Comparative Analysis of Tax Structures: India's Case Study

VerifiedAdded on 2022/08/16

|16

|4270

|15

Report

AI Summary

This report delves into the intricacies of tax structures, specifically focusing on progressive and regressive models, and their implications for developing countries. It begins by defining and contrasting progressive taxation, where higher earners pay a larger percentage of their income in taxes, with regressive taxation, where lower earners bear a proportionally heavier tax burden. The report then explores a tax structure that combines elements of both, examining its advantages, such as potentially increasing government revenue and reducing income inequality, as well as its disadvantages, like the potential for discouraging lower-income earners. A significant portion of the report is dedicated to analyzing the tax structure in India, a developing nation, evaluating its current state, and assessing the potential impact of a combined progressive and regressive approach, considering factors like income distribution and economic growth. The report concludes by summarizing the key findings and their relevance to economic policy in developing nations.

Running head: TAX STRUCTURE

Tax Structure

Name of the Student

Name of the University

Student ID

Tax Structure

Name of the Student

Name of the University

Student ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAX STRUCTURE

Table of Contents

Introduction......................................................................................................................................3

Progressive tax.................................................................................................................................4

Regressive tax..................................................................................................................................5

Tax structure with progressive and regressive tax characteristics...................................................6

Advantages of the new tax structure................................................................................................7

Disadvantages of the new tax structure...........................................................................................8

Tax Structure in a developing country.............................................................................................9

Tax condition in India....................................................................................................................11

Impact of combined tax structure on India....................................................................................12

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................14

Table of Contents

Introduction......................................................................................................................................3

Progressive tax.................................................................................................................................4

Regressive tax..................................................................................................................................5

Tax structure with progressive and regressive tax characteristics...................................................6

Advantages of the new tax structure................................................................................................7

Disadvantages of the new tax structure...........................................................................................8

Tax Structure in a developing country.............................................................................................9

Tax condition in India....................................................................................................................11

Impact of combined tax structure on India....................................................................................12

Conclusion.....................................................................................................................................12

Reference.......................................................................................................................................14

2TAX STRUCTURE

Introduction

The government of country gain funds for its expenditures through various ways and one

of them is taxation. Taxation rather is one of the biggest source of revenue earned by the

government of most of the country in the world However, different government sues different

methods or policies to collect tax. Broadly, tax system of a country can be can be categorized

into three types and they are progressive taxation, regressive taxation and proportional taxation.

Under progressive taxation, individuals with higher income are burdened more with tax. On the

other hand, in case of regressive taxation individuals with lower income are burdened more with

tax. Conversely, every individual whether belonging to low income or high income group are

burdened with equal proportion of tax (Toma, 2019). Therefore, it is the discretion of the

government to decide whether to use progressive, regressive or proportional tax structure. The

report however focuses on progressive and regressive tax structure. To understand the tax

structures the report discusses the characteristics of the respective tax structures and thereby

describes their impacts. The report considers the case of India and its tax structure provides brief

on the existing tax condition in the country and try to draw the impact of a tax structure that

include both the tax methods of progressive tax and regressive tax. Thus, the tax structure exhibit

the characteristics of both the progressive and regressive taxation. The report further explains the

advantages and disadvantages of the said tax structure on the economy of India. India is a

developing country with most of the population belonging to low income group in comparison to

high income group. The report thus critically analyses both the tax structures and thereby by

finds the impact of combined use of both the structure on in a developing country.

Introduction

The government of country gain funds for its expenditures through various ways and one

of them is taxation. Taxation rather is one of the biggest source of revenue earned by the

government of most of the country in the world However, different government sues different

methods or policies to collect tax. Broadly, tax system of a country can be can be categorized

into three types and they are progressive taxation, regressive taxation and proportional taxation.

Under progressive taxation, individuals with higher income are burdened more with tax. On the

other hand, in case of regressive taxation individuals with lower income are burdened more with

tax. Conversely, every individual whether belonging to low income or high income group are

burdened with equal proportion of tax (Toma, 2019). Therefore, it is the discretion of the

government to decide whether to use progressive, regressive or proportional tax structure. The

report however focuses on progressive and regressive tax structure. To understand the tax

structures the report discusses the characteristics of the respective tax structures and thereby

describes their impacts. The report considers the case of India and its tax structure provides brief

on the existing tax condition in the country and try to draw the impact of a tax structure that

include both the tax methods of progressive tax and regressive tax. Thus, the tax structure exhibit

the characteristics of both the progressive and regressive taxation. The report further explains the

advantages and disadvantages of the said tax structure on the economy of India. India is a

developing country with most of the population belonging to low income group in comparison to

high income group. The report thus critically analyses both the tax structures and thereby by

finds the impact of combined use of both the structure on in a developing country.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAX STRUCTURE

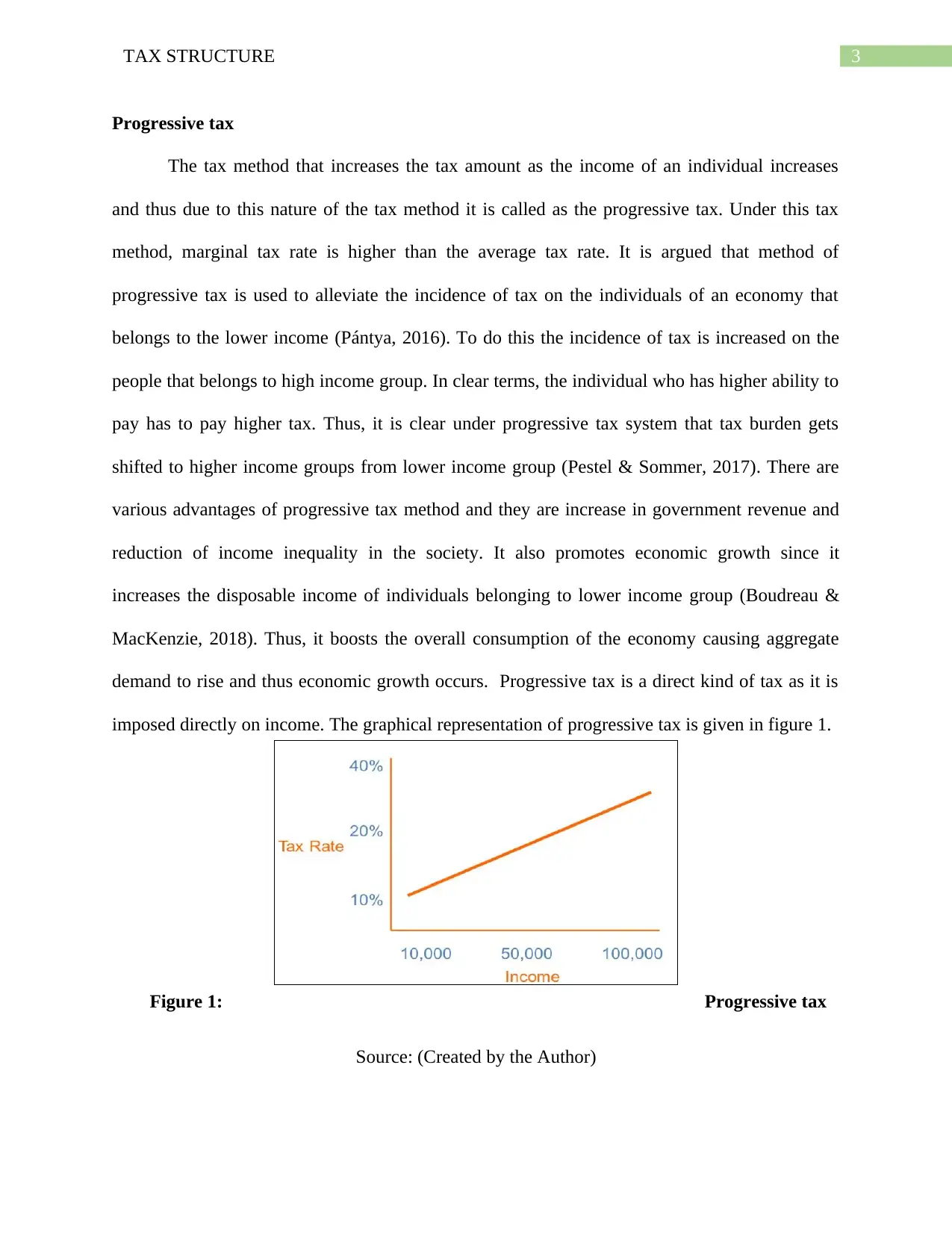

Progressive tax

The tax method that increases the tax amount as the income of an individual increases

and thus due to this nature of the tax method it is called as the progressive tax. Under this tax

method, marginal tax rate is higher than the average tax rate. It is argued that method of

progressive tax is used to alleviate the incidence of tax on the individuals of an economy that

belongs to the lower income (Pántya, 2016). To do this the incidence of tax is increased on the

people that belongs to high income group. In clear terms, the individual who has higher ability to

pay has to pay higher tax. Thus, it is clear under progressive tax system that tax burden gets

shifted to higher income groups from lower income group (Pestel & Sommer, 2017). There are

various advantages of progressive tax method and they are increase in government revenue and

reduction of income inequality in the society. It also promotes economic growth since it

increases the disposable income of individuals belonging to lower income group (Boudreau &

MacKenzie, 2018). Thus, it boosts the overall consumption of the economy causing aggregate

demand to rise and thus economic growth occurs. Progressive tax is a direct kind of tax as it is

imposed directly on income. The graphical representation of progressive tax is given in figure 1.

Figure 1: Progressive tax

Source: (Created by the Author)

Progressive tax

The tax method that increases the tax amount as the income of an individual increases

and thus due to this nature of the tax method it is called as the progressive tax. Under this tax

method, marginal tax rate is higher than the average tax rate. It is argued that method of

progressive tax is used to alleviate the incidence of tax on the individuals of an economy that

belongs to the lower income (Pántya, 2016). To do this the incidence of tax is increased on the

people that belongs to high income group. In clear terms, the individual who has higher ability to

pay has to pay higher tax. Thus, it is clear under progressive tax system that tax burden gets

shifted to higher income groups from lower income group (Pestel & Sommer, 2017). There are

various advantages of progressive tax method and they are increase in government revenue and

reduction of income inequality in the society. It also promotes economic growth since it

increases the disposable income of individuals belonging to lower income group (Boudreau &

MacKenzie, 2018). Thus, it boosts the overall consumption of the economy causing aggregate

demand to rise and thus economic growth occurs. Progressive tax is a direct kind of tax as it is

imposed directly on income. The graphical representation of progressive tax is given in figure 1.

Figure 1: Progressive tax

Source: (Created by the Author)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAX STRUCTURE

In figure 1, progressive curve is shown as an upward sloping curve since with rise in

income percentage of tax imposed upon increases. However, it should be noted that most of the

governments impose tax at slabs and thus in those cases progressive tax curve takes the shape of

steps.

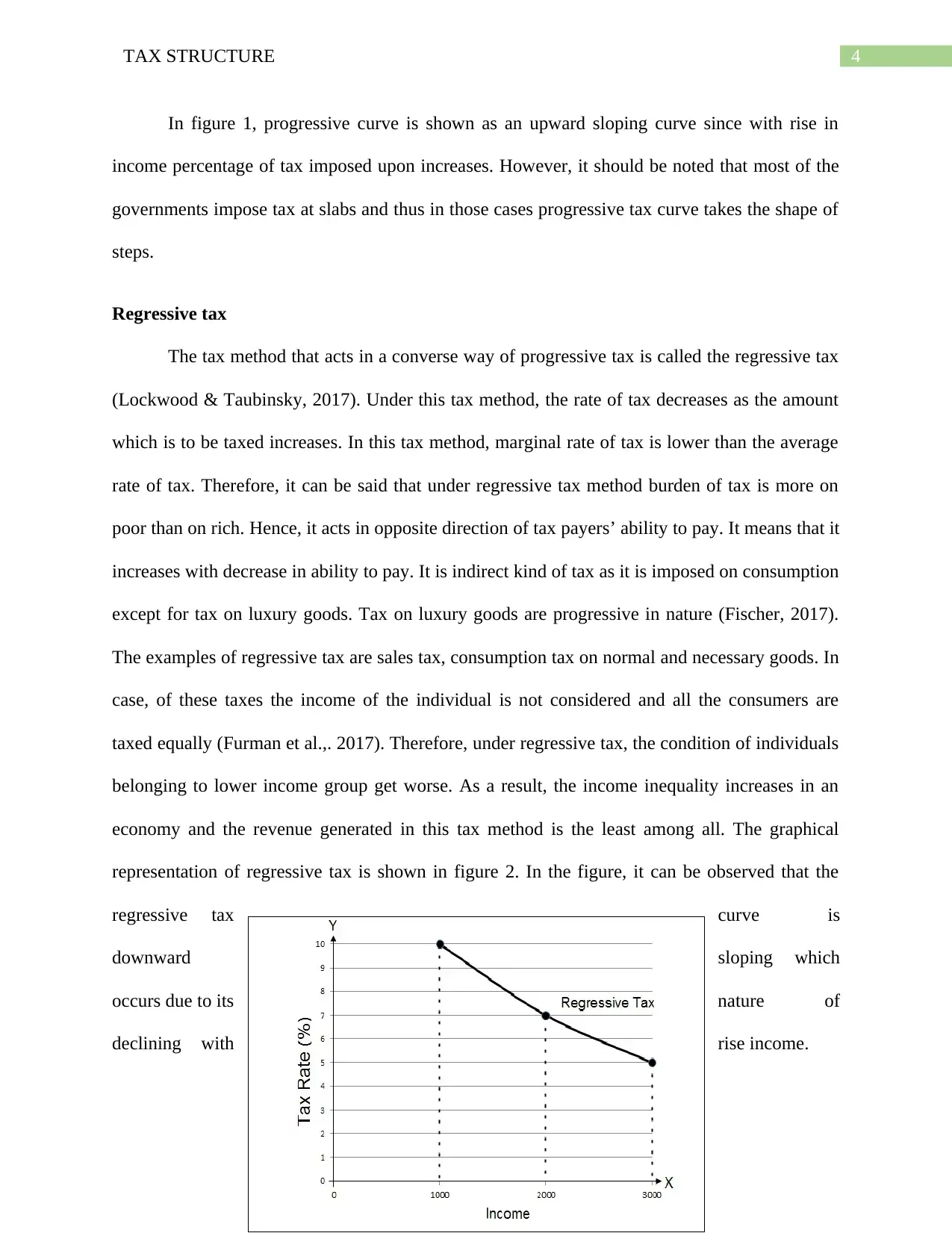

Regressive tax

The tax method that acts in a converse way of progressive tax is called the regressive tax

(Lockwood & Taubinsky, 2017). Under this tax method, the rate of tax decreases as the amount

which is to be taxed increases. In this tax method, marginal rate of tax is lower than the average

rate of tax. Therefore, it can be said that under regressive tax method burden of tax is more on

poor than on rich. Hence, it acts in opposite direction of tax payers’ ability to pay. It means that it

increases with decrease in ability to pay. It is indirect kind of tax as it is imposed on consumption

except for tax on luxury goods. Tax on luxury goods are progressive in nature (Fischer, 2017).

The examples of regressive tax are sales tax, consumption tax on normal and necessary goods. In

case, of these taxes the income of the individual is not considered and all the consumers are

taxed equally (Furman et al.,. 2017). Therefore, under regressive tax, the condition of individuals

belonging to lower income group get worse. As a result, the income inequality increases in an

economy and the revenue generated in this tax method is the least among all. The graphical

representation of regressive tax is shown in figure 2. In the figure, it can be observed that the

regressive tax curve is

downward sloping which

occurs due to its nature of

declining with rise income.

In figure 1, progressive curve is shown as an upward sloping curve since with rise in

income percentage of tax imposed upon increases. However, it should be noted that most of the

governments impose tax at slabs and thus in those cases progressive tax curve takes the shape of

steps.

Regressive tax

The tax method that acts in a converse way of progressive tax is called the regressive tax

(Lockwood & Taubinsky, 2017). Under this tax method, the rate of tax decreases as the amount

which is to be taxed increases. In this tax method, marginal rate of tax is lower than the average

rate of tax. Therefore, it can be said that under regressive tax method burden of tax is more on

poor than on rich. Hence, it acts in opposite direction of tax payers’ ability to pay. It means that it

increases with decrease in ability to pay. It is indirect kind of tax as it is imposed on consumption

except for tax on luxury goods. Tax on luxury goods are progressive in nature (Fischer, 2017).

The examples of regressive tax are sales tax, consumption tax on normal and necessary goods. In

case, of these taxes the income of the individual is not considered and all the consumers are

taxed equally (Furman et al.,. 2017). Therefore, under regressive tax, the condition of individuals

belonging to lower income group get worse. As a result, the income inequality increases in an

economy and the revenue generated in this tax method is the least among all. The graphical

representation of regressive tax is shown in figure 2. In the figure, it can be observed that the

regressive tax curve is

downward sloping which

occurs due to its nature of

declining with rise income.

5TAX STRUCTURE

Figure 2: Regressive tax

Source: (Created by the Author)

Tax structure with progressive and regressive tax characteristics

Tax structure that has the characteristics of both the progressive and regressive tax

structure exhibits an inverted U-shaped tax curve (Vgo, Lauer & World Health Organization,

2018). Therefore, under this tax structure the amount of tax increases as the income of an

individual increases until a certain point is reached and after that the tax structure decreases. The

tax rate is however increases with income (Di Nicola, Boschi & Mongelli, 2017). The rise in

income increases the tax rate but the question is how the taxpayers response to the increase in tax

rate. It has been studied that the tax payers are more responsive to the marginal tax rate than to

absolute tax rate. The meaning of the tax concept is that tax payers weighs the amount of

increase in tax with every unit rise in income (Ballard-Rosa, Martin & Scheve, 2017).

Therefore, it can be stated that if the marginal rate of tax is higher, then the tax payers with

higher income pays more tax with rise in their income. Therefore, the tax structure in this case

takes into account the marginal tax rate. Therefore, the rise in income and would impact the tax

payers that belongs to the first bracket of tax. In the first bracket of tax rate, the amount of tax

Figure 2: Regressive tax

Source: (Created by the Author)

Tax structure with progressive and regressive tax characteristics

Tax structure that has the characteristics of both the progressive and regressive tax

structure exhibits an inverted U-shaped tax curve (Vgo, Lauer & World Health Organization,

2018). Therefore, under this tax structure the amount of tax increases as the income of an

individual increases until a certain point is reached and after that the tax structure decreases. The

tax rate is however increases with income (Di Nicola, Boschi & Mongelli, 2017). The rise in

income increases the tax rate but the question is how the taxpayers response to the increase in tax

rate. It has been studied that the tax payers are more responsive to the marginal tax rate than to

absolute tax rate. The meaning of the tax concept is that tax payers weighs the amount of

increase in tax with every unit rise in income (Ballard-Rosa, Martin & Scheve, 2017).

Therefore, it can be stated that if the marginal rate of tax is higher, then the tax payers with

higher income pays more tax with rise in their income. Therefore, the tax structure in this case

takes into account the marginal tax rate. Therefore, the rise in income and would impact the tax

payers that belongs to the first bracket of tax. In the first bracket of tax rate, the amount of tax

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAX STRUCTURE

payment suddenly rise from zero and thus the marginal rate of tax in this case rise. However, if

the marginal tax rate falls the tax payers would have to pay less for every level of rise in income.

In such a case, the tax structure takes the form of progressive tax initially and becomes

regressive as the marginal tax rate. Therefore, this transition of marginal tax rate from high to

low encourages the tax payers to earn more such that their marginal tax rate decreases (Mehta &

Kaur, 2018). I this way, the government of country would be able to earn more tax revenue.

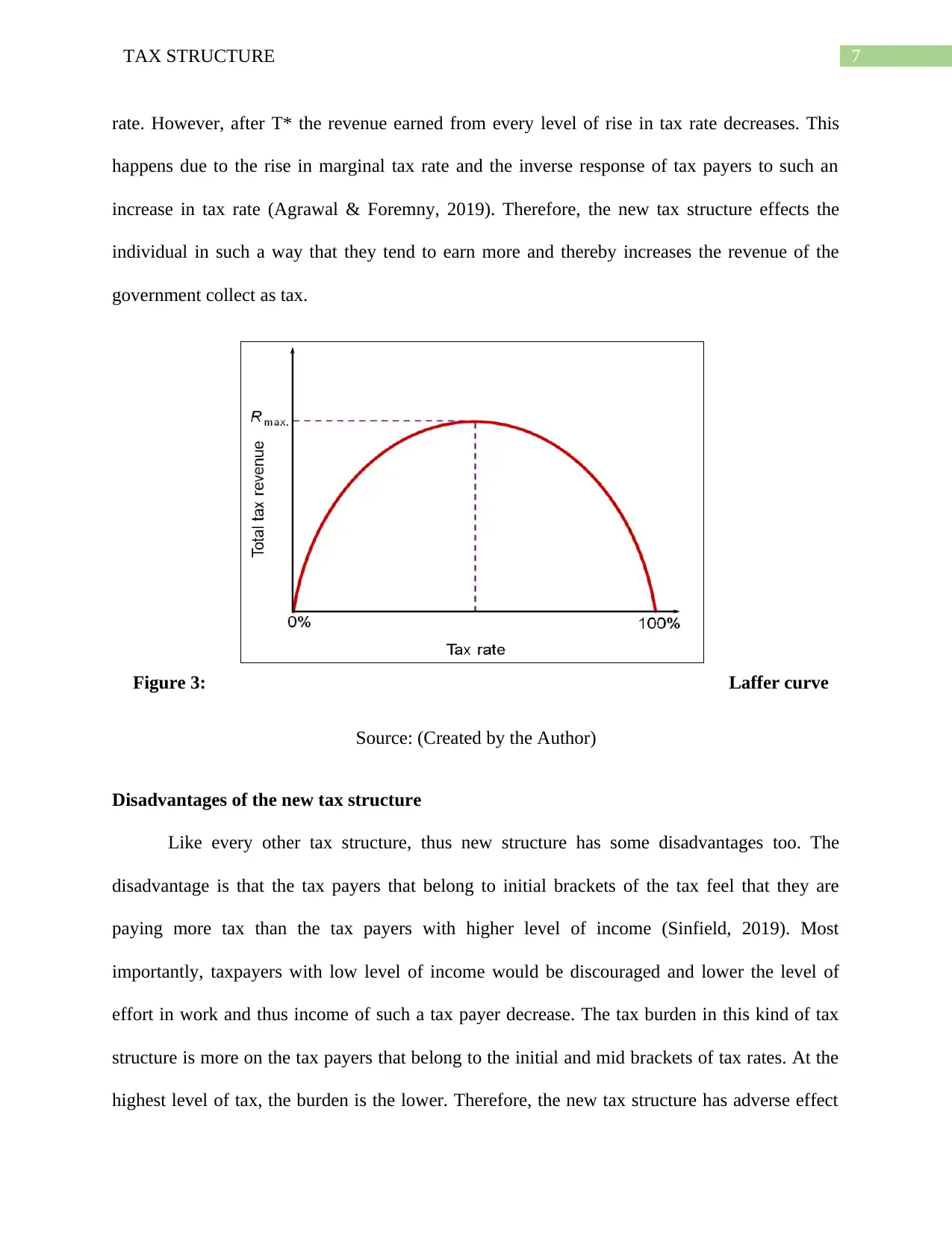

Advantages of the new tax structure

The new tax structure has the characteristics of both the progressive and regressive taxes.

Thus, the advantages the tax structure has are similar to the combination of advantages of

progressive and regressive tax structure (Bogoviz et al., 2019). The advantages of the new tax

structure are that individuals with low income are less impacted or pressurized with tax rate.

However, when the income rises the marginal tax rate increases up to a certain level of income

and then it falls. Beyond this amount of income, the marginal tax rate decreases gradually.

Therefore, with rise income the tax payers will be more eager to increase their by putting in more

effort (Chen, Leith and Ricci, 2018). Therefore, the tax structure escapes the problem explained

by theory of laffer curve. Laffer curve shows that with rise in marginal tax rate with increase in

income, the revenue of the government from collection of tax increases initially. However, if the

marginal tax rate keeps on rising the revenue from tax collection decreases at a higher level of

tax rate. Due to this laffer curve is inverted U-shaped. In figure 2, the graphical representation of

laffer curve has been shown (Gupta & Gupta, 2019). At level 0% tax rate, the amount of revenue

gathered by the government is nil. With rise in tax rate, the sum of revenue gathered by the

government increases till it reaches the point markets Rmax. The revenue is maximized at the

point Rmax and at that point the amount of tax rate is T*. Hence, T* is the highest yielding tax

payment suddenly rise from zero and thus the marginal rate of tax in this case rise. However, if

the marginal tax rate falls the tax payers would have to pay less for every level of rise in income.

In such a case, the tax structure takes the form of progressive tax initially and becomes

regressive as the marginal tax rate. Therefore, this transition of marginal tax rate from high to

low encourages the tax payers to earn more such that their marginal tax rate decreases (Mehta &

Kaur, 2018). I this way, the government of country would be able to earn more tax revenue.

Advantages of the new tax structure

The new tax structure has the characteristics of both the progressive and regressive taxes.

Thus, the advantages the tax structure has are similar to the combination of advantages of

progressive and regressive tax structure (Bogoviz et al., 2019). The advantages of the new tax

structure are that individuals with low income are less impacted or pressurized with tax rate.

However, when the income rises the marginal tax rate increases up to a certain level of income

and then it falls. Beyond this amount of income, the marginal tax rate decreases gradually.

Therefore, with rise income the tax payers will be more eager to increase their by putting in more

effort (Chen, Leith and Ricci, 2018). Therefore, the tax structure escapes the problem explained

by theory of laffer curve. Laffer curve shows that with rise in marginal tax rate with increase in

income, the revenue of the government from collection of tax increases initially. However, if the

marginal tax rate keeps on rising the revenue from tax collection decreases at a higher level of

tax rate. Due to this laffer curve is inverted U-shaped. In figure 2, the graphical representation of

laffer curve has been shown (Gupta & Gupta, 2019). At level 0% tax rate, the amount of revenue

gathered by the government is nil. With rise in tax rate, the sum of revenue gathered by the

government increases till it reaches the point markets Rmax. The revenue is maximized at the

point Rmax and at that point the amount of tax rate is T*. Hence, T* is the highest yielding tax

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAX STRUCTURE

rate. However, after T* the revenue earned from every level of rise in tax rate decreases. This

happens due to the rise in marginal tax rate and the inverse response of tax payers to such an

increase in tax rate (Agrawal & Foremny, 2019). Therefore, the new tax structure effects the

individual in such a way that they tend to earn more and thereby increases the revenue of the

government collect as tax.

Figure 3: Laffer curve

Source: (Created by the Author)

Disadvantages of the new tax structure

Like every other tax structure, thus new structure has some disadvantages too. The

disadvantage is that the tax payers that belong to initial brackets of the tax feel that they are

paying more tax than the tax payers with higher level of income (Sinfield, 2019). Most

importantly, taxpayers with low level of income would be discouraged and lower the level of

effort in work and thus income of such a tax payer decrease. The tax burden in this kind of tax

structure is more on the tax payers that belong to the initial and mid brackets of tax rates. At the

highest level of tax, the burden is the lower. Therefore, the new tax structure has adverse effect

rate. However, after T* the revenue earned from every level of rise in tax rate decreases. This

happens due to the rise in marginal tax rate and the inverse response of tax payers to such an

increase in tax rate (Agrawal & Foremny, 2019). Therefore, the new tax structure effects the

individual in such a way that they tend to earn more and thereby increases the revenue of the

government collect as tax.

Figure 3: Laffer curve

Source: (Created by the Author)

Disadvantages of the new tax structure

Like every other tax structure, thus new structure has some disadvantages too. The

disadvantage is that the tax payers that belong to initial brackets of the tax feel that they are

paying more tax than the tax payers with higher level of income (Sinfield, 2019). Most

importantly, taxpayers with low level of income would be discouraged and lower the level of

effort in work and thus income of such a tax payer decrease. The tax burden in this kind of tax

structure is more on the tax payers that belong to the initial and mid brackets of tax rates. At the

highest level of tax, the burden is the lower. Therefore, the new tax structure has adverse effect

8TAX STRUCTURE

on the country that is using (Dang, Fang & He, 2019). The question in this cases arises is how a

developing country is impacted by this kind of tax structure.

Tax Structure in a developing country

For the estimation of the impact of new tax structure on a developing country considering

the tax structure present in India. In Indian tax structure, the tax is imposed at slabs. For different

level of income tax rate is different for different level of income (Sachsida, Mendonca &

Moreira, 2016). However, it should be noted that in Indian tax structure there is limit of income

below which the individuals are not taxed that is there is a 0% tax slab included in the tax

structure. The details of tax structure in India is given in table 1. It can be seen in the table that

individuals having income lower than or equal to 2, 50, 000 per annum are exempted from any₹

kind of tax in the tax structure of the country. The tax slab starts in Indian above the income of ₹

2, 50, 000. This is the first slab of tax where the tax charged at 5% up to the income level of 5,₹

00, 000. Beyond the said amount of income, the tax rate increased by 5% and thus the total tax

rate becomes 10%. Up to the level of 7, 50, 000 of income the amount of second slab of tax₹

rate remains and then again increases by 5%. The individuals with level of income equal to 10,₹

00, 000 or less thus pays tax rate of 15%. This can be observed from the table that at every

increase in income by 2, 50, 000 after the exempted slab of 2, 50, 000 the tax rate increases₹ ₹

by 5% till the level of income reached 15, 00, 000. Thus, as per the table the highest level of₹

tax rate increases till 30%. No increment in tax rate is there in Indian tax system (Singh, 2018).

Therefore, at every level of income after 15, 00, 000 the tax payers has to pay at 30% rate of₹

tax. However, it should be noted that the amount of tax increase is payable against the amount of

increased income not on the total income. That is the tax rates are fixed the respective slabs only.

on the country that is using (Dang, Fang & He, 2019). The question in this cases arises is how a

developing country is impacted by this kind of tax structure.

Tax Structure in a developing country

For the estimation of the impact of new tax structure on a developing country considering

the tax structure present in India. In Indian tax structure, the tax is imposed at slabs. For different

level of income tax rate is different for different level of income (Sachsida, Mendonca &

Moreira, 2016). However, it should be noted that in Indian tax structure there is limit of income

below which the individuals are not taxed that is there is a 0% tax slab included in the tax

structure. The details of tax structure in India is given in table 1. It can be seen in the table that

individuals having income lower than or equal to 2, 50, 000 per annum are exempted from any₹

kind of tax in the tax structure of the country. The tax slab starts in Indian above the income of ₹

2, 50, 000. This is the first slab of tax where the tax charged at 5% up to the income level of 5,₹

00, 000. Beyond the said amount of income, the tax rate increased by 5% and thus the total tax

rate becomes 10%. Up to the level of 7, 50, 000 of income the amount of second slab of tax₹

rate remains and then again increases by 5%. The individuals with level of income equal to 10,₹

00, 000 or less thus pays tax rate of 15%. This can be observed from the table that at every

increase in income by 2, 50, 000 after the exempted slab of 2, 50, 000 the tax rate increases₹ ₹

by 5% till the level of income reached 15, 00, 000. Thus, as per the table the highest level of₹

tax rate increases till 30%. No increment in tax rate is there in Indian tax system (Singh, 2018).

Therefore, at every level of income after 15, 00, 000 the tax payers has to pay at 30% rate of₹

tax. However, it should be noted that the amount of tax increase is payable against the amount of

increased income not on the total income. That is the tax rates are fixed the respective slabs only.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAX STRUCTURE

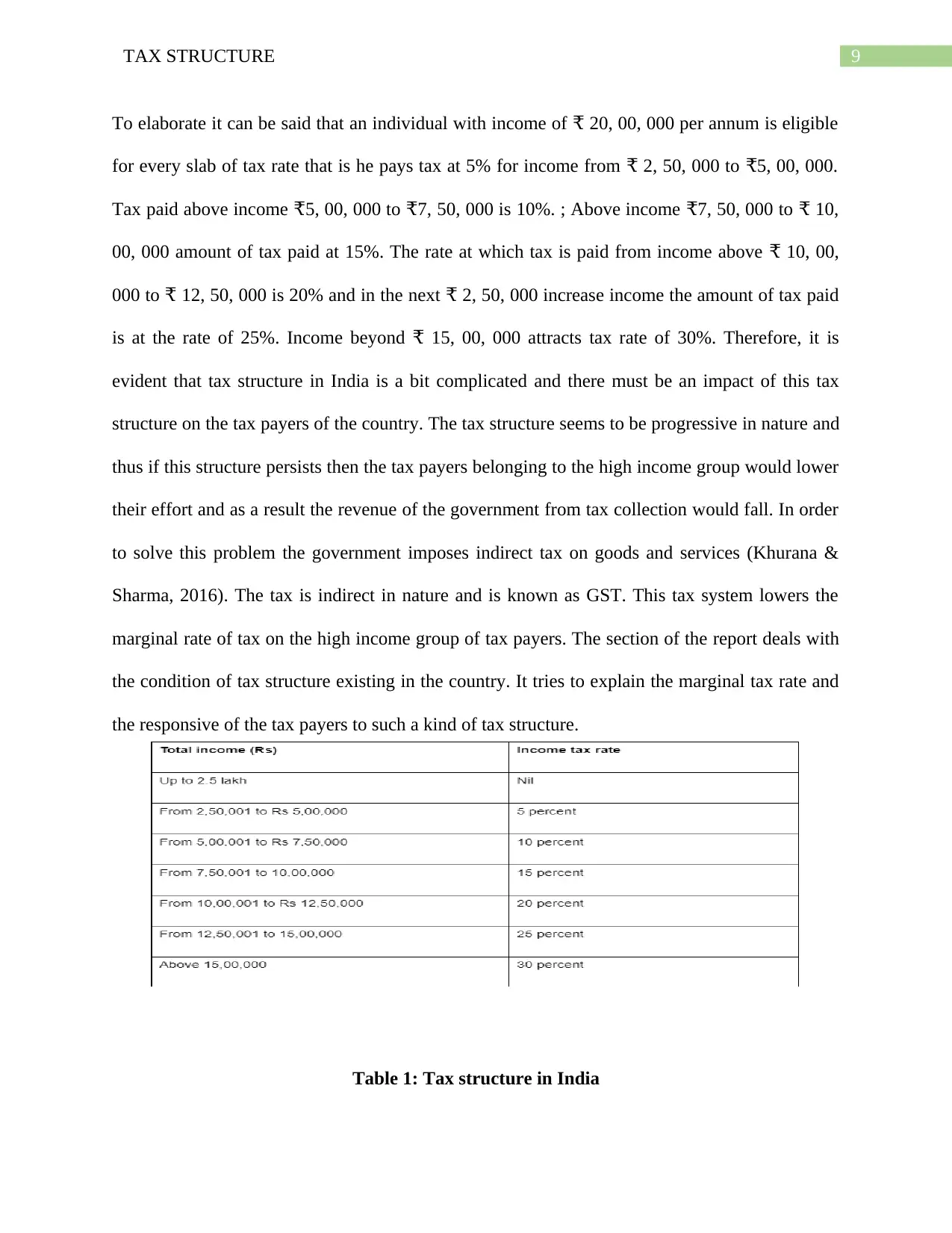

To elaborate it can be said that an individual with income of 20, 00, 000 per annum is eligible₹

for every slab of tax rate that is he pays tax at 5% for income from 2, 50, 000 to 5, 00, 000.₹ ₹

Tax paid above income 5, 00, 000 to 7, 50, 000 is 10%. ; Above income 7, 50, 000 to 10,₹ ₹ ₹ ₹

00, 000 amount of tax paid at 15%. The rate at which tax is paid from income above 10, 00,₹

000 to 12, 50, 000 is 20% and in the next 2, 50, 000 increase income the amount of tax paid₹ ₹

is at the rate of 25%. Income beyond 15, 00, 000 attracts tax rate of 30%. Therefore, it is₹

evident that tax structure in India is a bit complicated and there must be an impact of this tax

structure on the tax payers of the country. The tax structure seems to be progressive in nature and

thus if this structure persists then the tax payers belonging to the high income group would lower

their effort and as a result the revenue of the government from tax collection would fall. In order

to solve this problem the government imposes indirect tax on goods and services (Khurana &

Sharma, 2016). The tax is indirect in nature and is known as GST. This tax system lowers the

marginal rate of tax on the high income group of tax payers. The section of the report deals with

the condition of tax structure existing in the country. It tries to explain the marginal tax rate and

the responsive of the tax payers to such a kind of tax structure.

Table 1: Tax structure in India

To elaborate it can be said that an individual with income of 20, 00, 000 per annum is eligible₹

for every slab of tax rate that is he pays tax at 5% for income from 2, 50, 000 to 5, 00, 000.₹ ₹

Tax paid above income 5, 00, 000 to 7, 50, 000 is 10%. ; Above income 7, 50, 000 to 10,₹ ₹ ₹ ₹

00, 000 amount of tax paid at 15%. The rate at which tax is paid from income above 10, 00,₹

000 to 12, 50, 000 is 20% and in the next 2, 50, 000 increase income the amount of tax paid₹ ₹

is at the rate of 25%. Income beyond 15, 00, 000 attracts tax rate of 30%. Therefore, it is₹

evident that tax structure in India is a bit complicated and there must be an impact of this tax

structure on the tax payers of the country. The tax structure seems to be progressive in nature and

thus if this structure persists then the tax payers belonging to the high income group would lower

their effort and as a result the revenue of the government from tax collection would fall. In order

to solve this problem the government imposes indirect tax on goods and services (Khurana &

Sharma, 2016). The tax is indirect in nature and is known as GST. This tax system lowers the

marginal rate of tax on the high income group of tax payers. The section of the report deals with

the condition of tax structure existing in the country. It tries to explain the marginal tax rate and

the responsive of the tax payers to such a kind of tax structure.

Table 1: Tax structure in India

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAX STRUCTURE

Source: (Created by the Author)

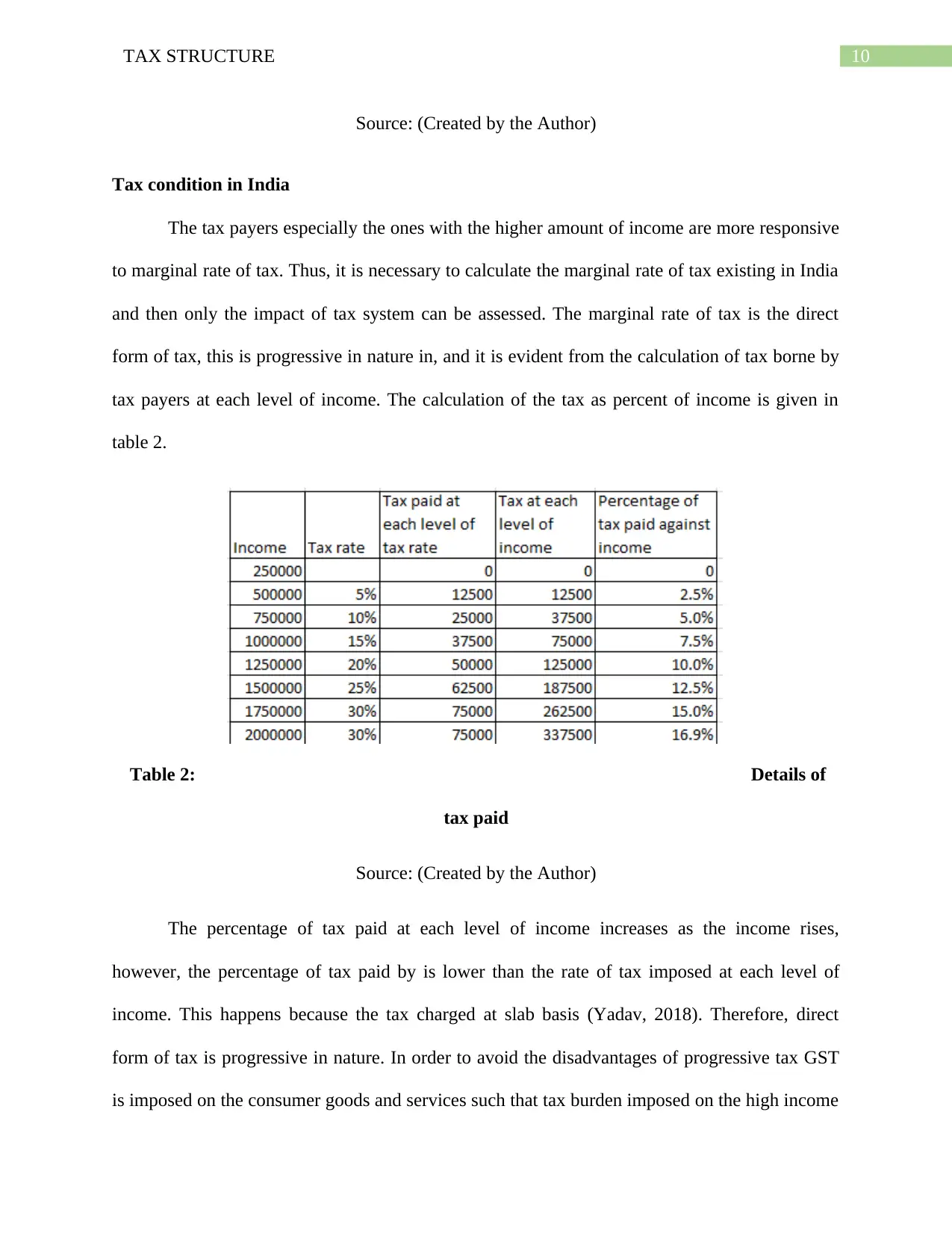

Tax condition in India

The tax payers especially the ones with the higher amount of income are more responsive

to marginal rate of tax. Thus, it is necessary to calculate the marginal rate of tax existing in India

and then only the impact of tax system can be assessed. The marginal rate of tax is the direct

form of tax, this is progressive in nature in, and it is evident from the calculation of tax borne by

tax payers at each level of income. The calculation of the tax as percent of income is given in

table 2.

Table 2: Details of

tax paid

Source: (Created by the Author)

The percentage of tax paid at each level of income increases as the income rises,

however, the percentage of tax paid by is lower than the rate of tax imposed at each level of

income. This happens because the tax charged at slab basis (Yadav, 2018). Therefore, direct

form of tax is progressive in nature. In order to avoid the disadvantages of progressive tax GST

is imposed on the consumer goods and services such that tax burden imposed on the high income

Source: (Created by the Author)

Tax condition in India

The tax payers especially the ones with the higher amount of income are more responsive

to marginal rate of tax. Thus, it is necessary to calculate the marginal rate of tax existing in India

and then only the impact of tax system can be assessed. The marginal rate of tax is the direct

form of tax, this is progressive in nature in, and it is evident from the calculation of tax borne by

tax payers at each level of income. The calculation of the tax as percent of income is given in

table 2.

Table 2: Details of

tax paid

Source: (Created by the Author)

The percentage of tax paid at each level of income increases as the income rises,

however, the percentage of tax paid by is lower than the rate of tax imposed at each level of

income. This happens because the tax charged at slab basis (Yadav, 2018). Therefore, direct

form of tax is progressive in nature. In order to avoid the disadvantages of progressive tax GST

is imposed on the consumer goods and services such that tax burden imposed on the high income

11TAX STRUCTURE

tax payers is reduced. In addition to that, there are provision of tax exemption or tax return upon

amount of investments made (Chaurey, 2017). More is the investment made more is the amount

of tax return or exemption. Individuals with higher income are able to invest more and thus the

tax exemption and tax return policies are mostly utilized by this category tax payers. On the

other hand, as the consumer goods and services are taxed the burden on the low income

taxpayers increase (Thomas et al., 217). Therefore, the tax curve slopes downward at the later

part. Thus, the tax condition of India exhibits the new structure of tax as stated above.

Impact of combined tax structure on India

India is a very diverse country and apart from central tax system there are different state

tax system. The state tax system however does not include the direct taxes like income tax but

comprises of most of the indirect taxes. Thus, due to different state taxes individuals living in

different states are taxed differently. In addition to that the taxed goods and services are available

mostly in urban areas in comparison to rural areas and thus individuals living in urban areas are

taxed at highly. These are the adverse side of the taxed system existing in India (Ghadge, 2019).

The tax system has helped the country to improve as well by increasing volume of savings. This

happens due to tax return policies that can be availed only if there is investment. The tax system

in India is somehow flawed as there is enormous amount of tax evasion incidents even after

existence of policies like tax exemption and tax return.

Conclusion

The above discussion on tax system puts light on the tax system like progressive and

regressive tax systems. The detailed discussion on the respective tax systems leads to the

conclusion that progressive tax structure deprives the tax payers belonging to higher income

group and in the case of regressive tax structure the low income tax payers are deprived.

tax payers is reduced. In addition to that, there are provision of tax exemption or tax return upon

amount of investments made (Chaurey, 2017). More is the investment made more is the amount

of tax return or exemption. Individuals with higher income are able to invest more and thus the

tax exemption and tax return policies are mostly utilized by this category tax payers. On the

other hand, as the consumer goods and services are taxed the burden on the low income

taxpayers increase (Thomas et al., 217). Therefore, the tax curve slopes downward at the later

part. Thus, the tax condition of India exhibits the new structure of tax as stated above.

Impact of combined tax structure on India

India is a very diverse country and apart from central tax system there are different state

tax system. The state tax system however does not include the direct taxes like income tax but

comprises of most of the indirect taxes. Thus, due to different state taxes individuals living in

different states are taxed differently. In addition to that the taxed goods and services are available

mostly in urban areas in comparison to rural areas and thus individuals living in urban areas are

taxed at highly. These are the adverse side of the taxed system existing in India (Ghadge, 2019).

The tax system has helped the country to improve as well by increasing volume of savings. This

happens due to tax return policies that can be availed only if there is investment. The tax system

in India is somehow flawed as there is enormous amount of tax evasion incidents even after

existence of policies like tax exemption and tax return.

Conclusion

The above discussion on tax system puts light on the tax system like progressive and

regressive tax systems. The detailed discussion on the respective tax systems leads to the

conclusion that progressive tax structure deprives the tax payers belonging to higher income

group and in the case of regressive tax structure the low income tax payers are deprived.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.