Taxation Report: Analysis of Australian Taxation and Deductions

VerifiedAdded on 2020/12/24

|7

|1865

|482

Report

AI Summary

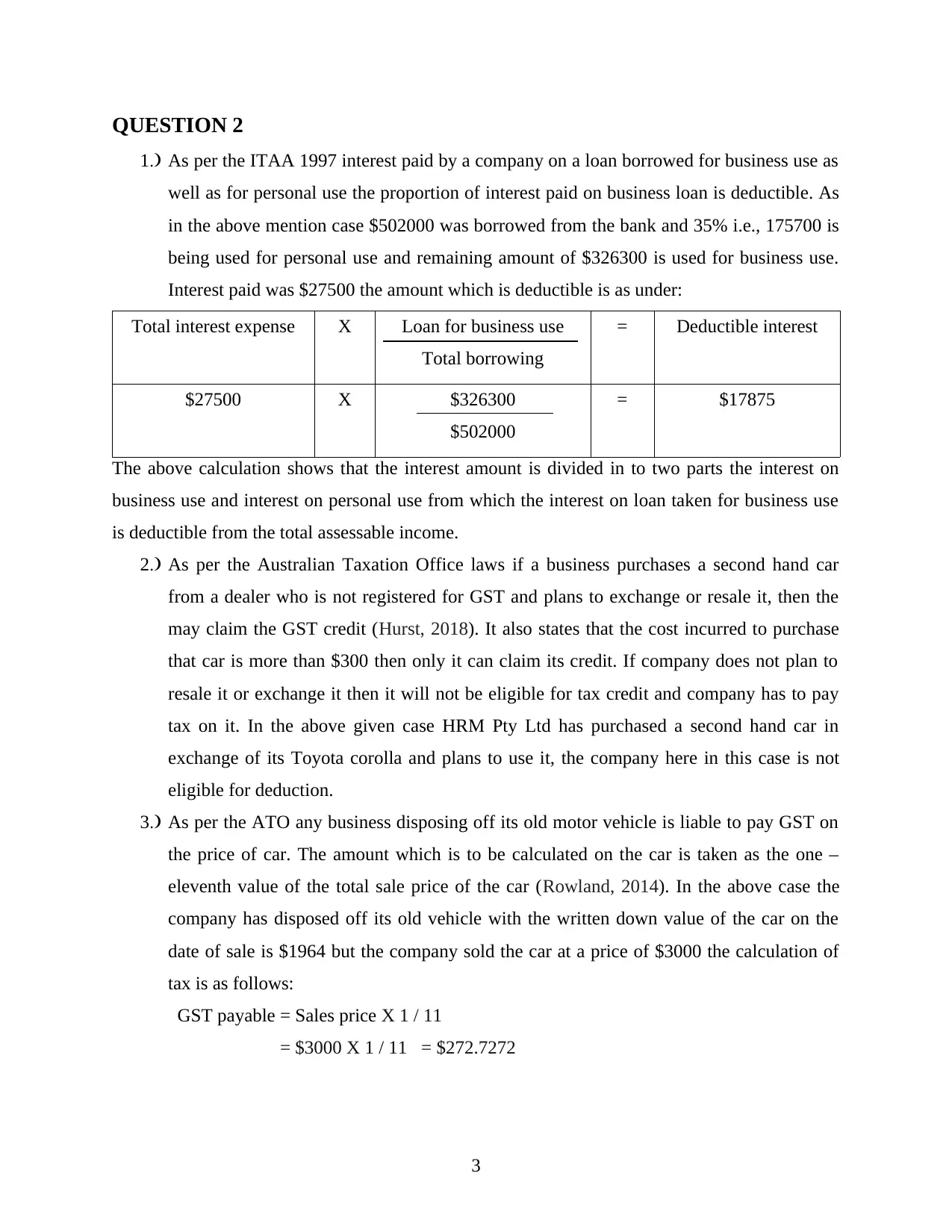

This report provides a comprehensive analysis of taxation principles, focusing on assessable income, deductions, and relevant tax laws in Australia. It begins with an introduction to taxation as a primary revenue source for governments and outlines the structure of the report. The report examines assessable income, as defined by the Income Tax Assessment Act 1997, including compensation payments and other income sources. It also covers allowable deductions, such as repairs and interest on business loans, referencing specific sections of the ITAA 1997. The report includes calculations for deductible interest and GST payable on disposed vehicles, as well as the deductibility of wages, salaries, and donations. It also addresses the recognition of inventories and the carry-forward of losses. The report concludes with a summary of the key concepts and their implications for businesses, referencing relevant books, journals, and online resources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.