Taxation Case Study: Analyzing CGT, FBT, and Income for Amber

VerifiedAdded on 2023/06/04

|12

|4037

|500

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of various taxation issues. It begins by examining Amber's transactions, including the sale of a chocolate shop (addressing capital gains tax implications on goodwill, equipment, and trading stock), the proceeds from a restrictive covenant, and the sale of an inherited apartment (focusing on main residence exemption). The analysis applies relevant legislation, tax rulings, and case law to determine the tax treatment of each transaction. The assignment further investigates the tax implications for both an employee (Jamie) and employer (Houses R Us) concerning benefits such as salary, commission, a company car for personal use, and a subsidized loan. It assesses whether amounts are assessable income, if tax deductions are applicable, and the fringe benefit tax liabilities. The analysis references specific sections of the ITAA 1997 and FBTAA 1986 to support its conclusions. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

TAXATION

Student ID

[Pick the date]

Student ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

The key issue in the given scenario is to ascertain the appropriate tax treatment of following

three transactions with regards to taxpayer Amber.

1) Sale of boutique chocolate shop with special reference to the potential CGT (Capital Gains

Tax) implications.

2) Proceeds from restrictive covenant imposed during sale of business - Capital proceeds or

revenue proceeds?

3) The sale of inner city one bedroom apartment with particular reference to inheritance of

capital asset and the computation of potential CGT implications that may arise.

Law and Application

In the given section, the transactions enacted by Amber would be analysed in light of relevant

legislation, tax rulings and case law to determine the applicable taxes.

Sale of boutique chocolate shop- Law

The definition of capital assets is highlighted in s. 108-5 ITAA 1997 which includes amongst

other assets goodwill along with plant & machinery that may be used in business. However,

the same cannot be said about trading stock which as per s. 70-10 ITAA 1997 s used in the

business and would be essentially converted into final goods which would be sold to

consumers (Coleman, 2015). As a result, s. 118-25 ITAA 1997 states that any capital gains or

loss that tends to arise on account of a CGT event would be disregarded if the underlying

asset is trading stock. This is because trading stock is part of the business and hence any

profit or loss arising from the same would be reflected as assessable income in accordance

with s. 6-5 ITAA 1997.

With regards to s. 104-5, whenever there is a disposal of a capital asset, then it corresponds to

event A1. In such cases, the capital gains or losses would be derived by subtracting the cost

base of the underlying asset from the sales proceeds of the asset (Reuters, 2017).

Additionally, for the computation of capital gains that would be subject to 30% CGT, there

are namely two methods i.e. Discount Method and Indexation Method. The taxpayer has the

choice to use either of the two methods so that the CGT liability can be minimised. The

Issue

The key issue in the given scenario is to ascertain the appropriate tax treatment of following

three transactions with regards to taxpayer Amber.

1) Sale of boutique chocolate shop with special reference to the potential CGT (Capital Gains

Tax) implications.

2) Proceeds from restrictive covenant imposed during sale of business - Capital proceeds or

revenue proceeds?

3) The sale of inner city one bedroom apartment with particular reference to inheritance of

capital asset and the computation of potential CGT implications that may arise.

Law and Application

In the given section, the transactions enacted by Amber would be analysed in light of relevant

legislation, tax rulings and case law to determine the applicable taxes.

Sale of boutique chocolate shop- Law

The definition of capital assets is highlighted in s. 108-5 ITAA 1997 which includes amongst

other assets goodwill along with plant & machinery that may be used in business. However,

the same cannot be said about trading stock which as per s. 70-10 ITAA 1997 s used in the

business and would be essentially converted into final goods which would be sold to

consumers (Coleman, 2015). As a result, s. 118-25 ITAA 1997 states that any capital gains or

loss that tends to arise on account of a CGT event would be disregarded if the underlying

asset is trading stock. This is because trading stock is part of the business and hence any

profit or loss arising from the same would be reflected as assessable income in accordance

with s. 6-5 ITAA 1997.

With regards to s. 104-5, whenever there is a disposal of a capital asset, then it corresponds to

event A1. In such cases, the capital gains or losses would be derived by subtracting the cost

base of the underlying asset from the sales proceeds of the asset (Reuters, 2017).

Additionally, for the computation of capital gains that would be subject to 30% CGT, there

are namely two methods i.e. Discount Method and Indexation Method. The taxpayer has the

choice to use either of the two methods so that the CGT liability can be minimised. The

discount method as outlined in s. 115-25 ITAA 1997 provides 50% discount on the capital

gains provided the asset has been held in excess of one year. No discount under s. 115-25 can

be availed for assets which are held for less than a year (Deutsch, Freizer, Fullerton, Hanley

& Snape, 2015). In case of indexation method, revised cost base is used for the computation

of capital gains.

Sale of boutique chocolate shop- Application

The first critical aspect is that the proceeds that Amber receives with regards to the business

assets would be capital proceeds and hence no tax would be applicable on these proceeds.

However, for capital gains made on the various assets related to the shop, CGT may be

applicable in accordance with the discussion carried out above. With regards to shop, there

are different assets which need to be segregated particularly with regards to presence of

trading stock (Reuters, 2017).

With regards to goodwill, the proceeds from sale are known and also the cost is given with

regards to the shop. As a result, the capital gains can be derived in accordance with s. 104-5

and event A 1 (Deutsch, Freizer, Fullerton, Hanley & Snape, 2015). Further, the discount

method would be applied in order to compute the taxable capital gains since the shop was

purchased in 2010 and sold in 2018 thus making the resulting capital gains as long term.

In relation to the equipment, the capital gains or capital loss would be derived by considering

the sale value of equipment and the book value of equipment at the time of sale. This is

imperative since depreciation is charged on the equipment and hence the original cost cannot

be considered for capital gains computation. Also, discount method would be applied in this

case since capital gains are long term.

In relation to the trading stock with the shop, capital gains would be disregarded in line with

s.118-25 ITAA 1997 and thus these no capital gains would be levied on the same.

Restrictive Covenant- Law

The key issue with regards to restrictive covenant is to determine whether the underlying

proceeds would be capital or revenue in nature. This is imperative so that it can be

ascertained whether the receipts are revenue or capital. This is essential as revenue receipts

would be taxable but the same is not true with regards to capital receipts. A relevant case law

is Reuter v. FC of T 93 ATC 4037; (1993) 24 ATR 527 where there was an agreement

gains provided the asset has been held in excess of one year. No discount under s. 115-25 can

be availed for assets which are held for less than a year (Deutsch, Freizer, Fullerton, Hanley

& Snape, 2015). In case of indexation method, revised cost base is used for the computation

of capital gains.

Sale of boutique chocolate shop- Application

The first critical aspect is that the proceeds that Amber receives with regards to the business

assets would be capital proceeds and hence no tax would be applicable on these proceeds.

However, for capital gains made on the various assets related to the shop, CGT may be

applicable in accordance with the discussion carried out above. With regards to shop, there

are different assets which need to be segregated particularly with regards to presence of

trading stock (Reuters, 2017).

With regards to goodwill, the proceeds from sale are known and also the cost is given with

regards to the shop. As a result, the capital gains can be derived in accordance with s. 104-5

and event A 1 (Deutsch, Freizer, Fullerton, Hanley & Snape, 2015). Further, the discount

method would be applied in order to compute the taxable capital gains since the shop was

purchased in 2010 and sold in 2018 thus making the resulting capital gains as long term.

In relation to the equipment, the capital gains or capital loss would be derived by considering

the sale value of equipment and the book value of equipment at the time of sale. This is

imperative since depreciation is charged on the equipment and hence the original cost cannot

be considered for capital gains computation. Also, discount method would be applied in this

case since capital gains are long term.

In relation to the trading stock with the shop, capital gains would be disregarded in line with

s.118-25 ITAA 1997 and thus these no capital gains would be levied on the same.

Restrictive Covenant- Law

The key issue with regards to restrictive covenant is to determine whether the underlying

proceeds would be capital or revenue in nature. This is imperative so that it can be

ascertained whether the receipts are revenue or capital. This is essential as revenue receipts

would be taxable but the same is not true with regards to capital receipts. A relevant case law

is Reuter v. FC of T 93 ATC 4037; (1993) 24 ATR 527 where there was an agreement

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between parties whereby right to sue was not allowed (Nethercott, Richardson & Devos,

2016). A critical aspect highlighted was that if a payment has been derived with regards to

restricting a legitimate right that the taxpayer has, then the underlying proceeds would be

capital in nature. The same logic can be extended to restrictive covenant which prohibit the

seller of a business from opening a business in certain geography and for certain time and

hence restraining the legitimate right the seller has to open a new business. Therefore, the

proceeds derived from the same would be capital in nature which has also been supported by

tax rulings TR95/35 and TR 94/D33 (ATO, 2018).

Restrictive Covenant- Application

In the given case, Amber has received an additional sum of $ 50,000 for signing a separate

contract with the buyer of the business whereby she is not allowed to open a similar business

within the radius of 20 km from the shop sold for a period extending to 5 years. It is apparent

that the restrictive covenant tends to restrict the rights available to Amber with regard to

opening shop and hence the proceeds from this contract would be capital in nature on which

no tax would be applicable. However, CGT may apply on any capital gains that may be

related to the contract.

Sale of one bedroom apartment-Law

As per s.149-10 ITAA 1997, any capital asset acquired before September 20, 1985 would be

considered as pre-CGT asset and the capital gains tax would not be applicable on any capital

gains or losses arising from the sale of such asset irrespective of holding period and the

quantum of capital gains (Nethercott, Richardson & Devos, 2016). In relation to deceased

estates, it is imperative to note that CGT implications before the death of the concerned

owner are disregarded. Also, even though the estate is inherited but the market value at the

time of death tends to serve as the cost base of the asset so that any CGT liabilities that may

arise from the sale of the asset may be computed. Also, with regards to TR 94/29, in

situations where the contract for sale is signed or executed in a given year but proceeds are

obtained in the next tax year, the CGT is payable in the same year when the sale contract is

executed and the CGT liability ought to be computed in accordance with the contract sale

terms as set in the sale contract (Kreyer, 2016). As per Division 118-B main residence

exemption is available when the taxpayer tends to use the given house as main residence. In

case of deceased estates, this benefit is extended to the taxpayer who has inherited the

property (Hodgson, Mortimer & Butler, 2016).

2016). A critical aspect highlighted was that if a payment has been derived with regards to

restricting a legitimate right that the taxpayer has, then the underlying proceeds would be

capital in nature. The same logic can be extended to restrictive covenant which prohibit the

seller of a business from opening a business in certain geography and for certain time and

hence restraining the legitimate right the seller has to open a new business. Therefore, the

proceeds derived from the same would be capital in nature which has also been supported by

tax rulings TR95/35 and TR 94/D33 (ATO, 2018).

Restrictive Covenant- Application

In the given case, Amber has received an additional sum of $ 50,000 for signing a separate

contract with the buyer of the business whereby she is not allowed to open a similar business

within the radius of 20 km from the shop sold for a period extending to 5 years. It is apparent

that the restrictive covenant tends to restrict the rights available to Amber with regard to

opening shop and hence the proceeds from this contract would be capital in nature on which

no tax would be applicable. However, CGT may apply on any capital gains that may be

related to the contract.

Sale of one bedroom apartment-Law

As per s.149-10 ITAA 1997, any capital asset acquired before September 20, 1985 would be

considered as pre-CGT asset and the capital gains tax would not be applicable on any capital

gains or losses arising from the sale of such asset irrespective of holding period and the

quantum of capital gains (Nethercott, Richardson & Devos, 2016). In relation to deceased

estates, it is imperative to note that CGT implications before the death of the concerned

owner are disregarded. Also, even though the estate is inherited but the market value at the

time of death tends to serve as the cost base of the asset so that any CGT liabilities that may

arise from the sale of the asset may be computed. Also, with regards to TR 94/29, in

situations where the contract for sale is signed or executed in a given year but proceeds are

obtained in the next tax year, the CGT is payable in the same year when the sale contract is

executed and the CGT liability ought to be computed in accordance with the contract sale

terms as set in the sale contract (Kreyer, 2016). As per Division 118-B main residence

exemption is available when the taxpayer tends to use the given house as main residence. In

case of deceased estates, this benefit is extended to the taxpayer who has inherited the

property (Hodgson, Mortimer & Butler, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sale of one bedroom apartment-Application

Based on the given case facts, it is apparent that Amber has inherited the property from his

uncle in October 2013. Since the property was purchased after 1985, hence the given asset is

not a pre-CGT asset. However, it is noteworthy that Amber’s uncle purchased the house in

1992 and had resided in the same house till his death. As a result, it may be concluded that

Amber’s uncle used the house as main residence. Further, Amber has continued the same

since from the time of inheritance, she has resided in the house thereby making it the main

residence. As a result, there would not be any capital gains tax on the sale of house in

accordance with Division 118-B which provides the main residence exemption. Besides, the

proceeds from the house sale are capital in nature and thereby non-assessable for tax

purposes.

Conclusion\

Based on the above discussion, it may be concluded that Amber would have to pay capital

gains tax on the sale of the chocolate shop but same would pertain only to the equipment and

goodwill. Any capital gains or loss on the trading stock would be disregarded. Further, the

proceeds from contract enacting the restrictive covenant would be capital in nature and hence

non-taxable . However, the capital gains if any on these would have to be computed and CGT

may be applicable. In relation to the sale of the inherited one bedroom house, it is apparent

that the main residence exemption would apply owing to which no CGT would be applicable

on the capital gains or losses derived from the sale of house. Further, the proceeds from house

sale are capital and thus non-taxable.

Question 2

Issue

The objective of the given task is to highlight the tax implications for both the employee

(Jamie) and employer (Houses R Us) with regards to the various benefits that have been

extended. The key issues would be as follows.

Determine whether a given amount is assessable income for Jamie under s. 6-5 or s.

6-10 ITAA 1997.

Based on the given case facts, it is apparent that Amber has inherited the property from his

uncle in October 2013. Since the property was purchased after 1985, hence the given asset is

not a pre-CGT asset. However, it is noteworthy that Amber’s uncle purchased the house in

1992 and had resided in the same house till his death. As a result, it may be concluded that

Amber’s uncle used the house as main residence. Further, Amber has continued the same

since from the time of inheritance, she has resided in the house thereby making it the main

residence. As a result, there would not be any capital gains tax on the sale of house in

accordance with Division 118-B which provides the main residence exemption. Besides, the

proceeds from the house sale are capital in nature and thereby non-assessable for tax

purposes.

Conclusion\

Based on the above discussion, it may be concluded that Amber would have to pay capital

gains tax on the sale of the chocolate shop but same would pertain only to the equipment and

goodwill. Any capital gains or loss on the trading stock would be disregarded. Further, the

proceeds from contract enacting the restrictive covenant would be capital in nature and hence

non-taxable . However, the capital gains if any on these would have to be computed and CGT

may be applicable. In relation to the sale of the inherited one bedroom house, it is apparent

that the main residence exemption would apply owing to which no CGT would be applicable

on the capital gains or losses derived from the sale of house. Further, the proceeds from house

sale are capital and thus non-taxable.

Question 2

Issue

The objective of the given task is to highlight the tax implications for both the employee

(Jamie) and employer (Houses R Us) with regards to the various benefits that have been

extended. The key issues would be as follows.

Determine whether a given amount is assessable income for Jamie under s. 6-5 or s.

6-10 ITAA 1997.

Determine whether Jamie can have any tax deduction with regards to the interest paid

on loan amount.

Determine whether the given amount spent by the employer would be tax deductible

under s.8-1 and other suitable provisions.

Determine the FBT (Fringe Benefit Tax) related liability on Jamie and employer with

regards to car for personal use and also loan provided at subsidised rate.

Law & Application

The discussion of the various amounts paid to the employee or spent by the employer

pertained to Jamie is carried below.

Base salary plus 10% commission

Employee – For Jamie, the above income derived on the basis of the employment contract

would be considered as employment salary for her services as a real estate agent.

Additionally, there is a 10% commission which is also linked to the given employment only.

Hence, both these payments would be considered as ordinary income under s.6(5) ITAA

1997 (Austlii, 2018e). As ordinary income is one of the components of assessable income,

hence the given amount would be subject to personal income tax on part of Jamie.

Employer – In accordance with s. 8-1 ITAA 1997, any outgoing or loss which is incurred for

production of assessable income is deductible (Barkoczy, 2017). However, ss. 8-1(2)

prohibits tax deduction for capital expense, private expenses and expenses for non-assessable

income production. The given expenditure in the form of salary and commission would be

revenue expenditure for gaining assessable income and hence tax deduction for Houses R Us

can be claimed.

Car to Employee

In accordance Division 2, Fringe Benefit Tax Assessment Act 1986, if the employer provides

a car to the employee for personal use, then it would amount to extension to car fringe

benefits. The fringe benefit tax on the same would be payable by the employer in accordance

with s. 9 FBTAA 1986. However, no fringe benefit tax or any other tax arises for the

employee (Austlii, 2018c).

Employee – It is apparent that the employer has provided a Toyota Kluger to Jamie and the

same is not only used for work purposes but also on weekends and for personal purposes.

on loan amount.

Determine whether the given amount spent by the employer would be tax deductible

under s.8-1 and other suitable provisions.

Determine the FBT (Fringe Benefit Tax) related liability on Jamie and employer with

regards to car for personal use and also loan provided at subsidised rate.

Law & Application

The discussion of the various amounts paid to the employee or spent by the employer

pertained to Jamie is carried below.

Base salary plus 10% commission

Employee – For Jamie, the above income derived on the basis of the employment contract

would be considered as employment salary for her services as a real estate agent.

Additionally, there is a 10% commission which is also linked to the given employment only.

Hence, both these payments would be considered as ordinary income under s.6(5) ITAA

1997 (Austlii, 2018e). As ordinary income is one of the components of assessable income,

hence the given amount would be subject to personal income tax on part of Jamie.

Employer – In accordance with s. 8-1 ITAA 1997, any outgoing or loss which is incurred for

production of assessable income is deductible (Barkoczy, 2017). However, ss. 8-1(2)

prohibits tax deduction for capital expense, private expenses and expenses for non-assessable

income production. The given expenditure in the form of salary and commission would be

revenue expenditure for gaining assessable income and hence tax deduction for Houses R Us

can be claimed.

Car to Employee

In accordance Division 2, Fringe Benefit Tax Assessment Act 1986, if the employer provides

a car to the employee for personal use, then it would amount to extension to car fringe

benefits. The fringe benefit tax on the same would be payable by the employer in accordance

with s. 9 FBTAA 1986. However, no fringe benefit tax or any other tax arises for the

employee (Austlii, 2018c).

Employee – It is apparent that the employer has provided a Toyota Kluger to Jamie and the

same is not only used for work purposes but also on weekends and for personal purposes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Also, the operating expenses are paid by the employer only and hence no deduction in this

regards would be provided for the employee. Besides, no tax burden on account of car fringe

benefit is levied on to the employee Jamie.

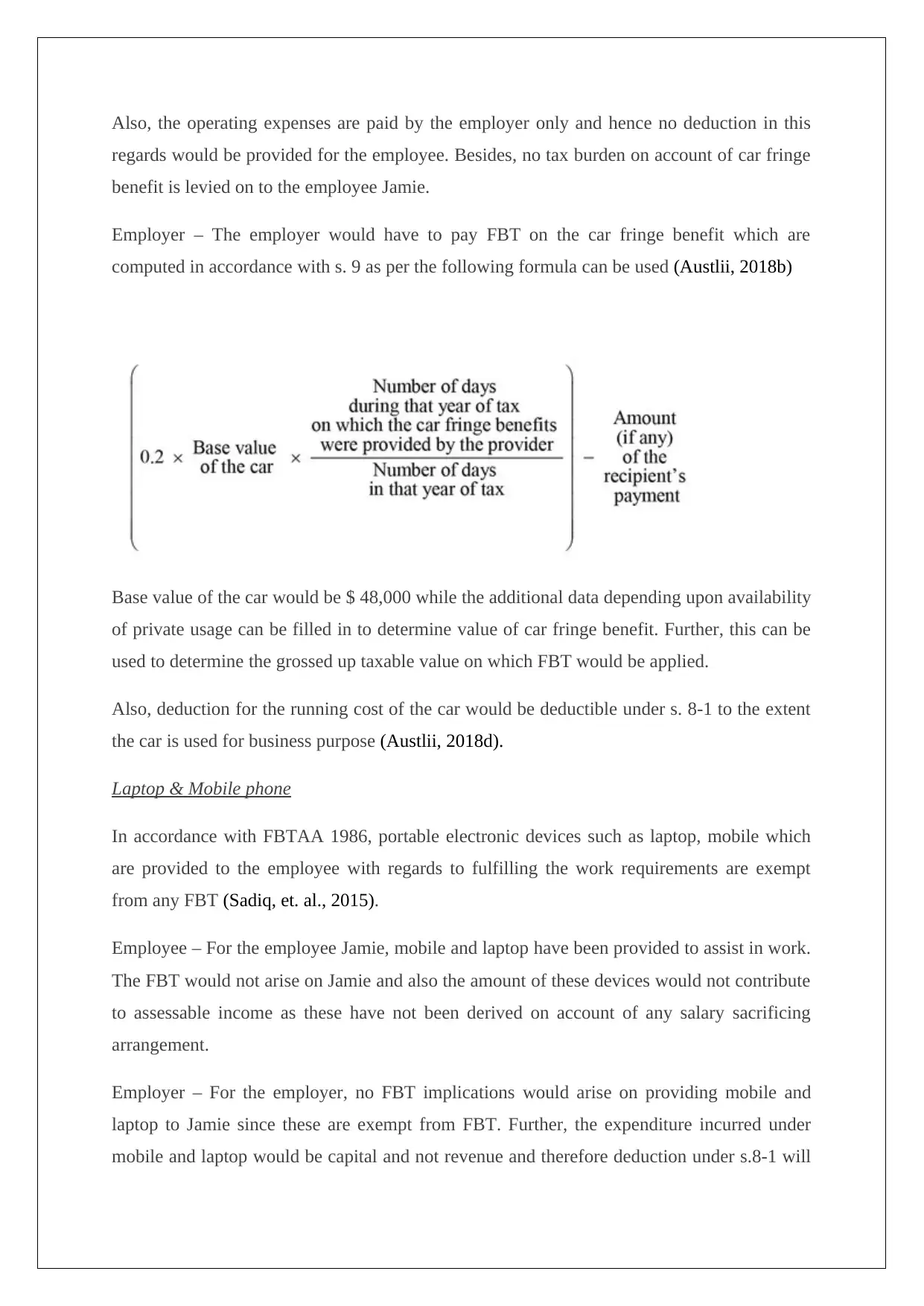

Employer – The employer would have to pay FBT on the car fringe benefit which are

computed in accordance with s. 9 as per the following formula can be used (Austlii, 2018b)

Base value of the car would be $ 48,000 while the additional data depending upon availability

of private usage can be filled in to determine value of car fringe benefit. Further, this can be

used to determine the grossed up taxable value on which FBT would be applied.

Also, deduction for the running cost of the car would be deductible under s. 8-1 to the extent

the car is used for business purpose (Austlii, 2018d).

Laptop & Mobile phone

In accordance with FBTAA 1986, portable electronic devices such as laptop, mobile which

are provided to the employee with regards to fulfilling the work requirements are exempt

from any FBT (Sadiq, et. al., 2015).

Employee – For the employee Jamie, mobile and laptop have been provided to assist in work.

The FBT would not arise on Jamie and also the amount of these devices would not contribute

to assessable income as these have not been derived on account of any salary sacrificing

arrangement.

Employer – For the employer, no FBT implications would arise on providing mobile and

laptop to Jamie since these are exempt from FBT. Further, the expenditure incurred under

mobile and laptop would be capital and not revenue and therefore deduction under s.8-1 will

regards would be provided for the employee. Besides, no tax burden on account of car fringe

benefit is levied on to the employee Jamie.

Employer – The employer would have to pay FBT on the car fringe benefit which are

computed in accordance with s. 9 as per the following formula can be used (Austlii, 2018b)

Base value of the car would be $ 48,000 while the additional data depending upon availability

of private usage can be filled in to determine value of car fringe benefit. Further, this can be

used to determine the grossed up taxable value on which FBT would be applied.

Also, deduction for the running cost of the car would be deductible under s. 8-1 to the extent

the car is used for business purpose (Austlii, 2018d).

Laptop & Mobile phone

In accordance with FBTAA 1986, portable electronic devices such as laptop, mobile which

are provided to the employee with regards to fulfilling the work requirements are exempt

from any FBT (Sadiq, et. al., 2015).

Employee – For the employee Jamie, mobile and laptop have been provided to assist in work.

The FBT would not arise on Jamie and also the amount of these devices would not contribute

to assessable income as these have not been derived on account of any salary sacrificing

arrangement.

Employer – For the employer, no FBT implications would arise on providing mobile and

laptop to Jamie since these are exempt from FBT. Further, the expenditure incurred under

mobile and laptop would be capital and not revenue and therefore deduction under s.8-1 will

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

not be available for the employer for capital expenses pertaining to laptop and mobile.

However, decline in value for these depreciating assets may be charged by the company

during the useful life of these assets and this would be a deductible expense.

Annual Professional Subscription

Employee –As per TR 92/15, for assessable income to be produced, it is essential that the

employee must gain some economic profit (Sadiq, et. al., 2015). However, in the given

scenario Jamie has been merely obtained reimbursement for the subscription of a magazine

which is related to his profession. Since, there is no expense or benefit derived on part of

Jamie, hence no tax implications would arise for him on account of the given transaction.

Employer – With regards to the employer, there has been an expense in the form of

subscription fee. Also, it is related that this is with regards to assessable income production.

Owing to sufficient nexus between the expense and the assessable income production,

deduction for this expense would be given to employer as per s. 8-1 ITAA 1997 (Barkoczy,

2017).

Entertainment Allowance

As per TR 92/15, allowance is defined as a payment whose quantum is predefined and is

provided to meet an estimated expense irrespective of the fact whether any expense has been

made on the same or not.

Employee – The entertainment allowance to the extent of $ 2000 per year would be

assessable income for the employee considering that he will receive $ 2,000 from the

employer irrespective of whether any expense on entertainment has been incurred or not.

Therefore, economic benefit would be derived on which income tax would be payable.

Employer – The entertainment allowance would be a business related revenue expense with

sufficient link to production of assessable income and hence tax deduction under s.8-1 is

permissible for the employer.

Home entertainment System

One of the components of assessable income is statutory income as per s. 6-10 ITAA 1997.

The various non-cash benefits that may be derived would be considered as statutory income if

the same can be linked to income production activity. This is in accordance with s. 21A

However, decline in value for these depreciating assets may be charged by the company

during the useful life of these assets and this would be a deductible expense.

Annual Professional Subscription

Employee –As per TR 92/15, for assessable income to be produced, it is essential that the

employee must gain some economic profit (Sadiq, et. al., 2015). However, in the given

scenario Jamie has been merely obtained reimbursement for the subscription of a magazine

which is related to his profession. Since, there is no expense or benefit derived on part of

Jamie, hence no tax implications would arise for him on account of the given transaction.

Employer – With regards to the employer, there has been an expense in the form of

subscription fee. Also, it is related that this is with regards to assessable income production.

Owing to sufficient nexus between the expense and the assessable income production,

deduction for this expense would be given to employer as per s. 8-1 ITAA 1997 (Barkoczy,

2017).

Entertainment Allowance

As per TR 92/15, allowance is defined as a payment whose quantum is predefined and is

provided to meet an estimated expense irrespective of the fact whether any expense has been

made on the same or not.

Employee – The entertainment allowance to the extent of $ 2000 per year would be

assessable income for the employee considering that he will receive $ 2,000 from the

employer irrespective of whether any expense on entertainment has been incurred or not.

Therefore, economic benefit would be derived on which income tax would be payable.

Employer – The entertainment allowance would be a business related revenue expense with

sufficient link to production of assessable income and hence tax deduction under s.8-1 is

permissible for the employer.

Home entertainment System

One of the components of assessable income is statutory income as per s. 6-10 ITAA 1997.

The various non-cash benefits that may be derived would be considered as statutory income if

the same can be linked to income production activity. This is in accordance with s. 21A

ITAA 1997 highlights that even though the non –cash benefit may not be convertible to cash

but it would be assumed to be cash convertible and contribute to assessable income (Austlii,

2018a).

Employee – It is apparent that the home entertainment system has been presented to Jamie

owing to the ensuring that he had the highest sales of all employees during the six month

period. Clearly, this is linked to his job and hence the value of the home entertainment system

would be assumed as statutory income and therefore would contribute to assessable income

of the employee Jamie.

Employer – The underlying expense of the home entertainment system would be an expense

related to employee benefits which are imperative in order to produce assessable income and

hence general tax deduction under s. 8-1 is permissible for the employer.

Loan to the staff to the extent of $ 100,000

One of the key benefits that employers provide to their employee is in the form of personal

loans which are either provided at zero interest or at substantially low interest rate. This may

pave the way for extension of loan fringe benefits (Austlii, 2018c). As per division 4, Part III

FBTAA 1986, if the employer provides loan to employees at a rate which is lower than the

corresponding rate that is prescribed by the RBA (Reserve Bank of Australia), then loan

fringe benefit has been extended to the taxpayer. For the year 2017/2018, the benchmark

interest rate decided by RBA is 5.25% p.a. as highlighted in TD 2017/3. As a result,

extension of loan below this rate would result in interest savings for the employee which

essentially highlights the quantum of loan fringe benefit on which then the FBT liability for

the employer would be computed.

Employee – Jamie has obtained loan amount to the extent of $ 100,000 from the employer to

build his first home. The interest rate levied on the loan amount is 4% p.a. which clearly

implies that loan fringe benefits have been extended to Jamie. However, in this regards no tax

implications would arise for Jamie. But, Jamie is paying interest on the home loan taken from

the employer and hence it needs to be ascertained if tax deduction can be availed by Jamie in

regards to the interest paid. Considering that the house being constructed is first time home,

hence it is likely that the same would be used for residence purpose and not for renting. As a

result, if the house does not produce any assessable income through rent, then interest

payments made by Jamie cannot be deducted under s. 8-1 ITAA 1997 (Austlii, 2018 d).

but it would be assumed to be cash convertible and contribute to assessable income (Austlii,

2018a).

Employee – It is apparent that the home entertainment system has been presented to Jamie

owing to the ensuring that he had the highest sales of all employees during the six month

period. Clearly, this is linked to his job and hence the value of the home entertainment system

would be assumed as statutory income and therefore would contribute to assessable income

of the employee Jamie.

Employer – The underlying expense of the home entertainment system would be an expense

related to employee benefits which are imperative in order to produce assessable income and

hence general tax deduction under s. 8-1 is permissible for the employer.

Loan to the staff to the extent of $ 100,000

One of the key benefits that employers provide to their employee is in the form of personal

loans which are either provided at zero interest or at substantially low interest rate. This may

pave the way for extension of loan fringe benefits (Austlii, 2018c). As per division 4, Part III

FBTAA 1986, if the employer provides loan to employees at a rate which is lower than the

corresponding rate that is prescribed by the RBA (Reserve Bank of Australia), then loan

fringe benefit has been extended to the taxpayer. For the year 2017/2018, the benchmark

interest rate decided by RBA is 5.25% p.a. as highlighted in TD 2017/3. As a result,

extension of loan below this rate would result in interest savings for the employee which

essentially highlights the quantum of loan fringe benefit on which then the FBT liability for

the employer would be computed.

Employee – Jamie has obtained loan amount to the extent of $ 100,000 from the employer to

build his first home. The interest rate levied on the loan amount is 4% p.a. which clearly

implies that loan fringe benefits have been extended to Jamie. However, in this regards no tax

implications would arise for Jamie. But, Jamie is paying interest on the home loan taken from

the employer and hence it needs to be ascertained if tax deduction can be availed by Jamie in

regards to the interest paid. Considering that the house being constructed is first time home,

hence it is likely that the same would be used for residence purpose and not for renting. As a

result, if the house does not produce any assessable income through rent, then interest

payments made by Jamie cannot be deducted under s. 8-1 ITAA 1997 (Austlii, 2018 d).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employer – With regards to the employer, it is apparent that the interest rate charged to the

employee is lesser than 5.25% p.a. which provides evidence of extension of loan fringe

benefits. The amount of these benefits would be equal to the interest savings that employee

would receive during the year. This would then be multiplied with the suitable gross up factor

for ascertaining the taxable value of loan fringe benefits on which FBT rate would be levied

to determine the FBT liability for the employer. Also, deduction of the interest would not be

available for the employer since Jamie is not using the same for production of taxable

income.

Conclusion

Based on the above discussion, the following conclusion may be drawn.

Base salary and 10% commission is assessable income under s. 6-5 for Jamie.

Deduction under s. 8-1 can be availed by taxpayer on the complete amount.

Car provided by employer for personal use would result in FBT on employer with

deductions under s. 8-1 for operating expenses for business use only. No tax

implication for employee.

The mobile phone derive and laptop are FBT exempt devices and hence no tax

implication for employee. The employer can claim decline in value of these assets as

tax deductions.

Annual subscription reimbursement would be tax deductible expense under s.8-1 for

employer with no tax implication for employee.

Entertainment allowance leads to assessable income for taxpayer Jamie with

corresponding s. 8-1 deduction for the employer.

Home entertainment system cost would be assessable income for employee since it is

a type of statutory income and tax deductible for employer under aegis of s. 8-1 ITAA

1997.

Loan fringe benefits have been extended to employee and hence FBT would be

charged on employer. No tax implication for Jamie, the employee. The interest paid

on the loan to employee cannot be deducted for tax purposes by Jamie considering

that the house is expected to be used for his own residential purpose rather than

income generation.

employee is lesser than 5.25% p.a. which provides evidence of extension of loan fringe

benefits. The amount of these benefits would be equal to the interest savings that employee

would receive during the year. This would then be multiplied with the suitable gross up factor

for ascertaining the taxable value of loan fringe benefits on which FBT rate would be levied

to determine the FBT liability for the employer. Also, deduction of the interest would not be

available for the employer since Jamie is not using the same for production of taxable

income.

Conclusion

Based on the above discussion, the following conclusion may be drawn.

Base salary and 10% commission is assessable income under s. 6-5 for Jamie.

Deduction under s. 8-1 can be availed by taxpayer on the complete amount.

Car provided by employer for personal use would result in FBT on employer with

deductions under s. 8-1 for operating expenses for business use only. No tax

implication for employee.

The mobile phone derive and laptop are FBT exempt devices and hence no tax

implication for employee. The employer can claim decline in value of these assets as

tax deductions.

Annual subscription reimbursement would be tax deductible expense under s.8-1 for

employer with no tax implication for employee.

Entertainment allowance leads to assessable income for taxpayer Jamie with

corresponding s. 8-1 deduction for the employer.

Home entertainment system cost would be assessable income for employee since it is

a type of statutory income and tax deductible for employer under aegis of s. 8-1 ITAA

1997.

Loan fringe benefits have been extended to employee and hence FBT would be

charged on employer. No tax implication for Jamie, the employee. The interest paid

on the loan to employee cannot be deducted for tax purposes by Jamie considering

that the house is expected to be used for his own residential purpose rather than

income generation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

ATO, (2018) TR 95/35.Income Tax : Capital gains: treatment of compensation

receipts. Retrieved from http://law.ato.gov.au/atolaw/view.htm?locid=txr/tr9535/nat/ato

Austlii, (2018 a) Income Tax Assessment Act 1936- SECT 21 A. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s21a.html

Austlii, (2018 b) Fringe Benefits Tax Assessment Act 1986- SECT 9 Taxable Value of

Car Fringe Benefits – Statutory Formula. Retrieved from http://www7.austlii.edu.au/cgi-

bin/viewdoc/au/legis/cth/consol_act/fbtaa1986312/s9.html

Austlii, (2018 d) Income Tax Assessment Act 1997-SEC 8.1. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s8.1.html

Austlii, (2018 e) Income Tax Assessment Act 1997-SEC 6.10. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.10.html

Austlii, (2018c) Fringe Benefits Tax Assessment Act 1986. Retrieved from

http://classic.austlii.edu.au/au/legis/cth/consol_act/fbtaa1986312/

Barkoczy, S. (2017) Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH

Publications.

Coleman, C. (2015) Australian Tax Analysis (4th ed.). Sydney: Thomson Reuters

(Professional) Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., & Snape, T. (2015) Australian tax

handbook. (8th ed.). Pymont: Thomson Reuters.

Hodgson, H., Mortimer, C. & Butler, J. (2016) Tax Questions and Answers 2016 (6th

ed.). Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017 (2nd ed.). Brisbane:

THOMSON LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study

Manual 2016. (8th ed.). Sydney: Oxford University Press.

ATO, (2018) TR 95/35.Income Tax : Capital gains: treatment of compensation

receipts. Retrieved from http://law.ato.gov.au/atolaw/view.htm?locid=txr/tr9535/nat/ato

Austlii, (2018 a) Income Tax Assessment Act 1936- SECT 21 A. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s21a.html

Austlii, (2018 b) Fringe Benefits Tax Assessment Act 1986- SECT 9 Taxable Value of

Car Fringe Benefits – Statutory Formula. Retrieved from http://www7.austlii.edu.au/cgi-

bin/viewdoc/au/legis/cth/consol_act/fbtaa1986312/s9.html

Austlii, (2018 d) Income Tax Assessment Act 1997-SEC 8.1. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s8.1.html

Austlii, (2018 e) Income Tax Assessment Act 1997-SEC 6.10. Retrieved from

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.10.html

Austlii, (2018c) Fringe Benefits Tax Assessment Act 1986. Retrieved from

http://classic.austlii.edu.au/au/legis/cth/consol_act/fbtaa1986312/

Barkoczy, S. (2017) Foundation of Taxation Law 2017 (9th ed.). North Ryde: CCH

Publications.

Coleman, C. (2015) Australian Tax Analysis (4th ed.). Sydney: Thomson Reuters

(Professional) Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., & Snape, T. (2015) Australian tax

handbook. (8th ed.). Pymont: Thomson Reuters.

Hodgson, H., Mortimer, C. & Butler, J. (2016) Tax Questions and Answers 2016 (6th

ed.). Sydney: Thomson Reuters.

Krever, R. (2016) Australian Taxation Law Cases 2017 (2nd ed.). Brisbane:

THOMSON LAWBOOK Company.

Nethercott, L., Richardson, G., & Devos, K. (2016) Australian Taxation Study

Manual 2016. (8th ed.). Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation 2017 (4th ed.). Sydney. THOMSON

REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A.

(2015) Principles of Taxation Law 2015 (7th ed.). Pymont: Thomson Reuters.

REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., & Ting, A.

(2015) Principles of Taxation Law 2015 (7th ed.). Pymont: Thomson Reuters.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.