TAXATION 11: Detailed Examination of Canadian Federal Taxation System

VerifiedAdded on 2022/09/09

|17

|3463

|24

Report

AI Summary

This report offers a detailed overview of the Canadian federal taxation system, covering key aspects such as income tax, taxable entities, and the federal/provincial system. It examines employment income, including deductions and tax planning strategies, and delves into the calculation of taxable income for individuals. The report explores capital cost allowance, business income, and the assessment of capital gains and losses. It also discusses other income sources, deductions, and special income arrangements like retirement savings, including RRSPs and RRIFs. The report further provides insights into corporate taxation, rollovers, and the decision to incorporate, along with the advantages and disadvantages of incorporating a business. Overall, the report offers a comprehensive analysis of the Canadian tax landscape and provides a valuable resource for understanding the intricacies of the system.

Running head: TAXATION

TAXATION

Name of the Student

Name of the University

Author note

TAXATION

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION

Table of Contents

Chapter 1....................................................................................................................................2

Chapter 2....................................................................................................................................3

Chapter 3....................................................................................................................................4

Chapter 4....................................................................................................................................5

Chapter 5....................................................................................................................................6

Chapter 6....................................................................................................................................6

Chapter 8....................................................................................................................................7

Chapter 9....................................................................................................................................7

Chapter 10..................................................................................................................................8

Chapter 11..................................................................................................................................9

Chapter 14................................................................................................................................10

Chapter 15................................................................................................................................10

Chapter 16................................................................................................................................11

Chapter 17................................................................................................................................12

Chapter 20................................................................................................................................12

Chapter 21................................................................................................................................13

References................................................................................................................................15

TAXATION

Table of Contents

Chapter 1....................................................................................................................................2

Chapter 2....................................................................................................................................3

Chapter 3....................................................................................................................................4

Chapter 4....................................................................................................................................5

Chapter 5....................................................................................................................................6

Chapter 6....................................................................................................................................6

Chapter 8....................................................................................................................................7

Chapter 9....................................................................................................................................7

Chapter 10..................................................................................................................................8

Chapter 11..................................................................................................................................9

Chapter 14................................................................................................................................10

Chapter 15................................................................................................................................10

Chapter 16................................................................................................................................11

Chapter 17................................................................................................................................12

Chapter 20................................................................................................................................12

Chapter 21................................................................................................................................13

References................................................................................................................................15

2

TAXATION

Chapter 1

Introduction to federal taxation in Canada

The entities in Canada is governed by two taxable categories one is taxable entities

under the income tax and the taxable entities under GST. Under the income tax the tax

liability of the individuals, corporations and trusts are assessed on the other hand the under

GST the income tax of individuals, corporations, trusts and others are assessed. Under the

federal system tax is imposed on individuals whose income is $20000 @15% federal tax on

the taxable income plus 7% of provincial tax, and the public corporation will be taxable if its

taxable income exceeds $100000 @15% of federal tax and an additional provincial tax of

11% is charged. The federal taxation system helps in bringing stability in the economic

condition of Canada. The main features of this federal taxation are

Equity; it fails to bring equity as the high-income individuals and the corporations does not

have to pay high amount of tax

Balance between sectors

The taxation system is highly dependent on the personal income tax

Complexity

The taxation system of Canada is very complicated

Dependability of revenues

The revenue generation is highly dependent on the resource sector

International competitiveness

TAXATION

Chapter 1

Introduction to federal taxation in Canada

The entities in Canada is governed by two taxable categories one is taxable entities

under the income tax and the taxable entities under GST. Under the income tax the tax

liability of the individuals, corporations and trusts are assessed on the other hand the under

GST the income tax of individuals, corporations, trusts and others are assessed. Under the

federal system tax is imposed on individuals whose income is $20000 @15% federal tax on

the taxable income plus 7% of provincial tax, and the public corporation will be taxable if its

taxable income exceeds $100000 @15% of federal tax and an additional provincial tax of

11% is charged. The federal taxation system helps in bringing stability in the economic

condition of Canada. The main features of this federal taxation are

Equity; it fails to bring equity as the high-income individuals and the corporations does not

have to pay high amount of tax

Balance between sectors

The taxation system is highly dependent on the personal income tax

Complexity

The taxation system of Canada is very complicated

Dependability of revenues

The revenue generation is highly dependent on the resource sector

International competitiveness

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION

This taxation system is favourable for corporations and not favourable for the individuals in

comparison to the US taxation system. The basic charging provision of the federal taxation

system is ITA 2(1). In Canada individuals are taxed on the basis of their residential status and

not on the basis of their citizenship status.

Chapter 2

Provision and administration

Individuals has to file the form T1 to pay their tax liability the date of submission of

the tax liability are April 30 of the following year, June 15 of the following year and 6

months after date of death if the assesses died before filling the return. the number of returns

filed in the year 2017 is 28.10 million out of which 24.20 million filled their return

electronically and 3.9 million files in paper mode. Individuals can pay their tax liability in

four equal instalments on march 15 June 15 September 15 and December 15. If the assesses

fails to pay their instalments they have to pay interest of 2% and penalty will be imposed if

the instalment amount is excessive.

The corporations have to file their returns in form T2, if the revenue of any particular

corporation exceeds $1 million then such corporation must file their return electronically. The

return of the corporations must be filed within 6 months after the end of the financial year.

The corporation can pay their tax liability on quarterly basis and they also has to pay interest

in case of any default in payment within the due date. For the trusts the returns are to be filled

in form T3 which should be filed within 90 days after December 31. The individuals and

corporations are entitled to get interest on refunds later of 30 days after return is filed and the

balance due date and for corporations later of 120 days after corporation’s year end and

TAXATION

This taxation system is favourable for corporations and not favourable for the individuals in

comparison to the US taxation system. The basic charging provision of the federal taxation

system is ITA 2(1). In Canada individuals are taxed on the basis of their residential status and

not on the basis of their citizenship status.

Chapter 2

Provision and administration

Individuals has to file the form T1 to pay their tax liability the date of submission of

the tax liability are April 30 of the following year, June 15 of the following year and 6

months after date of death if the assesses died before filling the return. the number of returns

filed in the year 2017 is 28.10 million out of which 24.20 million filled their return

electronically and 3.9 million files in paper mode. Individuals can pay their tax liability in

four equal instalments on march 15 June 15 September 15 and December 15. If the assesses

fails to pay their instalments they have to pay interest of 2% and penalty will be imposed if

the instalment amount is excessive.

The corporations have to file their returns in form T2, if the revenue of any particular

corporation exceeds $1 million then such corporation must file their return electronically. The

return of the corporations must be filed within 6 months after the end of the financial year.

The corporation can pay their tax liability on quarterly basis and they also has to pay interest

in case of any default in payment within the due date. For the trusts the returns are to be filled

in form T3 which should be filed within 90 days after December 31. The individuals and

corporations are entitled to get interest on refunds later of 30 days after return is filed and the

balance due date and for corporations later of 120 days after corporation’s year end and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION

30days after return is filed. The assesses can settle their disputes by appealing either in the

federal courts or in the supreme court of Canada.

Chapter 3

Employment income

The employment income is classified under four section of the income tax act these are

Section 5: definitions

Section 6: inclusions

Section 7: stock options

Section 8: deductions

As per the provision of the ITA 5(1) the income of taxpayer from an office or

employment is the wage, salary and other remuneration which also includes gratuities

received by the assesses. The basic form of concession is the salaries and wages, the

legislative guidance includes allowance for personal expense, director’s fees employee

benefit plans and employee trust. The main tax planning strategy that an assesses can make is

to take the advantage of deduction when the salary is accrued and taxed when paid. There are

several allowances using which the tax payer can take the advantage of exemptions from tax

liability which will reduce the amount of their total tax liability. The employees are also

entitled to receive options to purchase shares of the company at a rate which is less than the

market price and can sell the shares at the market price. The deductions are provided

undersection ITA 8(1)(f) which are;

Required to pay expenses

TAXATION

30days after return is filed. The assesses can settle their disputes by appealing either in the

federal courts or in the supreme court of Canada.

Chapter 3

Employment income

The employment income is classified under four section of the income tax act these are

Section 5: definitions

Section 6: inclusions

Section 7: stock options

Section 8: deductions

As per the provision of the ITA 5(1) the income of taxpayer from an office or

employment is the wage, salary and other remuneration which also includes gratuities

received by the assesses. The basic form of concession is the salaries and wages, the

legislative guidance includes allowance for personal expense, director’s fees employee

benefit plans and employee trust. The main tax planning strategy that an assesses can make is

to take the advantage of deduction when the salary is accrued and taxed when paid. There are

several allowances using which the tax payer can take the advantage of exemptions from tax

liability which will reduce the amount of their total tax liability. The employees are also

entitled to receive options to purchase shares of the company at a rate which is less than the

market price and can sell the shares at the market price. The deductions are provided

undersection ITA 8(1)(f) which are;

Required to pay expenses

5

TAXATION

Required to work away from office

Made partial payment by commissions

Have to sign form T2200.

Chapter 4

Taxable income and tax payable for individuals

The taxable income is calculated in the following way

Employment income + business and property income + net taxable capital gains +other

sources of income – other deductions from income – division C deductions = taxable income.

The available deductions are employee stock options, deductions for payments, lump sum

payments, life time capital gains deductions, northern resident deductions and loss carry

overs. The basic system of the calculation of the taxable liability of an individual are stated

below

Tax on first $93208 $16544

Tax on next $6792($100000-93208) 1766

Total federal tax 18310

Basic personal credit (1771)

Federal tax payable 16539

All the provinces in Canada should apply progressive rates to taxable income. The

assesses are allowed to get refunds if their total tax payment exceeds the tax liability. The tax

credit system has the following features which explains the amount that can be refunded and

TAXATION

Required to work away from office

Made partial payment by commissions

Have to sign form T2200.

Chapter 4

Taxable income and tax payable for individuals

The taxable income is calculated in the following way

Employment income + business and property income + net taxable capital gains +other

sources of income – other deductions from income – division C deductions = taxable income.

The available deductions are employee stock options, deductions for payments, lump sum

payments, life time capital gains deductions, northern resident deductions and loss carry

overs. The basic system of the calculation of the taxable liability of an individual are stated

below

Tax on first $93208 $16544

Tax on next $6792($100000-93208) 1766

Total federal tax 18310

Basic personal credit (1771)

Federal tax payable 16539

All the provinces in Canada should apply progressive rates to taxable income. The

assesses are allowed to get refunds if their total tax payment exceeds the tax liability. The tax

credit system has the following features which explains the amount that can be refunded and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION

what cannot be which credits have income threshold and all the provinces have similar credit

facilities. The refundable credits will be paid to the tax payer, irrespective of the fact that the

individual has tax payable balance.

Chapter 5

Capital cost allowance

The general rules of the capital cost allowance are that it is applicable for capital

assets only, in addition to that the government assistance, non arm’s length transactions and

GST / HST / PST considerations are also required to be considered for assessing the capital

cost allowance. The assets that are eligible for capital cost allowance are divided into various

classes these are class 1, class3, class 8, class 10, class 10.1, class 12, class 13, class 14, class

14.1 manufacturing and processing assets, class 44 and class 50. The capital cost allowance

can be used as a major tax planning strategy as it entitles the assesses to claim deduction from

the net income. Under the separate class election, the eligible assets are photocopiers,

electronic communications equipment and some computer software these are some of the

assets which are included for calculation of the capital assets and are eligible for claiming

deduction.

Chapter 6

Income or loss from a business

The business income or loss is calculated on the basis of certain items that are

considered as the main source of income and from such income some specific expenditures

are allowed for deductions from which it will be possible to assess the net income or loss.

The business income is defined under ITA 248 which includes income from profession,

calling, trade, manufacture or any kind of undertaking. On e of the major rule of the business

TAXATION

what cannot be which credits have income threshold and all the provinces have similar credit

facilities. The refundable credits will be paid to the tax payer, irrespective of the fact that the

individual has tax payable balance.

Chapter 5

Capital cost allowance

The general rules of the capital cost allowance are that it is applicable for capital

assets only, in addition to that the government assistance, non arm’s length transactions and

GST / HST / PST considerations are also required to be considered for assessing the capital

cost allowance. The assets that are eligible for capital cost allowance are divided into various

classes these are class 1, class3, class 8, class 10, class 10.1, class 12, class 13, class 14, class

14.1 manufacturing and processing assets, class 44 and class 50. The capital cost allowance

can be used as a major tax planning strategy as it entitles the assesses to claim deduction from

the net income. Under the separate class election, the eligible assets are photocopiers,

electronic communications equipment and some computer software these are some of the

assets which are included for calculation of the capital assets and are eligible for claiming

deduction.

Chapter 6

Income or loss from a business

The business income or loss is calculated on the basis of certain items that are

considered as the main source of income and from such income some specific expenditures

are allowed for deductions from which it will be possible to assess the net income or loss.

The business income is defined under ITA 248 which includes income from profession,

calling, trade, manufacture or any kind of undertaking. On e of the major rule of the business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION

income is that it can not be adjusted with the capital gains or loss business income for

corporations are allowed to get small business deductions. The main difference between a

capital asset and a business asset are its intent the other considerations are length of

ownership period nature of assets, objectives in articles of incorporation, supplemental work

on property. The business income is assessed on the basis of the principles of GAAP which

includes the accrual basis and the net concept basis. The taxation year for the assessment of

the business income are nay period that does not exceed 53 weeks and for unincorporated

businesses is generally used calendar year.

Chapter 8

Capital gains and capital losses

The capital gains and losses are assessed on the capital assets the types of loss that can

be adjusted with the capital gains are discussed below:

Adjustment for Net capital loss with net capital gain

This type of loss can be carried back for 3 years and carried forward indefinitely, this

can be adjusted with the taxable gains in the financial year. The farm loss can be carried back

for 3 years and for a loss that is incurred after 2005 which can be carried forward for 20

years. For a loss incurred before 2006 and can be carried forward for 10 years. Listed

personal property loss, this kind of loss can be carried back for 3 years and can be carried

forward for 7 years this can be adjusted to net gains from listed personal property loss in the

current fiscal year. The loss from restricted personal property is not allowed to be carried

back or carried forward and it is not allowed for adjustment with capital gains.

Chapter 9

Other income other deductions and other issues

TAXATION

income is that it can not be adjusted with the capital gains or loss business income for

corporations are allowed to get small business deductions. The main difference between a

capital asset and a business asset are its intent the other considerations are length of

ownership period nature of assets, objectives in articles of incorporation, supplemental work

on property. The business income is assessed on the basis of the principles of GAAP which

includes the accrual basis and the net concept basis. The taxation year for the assessment of

the business income are nay period that does not exceed 53 weeks and for unincorporated

businesses is generally used calendar year.

Chapter 8

Capital gains and capital losses

The capital gains and losses are assessed on the capital assets the types of loss that can

be adjusted with the capital gains are discussed below:

Adjustment for Net capital loss with net capital gain

This type of loss can be carried back for 3 years and carried forward indefinitely, this

can be adjusted with the taxable gains in the financial year. The farm loss can be carried back

for 3 years and for a loss that is incurred after 2005 which can be carried forward for 20

years. For a loss incurred before 2006 and can be carried forward for 10 years. Listed

personal property loss, this kind of loss can be carried back for 3 years and can be carried

forward for 7 years this can be adjusted to net gains from listed personal property loss in the

current fiscal year. The loss from restricted personal property is not allowed to be carried

back or carried forward and it is not allowed for adjustment with capital gains.

Chapter 9

Other income other deductions and other issues

8

TAXATION

The other income of the individuals includes the pensions benefits under ITA 56(1)(a)

(i) retiring allowances under section ITA 56(1)(a)(ii) and the death benefits. The other

income also includes the income generated from RRSP’S, DPSP’S AND RRIF withdrawals.

In addition to that if an individual receive scholarship that will be assessed under the other

income which does not include post doc fellowship if part time scholarship is received.

Research grants are also included in the income of the individual. The net income is also

including worker’s compensation. The CPP contributions are allowed for deductions the self

employed are required to pay both halves of CPP for claiming deductions. Moving expenses

are also allowed for deductions the moving expenses are travel costs taxpayer and family,

moving household effects and lease cancelation costs. Meal expense of $51 per person per

day are allowed for deduction and mileage expense which varies as per different province.

Chapter 10

Retirement savings and other special income arrangements

The main tools for retirement savings are registered retirement savings plan

Registered pension plans for employees only

Funds that are registered for retirement income.

Pooled registered pensions plans.

Individual pension plans.

Tax free savings account

For retirement benefits is advised to the individuals to make contribution in the

retirement funds as early as possible which will help to generate an extra 10 percent in the

plan. The tax savings is dependent on the bracket of the individual at retirement versus the

TAXATION

The other income of the individuals includes the pensions benefits under ITA 56(1)(a)

(i) retiring allowances under section ITA 56(1)(a)(ii) and the death benefits. The other

income also includes the income generated from RRSP’S, DPSP’S AND RRIF withdrawals.

In addition to that if an individual receive scholarship that will be assessed under the other

income which does not include post doc fellowship if part time scholarship is received.

Research grants are also included in the income of the individual. The net income is also

including worker’s compensation. The CPP contributions are allowed for deductions the self

employed are required to pay both halves of CPP for claiming deductions. Moving expenses

are also allowed for deductions the moving expenses are travel costs taxpayer and family,

moving household effects and lease cancelation costs. Meal expense of $51 per person per

day are allowed for deduction and mileage expense which varies as per different province.

Chapter 10

Retirement savings and other special income arrangements

The main tools for retirement savings are registered retirement savings plan

Registered pension plans for employees only

Funds that are registered for retirement income.

Pooled registered pensions plans.

Individual pension plans.

Tax free savings account

For retirement benefits is advised to the individuals to make contribution in the

retirement funds as early as possible which will help to generate an extra 10 percent in the

plan. The tax savings is dependent on the bracket of the individual at retirement versus the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

TAXATION

bracket of contribution made by him. The options that are available to the individual at the

time of retirement is to withdraw the fund at the age of 71 and transfer a portion of the fund

to the RRIF. It is often observed that the individuals fail to save for retirement for them the

proposed solution is to make a pool of RPP and should give more emphasis on disciplined

savings.

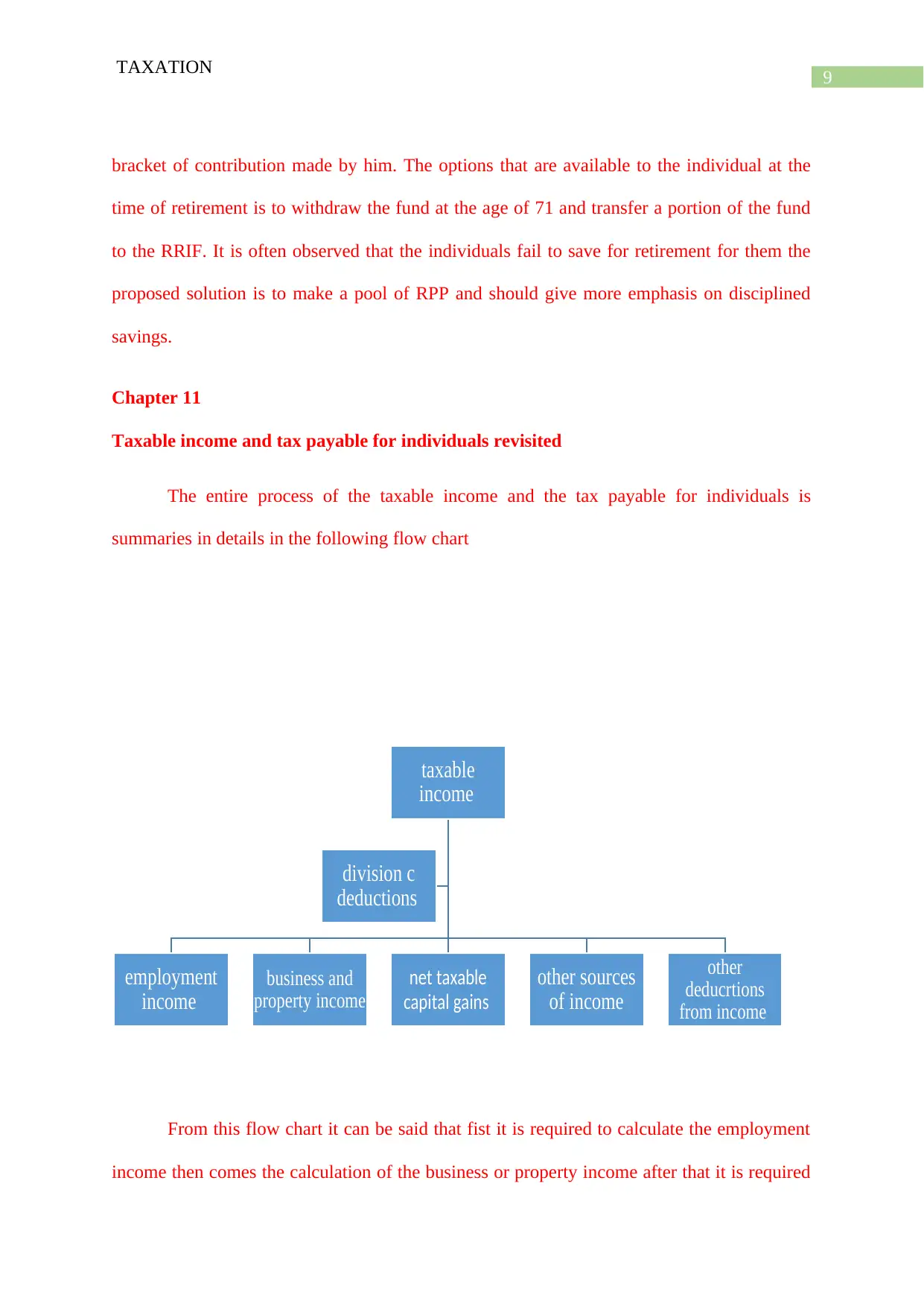

Chapter 11

Taxable income and tax payable for individuals revisited

The entire process of the taxable income and the tax payable for individuals is

summaries in details in the following flow chart

From this flow chart it can be said that fist it is required to calculate the employment

income then comes the calculation of the business or property income after that it is required

taxable

income

employment

income

business and

property income

net taxable

capital gains

other sources

of income

other

deducrtions

from income

division c

deductions

TAXATION

bracket of contribution made by him. The options that are available to the individual at the

time of retirement is to withdraw the fund at the age of 71 and transfer a portion of the fund

to the RRIF. It is often observed that the individuals fail to save for retirement for them the

proposed solution is to make a pool of RPP and should give more emphasis on disciplined

savings.

Chapter 11

Taxable income and tax payable for individuals revisited

The entire process of the taxable income and the tax payable for individuals is

summaries in details in the following flow chart

From this flow chart it can be said that fist it is required to calculate the employment

income then comes the calculation of the business or property income after that it is required

taxable

income

employment

income

business and

property income

net taxable

capital gains

other sources

of income

other

deducrtions

from income

division c

deductions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION

to calculate the capital gains after that the other source of income is calculated adding these

incomes the total income is calculated from which the other deductions are adjusted, after

that division C deductions are made and after that in the final stage the taxable income will be

assessed. All the incomes are to be classified under the proper headings and the losses are to

be adjusted with the appropriate gains. Only then it will be possible to make proper

assessment of the taxable income and on the taxable income after charging the federal taxes

and the provincial taxes the tax liability will be calculated.

Chapter 14

Other issue in corporate taxation

The other issues in the corporate taxation includes the acquisition of control the

common scenarios that are observed are, through acquisition in which one person acquires

most of the portion of a corporation’s common shares from a person who has arms length

transactions with that particular organisation. this can also occur through the redemption of

shares. The deemed year of such transaction is June 30 of any financial year. Under this

provision a related person includes parents and grandparents, a taxpayer’s spouse or in law

parents, siblings of the individual who is liable to pay tax, children which also includes

adopted children and related corporations means a corporation which is related with a person

who has the controlling power of such organisation. the association rules are provided under

the provision of then ITA 268(1)(a), 268(1)(b),268(1)(c), 268(1)(d) and 268(1)(e). Further the

credit that the taxpayer gets during a current financial year is added back in the following

year.

Chapter 15

Corporate taxation and management decisions

TAXATION

to calculate the capital gains after that the other source of income is calculated adding these

incomes the total income is calculated from which the other deductions are adjusted, after

that division C deductions are made and after that in the final stage the taxable income will be

assessed. All the incomes are to be classified under the proper headings and the losses are to

be adjusted with the appropriate gains. Only then it will be possible to make proper

assessment of the taxable income and on the taxable income after charging the federal taxes

and the provincial taxes the tax liability will be calculated.

Chapter 14

Other issue in corporate taxation

The other issues in the corporate taxation includes the acquisition of control the

common scenarios that are observed are, through acquisition in which one person acquires

most of the portion of a corporation’s common shares from a person who has arms length

transactions with that particular organisation. this can also occur through the redemption of

shares. The deemed year of such transaction is June 30 of any financial year. Under this

provision a related person includes parents and grandparents, a taxpayer’s spouse or in law

parents, siblings of the individual who is liable to pay tax, children which also includes

adopted children and related corporations means a corporation which is related with a person

who has the controlling power of such organisation. the association rules are provided under

the provision of then ITA 268(1)(a), 268(1)(b),268(1)(c), 268(1)(d) and 268(1)(e). Further the

credit that the taxpayer gets during a current financial year is added back in the following

year.

Chapter 15

Corporate taxation and management decisions

11

TAXATION

The corporate taxation and management decisions are made with the object to reduce

the burden of tax, deferring tax, splitting of income and other considerations. The

disadvantages of the taxation system are that the loss deductions can not be used, the tax

credits can not be used, charitable donations are not allowed for deductions, cost of

maintaining corporations and winding up procedures are very complicated. Tax deferrals are

allowed for CCPC investment income and eligible income subject to pat IV. One of the

benefits is that no taxes are required to pay for dividend income. The corporates should take

the advantage of the alternative minimum tax. The income splitting strategy can be used for

reducing the tax burden which is often used by the corporates to avail the benefits of tax

exemptions. The tax effective solutions that are available to the management are RPP, DPSP,

private health care and the stock option schemes these are some of the sources from which

the assesses can avail deductions.

Chapter 16

Rollover under section 85

The standard section for the rollover is the section 85, some of the examples of the

transfer of property at tax values are inter Vivos to a spouse, to a spouse at death, to a

corporation at elected values. The transfers can be made by the individuals, trusts and

corporations under the provision of the section ITA 85(1). The type of corporation that can

make such transfer are the Canadian resident, and any corporation that is situated in Canada.

The types of property that are eligible for transfer of property are, capital property, Canadian

property, foreign resource properties, inventories, and real estates. The related person can get

several benefits under the provisions of ITA 85(1)(e.2) and the transferor shareholder also

enjoys benefits under the provision of ITA 15(1) of this rule. The corporation can avail the

TAXATION

The corporate taxation and management decisions are made with the object to reduce

the burden of tax, deferring tax, splitting of income and other considerations. The

disadvantages of the taxation system are that the loss deductions can not be used, the tax

credits can not be used, charitable donations are not allowed for deductions, cost of

maintaining corporations and winding up procedures are very complicated. Tax deferrals are

allowed for CCPC investment income and eligible income subject to pat IV. One of the

benefits is that no taxes are required to pay for dividend income. The corporates should take

the advantage of the alternative minimum tax. The income splitting strategy can be used for

reducing the tax burden which is often used by the corporates to avail the benefits of tax

exemptions. The tax effective solutions that are available to the management are RPP, DPSP,

private health care and the stock option schemes these are some of the sources from which

the assesses can avail deductions.

Chapter 16

Rollover under section 85

The standard section for the rollover is the section 85, some of the examples of the

transfer of property at tax values are inter Vivos to a spouse, to a spouse at death, to a

corporation at elected values. The transfers can be made by the individuals, trusts and

corporations under the provision of the section ITA 85(1). The type of corporation that can

make such transfer are the Canadian resident, and any corporation that is situated in Canada.

The types of property that are eligible for transfer of property are, capital property, Canadian

property, foreign resource properties, inventories, and real estates. The related person can get

several benefits under the provisions of ITA 85(1)(e.2) and the transferor shareholder also

enjoys benefits under the provision of ITA 15(1) of this rule. The corporation can avail the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.