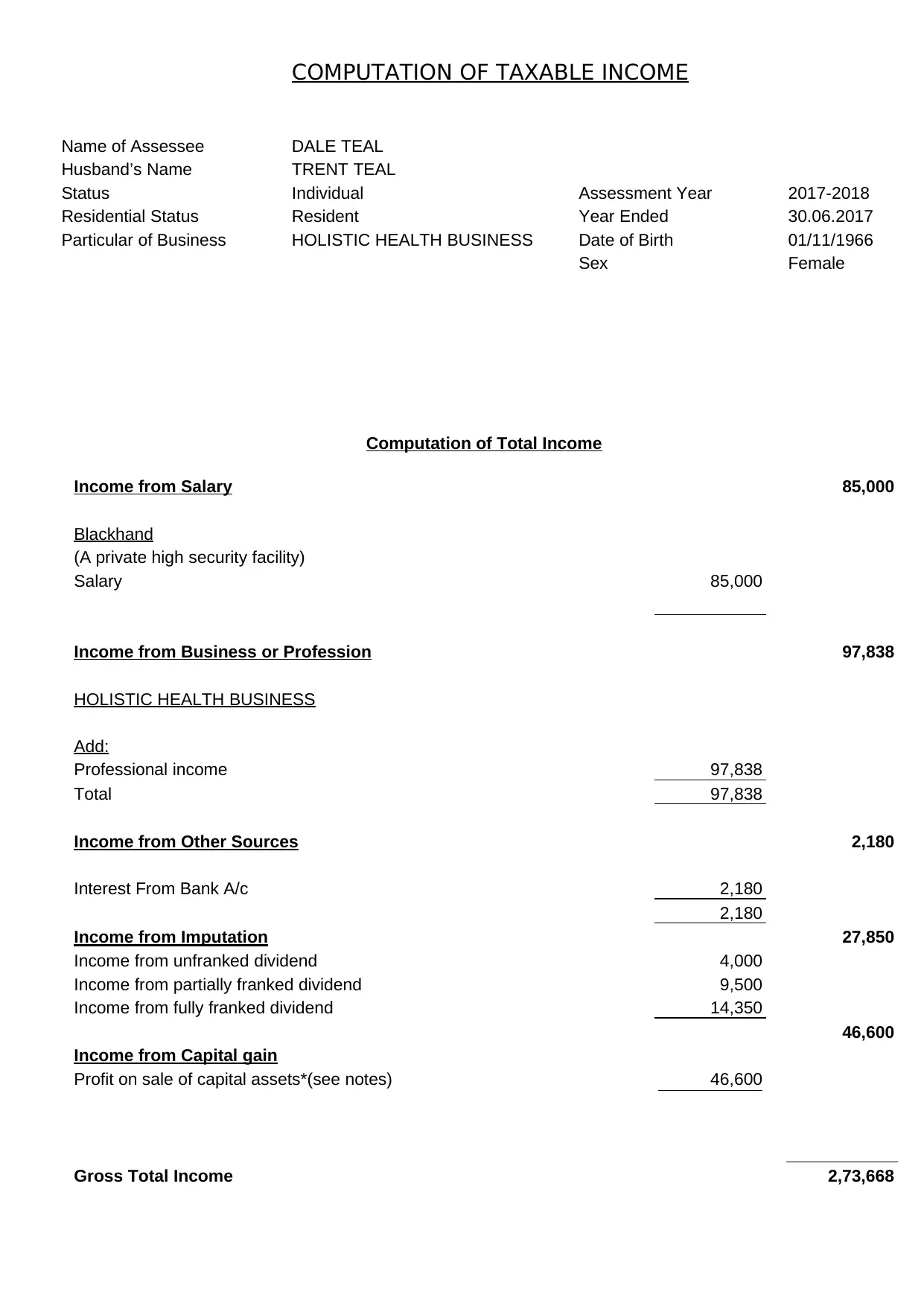

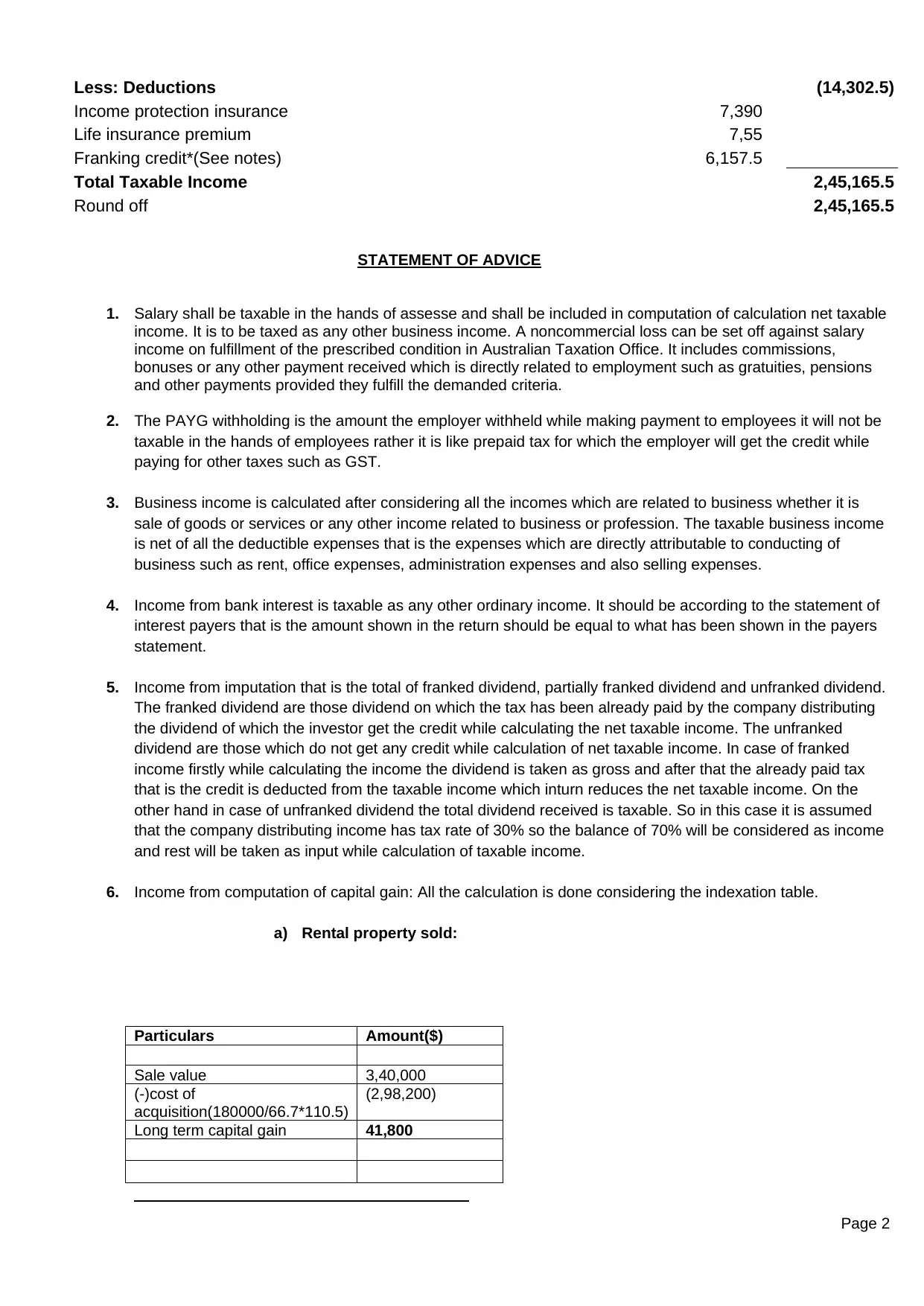

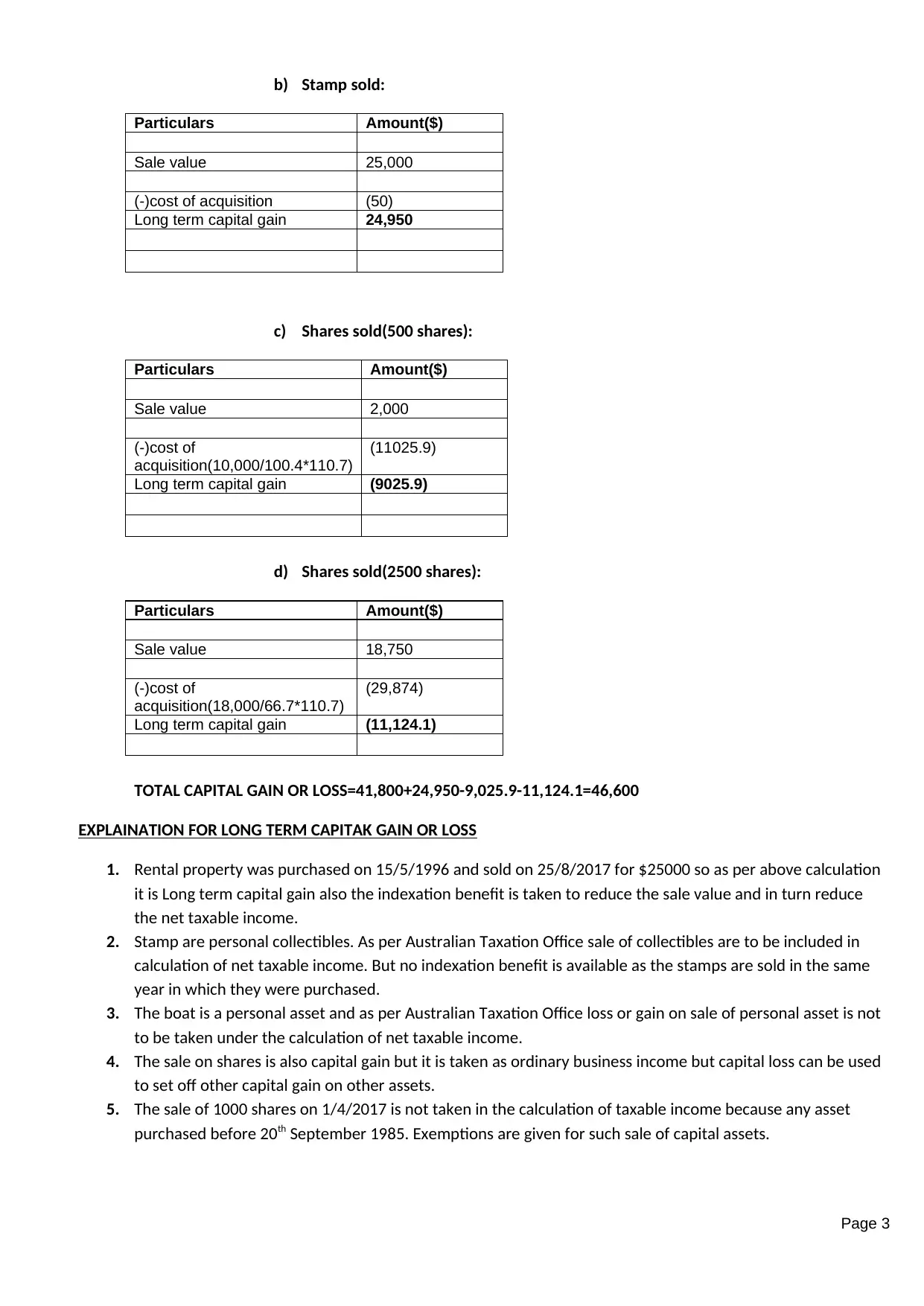

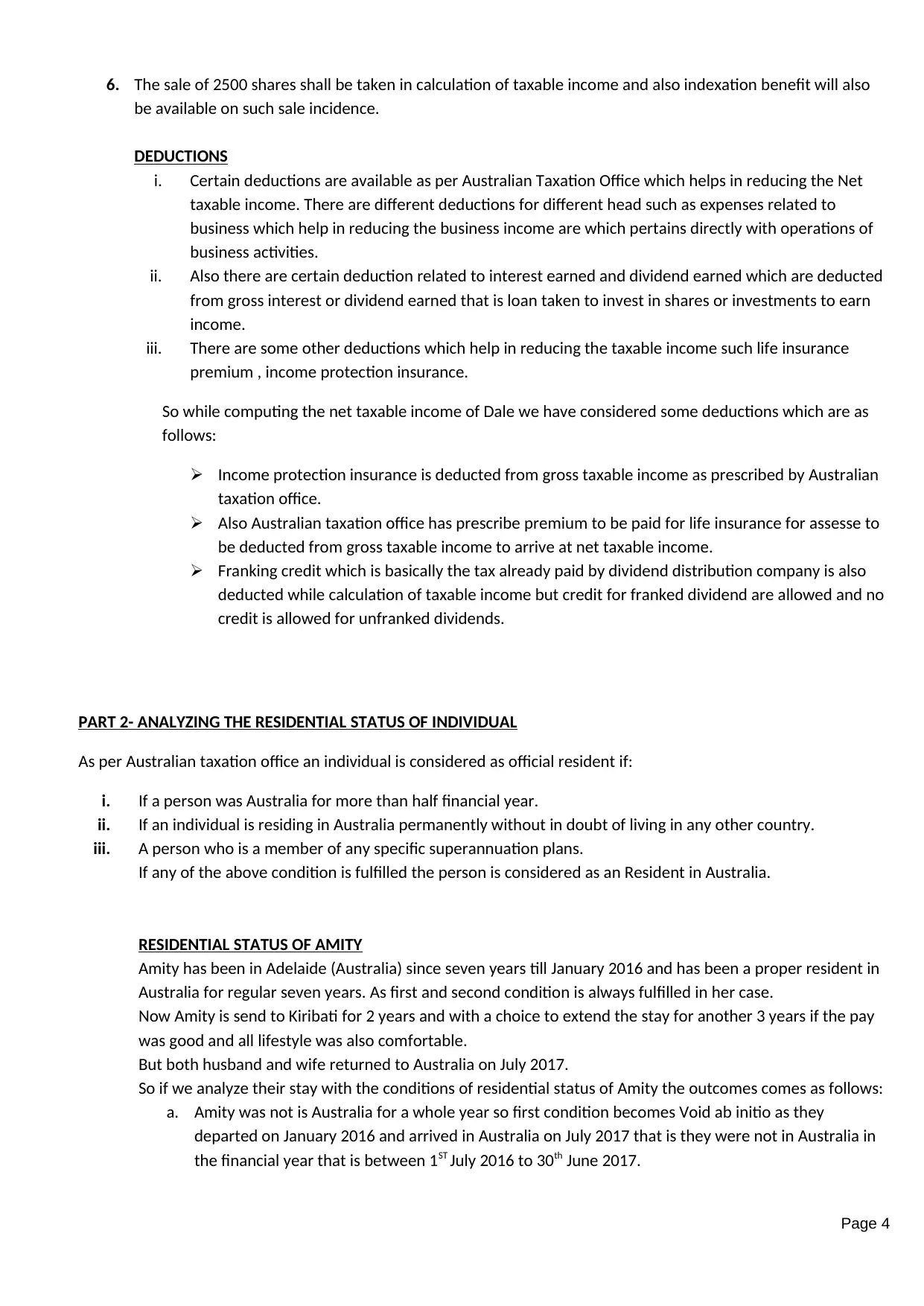

Taxable Income Computation and Analysis: Holistic Health Business

VerifiedAdded on 2023/06/13

|5

|1685

|159

Homework Assignment

AI Summary

This assignment solution details the computation of taxable income for Dale Teal's holistic health business for the assessment year 2017-2018. It covers various income sources, including salary, business income, interest, dividends (franked and unfranked), and capital gains. The solution provides a breakdown of income from salary as a prison guard and the income from her sole trader holistic health business, accounting for cash receipts, invoices, and trading stock. It also addresses the tax implications of different types of dividends, detailing how franking credits impact taxable income. Furthermore, the document outlines the calculation of capital gains from the sale of rental property, stamps, and shares, considering indexation benefits where applicable. Deductions such as income protection insurance, life insurance premiums, and franking credits are also factored into the computation to arrive at the final taxable income. In addition, the assignment analyzes the residential status of an individual named Amity, applying Australian Taxation Office guidelines to determine residency based on physical presence, domicile, and superannuation membership.

1 out of 5

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.