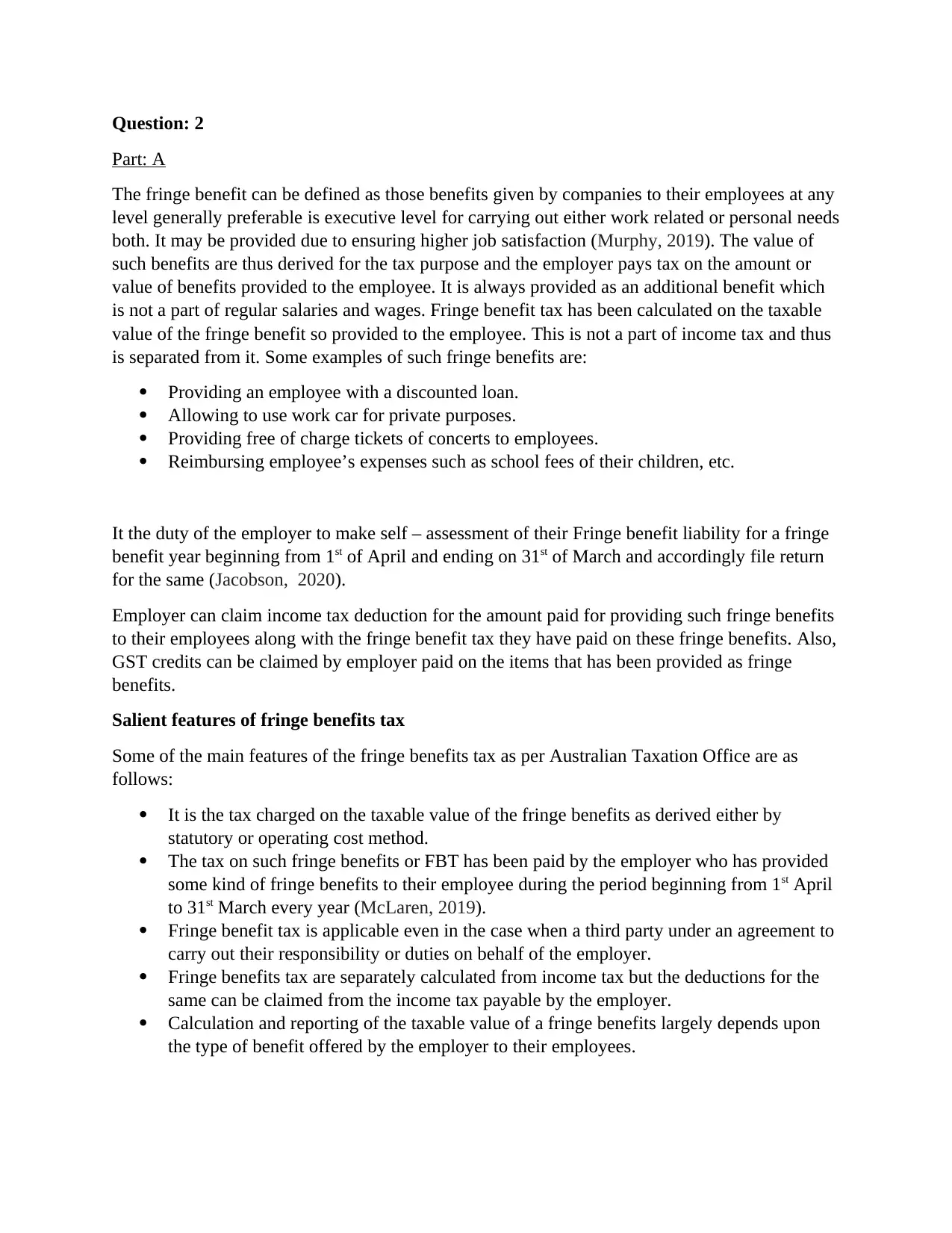

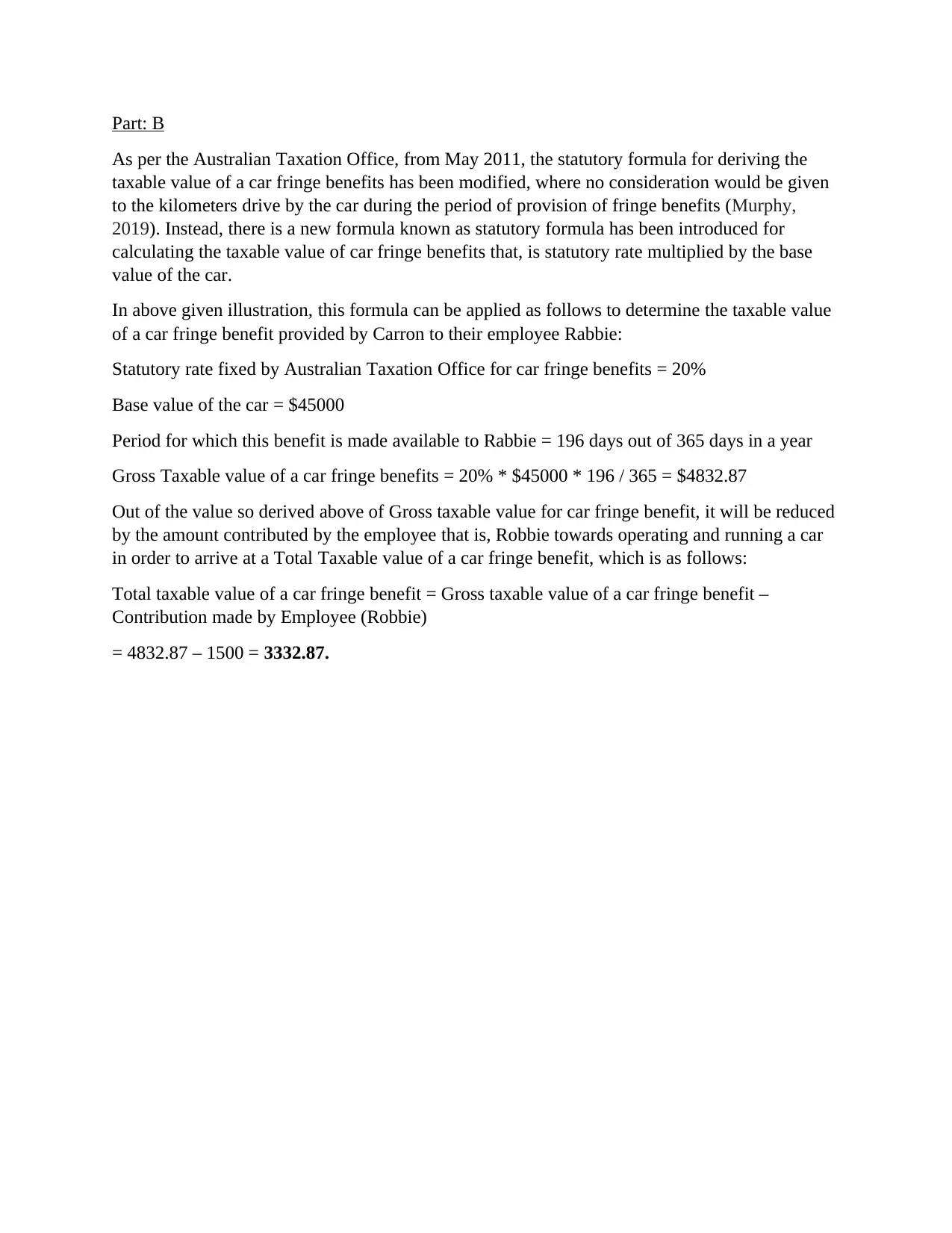

This document presents a comprehensive solution to a taxation assignment, addressing key concepts in Australian income tax law. It begins with a detailed calculation of an individual's total assessable income, taxable income, and tax liability, including the application of Medicare levy, Medicare levy surcharge, and student loan (HECS). The solution demonstrates the application of different tax rates based on income slabs provided by ATO. Furthermore, the assignment delves into the concept of Fringe Benefit Tax (FBT), defining it and providing examples such as discounted loans, work car usage, and reimbursement of employee expenses. The solution explains the features of FBT and its calculation, including the statutory formula for car fringe benefits, and provides a step-by-step calculation of the gross and total taxable value of a car fringe benefit, along with relevant references to support the analysis. The assignment covers the topics of taxation, FBT, and tax liability calculation for students.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.