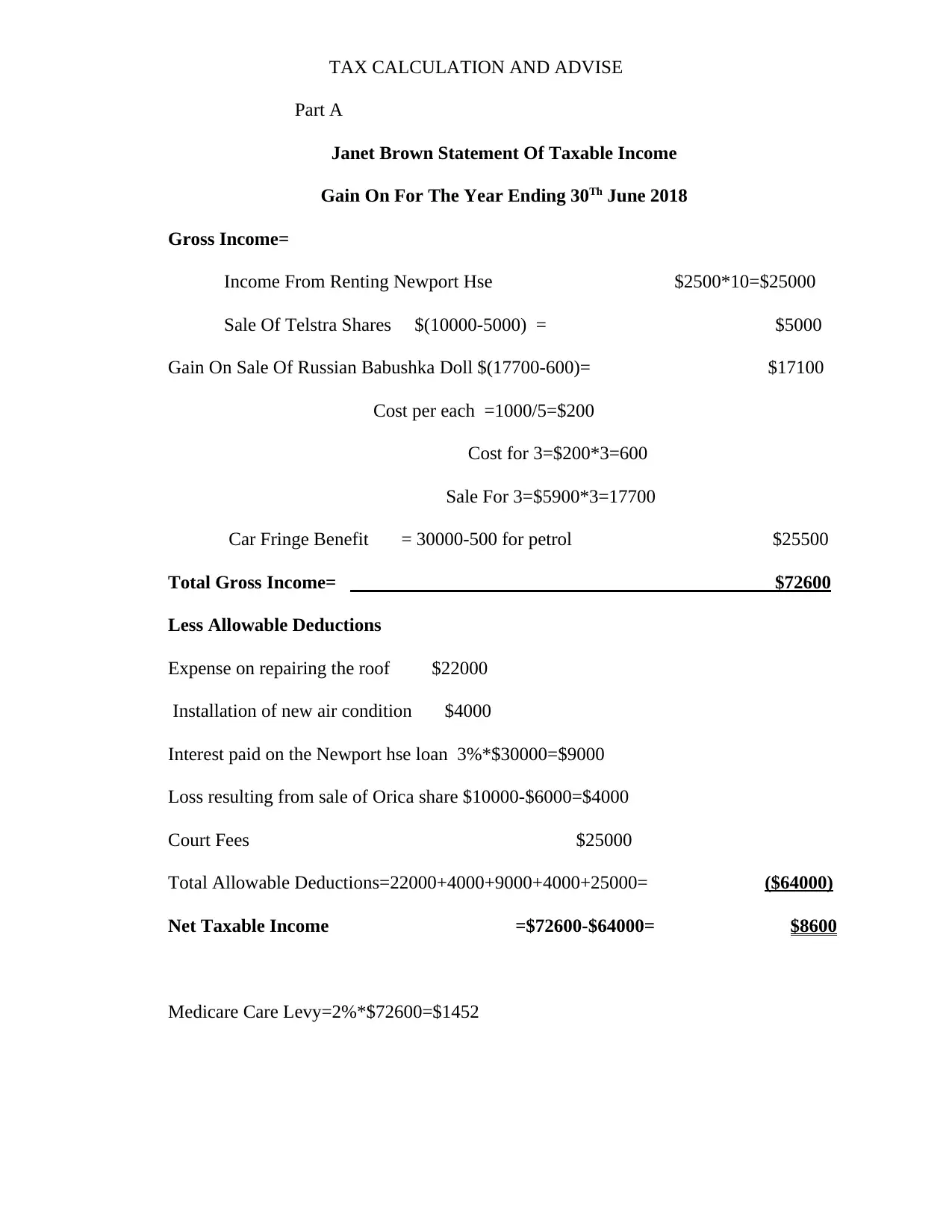

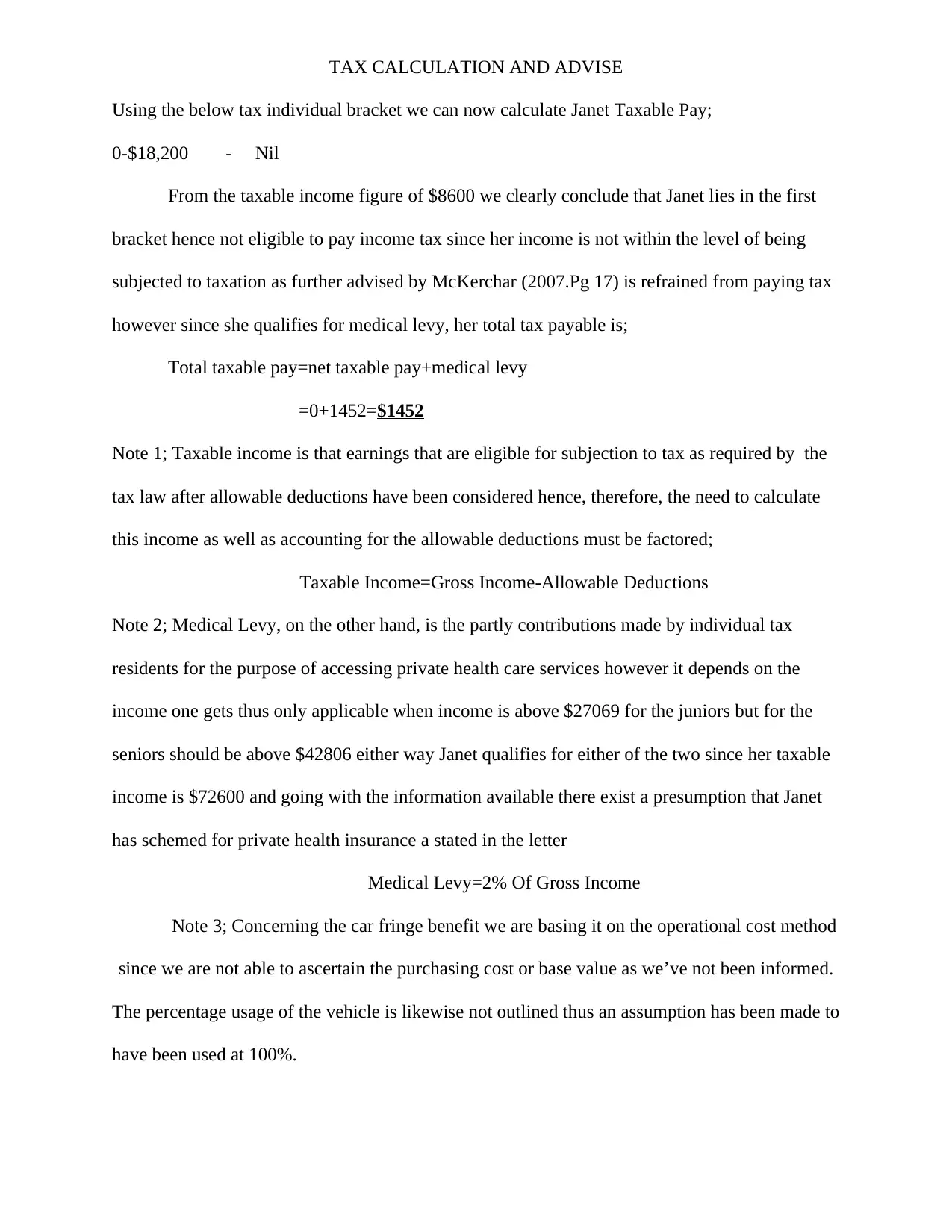

Taxable Income and Allowable Deductions for Janet Brown's Assessment

VerifiedAdded on 2020/04/01

|5

|608

|79

Homework Assignment

AI Summary

This assignment provides a detailed calculation of Janet Brown's taxable income for the year ending June 30, 2018. It includes the determination of gross income from various sources such as rental income, sale of shares, and fringe benefits. The solution meticulously calculates allowable deductions including expenses for roof repairs, air conditioning installation, interest on a loan, and court fees. It then calculates the net taxable income and determines the applicable Medicare levy. The assignment offers explanations for each calculation, including the application of tax brackets and the basis for the car fringe benefit calculation. The solution references Australian tax law and relevant publications to support its analysis, providing a comprehensive understanding of Janet Brown's tax liability.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.