Analysis of Tax Systems: Progressive, Regressive, and UK Tax Laws

VerifiedAdded on 2020/10/23

|10

|2576

|121

Report

AI Summary

This report provides a comprehensive overview of tax systems, focusing on progressive and regressive models, with examples illustrating their application and impact. It delves into the sources of UK tax law, differentiating between direct and indirect taxes and examining the roles of statute law, case law, and HMRC guidance. The report then contrasts tax avoidance and tax evasion, outlining their implications for both individuals and the government, including legal and economic consequences. The analysis includes comparisons between the two tax systems and offers an opinion on which is fairer. The report concludes with a discussion on the implications of each for the economy and the government. The document is contributed by a student to be published on the website Desklib. Desklib is a platform which provides all the necessary AI based study tools for students.

PRINCIPLES OF TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TAX SYSTEMS .............................................................................................................................1

Progressive tax systems with examples......................................................................................1

Regressive tax systems with examples.......................................................................................1

Comparison in two systems with opinion on better and fairer system.......................................2

SOURCES OF TAX LAWS............................................................................................................3

Discussing different sources of tax law In UK...........................................................................3

TAX AVOIDANCE VERSUS TAX EVASION............................................................................5

Differentiating among tax avoidance and evasion with implications of both on individual and

on government.............................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TAX SYSTEMS .............................................................................................................................1

Progressive tax systems with examples......................................................................................1

Regressive tax systems with examples.......................................................................................1

Comparison in two systems with opinion on better and fairer system.......................................2

SOURCES OF TAX LAWS............................................................................................................3

Discussing different sources of tax law In UK...........................................................................3

TAX AVOIDANCE VERSUS TAX EVASION............................................................................5

Differentiating among tax avoidance and evasion with implications of both on individual and

on government.............................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................8

INTRODUCTION

Tax is replicates as compulsory payment made through individuals and companies to

government with context to well established rules along with criteria like property owned,

income earned, capital gains made or expenditure incurred on imported and domestic articles.

The present report will provide discussion about progressive and regressive tax system with

appropriate examples. Similarly, this would give comparison of these tax systems and discussion

of different sources of tax law in UK. Lastly, this report will differentiate among tax avoidance

and tax evasion with reference to implication of both on individual and on government as well.

TAX SYSTEMS

Progressive tax systems with examples

Progressive tax is a tax rate which is taxable as value raises as this is segmented into tax

brackets which progress to successively with higher rates. This is a tax which impose lower tax

rate on earners of low income compared with higher income on basis of ability of taxpayer to

pay. It means for undertaking larger percentage through high income earners than it does from

individuals of low income (Bird and Davis-Nozemack, 2018). This is the one which charges of

high tax rate for one who earns high income. The main reason behind this that lower income

would spend a great percentage of their lower income for maintaining standard of living.

Simultaneously, who are richer typically afford the necessities in life. This system decreases the

tax burdens on people who could least afford for repay and these systems leave more money in

pockets of low-wage earners who spend money and stimulate the economy. This tax systems has

capability for collecting more taxes comparatively to flat taxes and tax rates indexed for

increment as income climb. In simple words, it allows people with great amount of resources to

fund a high portion of services as everyone relies to people and business .

The example of progressive tax are stated as investment income taxes which are most of

the activities which generate income and it reduces through excess money for involving and

saving in investment. Similarly, estate tax is form of tax levied against whom succeed a deceased

as this only applies when estate of deceased is above a specific amount as set through

government.

Regressive tax systems with examples

Taxes are regressive when it impose harsh burden on poor compared to rich. On basis of

poor families, high proportion of their income pays for food, transportation and shelter. This tax

1

Tax is replicates as compulsory payment made through individuals and companies to

government with context to well established rules along with criteria like property owned,

income earned, capital gains made or expenditure incurred on imported and domestic articles.

The present report will provide discussion about progressive and regressive tax system with

appropriate examples. Similarly, this would give comparison of these tax systems and discussion

of different sources of tax law in UK. Lastly, this report will differentiate among tax avoidance

and tax evasion with reference to implication of both on individual and on government as well.

TAX SYSTEMS

Progressive tax systems with examples

Progressive tax is a tax rate which is taxable as value raises as this is segmented into tax

brackets which progress to successively with higher rates. This is a tax which impose lower tax

rate on earners of low income compared with higher income on basis of ability of taxpayer to

pay. It means for undertaking larger percentage through high income earners than it does from

individuals of low income (Bird and Davis-Nozemack, 2018). This is the one which charges of

high tax rate for one who earns high income. The main reason behind this that lower income

would spend a great percentage of their lower income for maintaining standard of living.

Simultaneously, who are richer typically afford the necessities in life. This system decreases the

tax burdens on people who could least afford for repay and these systems leave more money in

pockets of low-wage earners who spend money and stimulate the economy. This tax systems has

capability for collecting more taxes comparatively to flat taxes and tax rates indexed for

increment as income climb. In simple words, it allows people with great amount of resources to

fund a high portion of services as everyone relies to people and business .

The example of progressive tax are stated as investment income taxes which are most of

the activities which generate income and it reduces through excess money for involving and

saving in investment. Similarly, estate tax is form of tax levied against whom succeed a deceased

as this only applies when estate of deceased is above a specific amount as set through

government.

Regressive tax systems with examples

Taxes are regressive when it impose harsh burden on poor compared to rich. On basis of

poor families, high proportion of their income pays for food, transportation and shelter. This tax

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is applied uniformly by undertaking large percentage of income through low income earners

compared to high income earners. Simultaneously, it is applied in such aspect that decrement in

tax rate with increment in income of tax payer. This places high burden on demographics of low

income instead of population of high income and imposes burden is identified through

percentage of tax amount to income. Moreover, low income population carries more burden as

this tax system is not used for purpose of income taxation. On the contrary, this is used with

many other taxes like sales or sin tax. It is directly opposite to progressive tax. This tax system

encourages investment and saving as high income earners pays less tax as they have presence of

discretionary funds for application of savings and investment. These savings and investments,

high earners of income produce more income which is subject to income taxes. If wealthy

generates more income, then theory goes with aggregate of economy and growth GDP to nation.

These taxes raises net government revenue as additional investments generates high taxable

income and cycle initiates again as more wealth, investment, tax revenues and all through lower

regressive taxes.

The example of regressive taxes as A and B went for shopping and bought clothes where

each cost was 300 as rate of sales tax is 13%. However, each paid 39 as taxes and salary of A is

3000 per month and B as 4000. As A and B both paid similar amount of tax, so proportion of tax

amount to income from B was 39/4000 as 0.975% and A as 39/3000 as 1.30%. Henceforth, sales

tax is regressive.

Comparison in two systems with opinion on better and fairer system

Progressive tax is elaborated as tax whose rate raises along with increment in income of

payer. The individuals who attain high income has high proportion of income undertaken

for paying tax (Progressive tax, 2019). Conversely, regressive rate is one with increment

in rate as with decrement in income of payer.

Progressive tax is tax where average tax rate or aggregate of total amount paid as

particular income percentage. The tax might be progressive if people with higher income

repays a higher tax rate. On alternative basis, taxes could be progressive if levied tax on

action or purchase which is common in wealthier people such as inheritance tax, luxury

car tax.

However, regressive tax is opposite with average tax rate or amount of tax paid as

particular income percentage, reduces when income raises (Regressive tax, 2019). The

2

compared to high income earners. Simultaneously, it is applied in such aspect that decrement in

tax rate with increment in income of tax payer. This places high burden on demographics of low

income instead of population of high income and imposes burden is identified through

percentage of tax amount to income. Moreover, low income population carries more burden as

this tax system is not used for purpose of income taxation. On the contrary, this is used with

many other taxes like sales or sin tax. It is directly opposite to progressive tax. This tax system

encourages investment and saving as high income earners pays less tax as they have presence of

discretionary funds for application of savings and investment. These savings and investments,

high earners of income produce more income which is subject to income taxes. If wealthy

generates more income, then theory goes with aggregate of economy and growth GDP to nation.

These taxes raises net government revenue as additional investments generates high taxable

income and cycle initiates again as more wealth, investment, tax revenues and all through lower

regressive taxes.

The example of regressive taxes as A and B went for shopping and bought clothes where

each cost was 300 as rate of sales tax is 13%. However, each paid 39 as taxes and salary of A is

3000 per month and B as 4000. As A and B both paid similar amount of tax, so proportion of tax

amount to income from B was 39/4000 as 0.975% and A as 39/3000 as 1.30%. Henceforth, sales

tax is regressive.

Comparison in two systems with opinion on better and fairer system

Progressive tax is elaborated as tax whose rate raises along with increment in income of

payer. The individuals who attain high income has high proportion of income undertaken

for paying tax (Progressive tax, 2019). Conversely, regressive rate is one with increment

in rate as with decrement in income of payer.

Progressive tax is tax where average tax rate or aggregate of total amount paid as

particular income percentage. The tax might be progressive if people with higher income

repays a higher tax rate. On alternative basis, taxes could be progressive if levied tax on

action or purchase which is common in wealthier people such as inheritance tax, luxury

car tax.

However, regressive tax is opposite with average tax rate or amount of tax paid as

particular income percentage, reduces when income raises (Regressive tax, 2019). The

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

example of this tax is lump sum tax, head tax which needs to be paid by every tax payer

as similar tax amount.

Basis Regressive tax Progressive tax

Consideration Indirect taxes Direct taxes

Benefits High income group Low income group

Assessment Asset purchased with

particular percentage

(Difference Between

Progressive and Regressive

Tax, 2019).

On profit or income

In nutshell, opposite of progressive system is regressive tax rate where liability decreases

as increment in taxable amount. Regardless of rate applied, objective of government is to gather

money through citizens and after pooling all money, it give public goods and services such as

security and affordable health care.

SOURCES OF TAX LAWS

Discussing different sources of tax law In UK

The taxation system of UK is composed of number of multiple taxes such as direct or

indirect taxes. Moreover, direct taxes are charged on income, other gains and profit are either

deducted at specific source or directly paid to authorities of tax. The main direct taxes are

payable through individuals are capital gains tax, income tax and inheritance tax. Although main

direct tax payable through organizations are corporation tax. These taxes are directly

administrated through HM revenue and customs merge with inland revenue (Introduction to the

UK tax system, 2018). Simultaneously, Indirect taxes are referred as taxes on spending as they

are charged when taxpayer purchases item paid to particular vendor as contribution of purchase

price of item. This is replicated as duty of vendor for surpassing tax on to authorities of tax. The

indirect taxes considers value added tax, custom duties, stamp duties along with excise duties

which are directly levied on tobacco, alcohol and petrol (Armour and et.al., 2018). There is

absence of any single source of tax law of UK as basic rules laid in Act of Parliament but it is

left to courts for purpose of interpreting these acts and to offer with detail of tax system.

3

as similar tax amount.

Basis Regressive tax Progressive tax

Consideration Indirect taxes Direct taxes

Benefits High income group Low income group

Assessment Asset purchased with

particular percentage

(Difference Between

Progressive and Regressive

Tax, 2019).

On profit or income

In nutshell, opposite of progressive system is regressive tax rate where liability decreases

as increment in taxable amount. Regardless of rate applied, objective of government is to gather

money through citizens and after pooling all money, it give public goods and services such as

security and affordable health care.

SOURCES OF TAX LAWS

Discussing different sources of tax law In UK

The taxation system of UK is composed of number of multiple taxes such as direct or

indirect taxes. Moreover, direct taxes are charged on income, other gains and profit are either

deducted at specific source or directly paid to authorities of tax. The main direct taxes are

payable through individuals are capital gains tax, income tax and inheritance tax. Although main

direct tax payable through organizations are corporation tax. These taxes are directly

administrated through HM revenue and customs merge with inland revenue (Introduction to the

UK tax system, 2018). Simultaneously, Indirect taxes are referred as taxes on spending as they

are charged when taxpayer purchases item paid to particular vendor as contribution of purchase

price of item. This is replicated as duty of vendor for surpassing tax on to authorities of tax. The

indirect taxes considers value added tax, custom duties, stamp duties along with excise duties

which are directly levied on tobacco, alcohol and petrol (Armour and et.al., 2018). There is

absence of any single source of tax law of UK as basic rules laid in Act of Parliament but it is

left to courts for purpose of interpreting these acts and to offer with detail of tax system.

3

The tax system of UK applies throughout the UK as England, Wales, Northern Ireland,

Scotland and various other smaller islands around British cost. There is consideration of oil

drilling platforms in British territorial waters but excludes Channel island, Republic of Ireland

and the Isle of man.

Statute law

The basic rules of tax system of UK are directly embodied in numerous tax statues or

with parliament Act (A complete guide to the UK tax system, 2019). At the current stage, main

statues is in force for every tax is stated below:

Although, these statues are directly amended every year through annual Finance Act on

basis of proposals of budget are put forwards through Chancellor of the Exchequer. These tax

statutes offers to make detailed regulation through statutory instrument (Hearson, 2018). This is

a document which is directly laid prior to parliament and then it becomes law within stated

duration unless with objections raised to it.

Case law

Over the past many years, tax authorities and taxpayers have disagreed frequently over

tax act's interpretation. As per its outcome, multiple of thousands of tax cases have brought prior

to courts. Generally, these decisions are made through judges in these cases form important

contribution of UK's tax law.

4

Scotland and various other smaller islands around British cost. There is consideration of oil

drilling platforms in British territorial waters but excludes Channel island, Republic of Ireland

and the Isle of man.

Statute law

The basic rules of tax system of UK are directly embodied in numerous tax statues or

with parliament Act (A complete guide to the UK tax system, 2019). At the current stage, main

statues is in force for every tax is stated below:

Although, these statues are directly amended every year through annual Finance Act on

basis of proposals of budget are put forwards through Chancellor of the Exchequer. These tax

statutes offers to make detailed regulation through statutory instrument (Hearson, 2018). This is

a document which is directly laid prior to parliament and then it becomes law within stated

duration unless with objections raised to it.

Case law

Over the past many years, tax authorities and taxpayers have disagreed frequently over

tax act's interpretation. As per its outcome, multiple of thousands of tax cases have brought prior

to courts. Generally, these decisions are made through judges in these cases form important

contribution of UK's tax law.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

HMRC guidance and statement made through tax authorities

The main statements along with other documents generated to HMRC as guidance for

taxation law is stated below:

Statement of practice sets HMRC interpretation of legislation of tax along with clarifying

method in which law would be applied in practice.

The Extra Statutory concession comprises relaxation which provides reduction to

taxpayers in liability which is not entitled under strict letter of law. Usually, concessions

are prepared for purpose of resolving anomalies or for relieving hardship. The process of

providing statutory impact to certain ESC is underway and is being done through mode of

statutory instruments.

Press releases are issued throughout year on variety of related to tax subjects as of special

interests are press releases along with notes issued on daily budget which gives detail

explanation on budget proposals.

HMRC gives comprehensive set of manual of internal tax for purpose of guidance of its

staff. These manuals might be directly inspected at HMRC enquiry centres linked of

accessed through internet.

TAX AVOIDANCE VERSUS TAX EVASION

Differentiating among tax avoidance and evasion with implications of both on individual and on

government

Tax avoidance is made to beat intent of law by undertaking unfair advantage of

shortcomings with tax rules. This is referred to extracting tools or methods for avoiding taxes

payment which are within limits of law. Generally, this could be done through adjusting accounts

in such manner which would not violate any tax rules and tax concurrence will also be

minimised. Tax invasion is an illegal act made to escape through paying taxes as these illegal

practices could be deliberate concealment of income, accounts manipulations, disclosure of

unreal expenses for deductions, reflects personal expenditure as business expenses,

overstatement of tax credit or suppression of capital gains and profits etc.

Tax avoidance Tax evasion

This minimizes tax liability by undertaking for

not violating tax rules.

It is meant that decreasing tax liability with

application of illegal methods.

5

The main statements along with other documents generated to HMRC as guidance for

taxation law is stated below:

Statement of practice sets HMRC interpretation of legislation of tax along with clarifying

method in which law would be applied in practice.

The Extra Statutory concession comprises relaxation which provides reduction to

taxpayers in liability which is not entitled under strict letter of law. Usually, concessions

are prepared for purpose of resolving anomalies or for relieving hardship. The process of

providing statutory impact to certain ESC is underway and is being done through mode of

statutory instruments.

Press releases are issued throughout year on variety of related to tax subjects as of special

interests are press releases along with notes issued on daily budget which gives detail

explanation on budget proposals.

HMRC gives comprehensive set of manual of internal tax for purpose of guidance of its

staff. These manuals might be directly inspected at HMRC enquiry centres linked of

accessed through internet.

TAX AVOIDANCE VERSUS TAX EVASION

Differentiating among tax avoidance and evasion with implications of both on individual and on

government

Tax avoidance is made to beat intent of law by undertaking unfair advantage of

shortcomings with tax rules. This is referred to extracting tools or methods for avoiding taxes

payment which are within limits of law. Generally, this could be done through adjusting accounts

in such manner which would not violate any tax rules and tax concurrence will also be

minimised. Tax invasion is an illegal act made to escape through paying taxes as these illegal

practices could be deliberate concealment of income, accounts manipulations, disclosure of

unreal expenses for deductions, reflects personal expenditure as business expenses,

overstatement of tax credit or suppression of capital gains and profits etc.

Tax avoidance Tax evasion

This minimizes tax liability by undertaking for

not violating tax rules.

It is meant that decreasing tax liability with

application of illegal methods.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

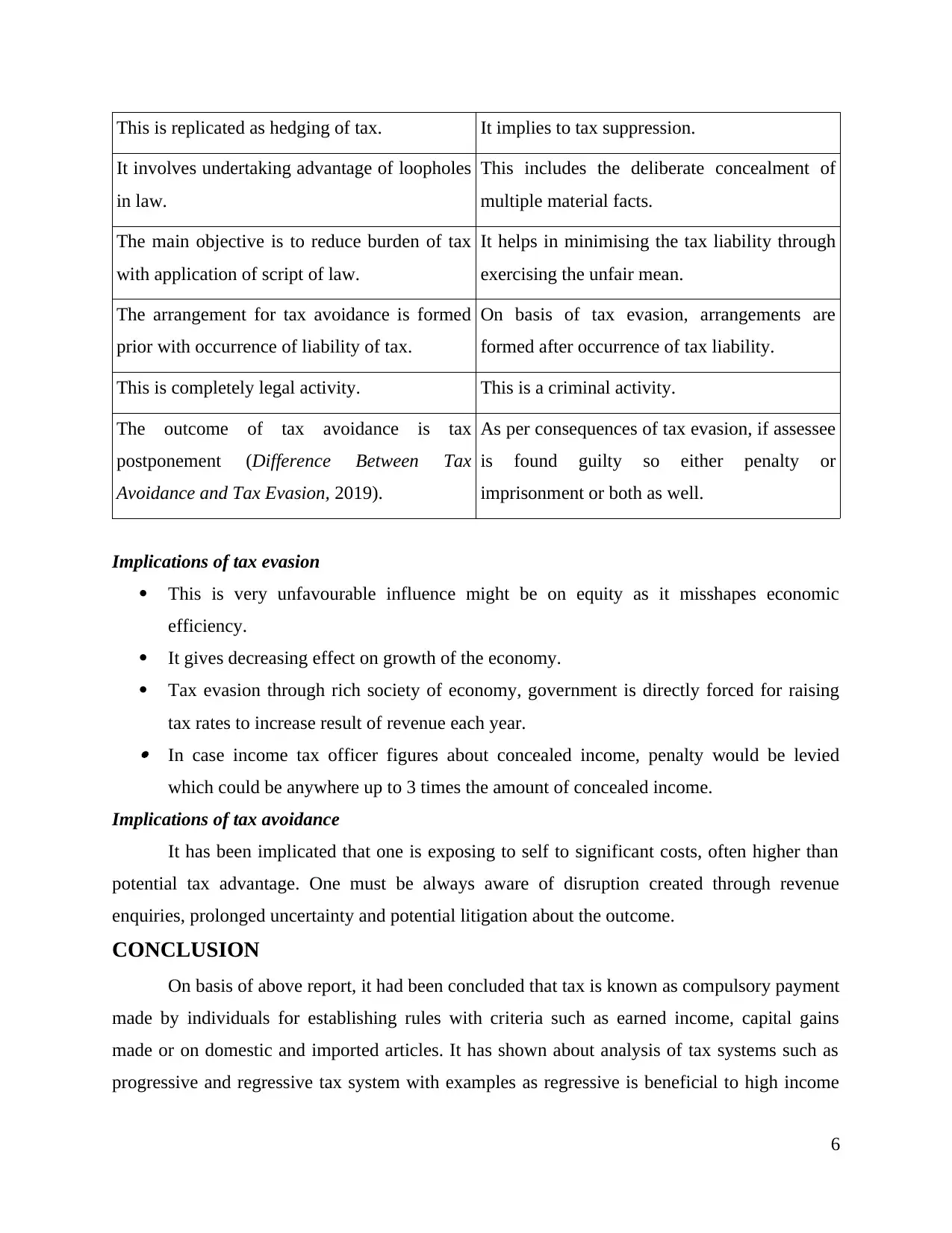

This is replicated as hedging of tax. It implies to tax suppression.

It involves undertaking advantage of loopholes

in law.

This includes the deliberate concealment of

multiple material facts.

The main objective is to reduce burden of tax

with application of script of law.

It helps in minimising the tax liability through

exercising the unfair mean.

The arrangement for tax avoidance is formed

prior with occurrence of liability of tax.

On basis of tax evasion, arrangements are

formed after occurrence of tax liability.

This is completely legal activity. This is a criminal activity.

The outcome of tax avoidance is tax

postponement (Difference Between Tax

Avoidance and Tax Evasion, 2019).

As per consequences of tax evasion, if assessee

is found guilty so either penalty or

imprisonment or both as well.

Implications of tax evasion

This is very unfavourable influence might be on equity as it misshapes economic

efficiency.

It gives decreasing effect on growth of the economy.

Tax evasion through rich society of economy, government is directly forced for raising

tax rates to increase result of revenue each year. In case income tax officer figures about concealed income, penalty would be levied

which could be anywhere up to 3 times the amount of concealed income.

Implications of tax avoidance

It has been implicated that one is exposing to self to significant costs, often higher than

potential tax advantage. One must be always aware of disruption created through revenue

enquiries, prolonged uncertainty and potential litigation about the outcome.

CONCLUSION

On basis of above report, it had been concluded that tax is known as compulsory payment

made by individuals for establishing rules with criteria such as earned income, capital gains

made or on domestic and imported articles. It has shown about analysis of tax systems such as

progressive and regressive tax system with examples as regressive is beneficial to high income

6

It involves undertaking advantage of loopholes

in law.

This includes the deliberate concealment of

multiple material facts.

The main objective is to reduce burden of tax

with application of script of law.

It helps in minimising the tax liability through

exercising the unfair mean.

The arrangement for tax avoidance is formed

prior with occurrence of liability of tax.

On basis of tax evasion, arrangements are

formed after occurrence of tax liability.

This is completely legal activity. This is a criminal activity.

The outcome of tax avoidance is tax

postponement (Difference Between Tax

Avoidance and Tax Evasion, 2019).

As per consequences of tax evasion, if assessee

is found guilty so either penalty or

imprisonment or both as well.

Implications of tax evasion

This is very unfavourable influence might be on equity as it misshapes economic

efficiency.

It gives decreasing effect on growth of the economy.

Tax evasion through rich society of economy, government is directly forced for raising

tax rates to increase result of revenue each year. In case income tax officer figures about concealed income, penalty would be levied

which could be anywhere up to 3 times the amount of concealed income.

Implications of tax avoidance

It has been implicated that one is exposing to self to significant costs, often higher than

potential tax advantage. One must be always aware of disruption created through revenue

enquiries, prolonged uncertainty and potential litigation about the outcome.

CONCLUSION

On basis of above report, it had been concluded that tax is known as compulsory payment

made by individuals for establishing rules with criteria such as earned income, capital gains

made or on domestic and imported articles. It has shown about analysis of tax systems such as

progressive and regressive tax system with examples as regressive is beneficial to high income

6

groups and progressive gives advantages to low income group. Moreover, it has articulated

about sources of tax laws of UK which are statue law, case law and HRMC guidance. Thus, it

has shown about tax avoidance and tax evasion where avoidance is legal but evasion is illegal

activity.

7

about sources of tax laws of UK which are statue law, case law and HRMC guidance. Thus, it

has shown about tax avoidance and tax evasion where avoidance is legal but evasion is illegal

activity.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Armour, J. and et.al., 2018. Putting technology to good use for society: the role of corporate,

competition and tax law. European Corporate Governance Institute (ECGI)-Law Working

Paper. (427).

Bird, R. and Davis-Nozemack, K., 2018. Tax avoidance as a sustainability problem. Journal of

Business Ethics. 151(4). pp.1009-1025.

Hearson, M., 2018. Transnational expertise and the expansion of the international tax regime:

imposing ‘acceptable’standards. Review of International Political Economy. 25(5). pp.647-

671.

Online

A complete guide to the UK tax system. 2019. [Online]. Available through

<https://www.expatica.com/uk/finance/taxes/a-complete-guide-to-the-uk-tax-system-

758254/>.

Difference Between Progressive and Regressive Tax. 2019. [Online]. Available through

<https://keydifferences.com/difference-between-progressive-and-regressive-tax.html>.

Difference Between Tax Avoidance and Tax Evasion. 2019. [Online]. Available through

<https://keydifferences.com/difference-between-tax-avoidance-and-tax-evasion.html>.

Introduction to the UK tax system. 2018. [Online]. Available through

<http://catalogue.pearsoned.co.uk/assets/hip/gb/hip_gb_pearsonhighered/samplechapter/

Melville16.pdf>.

Progressive tax. 2019. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/progressive-tax-

system/>.

Regressive tax. 2019. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/regressive-tax-

system/>.

8

Books and Journals

Armour, J. and et.al., 2018. Putting technology to good use for society: the role of corporate,

competition and tax law. European Corporate Governance Institute (ECGI)-Law Working

Paper. (427).

Bird, R. and Davis-Nozemack, K., 2018. Tax avoidance as a sustainability problem. Journal of

Business Ethics. 151(4). pp.1009-1025.

Hearson, M., 2018. Transnational expertise and the expansion of the international tax regime:

imposing ‘acceptable’standards. Review of International Political Economy. 25(5). pp.647-

671.

Online

A complete guide to the UK tax system. 2019. [Online]. Available through

<https://www.expatica.com/uk/finance/taxes/a-complete-guide-to-the-uk-tax-system-

758254/>.

Difference Between Progressive and Regressive Tax. 2019. [Online]. Available through

<https://keydifferences.com/difference-between-progressive-and-regressive-tax.html>.

Difference Between Tax Avoidance and Tax Evasion. 2019. [Online]. Available through

<https://keydifferences.com/difference-between-tax-avoidance-and-tax-evasion.html>.

Introduction to the UK tax system. 2018. [Online]. Available through

<http://catalogue.pearsoned.co.uk/assets/hip/gb/hip_gb_pearsonhighered/samplechapter/

Melville16.pdf>.

Progressive tax. 2019. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/progressive-tax-

system/>.

Regressive tax. 2019. [Online]. Available through

<https://corporatefinanceinstitute.com/resources/knowledge/accounting/regressive-tax-

system/>.

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.