Tax Planning Strategies for Maximizing Deductions and Investments

VerifiedAdded on 2019/09/30

|6

|1635

|233

Homework Assignment

AI Summary

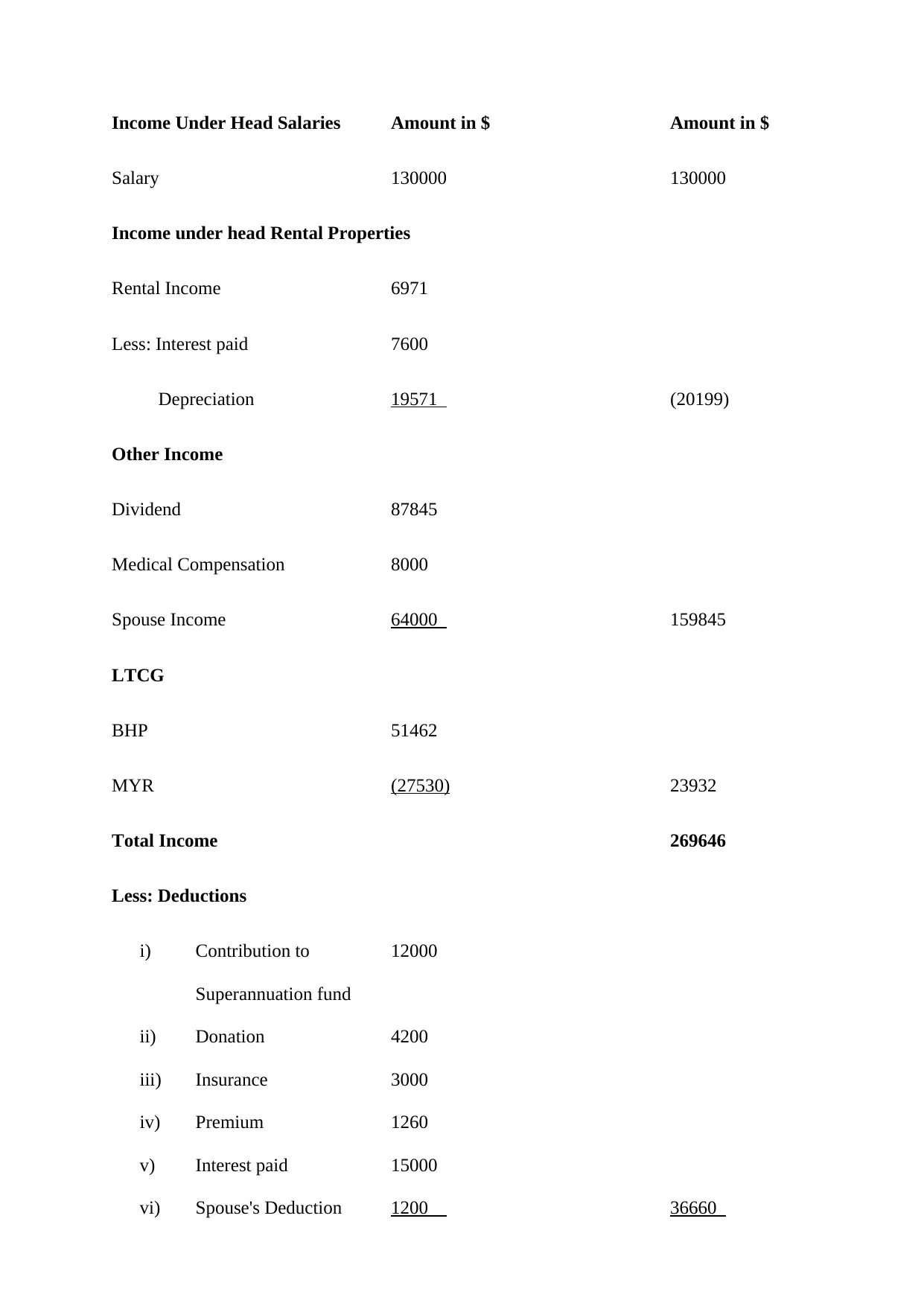

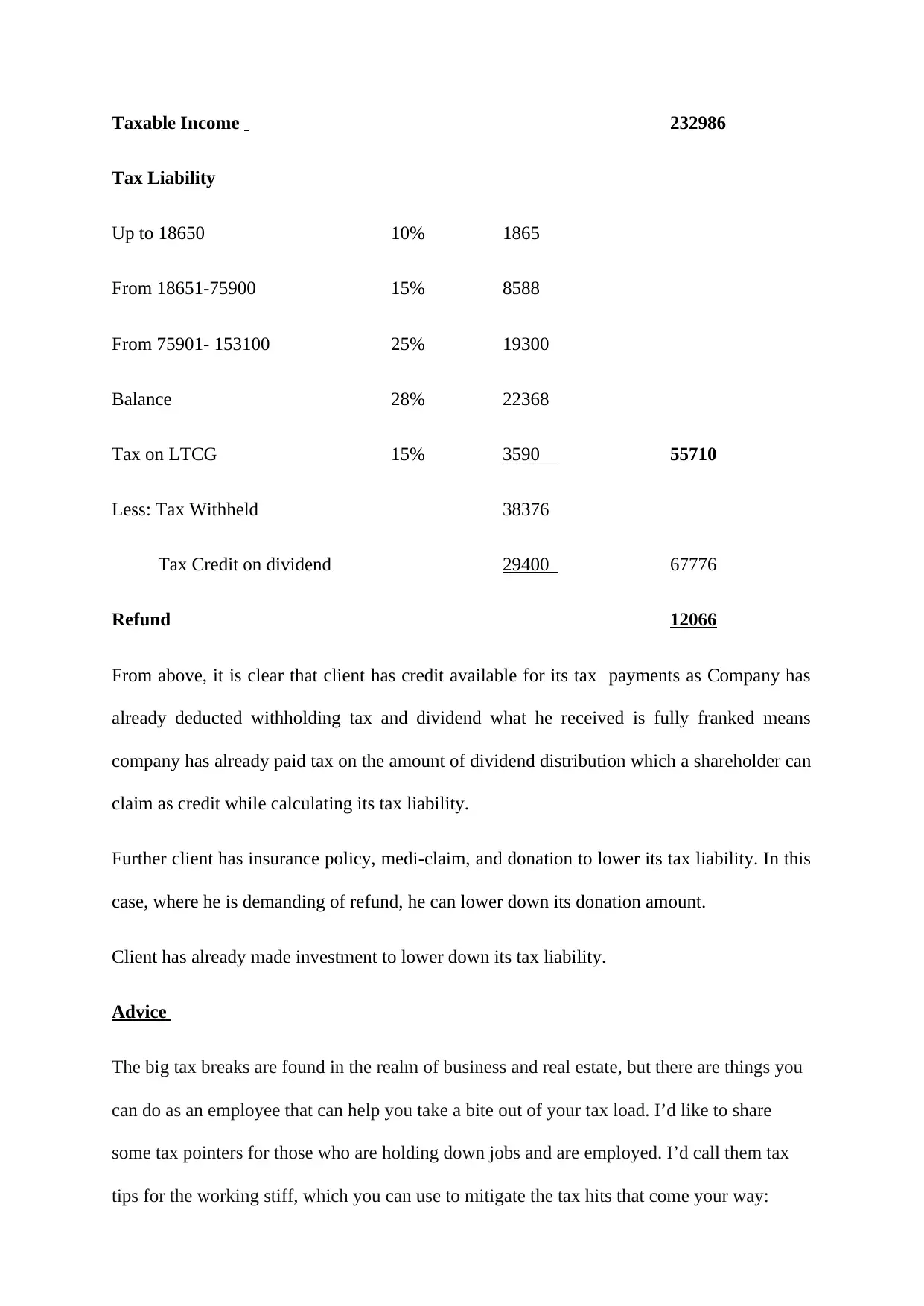

This assignment provides comprehensive tax planning advice for an individual, detailing income sources, deductions, and tax liabilities. It analyzes various income streams including salary, rental income, dividends, and spouse's income, along with deductions for superannuation, donations, insurance, and interest paid. The analysis calculates taxable income and tax liability, including tax on long-term capital gains, and identifies a tax refund. Furthermore, the assignment offers practical tax tips for employees, such as utilizing employer benefit plans (commuter benefits, group insurance), flexible spending plans, charitable contribution matching, and deducting job-related expenses. It emphasizes the importance of contributing to 401(k) plans and IRAs, donating unwanted items, and exploring options like 529 accounts and home businesses to optimize tax savings. The document concludes by highlighting real estate and business as key areas for effective tax strategies.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.