Taxation Report: Income Tax, Capital Gains, and Deductions Review

VerifiedAdded on 2023/06/05

|16

|2913

|127

Report

AI Summary

This report examines the taxation implications for an individual, Brent Wilson, in Australia, focusing on capital gains tax (CGT) from the sale of his house and the deductibility of legal fees. The report analyzes the application of the Income Tax Assessment Act 1997 (ITAA 1997) and the Australian Taxation Office (ATO) guidelines. Part 1 addresses the main residence exemption, calculating assessable and exempted capital gains when a portion of the property was used for income-producing purposes. Part 2 discusses the deductibility of legal fees incurred in defending against a medical negligence lawsuit. Part 3 compiles a statement of taxable income, calculating tax liability and Medicare Levy based on the provided income, capital gains, and deductions. The report provides detailed calculations and assumptions to determine the final taxable income and tax obligations of Mr. Wilson.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University:

Authors Note:

Taxation

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:...............................................................................................................................................6

Part 3:...............................................................................................................................................8

References:....................................................................................................................................13

TAXATION

Contents

Introduction:....................................................................................................................................2

Part 1:...............................................................................................................................................2

Part 2:...............................................................................................................................................6

Part 3:...............................................................................................................................................8

References:....................................................................................................................................13

2

TAXATION

Introduction:

Income Tax Assessment Act, 1997 is the current legislation in Australia governing the

provisions in relation to the income tax for the individuals and corporations in the country.

Australian Taxation Office, here in after to be referred to as ATO, is an independent statutory

body of Government of Australia that regulates the taxation environment in the country. The

relevant provisions of the Income Tax Assessment Act, 1997 (ITAA 1997) along with the

instructions of ATO shall be followed in this document to recommend the tax treatments to the

taxpayer.

Part 1:

Issue:

Identification of tax implications for the sale of Brent Wilson’s house and the treatment of

resultant capital gains, if any arising from the sale his house shall be discussed here as per ITAA

1997.

Rules:

As per ITAA 1997, capital gain is the profit arising to the seller of a capital asset from the sale of

such capital asset. Such sale must not be part of any ordinary course of business ran by him. In

Australia, capital gain was introduced on 20th September, 1985 and thus, all assets acquired after

the introduction of capital gain tax in the country, i.e. September 20, 1997 shall be eligible to be

taxed for capital gain or capital loss. However, there are certain exceptions to the provisions of

capital gain (Evans, Minas and Lim, 2015). Generally the main residence of a tax payer is

exempted from capital gain tax provided necessary conditions have been fulfilled by the owner

of the house.

TAXATION

Introduction:

Income Tax Assessment Act, 1997 is the current legislation in Australia governing the

provisions in relation to the income tax for the individuals and corporations in the country.

Australian Taxation Office, here in after to be referred to as ATO, is an independent statutory

body of Government of Australia that regulates the taxation environment in the country. The

relevant provisions of the Income Tax Assessment Act, 1997 (ITAA 1997) along with the

instructions of ATO shall be followed in this document to recommend the tax treatments to the

taxpayer.

Part 1:

Issue:

Identification of tax implications for the sale of Brent Wilson’s house and the treatment of

resultant capital gains, if any arising from the sale his house shall be discussed here as per ITAA

1997.

Rules:

As per ITAA 1997, capital gain is the profit arising to the seller of a capital asset from the sale of

such capital asset. Such sale must not be part of any ordinary course of business ran by him. In

Australia, capital gain was introduced on 20th September, 1985 and thus, all assets acquired after

the introduction of capital gain tax in the country, i.e. September 20, 1997 shall be eligible to be

taxed for capital gain or capital loss. However, there are certain exceptions to the provisions of

capital gain (Evans, Minas and Lim, 2015). Generally the main residence of a tax payer is

exempted from capital gain tax provided necessary conditions have been fulfilled by the owner

of the house.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

According to ATO, the ‘main residence’ is exempt from capital gain tax (CGT) provided the

attached conditions as enumerated in the ITAA 1997 have been followed. Sub division 118-B of

ITAA 1997 provides the provisions for main residence exemption from capital gain tax (CGT)

(Braithwaite, 2017). In order to get the main residence exemption as enumerated in subdivision

118-B of ITAA 1997 from CGT, the property, i.e. residence must have dwelling and it must have

been used by the seller for living purpose till the time it was sold. In case there is any vacant

block in the property, the exemption of main residence from CGT is not applicable to such

vacant block (Collier et. al. 2017). A dwelling is considered as the main residence of the person

who has lived in the house by himself alone or along with his family and the address of the house

has been used to deliver mail to the person.

ATO also provides exception to the above rule of main residence exemption. It provides that

though main residence is generally exempt from CGT but the tax payer would not be entitled to

the full exemption for the entire gain from the sale of main residence if any part of the dwelling

on the main residence was used for producing income to the tax payer (Owner and seller of the

property). Thus, in case any part of the dwelling on the main residence was rented out to a

business or used for the business or profession of the owner then proportionate gain from the sale

of the property shall be assessable and included in the income of the tax payer to calculate

taxable income of the tax payer. ATO provides that generally the floor area of the dwelling shall

be used as the basis to apportion the portion of gain that is to be assessable and the portion shall

be exempt under main residence exemption as per subdivision 118-B of ITAA 1997 (Jones,

2016).

Application:

TAXATION

According to ATO, the ‘main residence’ is exempt from capital gain tax (CGT) provided the

attached conditions as enumerated in the ITAA 1997 have been followed. Sub division 118-B of

ITAA 1997 provides the provisions for main residence exemption from capital gain tax (CGT)

(Braithwaite, 2017). In order to get the main residence exemption as enumerated in subdivision

118-B of ITAA 1997 from CGT, the property, i.e. residence must have dwelling and it must have

been used by the seller for living purpose till the time it was sold. In case there is any vacant

block in the property, the exemption of main residence from CGT is not applicable to such

vacant block (Collier et. al. 2017). A dwelling is considered as the main residence of the person

who has lived in the house by himself alone or along with his family and the address of the house

has been used to deliver mail to the person.

ATO also provides exception to the above rule of main residence exemption. It provides that

though main residence is generally exempt from CGT but the tax payer would not be entitled to

the full exemption for the entire gain from the sale of main residence if any part of the dwelling

on the main residence was used for producing income to the tax payer (Owner and seller of the

property). Thus, in case any part of the dwelling on the main residence was rented out to a

business or used for the business or profession of the owner then proportionate gain from the sale

of the property shall be assessable and included in the income of the tax payer to calculate

taxable income of the tax payer. ATO provides that generally the floor area of the dwelling shall

be used as the basis to apportion the portion of gain that is to be assessable and the portion shall

be exempt under main residence exemption as per subdivision 118-B of ITAA 1997 (Jones,

2016).

Application:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

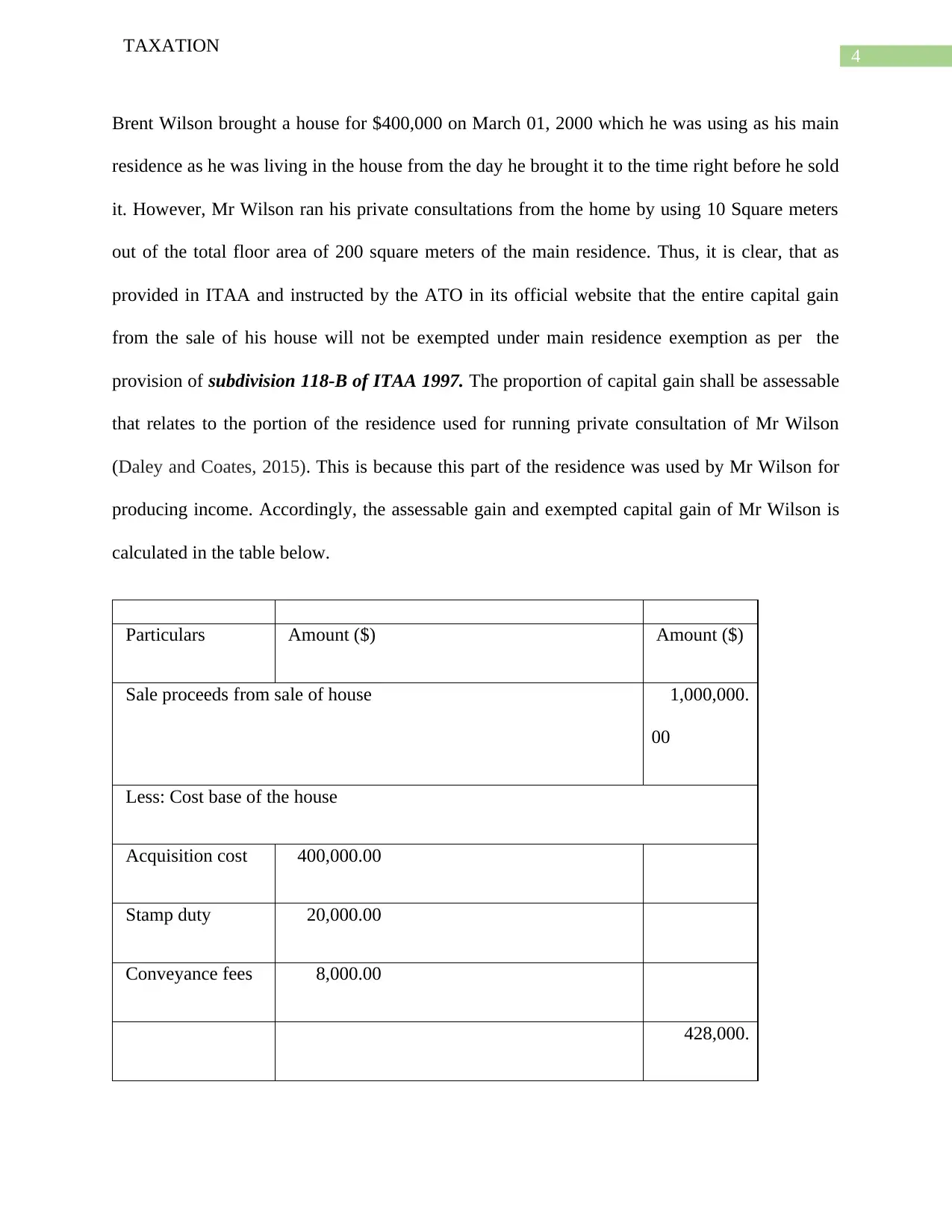

Brent Wilson brought a house for $400,000 on March 01, 2000 which he was using as his main

residence as he was living in the house from the day he brought it to the time right before he sold

it. However, Mr Wilson ran his private consultations from the home by using 10 Square meters

out of the total floor area of 200 square meters of the main residence. Thus, it is clear, that as

provided in ITAA and instructed by the ATO in its official website that the entire capital gain

from the sale of his house will not be exempted under main residence exemption as per the

provision of subdivision 118-B of ITAA 1997. The proportion of capital gain shall be assessable

that relates to the portion of the residence used for running private consultation of Mr Wilson

(Daley and Coates, 2015). This is because this part of the residence was used by Mr Wilson for

producing income. Accordingly, the assessable gain and exempted capital gain of Mr Wilson is

calculated in the table below.

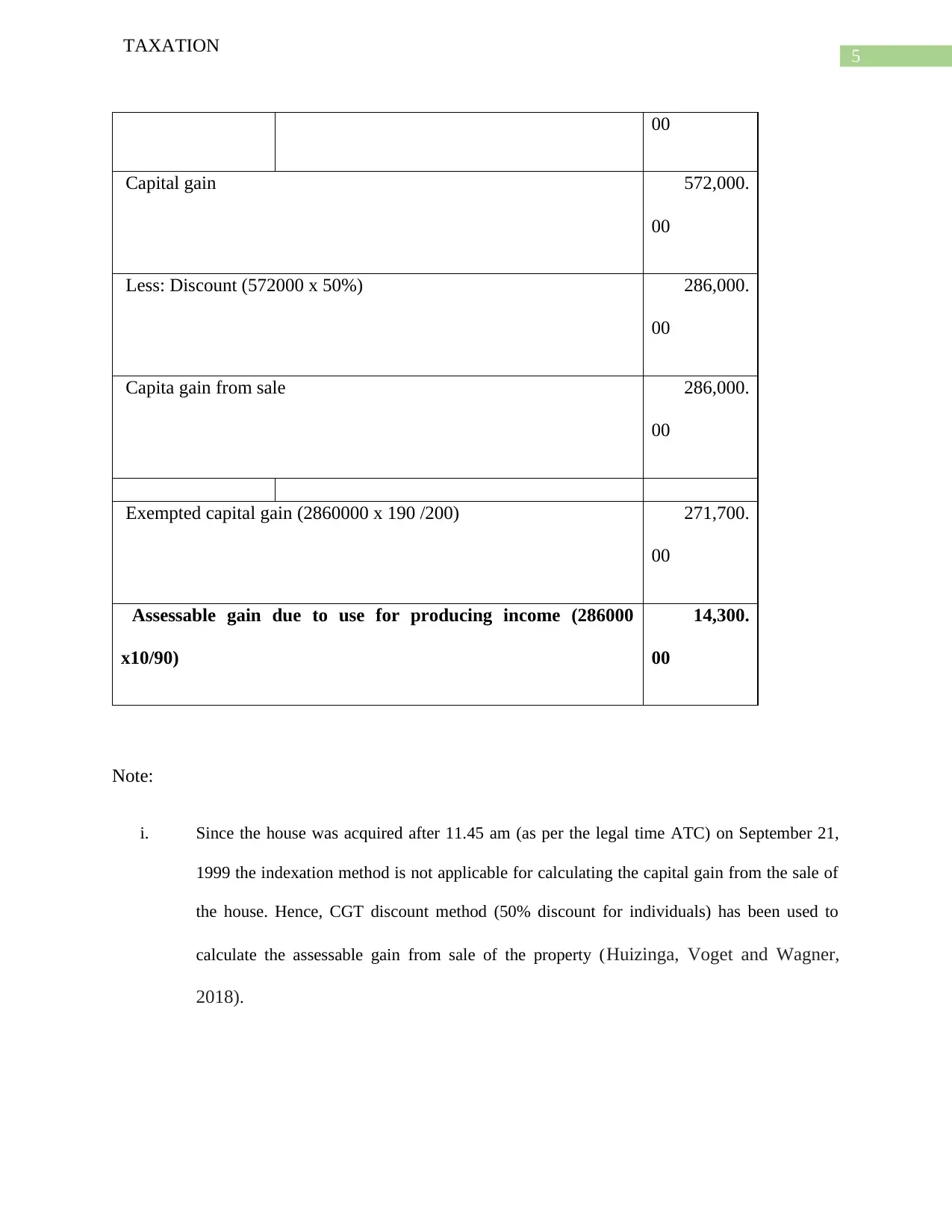

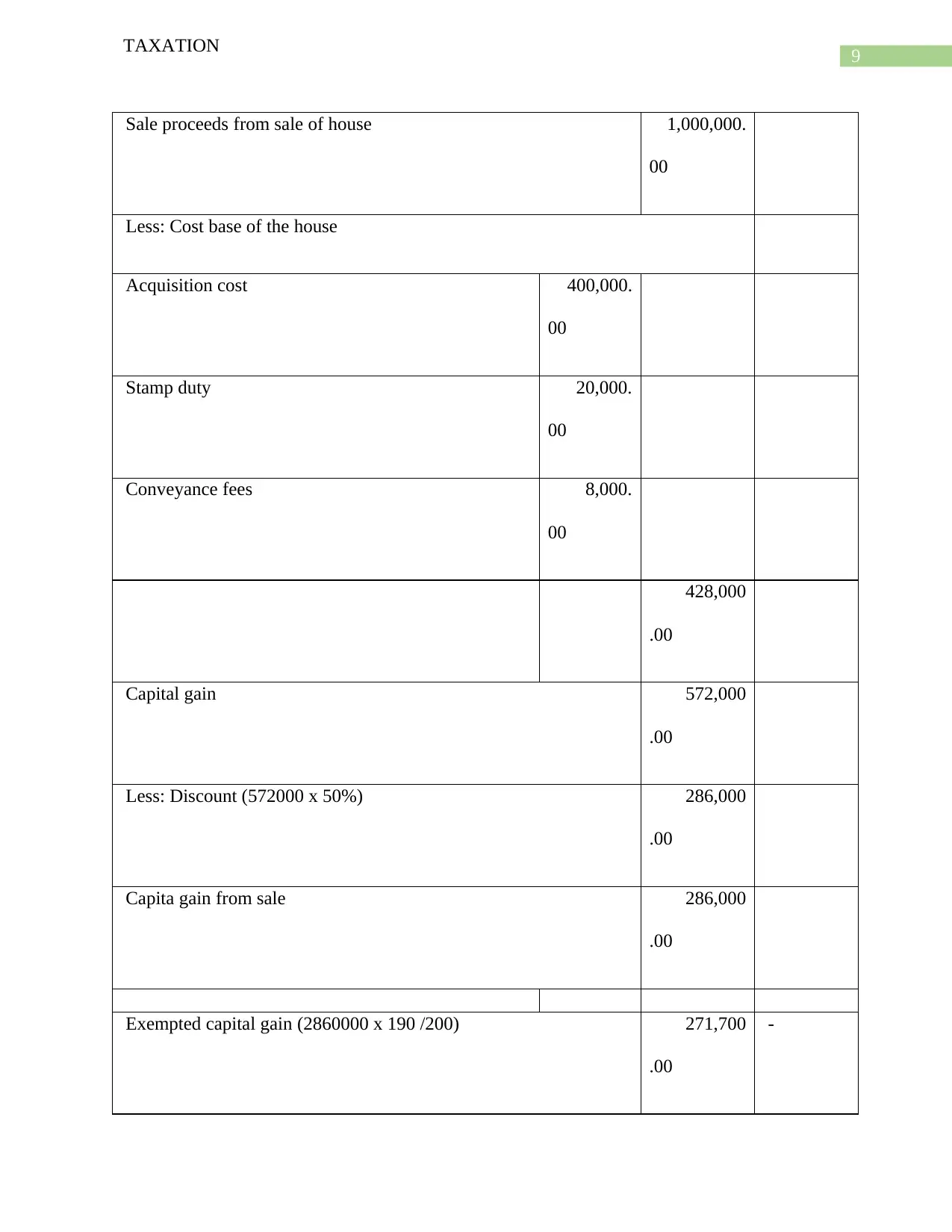

Particulars Amount ($) Amount ($)

Sale proceeds from sale of house 1,000,000.

00

Less: Cost base of the house

Acquisition cost 400,000.00

Stamp duty 20,000.00

Conveyance fees 8,000.00

428,000.

TAXATION

Brent Wilson brought a house for $400,000 on March 01, 2000 which he was using as his main

residence as he was living in the house from the day he brought it to the time right before he sold

it. However, Mr Wilson ran his private consultations from the home by using 10 Square meters

out of the total floor area of 200 square meters of the main residence. Thus, it is clear, that as

provided in ITAA and instructed by the ATO in its official website that the entire capital gain

from the sale of his house will not be exempted under main residence exemption as per the

provision of subdivision 118-B of ITAA 1997. The proportion of capital gain shall be assessable

that relates to the portion of the residence used for running private consultation of Mr Wilson

(Daley and Coates, 2015). This is because this part of the residence was used by Mr Wilson for

producing income. Accordingly, the assessable gain and exempted capital gain of Mr Wilson is

calculated in the table below.

Particulars Amount ($) Amount ($)

Sale proceeds from sale of house 1,000,000.

00

Less: Cost base of the house

Acquisition cost 400,000.00

Stamp duty 20,000.00

Conveyance fees 8,000.00

428,000.

5

TAXATION

00

Capital gain 572,000.

00

Less: Discount (572000 x 50%) 286,000.

00

Capita gain from sale 286,000.

00

Exempted capital gain (2860000 x 190 /200) 271,700.

00

Assessable gain due to use for producing income (286000

x10/90)

14,300.

00

Note:

i. Since the house was acquired after 11.45 am (as per the legal time ATC) on September 21,

1999 the indexation method is not applicable for calculating the capital gain from the sale of

the house. Hence, CGT discount method (50% discount for individuals) has been used to

calculate the assessable gain from sale of the property (Huizinga, Voget and Wagner,

2018).

TAXATION

00

Capital gain 572,000.

00

Less: Discount (572000 x 50%) 286,000.

00

Capita gain from sale 286,000.

00

Exempted capital gain (2860000 x 190 /200) 271,700.

00

Assessable gain due to use for producing income (286000

x10/90)

14,300.

00

Note:

i. Since the house was acquired after 11.45 am (as per the legal time ATC) on September 21,

1999 the indexation method is not applicable for calculating the capital gain from the sale of

the house. Hence, CGT discount method (50% discount for individuals) has been used to

calculate the assessable gain from sale of the property (Huizinga, Voget and Wagner,

2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

ii. The assessable gain has been calculated by taking into consideration 10 square meters of the

floor area out of the total of 20 square meters used by Mr Wilson to run his private

consultations.

Conclusion:

Taking into consideration the discussion and calculation provided immediately prior to this, it is

clear that the entire capital gain of Mr Wilson from sale of the house is not exempted as he used

part of the dwelling to produce income from his private consultations. Hence, as per the

calculation, the assessable amount of gain that shall be considered for calculating his total

taxable income in the income year 2018-19 would be $14,300. The majority portion of the

capital gain, i.e. $271,700 shall be exempted under the main residence exemption of subdivision

118-B of ITAA 1997 (Evans and Krever, 2017).

Part 2:

Issue:

Mr Wilson paid legal fees of $25,000 for defending himself against a medical negligence

lawsuit. The issue here is to discuss the deductibility of the legal fees incurred by Mr Wilson in

calculating his taxable income.

Rules:

Australian Taxation Office (ATO) instructs that a tax payer earning income from running a

profession as a medical practitioner, an accountant or any other professional with due

qualification, shall be allowed to deduct legal fees for defending a lawsuit against him provided

the lawsuit is decided in favour of the professional, i.e. the tax payer. The main aspect of the

TAXATION

ii. The assessable gain has been calculated by taking into consideration 10 square meters of the

floor area out of the total of 20 square meters used by Mr Wilson to run his private

consultations.

Conclusion:

Taking into consideration the discussion and calculation provided immediately prior to this, it is

clear that the entire capital gain of Mr Wilson from sale of the house is not exempted as he used

part of the dwelling to produce income from his private consultations. Hence, as per the

calculation, the assessable amount of gain that shall be considered for calculating his total

taxable income in the income year 2018-19 would be $14,300. The majority portion of the

capital gain, i.e. $271,700 shall be exempted under the main residence exemption of subdivision

118-B of ITAA 1997 (Evans and Krever, 2017).

Part 2:

Issue:

Mr Wilson paid legal fees of $25,000 for defending himself against a medical negligence

lawsuit. The issue here is to discuss the deductibility of the legal fees incurred by Mr Wilson in

calculating his taxable income.

Rules:

Australian Taxation Office (ATO) instructs that a tax payer earning income from running a

profession as a medical practitioner, an accountant or any other professional with due

qualification, shall be allowed to deduct legal fees for defending a lawsuit against him provided

the lawsuit is decided in favour of the professional, i.e. the tax payer. The main aspect of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

above ruling is to promote ethical practice in profession (Edmonds, 2015). ATO provides that

conducting professional practice with necessary skills, competencies and integrity would be

rewarded. Thus, if a professional is wrongly accused of negligence in discharging his duty and a

lawsuit is filed against the professional then in order to defend himself such professional would

have to take the legal support as necessary. If the lawsuit against the professional quashed by the

honourable court and the decision is given in favour of the professional by upholding his

professional integrity and competency then, the amount legal fees incurred will be allowed as

deduction (King and Case, 2015). This is because such legal fees is not for any breach of

professional ethics and code of conduct but to defend the rights of the professional.

Application:

Mr Wilson is a psychiatrist employed by Mindful Pty Ltd. He also runs his private consultations

to help patients deal with physiatrist issues. On May 10, 2019 Mr Wilson has paid $25,000 legal

fees to his councillor for defending a medial lawsuit against him. As provided in the rules that

the deductibility of such legal fees is dependent on the outcome of such cases (Chardon,

Freudenberg and Brimble 2016). In case the lawsuit has already been decided and the court has

declared that the medical negligence lawsuit against Mr Wilson is not correct and has quashed

the lawsuit then the legal fees of $25,000 paid by Wilson shall be allowed as deduction to

compute the taxable income of his for the income year 2018-19. As a psychiatrist it is the

responsibility of Mr Wilson to provide proper treatment to his patients. In case he has been

negligent in discharging his duties as a medical practitioner and the court decides that the

medical negligence has been committed by Mr Wilson then the legal fees will not be allowable

as deduction (Burkhauser, Hahn and Wilkins, 2015).

TAXATION

above ruling is to promote ethical practice in profession (Edmonds, 2015). ATO provides that

conducting professional practice with necessary skills, competencies and integrity would be

rewarded. Thus, if a professional is wrongly accused of negligence in discharging his duty and a

lawsuit is filed against the professional then in order to defend himself such professional would

have to take the legal support as necessary. If the lawsuit against the professional quashed by the

honourable court and the decision is given in favour of the professional by upholding his

professional integrity and competency then, the amount legal fees incurred will be allowed as

deduction (King and Case, 2015). This is because such legal fees is not for any breach of

professional ethics and code of conduct but to defend the rights of the professional.

Application:

Mr Wilson is a psychiatrist employed by Mindful Pty Ltd. He also runs his private consultations

to help patients deal with physiatrist issues. On May 10, 2019 Mr Wilson has paid $25,000 legal

fees to his councillor for defending a medial lawsuit against him. As provided in the rules that

the deductibility of such legal fees is dependent on the outcome of such cases (Chardon,

Freudenberg and Brimble 2016). In case the lawsuit has already been decided and the court has

declared that the medical negligence lawsuit against Mr Wilson is not correct and has quashed

the lawsuit then the legal fees of $25,000 paid by Wilson shall be allowed as deduction to

compute the taxable income of his for the income year 2018-19. As a psychiatrist it is the

responsibility of Mr Wilson to provide proper treatment to his patients. In case he has been

negligent in discharging his duties as a medical practitioner and the court decides that the

medical negligence has been committed by Mr Wilson then the legal fees will not be allowable

as deduction (Burkhauser, Hahn and Wilkins, 2015).

8

TAXATION

Conclusion:

Assuming that medical negligence lawsuit filed against Mr Wilson has been decided by the

honourable court in favour of Mr Wilson, the entire legal fees of $25,000 incurred for defending

the lawsuit shall be allowed as deduction for computation his taxable income.

Part 3:

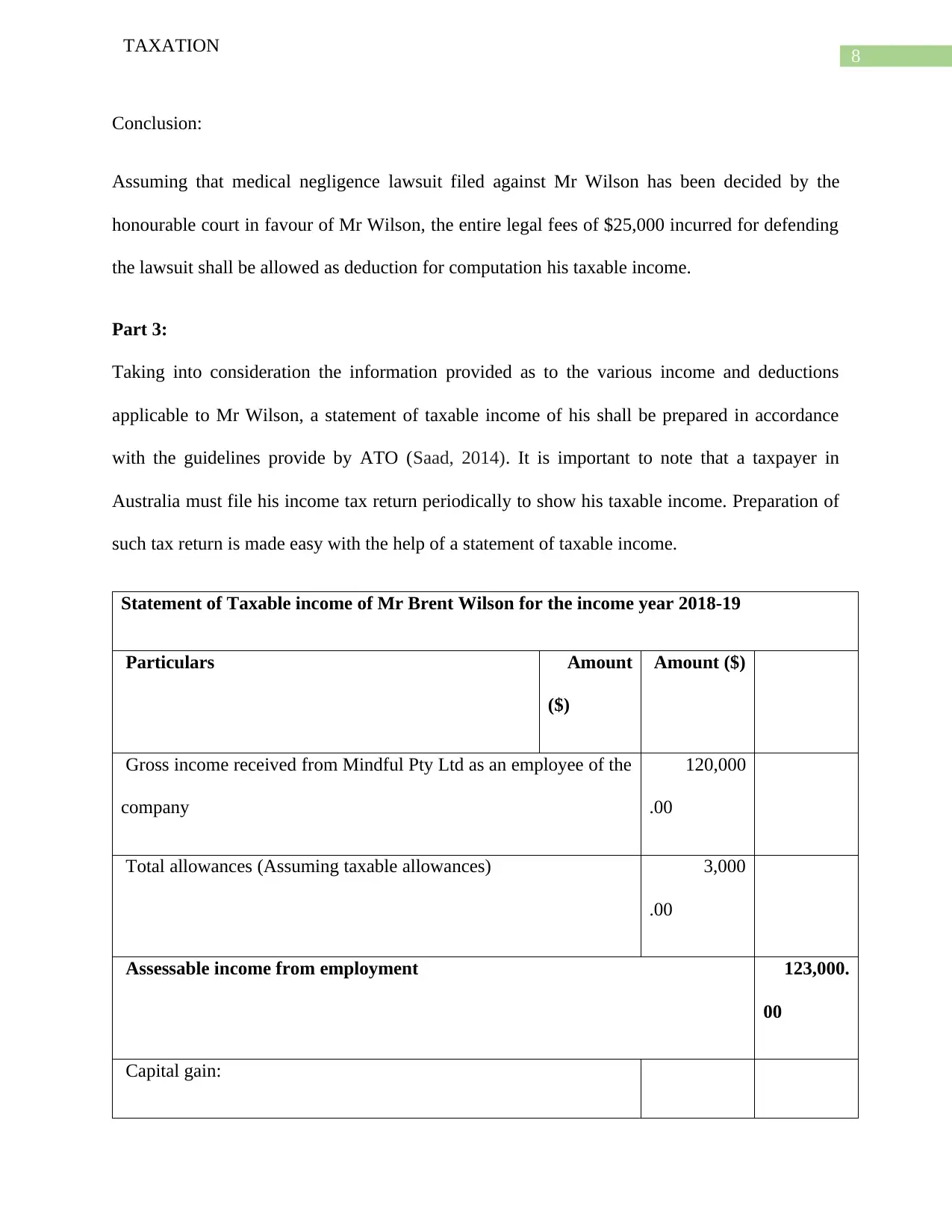

Taking into consideration the information provided as to the various income and deductions

applicable to Mr Wilson, a statement of taxable income of his shall be prepared in accordance

with the guidelines provide by ATO (Saad, 2014). It is important to note that a taxpayer in

Australia must file his income tax return periodically to show his taxable income. Preparation of

such tax return is made easy with the help of a statement of taxable income.

Statement of Taxable income of Mr Brent Wilson for the income year 2018-19

Particulars Amount

($)

Amount ($)

Gross income received from Mindful Pty Ltd as an employee of the

company

120,000

.00

Total allowances (Assuming taxable allowances) 3,000

.00

Assessable income from employment 123,000.

00

Capital gain:

TAXATION

Conclusion:

Assuming that medical negligence lawsuit filed against Mr Wilson has been decided by the

honourable court in favour of Mr Wilson, the entire legal fees of $25,000 incurred for defending

the lawsuit shall be allowed as deduction for computation his taxable income.

Part 3:

Taking into consideration the information provided as to the various income and deductions

applicable to Mr Wilson, a statement of taxable income of his shall be prepared in accordance

with the guidelines provide by ATO (Saad, 2014). It is important to note that a taxpayer in

Australia must file his income tax return periodically to show his taxable income. Preparation of

such tax return is made easy with the help of a statement of taxable income.

Statement of Taxable income of Mr Brent Wilson for the income year 2018-19

Particulars Amount

($)

Amount ($)

Gross income received from Mindful Pty Ltd as an employee of the

company

120,000

.00

Total allowances (Assuming taxable allowances) 3,000

.00

Assessable income from employment 123,000.

00

Capital gain:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

Sale proceeds from sale of house 1,000,000.

00

Less: Cost base of the house

Acquisition cost 400,000.

00

Stamp duty 20,000.

00

Conveyance fees 8,000.

00

428,000

.00

Capital gain 572,000

.00

Less: Discount (572000 x 50%) 286,000

.00

Capita gain from sale 286,000

.00

Exempted capital gain (2860000 x 190 /200) 271,700

.00

-

TAXATION

Sale proceeds from sale of house 1,000,000.

00

Less: Cost base of the house

Acquisition cost 400,000.

00

Stamp duty 20,000.

00

Conveyance fees 8,000.

00

428,000

.00

Capital gain 572,000

.00

Less: Discount (572000 x 50%) 286,000

.00

Capita gain from sale 286,000

.00

Exempted capital gain (2860000 x 190 /200) 271,700

.00

-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION

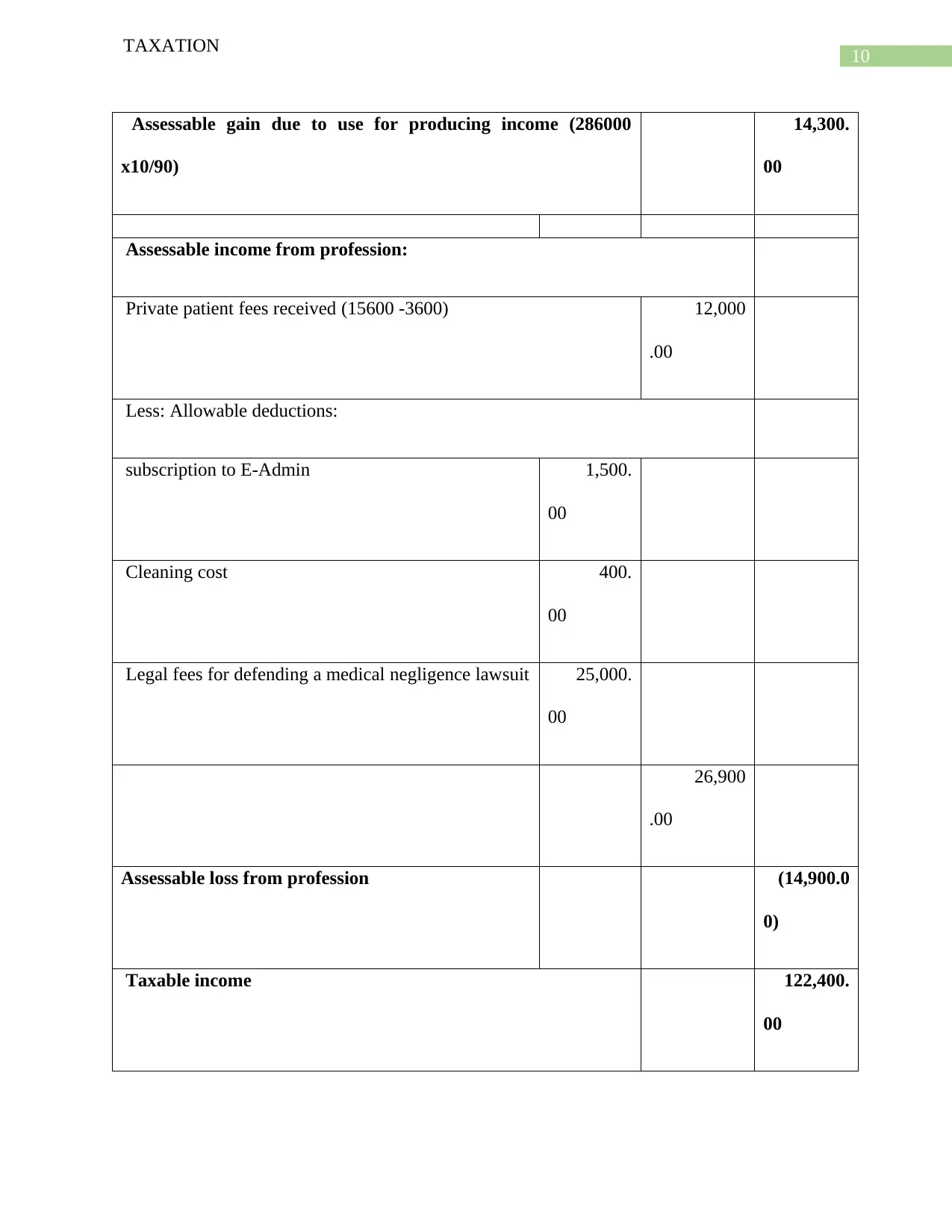

Assessable gain due to use for producing income (286000

x10/90)

14,300.

00

Assessable income from profession:

Private patient fees received (15600 -3600) 12,000

.00

Less: Allowable deductions:

subscription to E-Admin 1,500.

00

Cleaning cost 400.

00

Legal fees for defending a medical negligence lawsuit 25,000.

00

26,900

.00

Assessable loss from profession (14,900.0

0)

Taxable income 122,400.

00

TAXATION

Assessable gain due to use for producing income (286000

x10/90)

14,300.

00

Assessable income from profession:

Private patient fees received (15600 -3600) 12,000

.00

Less: Allowable deductions:

subscription to E-Admin 1,500.

00

Cleaning cost 400.

00

Legal fees for defending a medical negligence lawsuit 25,000.

00

26,900

.00

Assessable loss from profession (14,900.0

0)

Taxable income 122,400.

00

11

TAXATION

Note:

In calculating the taxable income of Mr Brent Wilson it has been assumed that assessable income

from profession does not include any other income and the negative income from profession is

due to the deduction of legal fees incurred by Mr Wilson for defending a law suit of medical

negligence against him. It has been assumed that the law suit has been decided in favour of Mr

Wilson thus, such fees has been deduced in computing the assessable income from profession

(Wilkins, 2015).

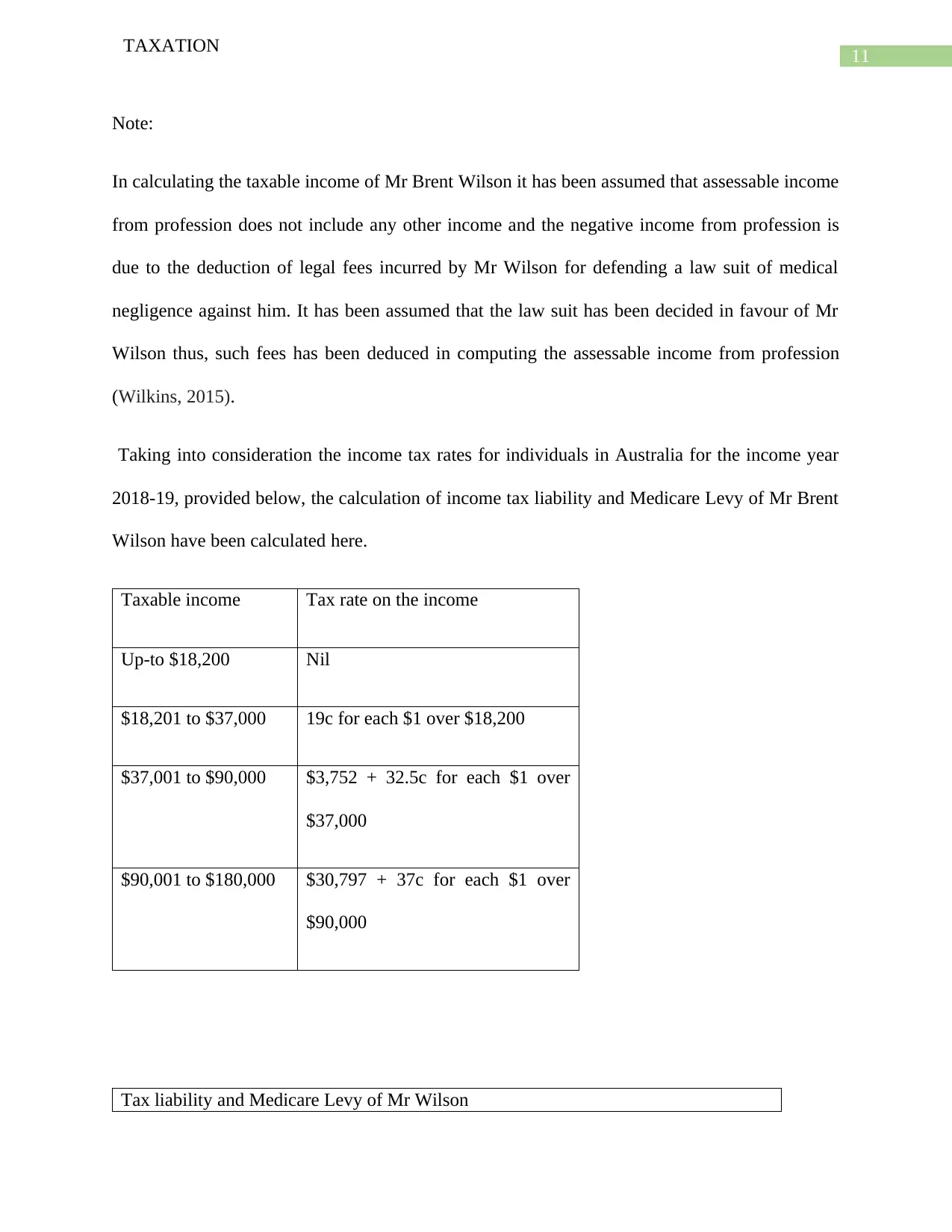

Taking into consideration the income tax rates for individuals in Australia for the income year

2018-19, provided below, the calculation of income tax liability and Medicare Levy of Mr Brent

Wilson have been calculated here.

Taxable income Tax rate on the income

Up-to $18,200 Nil

$18,201 to $37,000 19c for each $1 over $18,200

$37,001 to $90,000 $3,752 + 32.5c for each $1 over

$37,000

$90,001 to $180,000 $30,797 + 37c for each $1 over

$90,000

Tax liability and Medicare Levy of Mr Wilson

TAXATION

Note:

In calculating the taxable income of Mr Brent Wilson it has been assumed that assessable income

from profession does not include any other income and the negative income from profession is

due to the deduction of legal fees incurred by Mr Wilson for defending a law suit of medical

negligence against him. It has been assumed that the law suit has been decided in favour of Mr

Wilson thus, such fees has been deduced in computing the assessable income from profession

(Wilkins, 2015).

Taking into consideration the income tax rates for individuals in Australia for the income year

2018-19, provided below, the calculation of income tax liability and Medicare Levy of Mr Brent

Wilson have been calculated here.

Taxable income Tax rate on the income

Up-to $18,200 Nil

$18,201 to $37,000 19c for each $1 over $18,200

$37,001 to $90,000 $3,752 + 32.5c for each $1 over

$37,000

$90,001 to $180,000 $30,797 + 37c for each $1 over

$90,000

Tax liability and Medicare Levy of Mr Wilson

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.