Taxation Assignment: Capital Gains and Fringe Benefit Tax Analysis

VerifiedAdded on 2023/06/04

|21

|3227

|151

Homework Assignment

AI Summary

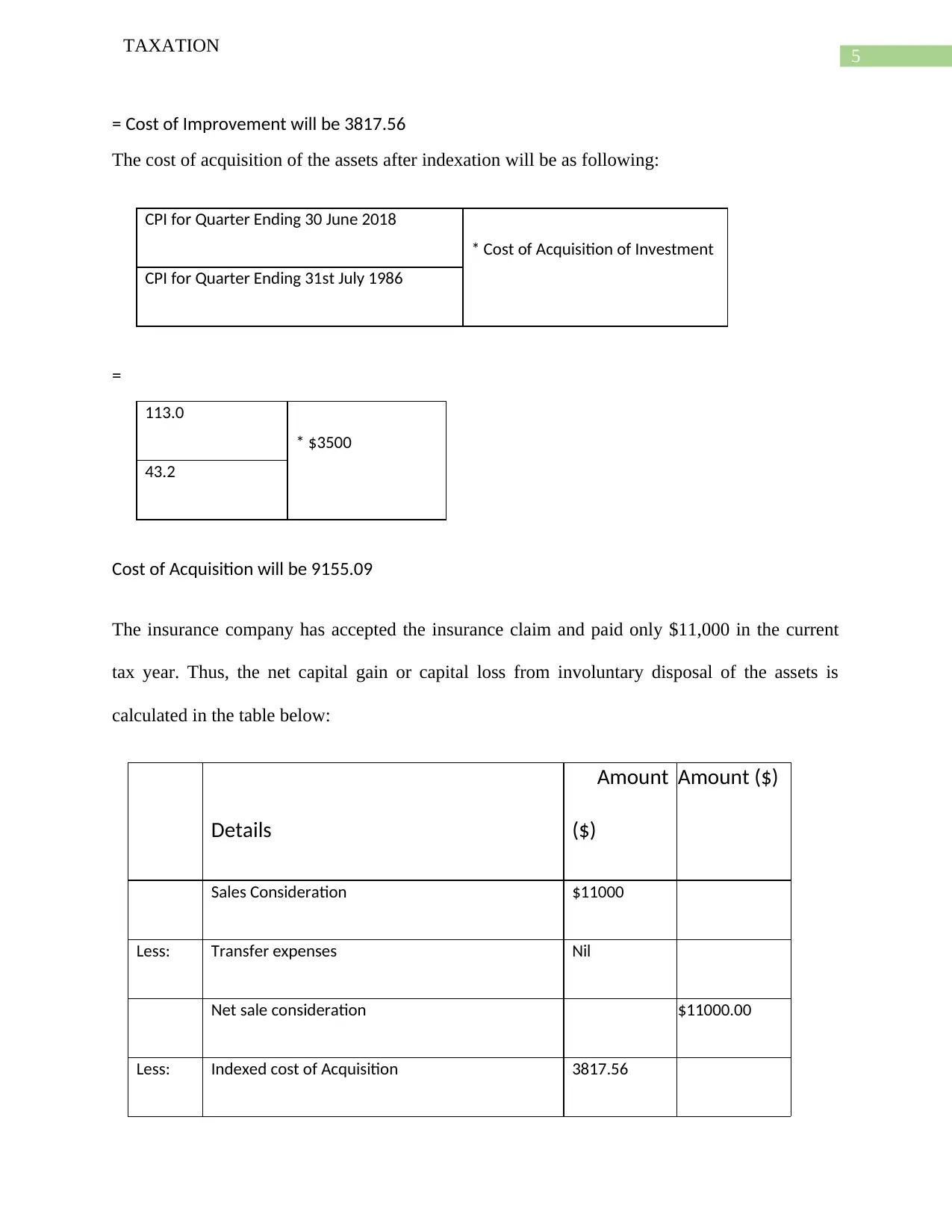

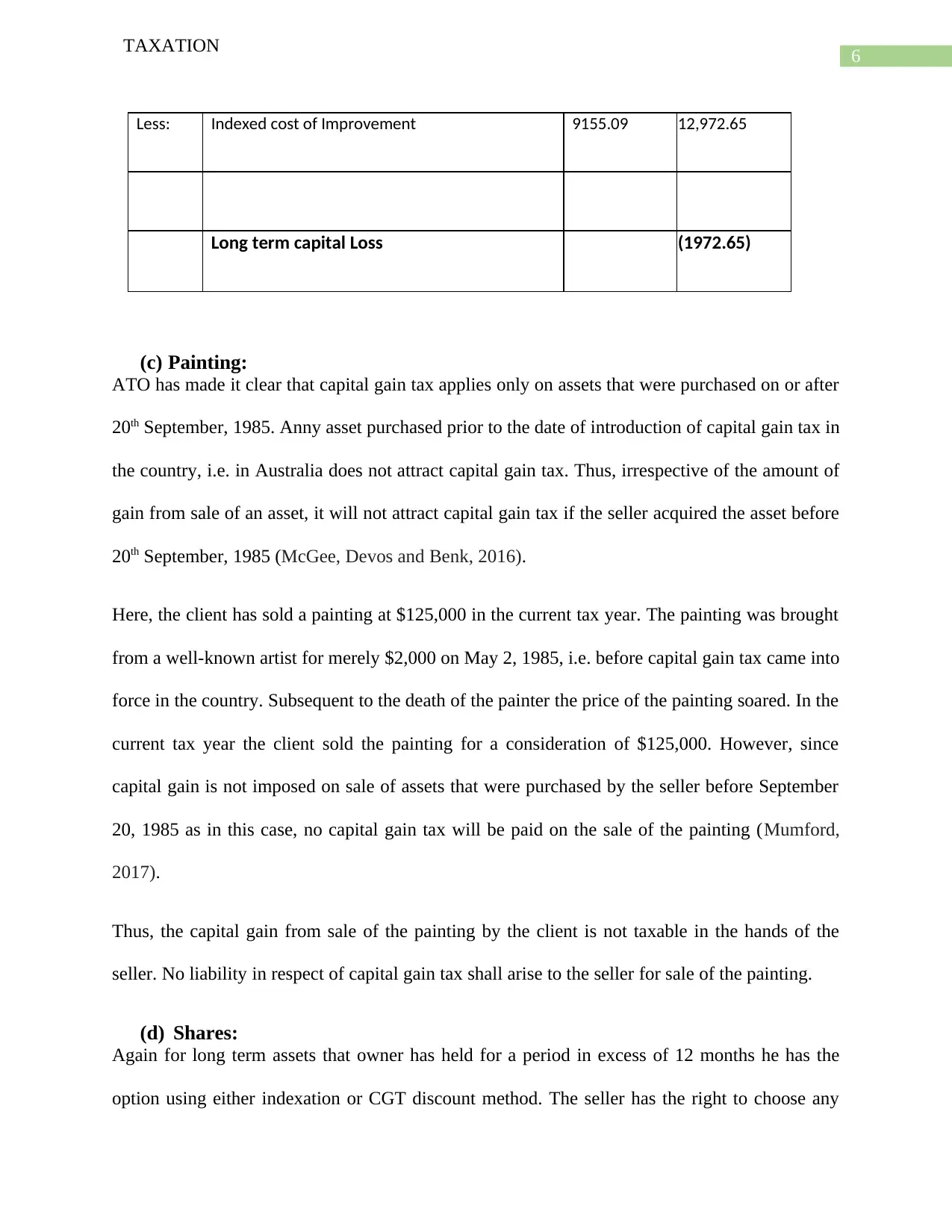

This document presents a comprehensive solution to a taxation assignment, addressing various aspects of Australian taxation law. The assignment analyzes capital gains tax (CGT) implications on the sale of assets such as vacant land, an antique bed, shares, and a violin, considering factors like acquisition costs, CGT discounts, and indexation. It also delves into fringe benefit tax (FBT) calculations related to providing a car to an employee, using statutory percentage methods. The solution includes detailed calculations, explanations, and references to relevant tax regulations and case laws, providing a thorough understanding of the tax implications for the client's transactions and employment benefits. The assignment covers key elements of taxation theory, practice, and law, offering a practical application of tax principles.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.