ACC 304 Taxation Law: Tax Practice Assignment - Residency & Income

VerifiedAdded on 2023/03/30

|10

|1164

|198

Report

AI Summary

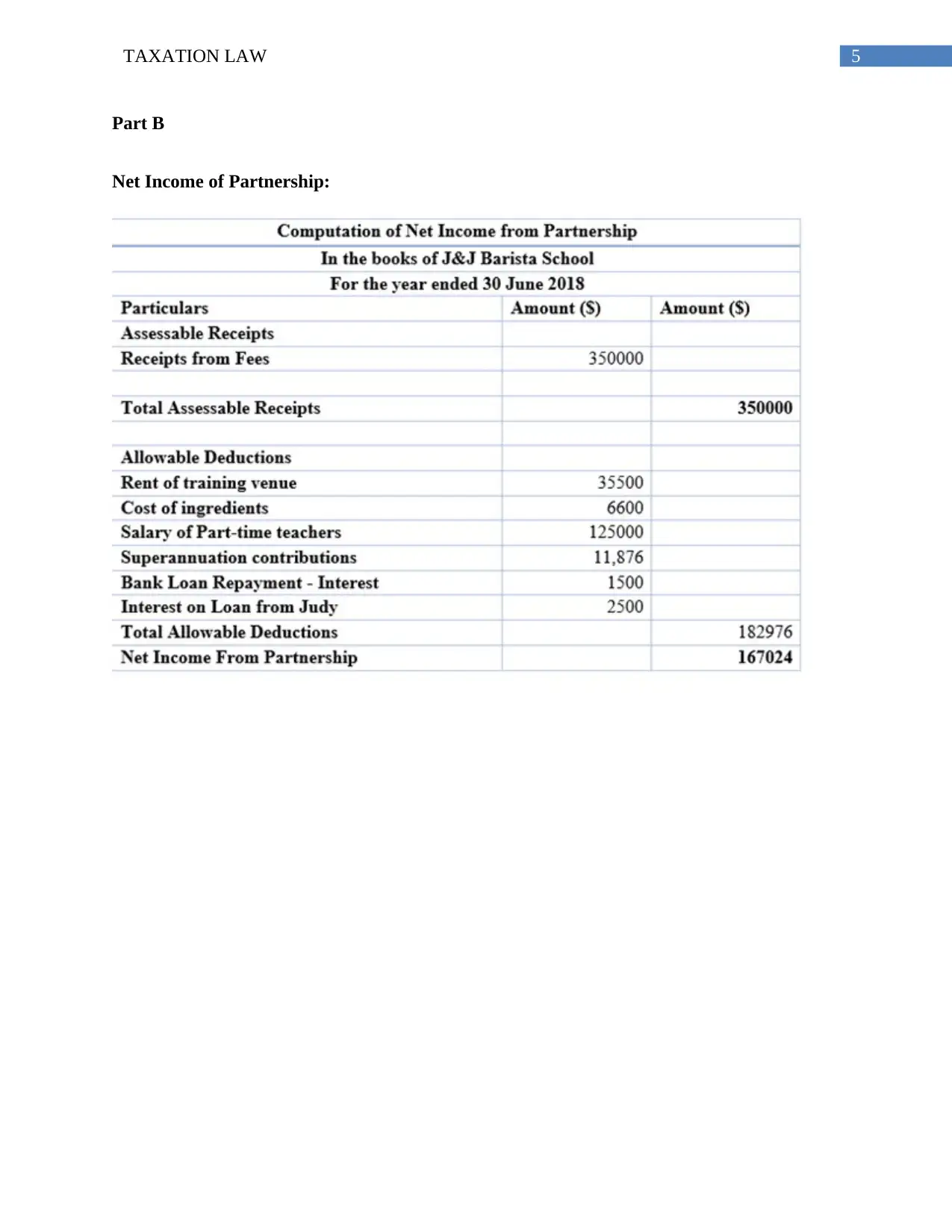

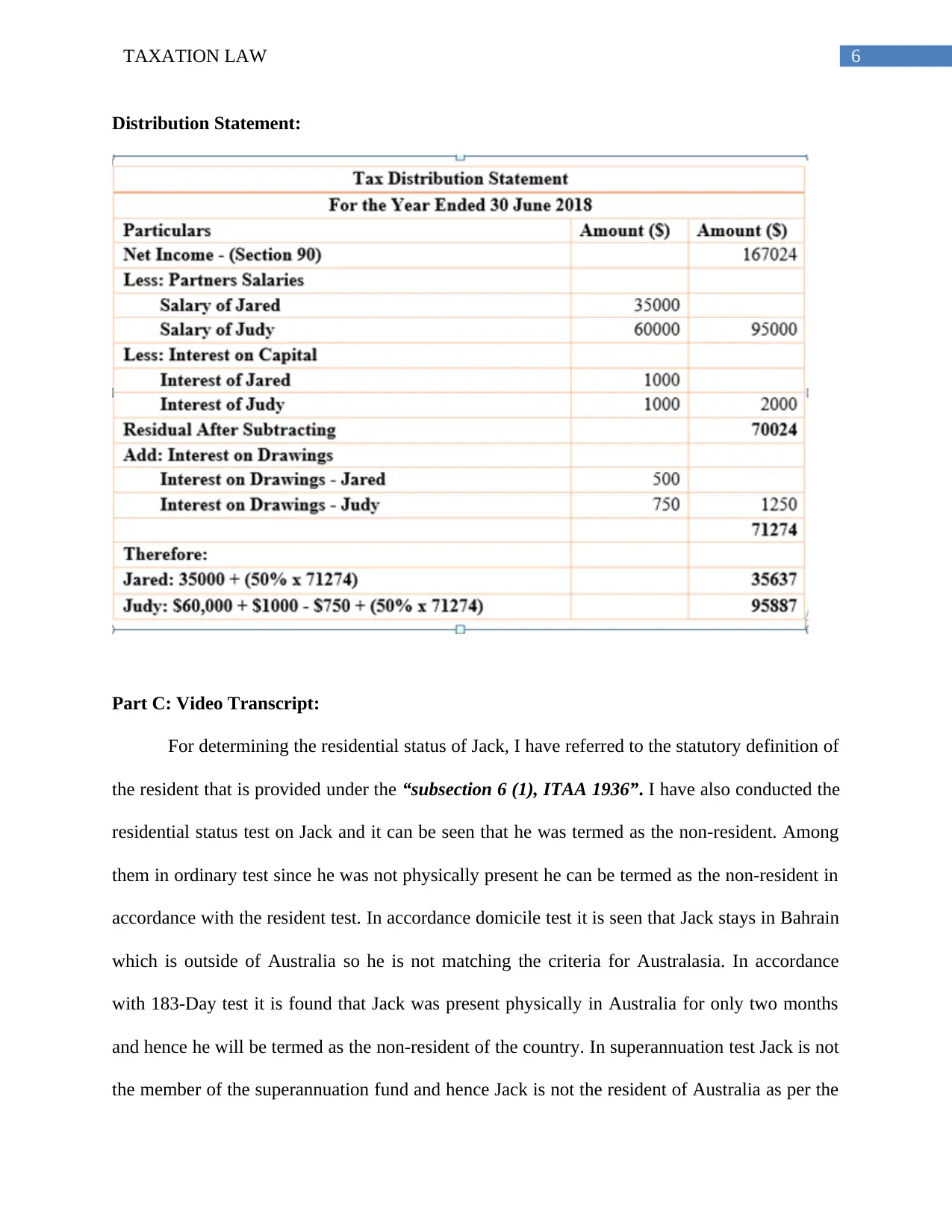

This report provides a comprehensive analysis of taxation law, focusing on the determination of residency status and the assessment of partnership income. Part A assesses an individual's residency based on statutory definitions and various tests, including the Ordinary Test, Domicile Test, 183-Day Test, and Commonwealth Superannuation Test, ultimately concluding the individual is a non-resident. Part B details the calculation of net partnership income and its distribution among partners. Part C includes a video transcript explaining the rationale behind the residency determination and income calculation. The report references relevant legal cases and legislation, such as the ITAA 1936 and the Domicile Act 1982. Desklib offers a wide array of similar solved assignments and resources for students.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.