Taxation Analysis Report

VerifiedAdded on 2020/03/28

|12

|2441

|39

Report

AI Summary

This report provides a comprehensive analysis of various taxation issues, including capital gains, fringe benefits, and the implications of specific tax rulings under Australian law. It discusses the application of the Income Tax Assessment Act (ITAA) 1997 and relevant case studies, offering insights into tax compliance and the legal framework governing taxation in Australia.

Running Head: TAXATION

Taxation

Name of the Student

Name of the University

Author Note

Taxation

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

ANSWER 1

Issue

The issue is regarding the measurement of the sustainable amount that can be obtained

from the loss or gain of the capital. The issue has to be discussed according to the Section 108-

(10) of the ITAA 1997.

Laws:

i. “Section 108-(20) of the ITAA 1997”

ii. “Section 108-(10) of ITAA 1997”

Applications

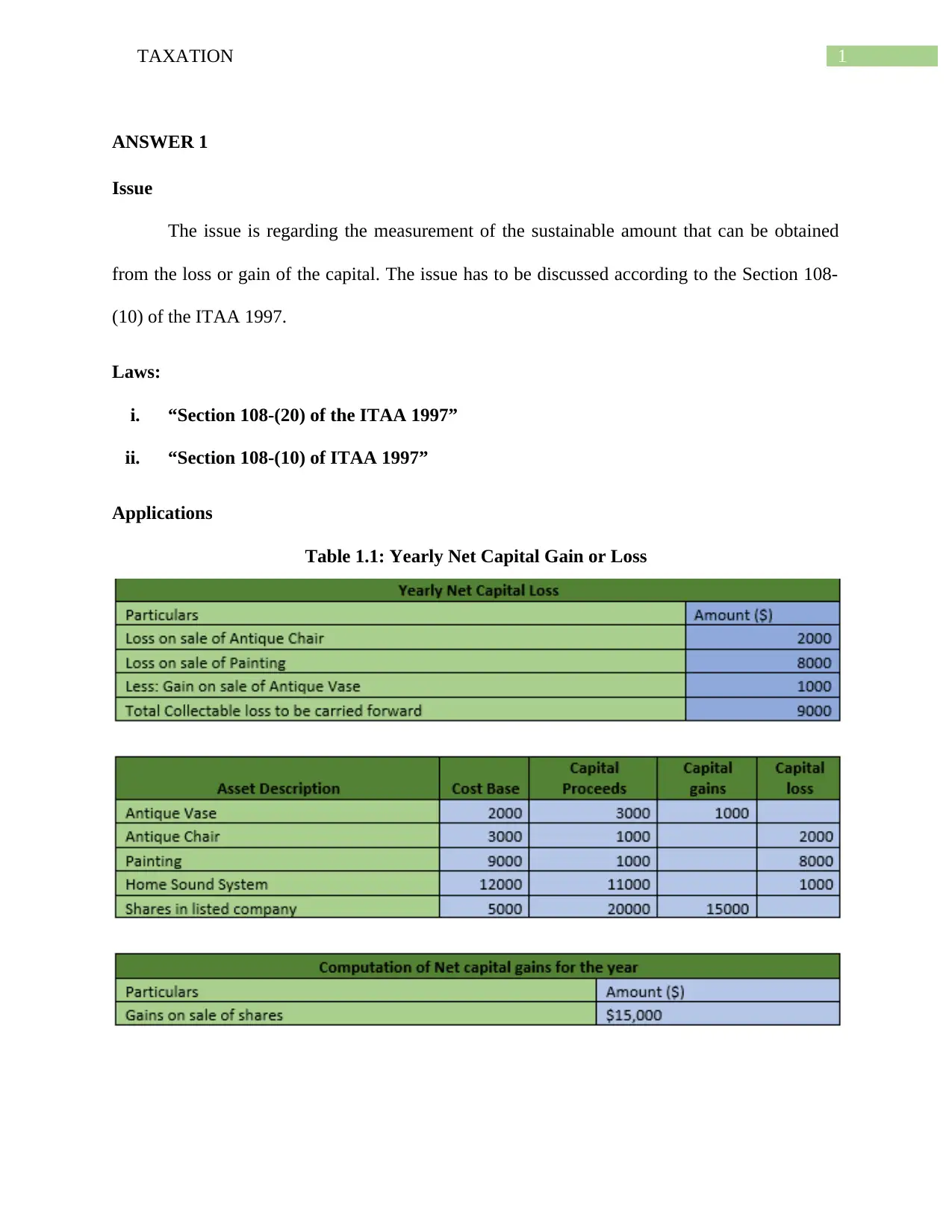

Table 1.1: Yearly Net Capital Gain or Loss

ANSWER 1

Issue

The issue is regarding the measurement of the sustainable amount that can be obtained

from the loss or gain of the capital. The issue has to be discussed according to the Section 108-

(10) of the ITAA 1997.

Laws:

i. “Section 108-(20) of the ITAA 1997”

ii. “Section 108-(10) of ITAA 1997”

Applications

Table 1.1: Yearly Net Capital Gain or Loss

2TAXATION

From the figures obtained from the taxpayer, it is clear that the loss that has been incurred

by selling the sound system is not enough to get approval to set off. The sound system is known

as personal asset. Thus, the loss that has been incurred from its sale is not eligible for set off. The

evidence for this discussion stated above is present in the guiding principles of “Section 108-

(10) of ITAA 1997”. The section states that the loss which is collectable in nature is not

considered for offset against the gains of ordinary nature that has been obtained from the sale of

shares and hence will not be allowed for set off (Dabner 2014). Keeping in mind the principles of

the “Section 108-(10) of ITAA 1997” profits were produced by Eric by selling ordinary assets

which did not have any existing yearly capital or reductions that can be relevant. As a result, Eric

incurred a capital gain of $15,000.

Conclusion

From the discussion above, it can be stated that Eric cannot set off the loss that he

incurred from the collectibles as the revenue was already received by him by selling the ordinary

assets.

From the figures obtained from the taxpayer, it is clear that the loss that has been incurred

by selling the sound system is not enough to get approval to set off. The sound system is known

as personal asset. Thus, the loss that has been incurred from its sale is not eligible for set off. The

evidence for this discussion stated above is present in the guiding principles of “Section 108-

(10) of ITAA 1997”. The section states that the loss which is collectable in nature is not

considered for offset against the gains of ordinary nature that has been obtained from the sale of

shares and hence will not be allowed for set off (Dabner 2014). Keeping in mind the principles of

the “Section 108-(10) of ITAA 1997” profits were produced by Eric by selling ordinary assets

which did not have any existing yearly capital or reductions that can be relevant. As a result, Eric

incurred a capital gain of $15,000.

Conclusion

From the discussion above, it can be stated that Eric cannot set off the loss that he

incurred from the collectibles as the revenue was already received by him by selling the ordinary

assets.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

Answer 2

Issue

The problem in this case is in computing the taxable value for the FBT year 2016/17, the

concept of which is described under the “Fringe Benefit Tax Act 1986”.

Laws:

i. “Fringe Benefit Tax Act 1986”

ii. “Taxation Rulings TR 93/6”

Applications

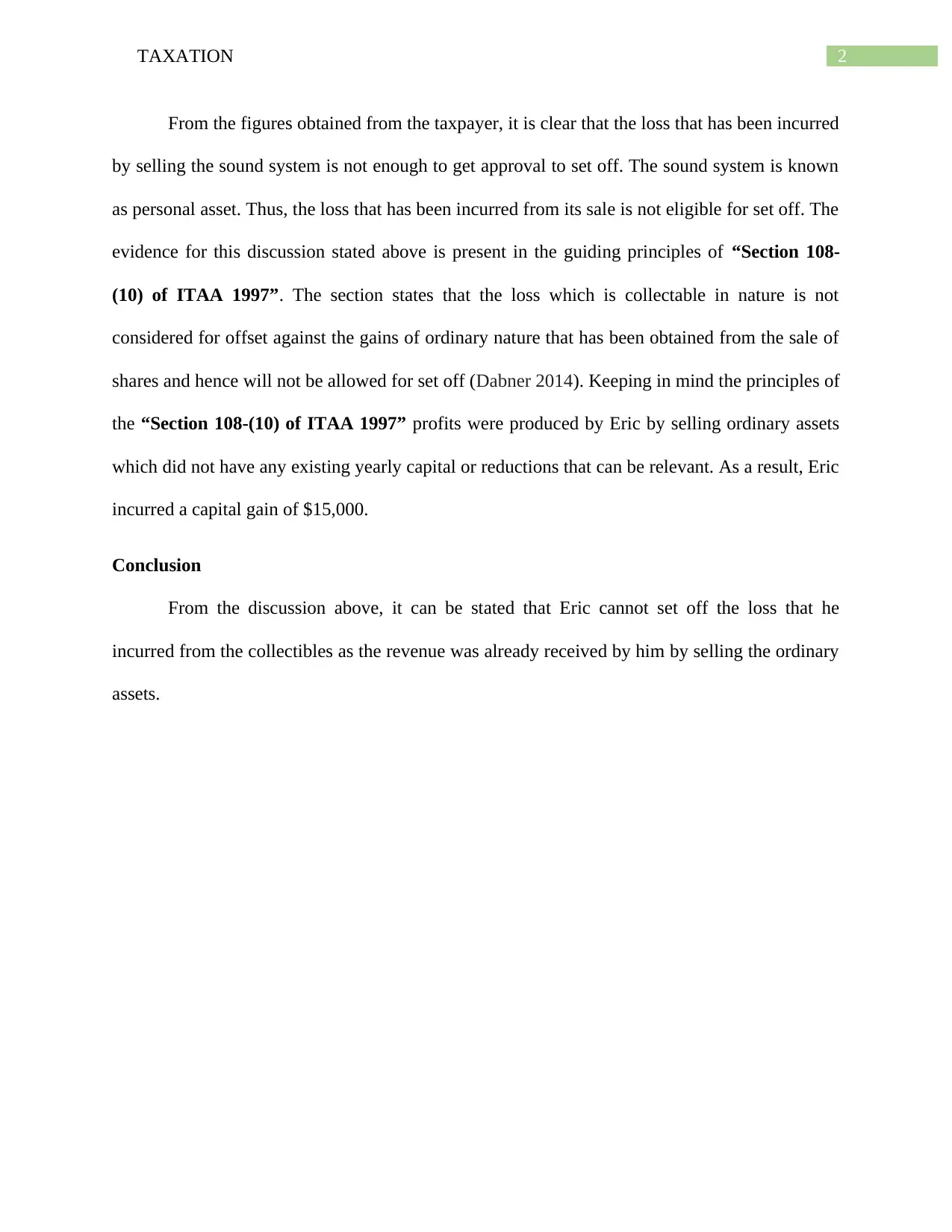

Table 2.1: Fringe Benefit Tax Calculations

Answer 2

Issue

The problem in this case is in computing the taxable value for the FBT year 2016/17, the

concept of which is described under the “Fringe Benefit Tax Act 1986”.

Laws:

i. “Fringe Benefit Tax Act 1986”

ii. “Taxation Rulings TR 93/6”

Applications

Table 2.1: Fringe Benefit Tax Calculations

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

From the guidelines stated in “Taxation Rulings TR 93/6” it can be understood that

different types of banks or companies that provide loans makes different plans to offset the

interests in the loan accounts of the people (Cane and Atiyah 2013). The guidelines of the rulings

mainly state that the customers will not be required to make any tax payments for the income

that has been derived by offsetting the interest. Taking into account this ruling and the figures

obtained from Brian’s accounts, he will not have to pay any interest at the end of the period of

loan and thus will not have to pay any taxes.

Conclusion

Thus, from the discussion done above, it can be concluded that Brian will not have to pay

any income tax if the interest that is payable for his loan is payable at the end of the loan period.

From the guidelines stated in “Taxation Rulings TR 93/6” it can be understood that

different types of banks or companies that provide loans makes different plans to offset the

interests in the loan accounts of the people (Cane and Atiyah 2013). The guidelines of the rulings

mainly state that the customers will not be required to make any tax payments for the income

that has been derived by offsetting the interest. Taking into account this ruling and the figures

obtained from Brian’s accounts, he will not have to pay any interest at the end of the period of

loan and thus will not have to pay any taxes.

Conclusion

Thus, from the discussion done above, it can be concluded that Brian will not have to pay

any income tax if the interest that is payable for his loan is payable at the end of the loan period.

5TAXATION

Answer 3

Issue

The issue described in this question relates to the loss distribution, which the taxpayers

incur from joint ownership of rental property.

Laws:

i. “FC of T v McDonald”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation ruling TR 93/23”

Applications

The guidelines described in “Taxation Ruling TR 93/32”, the income tax division or any

kind of loss that has been incurred from a rented property amongst the joint owners of the

property has been described (Althaus, Bridgman and Davis 2012). However, the ruling described

above states that rule for judging the measurable position of the co-owners which cannot be

considered valid for running a business within the defined curriculum. Thus, in this case the

assessable positions of Jack and Jill are measured from the property that they have rented. It has

been observed that the Jack will be earning 10% of the profit and his wife Jill will be earning the

remaining 90% of the profit from their rented property.

According to the TR 92/32 ruling, joint ownership can be indicated as a partnership

business which will influence the income tax to be paid by a taxpayer. The idea of the general

law defines that income tax is not concerned with partnership (Althaus, Bridgman and Davis

2012). This concept of joint ownership in any kind of business is not considered in paying the

income taxes. If the company suffers from a loss in income from the property that is rented, then

Answer 3

Issue

The issue described in this question relates to the loss distribution, which the taxpayers

incur from joint ownership of rental property.

Laws:

i. “FC of T v McDonald”

ii. “Section 51 of the ITAA 1997”

iii. “Taxation ruling TR 93/23”

Applications

The guidelines described in “Taxation Ruling TR 93/32”, the income tax division or any

kind of loss that has been incurred from a rented property amongst the joint owners of the

property has been described (Althaus, Bridgman and Davis 2012). However, the ruling described

above states that rule for judging the measurable position of the co-owners which cannot be

considered valid for running a business within the defined curriculum. Thus, in this case the

assessable positions of Jack and Jill are measured from the property that they have rented. It has

been observed that the Jack will be earning 10% of the profit and his wife Jill will be earning the

remaining 90% of the profit from their rented property.

According to the TR 92/32 ruling, joint ownership can be indicated as a partnership

business which will influence the income tax to be paid by a taxpayer. The idea of the general

law defines that income tax is not concerned with partnership (Althaus, Bridgman and Davis

2012). This concept of joint ownership in any kind of business is not considered in paying the

income taxes. If the company suffers from a loss in income from the property that is rented, then

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

the loss will be determined in accordance to the joint ownership and distributed according to the

profits and losses suffered. From the situation of Jack and Jill described in the question, it can be

clearly understood that according to the general law, the income tax accounted for the joint

ownership of the rented property will not be distributed as the partnership. However, it can be

said that the basis of the income tax has been framed by the joint ownership but the distribution

of the income tax payable is not dependent on the percentage of ownership.

The guidelines provided in “Taxation ruling TR 92/32” helps to understand the fact that

under the general law, joint ownership of the leased property will not be considered as a

partnership business (Aust 2013). In this problem, the agreement of the partnership between Jack

and Jill, which can have some written document or can be oral, thus has no impact on the income

shares or loss that has been achieved by renting the property. In the article of the agreement, it

was stated that the person who will be responsible for the total loss incurred by renting the

property is Jack. This case resembled somewhat the case of Mr. McDonald. In the case of “FC

of T v McDonald” (1987), it was stated that Mr. and Mrs. McDonald would have 25% and 75%

of the profits earned from their property (Palan, Murphy and Chavagneux 2013). Thus, when

there will be any loss from the property, Mr. McDonald will bear the total loss and the income of

his wife will prevent his wife to compensate for such loss. This will result in the advancement of

his wife’s income.

Just like the plan of Mr. McDonald, the partnership of Jack and Jill will not be considered

under the general law and thus any loss incurred from their business can be shared equally

amongst them so that no one is overburdened.

the loss will be determined in accordance to the joint ownership and distributed according to the

profits and losses suffered. From the situation of Jack and Jill described in the question, it can be

clearly understood that according to the general law, the income tax accounted for the joint

ownership of the rented property will not be distributed as the partnership. However, it can be

said that the basis of the income tax has been framed by the joint ownership but the distribution

of the income tax payable is not dependent on the percentage of ownership.

The guidelines provided in “Taxation ruling TR 92/32” helps to understand the fact that

under the general law, joint ownership of the leased property will not be considered as a

partnership business (Aust 2013). In this problem, the agreement of the partnership between Jack

and Jill, which can have some written document or can be oral, thus has no impact on the income

shares or loss that has been achieved by renting the property. In the article of the agreement, it

was stated that the person who will be responsible for the total loss incurred by renting the

property is Jack. This case resembled somewhat the case of Mr. McDonald. In the case of “FC

of T v McDonald” (1987), it was stated that Mr. and Mrs. McDonald would have 25% and 75%

of the profits earned from their property (Palan, Murphy and Chavagneux 2013). Thus, when

there will be any loss from the property, Mr. McDonald will bear the total loss and the income of

his wife will prevent his wife to compensate for such loss. This will result in the advancement of

his wife’s income.

Just like the plan of Mr. McDonald, the partnership of Jack and Jill will not be considered

under the general law and thus any loss incurred from their business can be shared equally

amongst them so that no one is overburdened.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

Conclusion

Thus, from the discussions above, it is clear that Jack and Jill will be sharing the loss

incurred by their renting business equally amongst them and the joint ownership of their business

will not be considered as a partnership business.

Answer 4

The most commonly quoted ruling, which states that avoiding tax can be legal and

accepted, has been mentioned in the “IRC v Duke Westminster (1936)”. The wages of the

gardener of the Duke of Westminster was paid weekly. Now he made a contract and drew up the

covenant agreement of paying weekly wages to the gardeners. He instead started paying them an

equivalent amount. As a result of this contract, the gardeners were happy as they as they have

been receiving an equivalent amount as their wages but the Duke started to gain tax benefits.

This was because of the law with the help of which the liability of the Duke to surtax was

lowered by the covenant (Braithwaite, Murphy and Reinhart 2013). The situation discussed

above describes that every person can lower the tax affairs than what he had to pay by

implementing certain plans to do so. It cannot be made compulsory for a person to pay a higher

amount of tax that what he had to pay.

With the application of this law discussed above in today’s life, it can be said that if a

person becomes successful enough to implement this law in his life, then the taxpayers genuinely

cannot be forced to pay taxes that are higher than what he had to pay (Burkhauser, Hahn and

Wilkins 2015). A person gets an opportunity to reduce their liability of taxes by agreeing to the

financial terms of the law with the application of this concept described above.

Conclusion

Thus, from the discussions above, it is clear that Jack and Jill will be sharing the loss

incurred by their renting business equally amongst them and the joint ownership of their business

will not be considered as a partnership business.

Answer 4

The most commonly quoted ruling, which states that avoiding tax can be legal and

accepted, has been mentioned in the “IRC v Duke Westminster (1936)”. The wages of the

gardener of the Duke of Westminster was paid weekly. Now he made a contract and drew up the

covenant agreement of paying weekly wages to the gardeners. He instead started paying them an

equivalent amount. As a result of this contract, the gardeners were happy as they as they have

been receiving an equivalent amount as their wages but the Duke started to gain tax benefits.

This was because of the law with the help of which the liability of the Duke to surtax was

lowered by the covenant (Braithwaite, Murphy and Reinhart 2013). The situation discussed

above describes that every person can lower the tax affairs than what he had to pay by

implementing certain plans to do so. It cannot be made compulsory for a person to pay a higher

amount of tax that what he had to pay.

With the application of this law discussed above in today’s life, it can be said that if a

person becomes successful enough to implement this law in his life, then the taxpayers genuinely

cannot be forced to pay taxes that are higher than what he had to pay (Burkhauser, Hahn and

Wilkins 2015). A person gets an opportunity to reduce their liability of taxes by agreeing to the

financial terms of the law with the application of this concept described above.

8TAXATION

Answer 5

Issue

The issue of this question is to provide an assessment which relates to deforestation and

cutting down of timber under “Subsection 6-(1) if ITAA 1997”.

Laws

i. “Subsection 6-(1) of the ITAA 1936”

ii. “McCauley v FC of T”

iii. “Taxation Rulings of TR 95/6”

iv. “Subsection 36-(1)”

v. “Section 26-(f)”

Application

From the present issue of Bill it is discovered that Bill is the proprietor of the land in

which there are a lot of pine trees. He initially planned to clear the land and start to graze sheep.

In the process, he was approached by a lodging company and they agreed to pay an amount of

$1000 for each meter of timbre that can be taken from the land by the lodging firm.

According to the taxation ruling described in “Taxation ruling TR 95/6”, the rulings of

income tax start from the performances of the initial production and forestry (Saad 2014). This

law also explains the extent to which an income of an individual from the activities of forestry

can be assessed. The taxpayers who are involved in any sort of primary forestry business such as

timber disposal also falls under this taxation ruling. According to the information provided in

“Subsection 6-(1) of the ITAA 1936” any taxpayer who is working on forest operations is

Answer 5

Issue

The issue of this question is to provide an assessment which relates to deforestation and

cutting down of timber under “Subsection 6-(1) if ITAA 1997”.

Laws

i. “Subsection 6-(1) of the ITAA 1936”

ii. “McCauley v FC of T”

iii. “Taxation Rulings of TR 95/6”

iv. “Subsection 36-(1)”

v. “Section 26-(f)”

Application

From the present issue of Bill it is discovered that Bill is the proprietor of the land in

which there are a lot of pine trees. He initially planned to clear the land and start to graze sheep.

In the process, he was approached by a lodging company and they agreed to pay an amount of

$1000 for each meter of timbre that can be taken from the land by the lodging firm.

According to the taxation ruling described in “Taxation ruling TR 95/6”, the rulings of

income tax start from the performances of the initial production and forestry (Saad 2014). This

law also explains the extent to which an income of an individual from the activities of forestry

can be assessed. The taxpayers who are involved in any sort of primary forestry business such as

timber disposal also falls under this taxation ruling. According to the information provided in

“Subsection 6-(1) of the ITAA 1936” any taxpayer who is working on forest operations is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

considered as a basic producer of income tax. This will be applicable only if the individual can

provide proper document to establish that forest operations is a part of his business (Saad 2014).

The initial production of this business can be regarded as tree plantation and nurturing

them as required according to the “Subsection 6-(1) of the ITAA 1936” (Norbury 2015). In the

situation described in this question, Bill is a primary producer as he is involved in the work of

cutting down the pine trees of his own land. Forest operations include planting and cutting down

of trees for vegetation. The taxpayer in this case has no role in planting or cutting them down by

himself.

Thus, from the above discussion, it can be said that Bill did not plant any pine tree,

neither did he cut them down by himself. However, the income that is made by Bill by selling the

timbre is an assessable amount for tax. Thus, according to the “Subsection 36-(1)” the sum of

money earned from this timbre business will fall under the taxable income of bill.

The income can be considered in another way. A very large amount of $50,000 was made

to the taxpayer as he was assigned by a company to cut down the timbre that will be necessary

for them. For this, tax payer can receive the amount as “Royalties”. According to the “Section

26-(f)” the royalty received by a taxpayer from the company will also fall under the assessable

yearly income for income tax (Norbury 2015). Now, in this scenario, if Bill receives royalty from

the company for cutting down trees and providing them with timbre, this will be a proof of

running a business in forest operations. Thus, the income of Bill by selling the timbre in this

situation will be included in his tax assessment income at the end of the financial year according

to “Section 26-(f)”

considered as a basic producer of income tax. This will be applicable only if the individual can

provide proper document to establish that forest operations is a part of his business (Saad 2014).

The initial production of this business can be regarded as tree plantation and nurturing

them as required according to the “Subsection 6-(1) of the ITAA 1936” (Norbury 2015). In the

situation described in this question, Bill is a primary producer as he is involved in the work of

cutting down the pine trees of his own land. Forest operations include planting and cutting down

of trees for vegetation. The taxpayer in this case has no role in planting or cutting them down by

himself.

Thus, from the above discussion, it can be said that Bill did not plant any pine tree,

neither did he cut them down by himself. However, the income that is made by Bill by selling the

timbre is an assessable amount for tax. Thus, according to the “Subsection 36-(1)” the sum of

money earned from this timbre business will fall under the taxable income of bill.

The income can be considered in another way. A very large amount of $50,000 was made

to the taxpayer as he was assigned by a company to cut down the timbre that will be necessary

for them. For this, tax payer can receive the amount as “Royalties”. According to the “Section

26-(f)” the royalty received by a taxpayer from the company will also fall under the assessable

yearly income for income tax (Norbury 2015). Now, in this scenario, if Bill receives royalty from

the company for cutting down trees and providing them with timbre, this will be a proof of

running a business in forest operations. Thus, the income of Bill by selling the timbre in this

situation will be included in his tax assessment income at the end of the financial year according

to “Section 26-(f)”

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Conclusion

The discussion above thus provides the information that the income of Bill by cutting

down and selling the timbre to the company will be assessed for income tax. In the second

scenario, the huge amount of money received by Bill for selling the timbre to the company will

be royalty which the company will be paying Bill for selling his timbre.

Conclusion

The discussion above thus provides the information that the income of Bill by cutting

down and selling the timbre to the company will be assessed for income tax. In the second

scenario, the huge amount of money received by Bill for selling the timbre to the company will

be royalty which the company will be paying Bill for selling his timbre.

11TAXATION

References

Althaus, C., Bridgman, P. and Davis, G., 2012. The Australian policy handbook. Allen & Unwin.

Aust, A., 2013. Modern treaty law and practice. Cambridge University Press.

Braithwaite, V., Murphy, K. and Reinhart, M., 2013. Taxation threat, motivational postures, and

responsive regulation. Law & Policy, 29(1), pp.137-158.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Cane, P. and Atiyah, P.S., 2013. Atiyah's accidents, compensation and the law. Cambridge

University Press.

Dabner, J., 2014. Commentary on 108-A of ITAA 1997: CGT asset rules. In Australian Tax

Practice. Thomson Legal and Regulatory.

Norbury, M., 2015. Track and the CGT small business concessions. Taxation in

Australia, 49(10), p.622.

Palan, R., Murphy, R. and Chavagneux, C., 2013. Tax havens: How globalization really works.

Cornell University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

References

Althaus, C., Bridgman, P. and Davis, G., 2012. The Australian policy handbook. Allen & Unwin.

Aust, A., 2013. Modern treaty law and practice. Cambridge University Press.

Braithwaite, V., Murphy, K. and Reinhart, M., 2013. Taxation threat, motivational postures, and

responsive regulation. Law & Policy, 29(1), pp.137-158.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax record

data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2), pp.181-205.

Cane, P. and Atiyah, P.S., 2013. Atiyah's accidents, compensation and the law. Cambridge

University Press.

Dabner, J., 2014. Commentary on 108-A of ITAA 1997: CGT asset rules. In Australian Tax

Practice. Thomson Legal and Regulatory.

Norbury, M., 2015. Track and the CGT small business concessions. Taxation in

Australia, 49(10), p.622.

Palan, R., Murphy, R. and Chavagneux, C., 2013. Tax havens: How globalization really works.

Cornell University Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’ view. Procedia-

Social and Behavioral Sciences, 109, pp.1069-1075.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.