Comprehensive Taxation Law Report: Case Analysis and Regulations

VerifiedAdded on 2020/04/01

|11

|1577

|57

Report

AI Summary

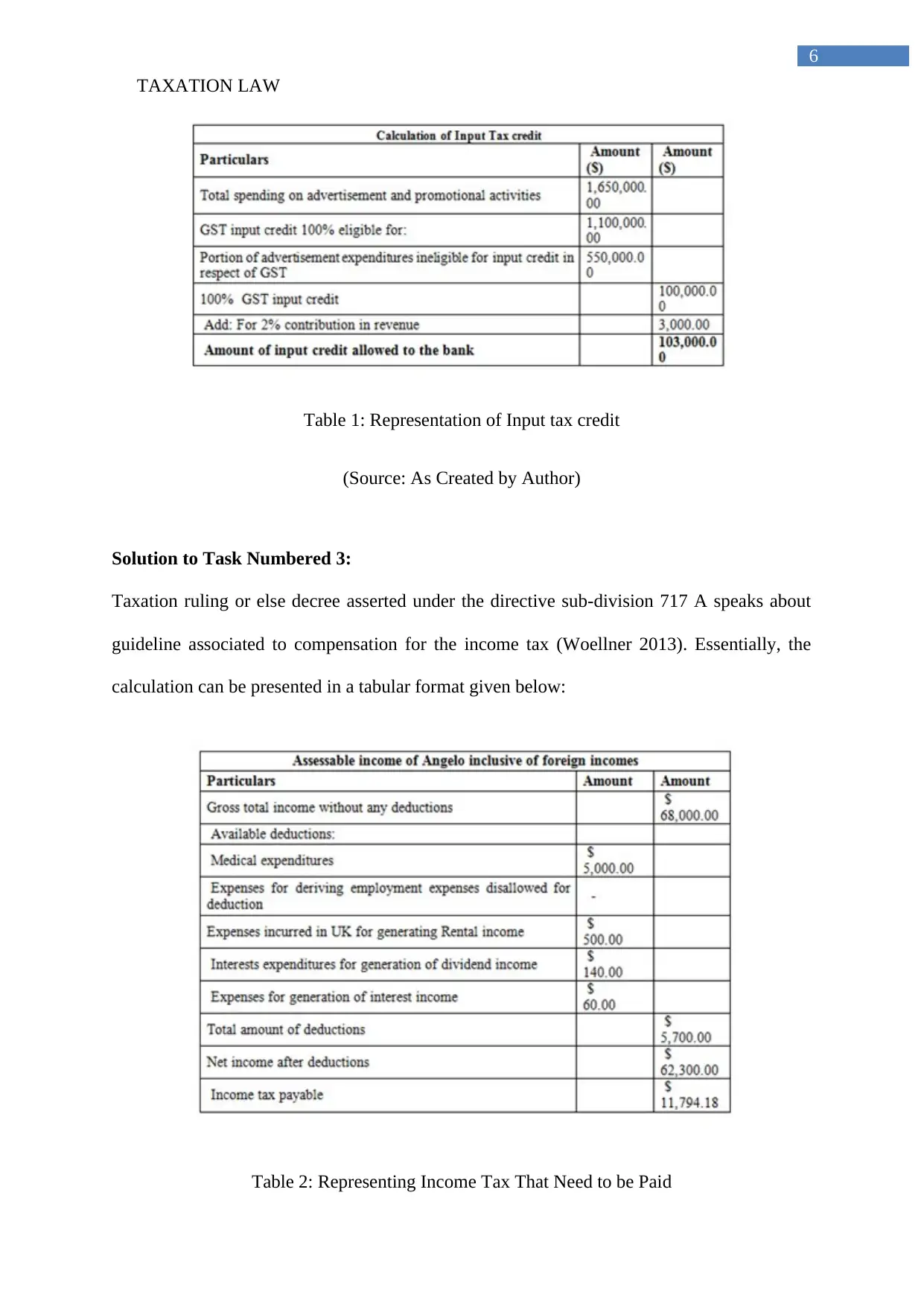

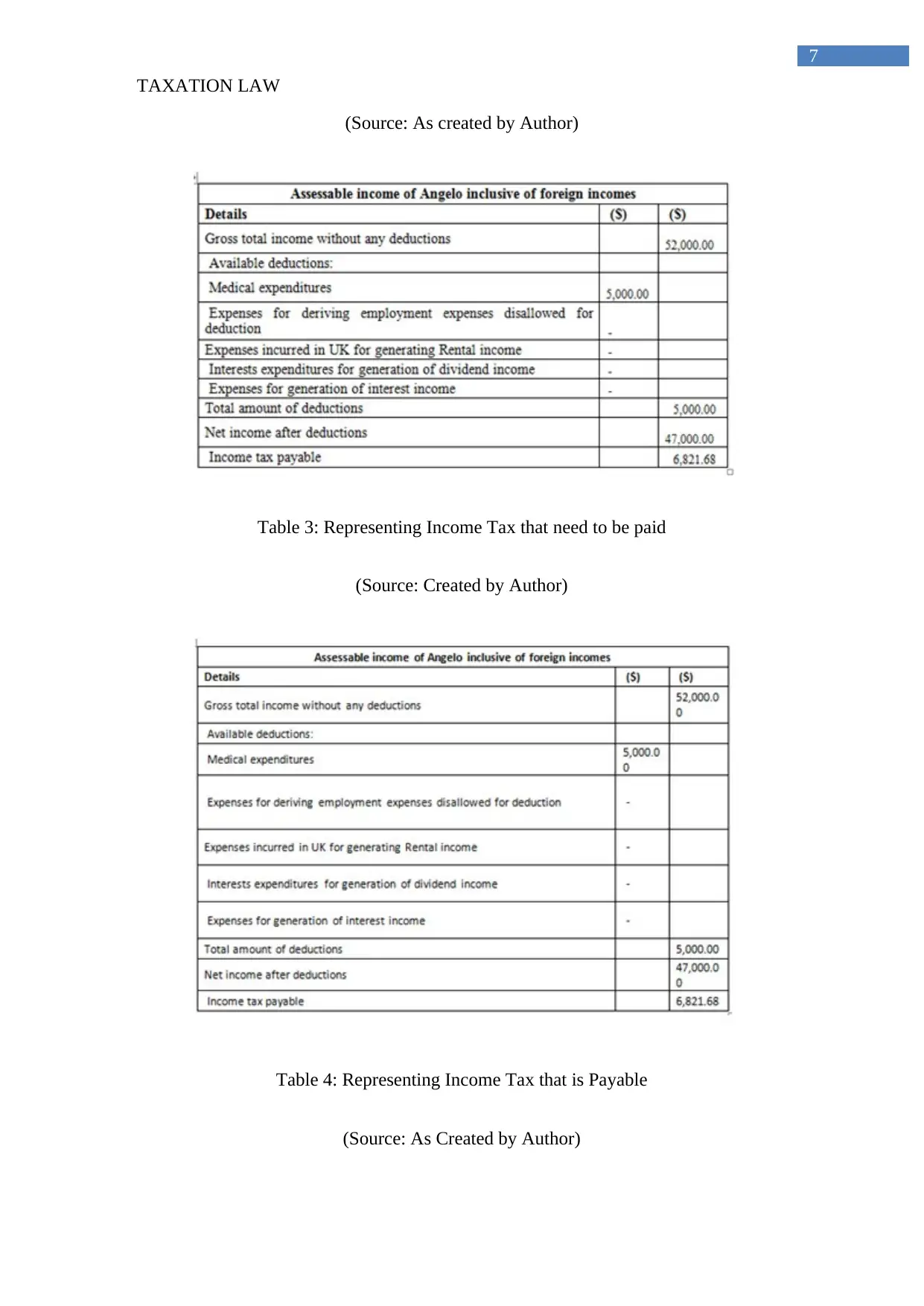

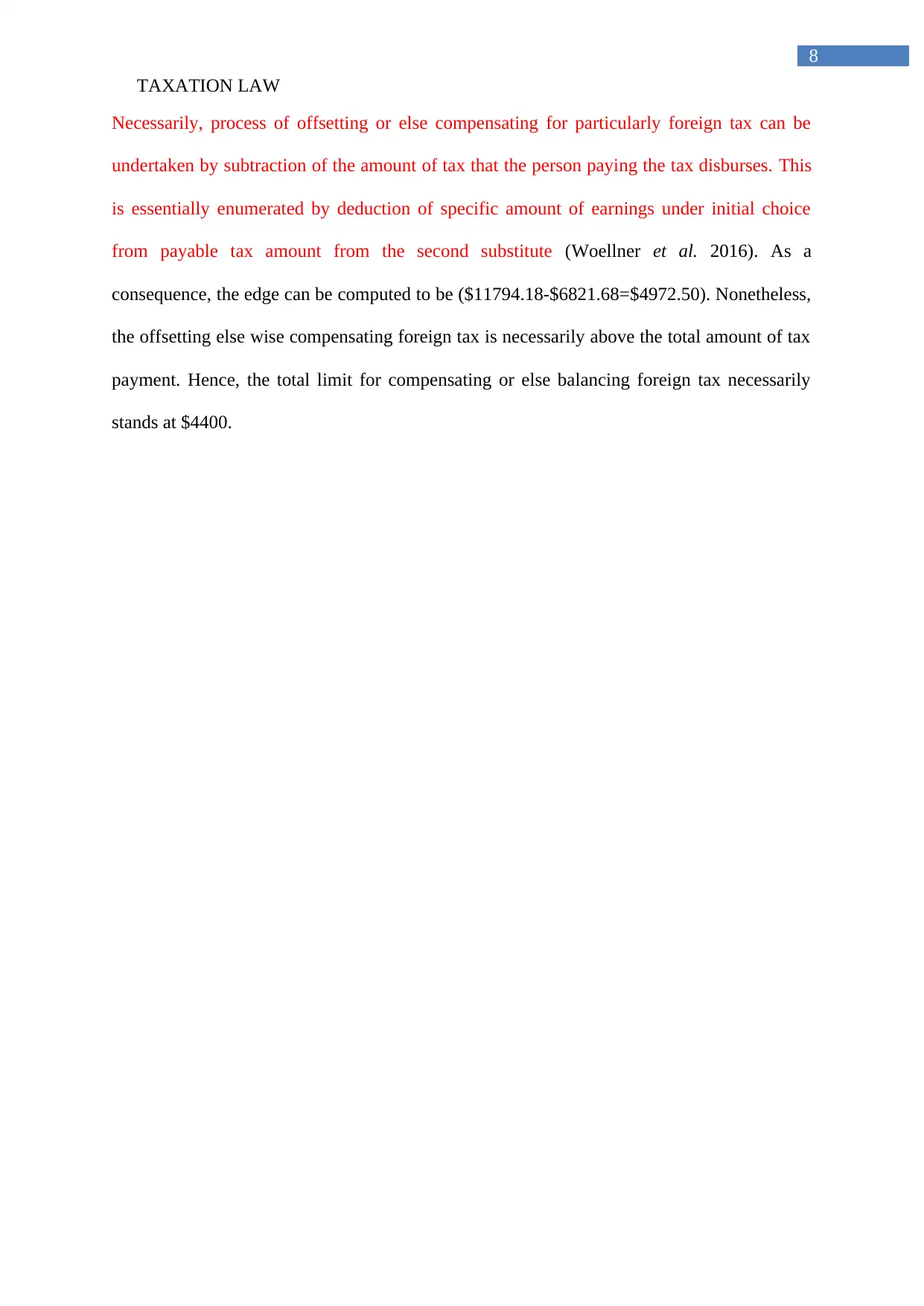

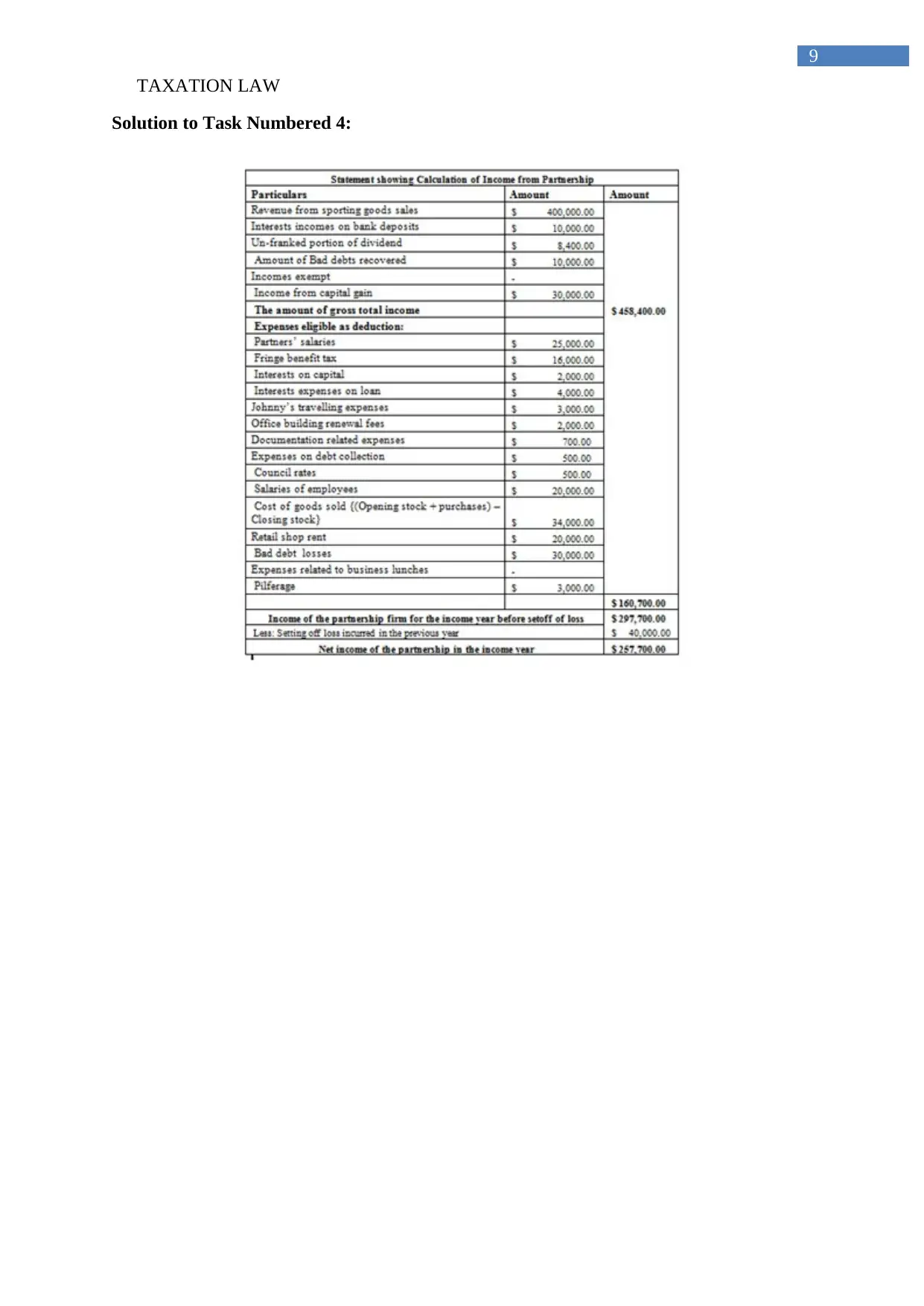

This report delves into the intricacies of taxation law, examining key aspects such as tax deductions, input tax credits, and relevant case studies. It begins by exploring the concept of taxable income and permissible expenses according to the Income Tax Assessment Act of 1997, including the deductibility of business expenses like machinery relocation and legal proceedings. The report then analyzes a case study involving a bank, focusing on the application of Goods and Service Tax (GST) input credit for advertising expenses, and provides a detailed breakdown of input tax credit calculations. Furthermore, it addresses the guidelines for compensation related to foreign tax, outlining the process and limitations. The report concludes with a comprehensive list of references, providing a solid foundation for understanding the complexities of taxation law and its practical applications.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.