Taxation Law: Tax Planning Assignment Solution - University Name

VerifiedAdded on 2023/03/20

|11

|2629

|61

Homework Assignment

AI Summary

This document provides a detailed solution to a tax planning assignment, addressing several key areas of taxation law. The solution begins with the computation of total taxable income for Nodoubt Pty Ltd, including assessable income and allowable deductions. It then analyzes prepaid expenditure, determining the eligibility for immediate deductions under the 12-month rule for Forsure Pty Ltd, and calculating the apportioned deductions for prepaid interest. The assignment further examines non-commercial business losses for David, applying division 35 rules and commerciality tests. It also covers trust losses, specifically the Valley View Trust, and determines the applicability of loss carry-forward rules. The solution delves into the tax implications of trading stock, depreciating assets, and goodwill for Ben and Sam, respectively. Finally, it explores capital gains tax (CGT) exemptions and rollovers for Nick, advising on the 50% active asset reduction and retirement exemptions.

Running head: TAXATION LAW

Tax Planning

Name of the Student

Name of the University

Authors Note

Course ID

Tax Planning

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................9

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................9

Answer to question 7:.................................................................................................................9

References:...............................................................................................................................11

2TAXATION LAW

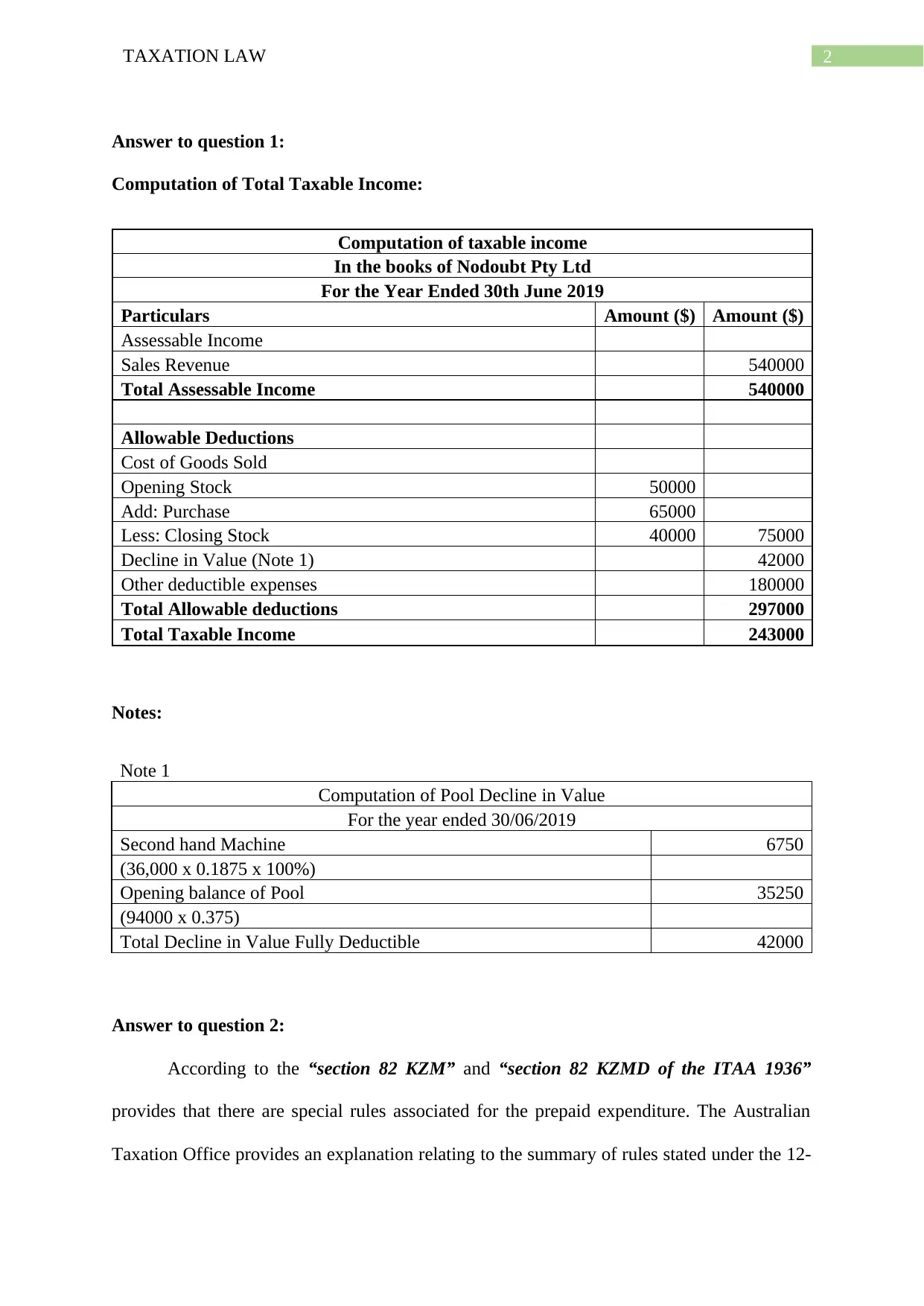

Answer to question 1:

Computation of Total Taxable Income:

Computation of taxable income

In the books of Nodoubt Pty Ltd

For the Year Ended 30th June 2019

Particulars Amount ($) Amount ($)

Assessable Income

Sales Revenue 540000

Total Assessable Income 540000

Allowable Deductions

Cost of Goods Sold

Opening Stock 50000

Add: Purchase 65000

Less: Closing Stock 40000 75000

Decline in Value (Note 1) 42000

Other deductible expenses 180000

Total Allowable deductions 297000

Total Taxable Income 243000

Notes:

Note 1

Computation of Pool Decline in Value

For the year ended 30/06/2019

Second hand Machine 6750

(36,000 x 0.1875 x 100%)

Opening balance of Pool 35250

(94000 x 0.375)

Total Decline in Value Fully Deductible 42000

Answer to question 2:

According to the “section 82 KZM” and “section 82 KZMD of the ITAA 1936”

provides that there are special rules associated for the prepaid expenditure. The Australian

Taxation Office provides an explanation relating to the summary of rules stated under the 12-

Answer to question 1:

Computation of Total Taxable Income:

Computation of taxable income

In the books of Nodoubt Pty Ltd

For the Year Ended 30th June 2019

Particulars Amount ($) Amount ($)

Assessable Income

Sales Revenue 540000

Total Assessable Income 540000

Allowable Deductions

Cost of Goods Sold

Opening Stock 50000

Add: Purchase 65000

Less: Closing Stock 40000 75000

Decline in Value (Note 1) 42000

Other deductible expenses 180000

Total Allowable deductions 297000

Total Taxable Income 243000

Notes:

Note 1

Computation of Pool Decline in Value

For the year ended 30/06/2019

Second hand Machine 6750

(36,000 x 0.1875 x 100%)

Opening balance of Pool 35250

(94000 x 0.375)

Total Decline in Value Fully Deductible 42000

Answer to question 2:

According to the “section 82 KZM” and “section 82 KZMD of the ITAA 1936”

provides that there are special rules associated for the prepaid expenditure. The Australian

Taxation Office provides an explanation relating to the summary of rules stated under the 12-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

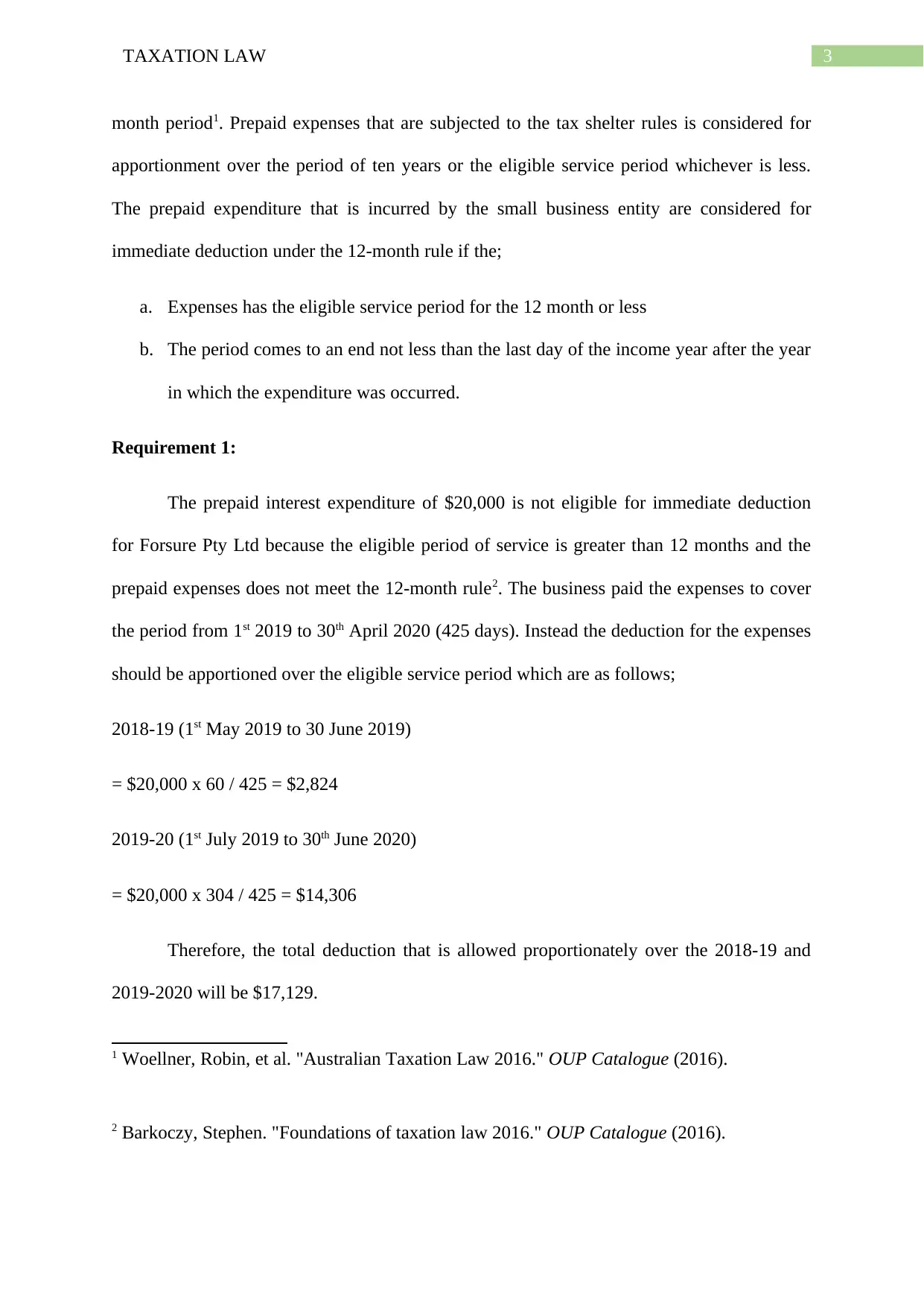

month period1. Prepaid expenses that are subjected to the tax shelter rules is considered for

apportionment over the period of ten years or the eligible service period whichever is less.

The prepaid expenditure that is incurred by the small business entity are considered for

immediate deduction under the 12-month rule if the;

a. Expenses has the eligible service period for the 12 month or less

b. The period comes to an end not less than the last day of the income year after the year

in which the expenditure was occurred.

Requirement 1:

The prepaid interest expenditure of $20,000 is not eligible for immediate deduction

for Forsure Pty Ltd because the eligible period of service is greater than 12 months and the

prepaid expenses does not meet the 12-month rule2. The business paid the expenses to cover

the period from 1st 2019 to 30th April 2020 (425 days). Instead the deduction for the expenses

should be apportioned over the eligible service period which are as follows;

2018-19 (1st May 2019 to 30 June 2019)

= $20,000 x 60 / 425 = $2,824

2019-20 (1st July 2019 to 30th June 2020)

= $20,000 x 304 / 425 = $14,306

Therefore, the total deduction that is allowed proportionately over the 2018-19 and

2019-2020 will be $17,129.

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

month period1. Prepaid expenses that are subjected to the tax shelter rules is considered for

apportionment over the period of ten years or the eligible service period whichever is less.

The prepaid expenditure that is incurred by the small business entity are considered for

immediate deduction under the 12-month rule if the;

a. Expenses has the eligible service period for the 12 month or less

b. The period comes to an end not less than the last day of the income year after the year

in which the expenditure was occurred.

Requirement 1:

The prepaid interest expenditure of $20,000 is not eligible for immediate deduction

for Forsure Pty Ltd because the eligible period of service is greater than 12 months and the

prepaid expenses does not meet the 12-month rule2. The business paid the expenses to cover

the period from 1st 2019 to 30th April 2020 (425 days). Instead the deduction for the expenses

should be apportioned over the eligible service period which are as follows;

2018-19 (1st May 2019 to 30 June 2019)

= $20,000 x 60 / 425 = $2,824

2019-20 (1st July 2019 to 30th June 2020)

= $20,000 x 304 / 425 = $14,306

Therefore, the total deduction that is allowed proportionately over the 2018-19 and

2019-2020 will be $17,129.

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

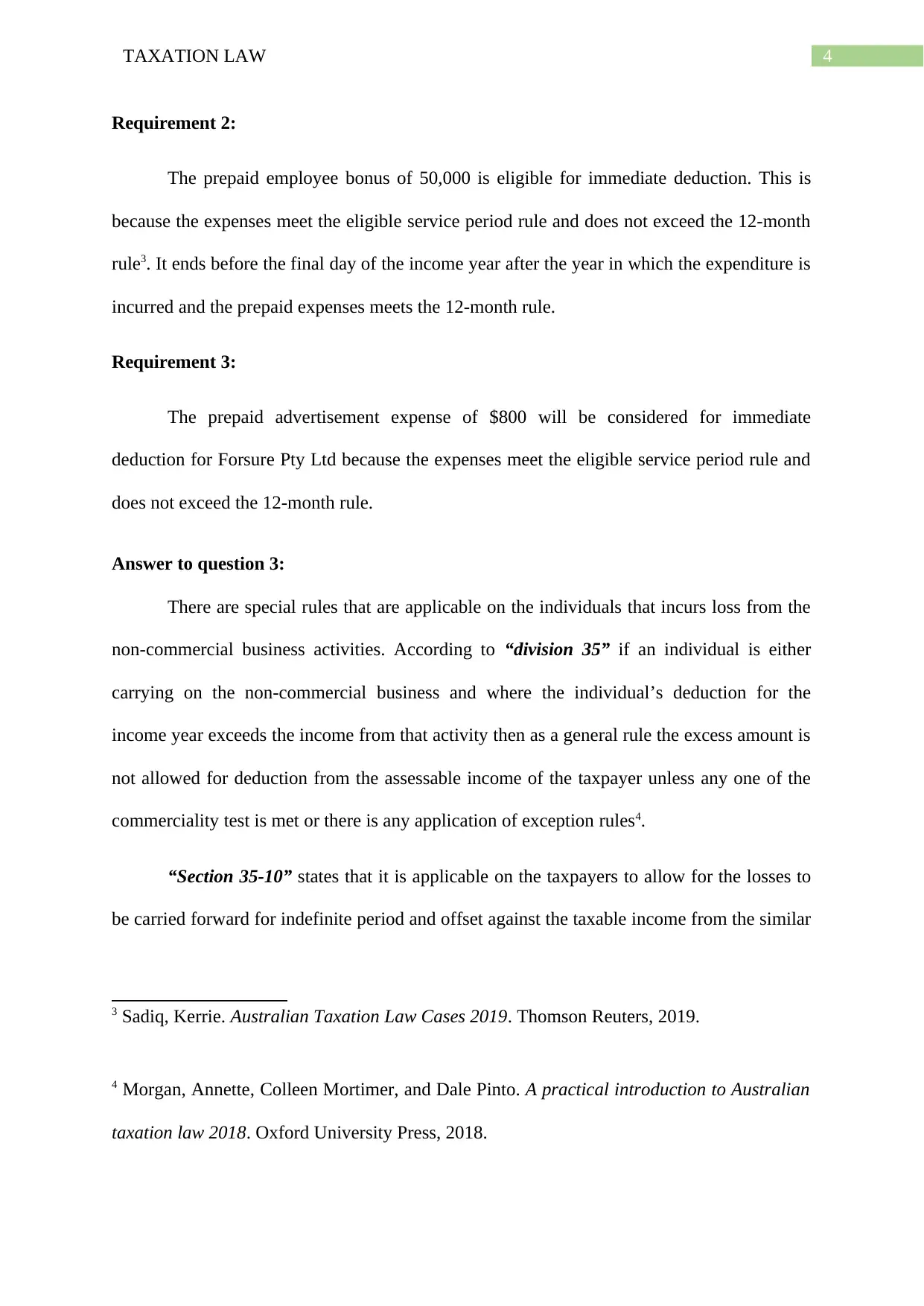

Requirement 2:

The prepaid employee bonus of 50,000 is eligible for immediate deduction. This is

because the expenses meet the eligible service period rule and does not exceed the 12-month

rule3. It ends before the final day of the income year after the year in which the expenditure is

incurred and the prepaid expenses meets the 12-month rule.

Requirement 3:

The prepaid advertisement expense of $800 will be considered for immediate

deduction for Forsure Pty Ltd because the expenses meet the eligible service period rule and

does not exceed the 12-month rule.

Answer to question 3:

There are special rules that are applicable on the individuals that incurs loss from the

non-commercial business activities. According to “division 35” if an individual is either

carrying on the non-commercial business and where the individual’s deduction for the

income year exceeds the income from that activity then as a general rule the excess amount is

not allowed for deduction from the assessable income of the taxpayer unless any one of the

commerciality test is met or there is any application of exception rules4.

“Section 35-10” states that it is applicable on the taxpayers to allow for the losses to

be carried forward for indefinite period and offset against the taxable income from the similar

3 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

4 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Requirement 2:

The prepaid employee bonus of 50,000 is eligible for immediate deduction. This is

because the expenses meet the eligible service period rule and does not exceed the 12-month

rule3. It ends before the final day of the income year after the year in which the expenditure is

incurred and the prepaid expenses meets the 12-month rule.

Requirement 3:

The prepaid advertisement expense of $800 will be considered for immediate

deduction for Forsure Pty Ltd because the expenses meet the eligible service period rule and

does not exceed the 12-month rule.

Answer to question 3:

There are special rules that are applicable on the individuals that incurs loss from the

non-commercial business activities. According to “division 35” if an individual is either

carrying on the non-commercial business and where the individual’s deduction for the

income year exceeds the income from that activity then as a general rule the excess amount is

not allowed for deduction from the assessable income of the taxpayer unless any one of the

commerciality test is met or there is any application of exception rules4.

“Section 35-10” states that it is applicable on the taxpayers to allow for the losses to

be carried forward for indefinite period and offset against the taxable income from the similar

3 Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

4 Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

5TAXATION LAW

activity for the next income year in which the activities were occurred and 1 one of the four

commerciality test is met5. The four commerciality test are as follows;

a. Assessable income test: Under “section 35-30” Assessable income from the activity

for the income should be at least $20,000.

b. Profit Test: Under “section 35-35” The activity should have the profit for at least 3

years out of the last five years together with the current year.

c. Real Property Test: Under “section 35-40” the total value of the real property or the

interest in the real property that is used on a constant basis should have the value of at

least $500,000.

d. Other asset test: Under the “section 35-45” the total value of the other assets that is

used for a continuous basis in the activity should be at least $100,000.

In the current case of David, it can be stated that the non-commercial loss rules would

be applicable because David does not meet any of the four commercial test. The taxable

income test is not satisfied by David because the income that is made from the business is

only $15,000 which is less than $20,000. Furthermore, the profit test is not relevant in case of

David because it is only the first year of business. David does not meet the real property test

as well because the value of the shed in which he operates his business is $30,000 which is

less than the $500,000 criteria. Finally, the other test is also not satisfied by David because

the value of business tool is only $10,000 which is less than $100,000. The taxable income of

David is calculated below;

Computation of Total Assessable Income

In the books of David

5 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

activity for the next income year in which the activities were occurred and 1 one of the four

commerciality test is met5. The four commerciality test are as follows;

a. Assessable income test: Under “section 35-30” Assessable income from the activity

for the income should be at least $20,000.

b. Profit Test: Under “section 35-35” The activity should have the profit for at least 3

years out of the last five years together with the current year.

c. Real Property Test: Under “section 35-40” the total value of the real property or the

interest in the real property that is used on a constant basis should have the value of at

least $500,000.

d. Other asset test: Under the “section 35-45” the total value of the other assets that is

used for a continuous basis in the activity should be at least $100,000.

In the current case of David, it can be stated that the non-commercial loss rules would

be applicable because David does not meet any of the four commercial test. The taxable

income test is not satisfied by David because the income that is made from the business is

only $15,000 which is less than $20,000. Furthermore, the profit test is not relevant in case of

David because it is only the first year of business. David does not meet the real property test

as well because the value of the shed in which he operates his business is $30,000 which is

less than the $500,000 criteria. Finally, the other test is also not satisfied by David because

the value of business tool is only $10,000 which is less than $100,000. The taxable income of

David is calculated below;

Computation of Total Assessable Income

In the books of David

5 Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

For the year ended 2019

Particulars Amount ($)

Assessable Income

Gross Wages 80000

Total Assessable Income 80000

Allowable Deduction

Loss from business 10000

Total Taxable Income 70000

Answer to question 4:

As held in the case of “Doherty v FCT (1933)” losses that are incurred by a trust

remains in the trust and cannot be considered for distribution to the beneficiaries. A

beneficially is not allowed to offset any part of the trust loss against the taxable income to

lower their tax liability in relation to the other sources of income. The trust loss might be as

an alternative be carried forward within the trust and can be offset against the taxable income

while calculating the tax net income of the trust in the future years. This is done in

accordance with the losses that are carried forward under the “provision 36-15 of the ITAA

1997”. “Schedule 2F of the ITAA 1936” restricts the situations where the previous year and

current year losses of the trust can be claimed as the specific deduction while calculating the

net of the trust6. There are three broad categories of trust that are identified for the purpose of

trust loss which are as follows;

a. Fixed Trust

b. Non-fixed trust

c. Excepted trust

6 Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

For the year ended 2019

Particulars Amount ($)

Assessable Income

Gross Wages 80000

Total Assessable Income 80000

Allowable Deduction

Loss from business 10000

Total Taxable Income 70000

Answer to question 4:

As held in the case of “Doherty v FCT (1933)” losses that are incurred by a trust

remains in the trust and cannot be considered for distribution to the beneficiaries. A

beneficially is not allowed to offset any part of the trust loss against the taxable income to

lower their tax liability in relation to the other sources of income. The trust loss might be as

an alternative be carried forward within the trust and can be offset against the taxable income

while calculating the tax net income of the trust in the future years. This is done in

accordance with the losses that are carried forward under the “provision 36-15 of the ITAA

1997”. “Schedule 2F of the ITAA 1936” restricts the situations where the previous year and

current year losses of the trust can be claimed as the specific deduction while calculating the

net of the trust6. There are three broad categories of trust that are identified for the purpose of

trust loss which are as follows;

a. Fixed Trust

b. Non-fixed trust

c. Excepted trust

6 Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Excepted trusts generally comprises of the family trust and this trust is not subjected

to trust loss rules under “schedule 2F”, “section 272-100 of the ITAA 1997”.

The Valley View Trust is the discretionary trust and not the family trust and to apply

for the losses it is required to satisfy any of the four test. By looking first at the patter of

distribution trust Valley View Trust, the lowest distribution over three years has been 50%

with Jack 30% and Jill 30%. As a result, it is more than 50% and the pattern of distribution

test is met. With no individual is holding more than 50% either jointly or individually fixed

stake the 50% stake is not applicable in the case of Valley View Trust.

Furthermore, there has been no kind of change in the trustee nor has been any kind of

change in the control. Therefore, the control test is met. With no such income is injected into

the trust by any external person the income injection test appears to be irrelevant for Valley

View Trust. Valley View Trust does not fail any of the four test that are applicable for the

non-fixed trust. Therefore, the trust can claim the previous year losses of $20,000 and

$30,000 to lower the net income of the trust for the income year 2019 from $220,000 to

$170,000.

Answer to question 5:

If the vendor entity sells the item of trading stock out of the ordinary business course,

the purchaser entity purchasing the item is regarded as the having purchased the item for the

amount included into the selling entity’s taxable income under the “section 70-90” based on

the market value. Even though trading stock is treated as the CGT asset since it is a form of

property, any capital gains or capital loss that is made from the sale of trading stock will be

disregarded under “section 118-25”7.

7 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Excepted trusts generally comprises of the family trust and this trust is not subjected

to trust loss rules under “schedule 2F”, “section 272-100 of the ITAA 1997”.

The Valley View Trust is the discretionary trust and not the family trust and to apply

for the losses it is required to satisfy any of the four test. By looking first at the patter of

distribution trust Valley View Trust, the lowest distribution over three years has been 50%

with Jack 30% and Jill 30%. As a result, it is more than 50% and the pattern of distribution

test is met. With no individual is holding more than 50% either jointly or individually fixed

stake the 50% stake is not applicable in the case of Valley View Trust.

Furthermore, there has been no kind of change in the trustee nor has been any kind of

change in the control. Therefore, the control test is met. With no such income is injected into

the trust by any external person the income injection test appears to be irrelevant for Valley

View Trust. Valley View Trust does not fail any of the four test that are applicable for the

non-fixed trust. Therefore, the trust can claim the previous year losses of $20,000 and

$30,000 to lower the net income of the trust for the income year 2019 from $220,000 to

$170,000.

Answer to question 5:

If the vendor entity sells the item of trading stock out of the ordinary business course,

the purchaser entity purchasing the item is regarded as the having purchased the item for the

amount included into the selling entity’s taxable income under the “section 70-90” based on

the market value. Even though trading stock is treated as the CGT asset since it is a form of

property, any capital gains or capital loss that is made from the sale of trading stock will be

disregarded under “section 118-25”7.

7 Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

8TAXATION LAW

As evident in the current situation of Ben who purchased the book retailing business

from Andrew the purchase of trading stock represents an interest of having the high market

value. Ben in this circumstances can maximise the deductible opening value of the trading

stock and minimise his taxable income on the succeeding sale.

Under “section 40-35” every item of the property plant and equipment would be

treated as the depreciating asset since it constitutes an asset that has the limited effective life

and it is reasonably anticipated to fall in value over the period of time. The purchase under

the “section 40-25 (1), ITAA 1997” can claim a specific deduction for the amount that is

equivalent to the decline in value of the depreciating asset which is held during the year for

assessable purpose. Similarly, in the current situation Sam can obtain a specific deduction

under “section 40-25 (1), ITAA 1997” for the decline in value of the property plant and

equipment.

Sam also bought a goodwill that valued $10,000. Under “section 8-1 (2)(a) of the

ITAA 1997” cost involved in purchasing the goodwill is regarded as the non-deductible

capital expenses. Therefore, Sam will not be allowed to claim deduction under “section 40-

880” because it is an outgoing of capital in nature and non-deductible expense.

Answer to question 6:

As stated by the ATO the taxpayers are allowed to claim CGT exemption and rollover

reliefs that helps them in disregarding or deferring the capital gains from the active asset that

is used in the business8. The concession includes the following

a. 15-year exemption of active asset held for 15 years

8 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

As evident in the current situation of Ben who purchased the book retailing business

from Andrew the purchase of trading stock represents an interest of having the high market

value. Ben in this circumstances can maximise the deductible opening value of the trading

stock and minimise his taxable income on the succeeding sale.

Under “section 40-35” every item of the property plant and equipment would be

treated as the depreciating asset since it constitutes an asset that has the limited effective life

and it is reasonably anticipated to fall in value over the period of time. The purchase under

the “section 40-25 (1), ITAA 1997” can claim a specific deduction for the amount that is

equivalent to the decline in value of the depreciating asset which is held during the year for

assessable purpose. Similarly, in the current situation Sam can obtain a specific deduction

under “section 40-25 (1), ITAA 1997” for the decline in value of the property plant and

equipment.

Sam also bought a goodwill that valued $10,000. Under “section 8-1 (2)(a) of the

ITAA 1997” cost involved in purchasing the goodwill is regarded as the non-deductible

capital expenses. Therefore, Sam will not be allowed to claim deduction under “section 40-

880” because it is an outgoing of capital in nature and non-deductible expense.

Answer to question 6:

As stated by the ATO the taxpayers are allowed to claim CGT exemption and rollover

reliefs that helps them in disregarding or deferring the capital gains from the active asset that

is used in the business8. The concession includes the following

a. 15-year exemption of active asset held for 15 years

8 Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

b. 50% active asset reduction from the capital gains on the asset owned for 12 months or

more.

c. Retirement exemption for the sale of asset till a lifetime limit of $500,000.

d. Rollover of active asset

As evident in case of Nick he sold the business for $4,200,000 and with respect to the

ATO provision Nick is advised to obtain a 50% active asset reduction for the building

because the building has been held for more than 12 months. Additionally, the capital gains

from the sale of business equipment and plant can be exempted till the limit of $500,000

because Nick is currently under 55 years. Therefore, Nick satisfies the basic eligibility

conditions as the net assets is not more than $6 million and it is solely used for producing

business income.

Answer to question 7:

As per the “section 9-5, ITAA 1997” the sale of business is regarded as the taxable

supply if the vendor is registered or required to be registered. However, the supply of the

going concern will be treated as GST-free if the vendor and the purchaser agree in writing

regarding the supply of going concern and the vendor supplies the purchaser with all the

things. Similarly, in case of Sally she sells the motel business to Helen based on the agreed

written contract. With respect to the above context Sally will not be liable for GST as the sale

of business constitute a supply of going concern under the written agreement and hence no

GST will be payable by Sally.

b. 50% active asset reduction from the capital gains on the asset owned for 12 months or

more.

c. Retirement exemption for the sale of asset till a lifetime limit of $500,000.

d. Rollover of active asset

As evident in case of Nick he sold the business for $4,200,000 and with respect to the

ATO provision Nick is advised to obtain a 50% active asset reduction for the building

because the building has been held for more than 12 months. Additionally, the capital gains

from the sale of business equipment and plant can be exempted till the limit of $500,000

because Nick is currently under 55 years. Therefore, Nick satisfies the basic eligibility

conditions as the net assets is not more than $6 million and it is solely used for producing

business income.

Answer to question 7:

As per the “section 9-5, ITAA 1997” the sale of business is regarded as the taxable

supply if the vendor is registered or required to be registered. However, the supply of the

going concern will be treated as GST-free if the vendor and the purchaser agree in writing

regarding the supply of going concern and the vendor supplies the purchaser with all the

things. Similarly, in case of Sally she sells the motel business to Helen based on the agreed

written contract. With respect to the above context Sally will not be liable for GST as the sale

of business constitute a supply of going concern under the written agreement and hence no

GST will be payable by Sally.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

References:

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Cavenagh, Jennifer, et al. "Australian legislation concerning matters of international law

2016." Australian Year Book of International Law 35 (2018): 353.

Morgan, Annette, and Donovan Castelyn. "Taxation Education in Secondary Schools." J.

Australasian Tax Tchrs. Ass'n 13 (2018): 307.

Morgan, Annette, Colleen Mortimer, and Dale Pinto. A practical introduction to Australian

taxation law 2018. Oxford University Press, 2018.

Robin & Barkoczy Woellner (Stephen & Murphy, Shirley Et Al.). Australian Taxation Law

Select 2019: Legislation And Commentary. Oxford University Press, 2019.

Robin, H. Australian Taxation Law 2019. Oxford University Press, 2019.

Sadiq, Kerrie. Australian Taxation Law Cases 2019. Thomson Reuters, 2019.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.