Assessment of Taxation Theory, Practice, and Law Principles

VerifiedAdded on 2022/11/13

|10

|3074

|447

Report

AI Summary

This report provides a comprehensive analysis of taxation principles, focusing on capital gains tax, income from personal exertion, and assessable income. The report addresses three key questions. The first question involves the calculation of net capital loss or gain for Helen, considering various transactions and the application of the indexation method for assets acquired before September 21, 1999. The second question examines the concept of personal exertion income, using case studies to illustrate how income earned from personal skills and experiences is classified. The third question discusses the treatment of assessable income, specifically addressing the tax implications of financial assistance provided as a loan from a parent to a child. The report concludes with a summary of the key findings and their implications within the context of Australian taxation law.

Taxation theory, Practice

and Law

1

and Law

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents......................................................................................................................................2

INTRODUCTION.........................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................6

Question 3...............................................................................................................................7

CONCLUSION............................................................................................................................9

REFERENCES..........................................................................................................................10

2

Contents......................................................................................................................................2

INTRODUCTION.........................................................................................................................3

Question 1...............................................................................................................................3

Question 2...............................................................................................................................6

Question 3...............................................................................................................................7

CONCLUSION............................................................................................................................9

REFERENCES..........................................................................................................................10

2

INTRODUCTION

Any income generated by an individual from the business or sales of capital goods is liable to

pay income tax to the taxation authority in the assessment year. This report is made upon the

taxation, theory and practice related provisions. It consists of three questions which are

related to capital gain tax, income from personal exertion, and income tax. In the first question

there are several transactions done by Helen, which shows capital gain or loss. While the

second question mention about income from personal exertion of Barbara. Third question

emphasis upon the treatment of assessable income of Mr Patrick.

Question 1

Calculation of net capital loss or gain of Helen for the assessment year

Capital gain tax is levied on the capital assets which are sold during the current assessment

year. Thus, capital gain will exist only if selling price is higher than the buying cost ( Goldin,

2015). Here in the given case, if Helen sold out its purchased asset in current year itself and

receive capital gain then Helen have to pay tax on the profit received by selling out its assets.

Similarly in case if Helen suffer from capital loss by selling out assets then such loss will be

moved forward and will be set off with future capital gain which Helen will receive. So

according to question it can be seen that Helen its assets in current year itself and which has

resulted in the form of capital gain to Helen (Woellner, et. al., 2014). Thus, in this case Helen

will be entitled to pay upon capital gain which she received from selling out assets in current

year itself. The main reason behind this is that separate provision in respect of capital gain is

being maintained as per ATA (Australian tax authority). Moreover, capital gain also leads in

shifting of tax burden upon assessee or a tax payer. According to Australian income tax

authority department after 20th September 1985 those assets which are acquired will be

considered under capital gain tax regime. Furthermore, specific rate is not being specified by

Australian income tax authority department upon capital gain (Brabazon, 2019). But side by

side in case if a tax payer retain assets for more than 12 months or for 12 months the

assessee will be lived to pay tax up to 23.5%. In addition to this if discount is being availed by

tax payer then also a tax payer will be liable to pay up to 23.5% tax. Whereas for those

assessee who retain assets before 21st September 1999 are not liable to for such type of 50%

discount facility upon taxable income. If an assessee purchase asset before aforementioned

date then in that case instead of discounted method indexation method is being applied. For

the purpose of calculating the capital gain/loss also both the discounted and indexation

method is being used and this take place only if an assessee will make purchase of an asset

before 21st September 1999. Similarly if an assessee hold out assets for a very long time

period (12 or more than 12 months) the none of the discounted and indexation will be applied

(Auerbach and Hassett, 2015). But here in this question an asset are being made purchased

before 21st September 1999, so in order to calculate capital gain/loss indexation method will

be used not the discounted method. Therefore elaboration of indexation method is being done

below:

Indexation method: Acquired assets value could be easily calculated by an assessee using

indexation method. Beside this, purchase cost value can also be easily examined with the

help of this method. In addition to this, only indexation method can be used if a CGT event

happened to an asset acquired by an assessee before 21st September 1999 and discount

3

Any income generated by an individual from the business or sales of capital goods is liable to

pay income tax to the taxation authority in the assessment year. This report is made upon the

taxation, theory and practice related provisions. It consists of three questions which are

related to capital gain tax, income from personal exertion, and income tax. In the first question

there are several transactions done by Helen, which shows capital gain or loss. While the

second question mention about income from personal exertion of Barbara. Third question

emphasis upon the treatment of assessable income of Mr Patrick.

Question 1

Calculation of net capital loss or gain of Helen for the assessment year

Capital gain tax is levied on the capital assets which are sold during the current assessment

year. Thus, capital gain will exist only if selling price is higher than the buying cost ( Goldin,

2015). Here in the given case, if Helen sold out its purchased asset in current year itself and

receive capital gain then Helen have to pay tax on the profit received by selling out its assets.

Similarly in case if Helen suffer from capital loss by selling out assets then such loss will be

moved forward and will be set off with future capital gain which Helen will receive. So

according to question it can be seen that Helen its assets in current year itself and which has

resulted in the form of capital gain to Helen (Woellner, et. al., 2014). Thus, in this case Helen

will be entitled to pay upon capital gain which she received from selling out assets in current

year itself. The main reason behind this is that separate provision in respect of capital gain is

being maintained as per ATA (Australian tax authority). Moreover, capital gain also leads in

shifting of tax burden upon assessee or a tax payer. According to Australian income tax

authority department after 20th September 1985 those assets which are acquired will be

considered under capital gain tax regime. Furthermore, specific rate is not being specified by

Australian income tax authority department upon capital gain (Brabazon, 2019). But side by

side in case if a tax payer retain assets for more than 12 months or for 12 months the

assessee will be lived to pay tax up to 23.5%. In addition to this if discount is being availed by

tax payer then also a tax payer will be liable to pay up to 23.5% tax. Whereas for those

assessee who retain assets before 21st September 1999 are not liable to for such type of 50%

discount facility upon taxable income. If an assessee purchase asset before aforementioned

date then in that case instead of discounted method indexation method is being applied. For

the purpose of calculating the capital gain/loss also both the discounted and indexation

method is being used and this take place only if an assessee will make purchase of an asset

before 21st September 1999. Similarly if an assessee hold out assets for a very long time

period (12 or more than 12 months) the none of the discounted and indexation will be applied

(Auerbach and Hassett, 2015). But here in this question an asset are being made purchased

before 21st September 1999, so in order to calculate capital gain/loss indexation method will

be used not the discounted method. Therefore elaboration of indexation method is being done

below:

Indexation method: Acquired assets value could be easily calculated by an assessee using

indexation method. Beside this, purchase cost value can also be easily examined with the

help of this method. In addition to this, only indexation method can be used if a CGT event

happened to an asset acquired by an assessee before 21st September 1999 and discount

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

method cannot use (Evans, Minas, and Lim, 2015). Any asset purchased after 21st September

1999 and asset hold for 12 months or more then discount and indexation method both can

use and assessee can chose nay of them which render could help to impose low tax.

Therefore, by dividing the CPI for quarter in which expenditure are being incurred, indexation

factors can be easily calculated.

Each transaction of Helen is being briefly explained below:

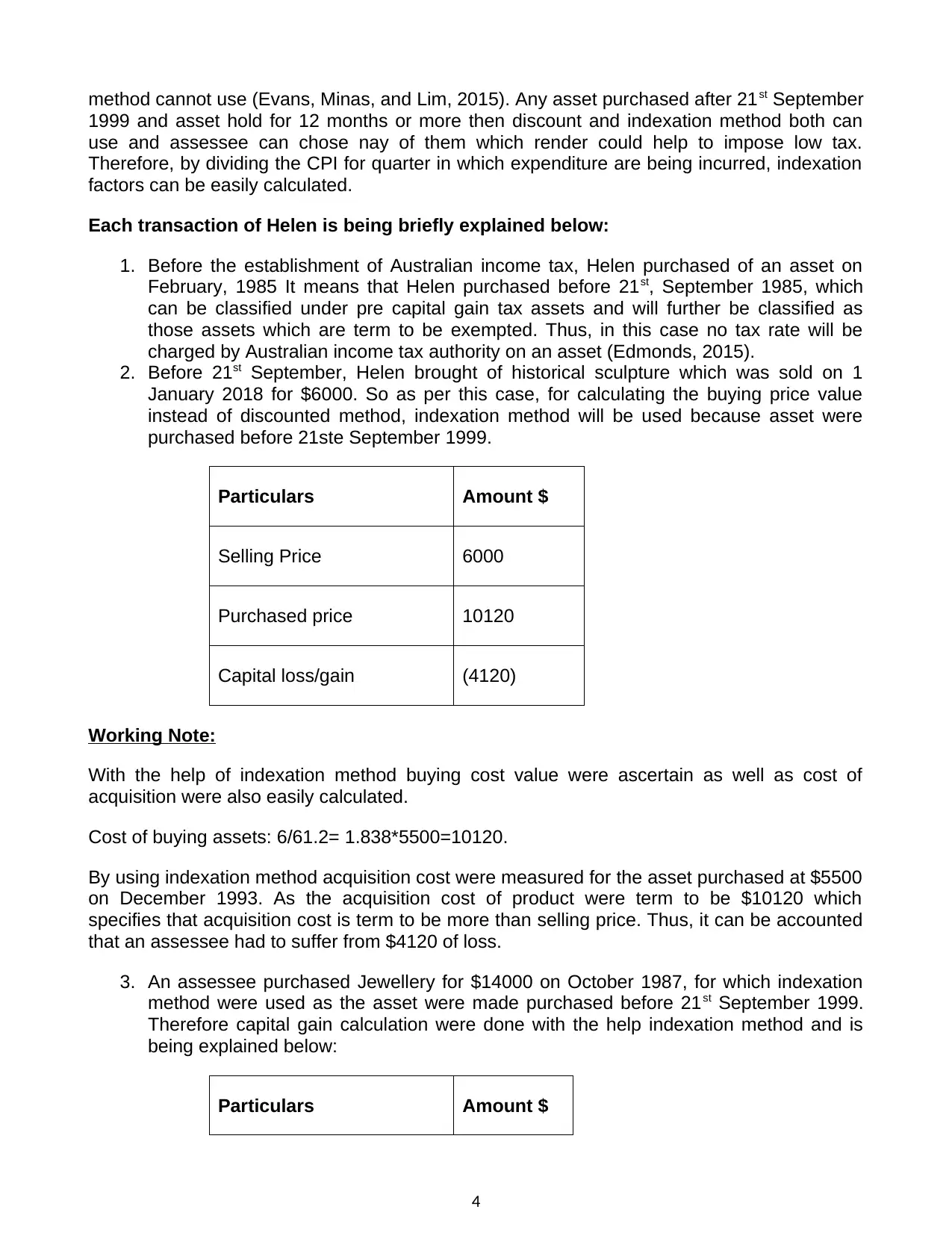

1. Before the establishment of Australian income tax, Helen purchased of an asset on

February, 1985 It means that Helen purchased before 21st, September 1985, which

can be classified under pre capital gain tax assets and will further be classified as

those assets which are term to be exempted. Thus, in this case no tax rate will be

charged by Australian income tax authority on an asset (Edmonds, 2015).

2. Before 21st September, Helen brought of historical sculpture which was sold on 1

January 2018 for $6000. So as per this case, for calculating the buying price value

instead of discounted method, indexation method will be used because asset were

purchased before 21ste September 1999.

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

With the help of indexation method buying cost value were ascertain as well as cost of

acquisition were also easily calculated.

Cost of buying assets: 6/61.2= 1.838*5500=10120.

By using indexation method acquisition cost were measured for the asset purchased at $5500

on December 1993. As the acquisition cost of product were term to be $10120 which

specifies that acquisition cost is term to be more than selling price. Thus, it can be accounted

that an assessee had to suffer from $4120 of loss.

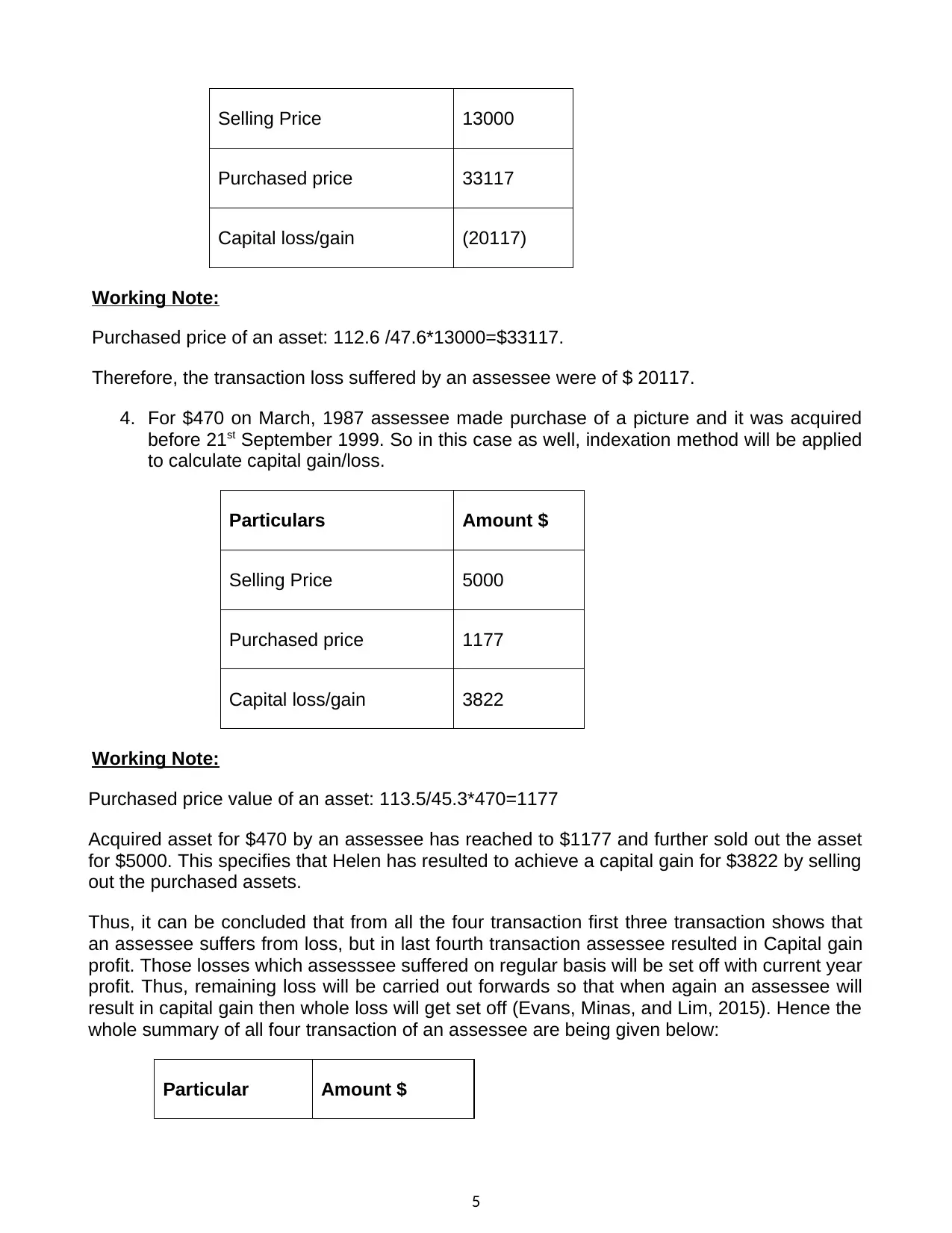

3. An assessee purchased Jewellery for $14000 on October 1987, for which indexation

method were used as the asset were made purchased before 21st September 1999.

Therefore capital gain calculation were done with the help indexation method and is

being explained below:

Particulars Amount $

4

1999 and asset hold for 12 months or more then discount and indexation method both can

use and assessee can chose nay of them which render could help to impose low tax.

Therefore, by dividing the CPI for quarter in which expenditure are being incurred, indexation

factors can be easily calculated.

Each transaction of Helen is being briefly explained below:

1. Before the establishment of Australian income tax, Helen purchased of an asset on

February, 1985 It means that Helen purchased before 21st, September 1985, which

can be classified under pre capital gain tax assets and will further be classified as

those assets which are term to be exempted. Thus, in this case no tax rate will be

charged by Australian income tax authority on an asset (Edmonds, 2015).

2. Before 21st September, Helen brought of historical sculpture which was sold on 1

January 2018 for $6000. So as per this case, for calculating the buying price value

instead of discounted method, indexation method will be used because asset were

purchased before 21ste September 1999.

Particulars Amount $

Selling Price 6000

Purchased price 10120

Capital loss/gain (4120)

Working Note:

With the help of indexation method buying cost value were ascertain as well as cost of

acquisition were also easily calculated.

Cost of buying assets: 6/61.2= 1.838*5500=10120.

By using indexation method acquisition cost were measured for the asset purchased at $5500

on December 1993. As the acquisition cost of product were term to be $10120 which

specifies that acquisition cost is term to be more than selling price. Thus, it can be accounted

that an assessee had to suffer from $4120 of loss.

3. An assessee purchased Jewellery for $14000 on October 1987, for which indexation

method were used as the asset were made purchased before 21st September 1999.

Therefore capital gain calculation were done with the help indexation method and is

being explained below:

Particulars Amount $

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Selling Price 13000

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Purchased price of an asset: 112.6 /47.6*13000=$33117.

Therefore, the transaction loss suffered by an assessee were of $ 20117.

4. For $470 on March, 1987 assessee made purchase of a picture and it was acquired

before 21st September 1999. So in this case as well, indexation method will be applied

to calculate capital gain/loss.

Particulars Amount $

Selling Price 5000

Purchased price 1177

Capital loss/gain 3822

Working Note:

Purchased price value of an asset: 113.5/45.3*470=1177

Acquired asset for $470 by an assessee has reached to $1177 and further sold out the asset

for $5000. This specifies that Helen has resulted to achieve a capital gain for $3822 by selling

out the purchased assets.

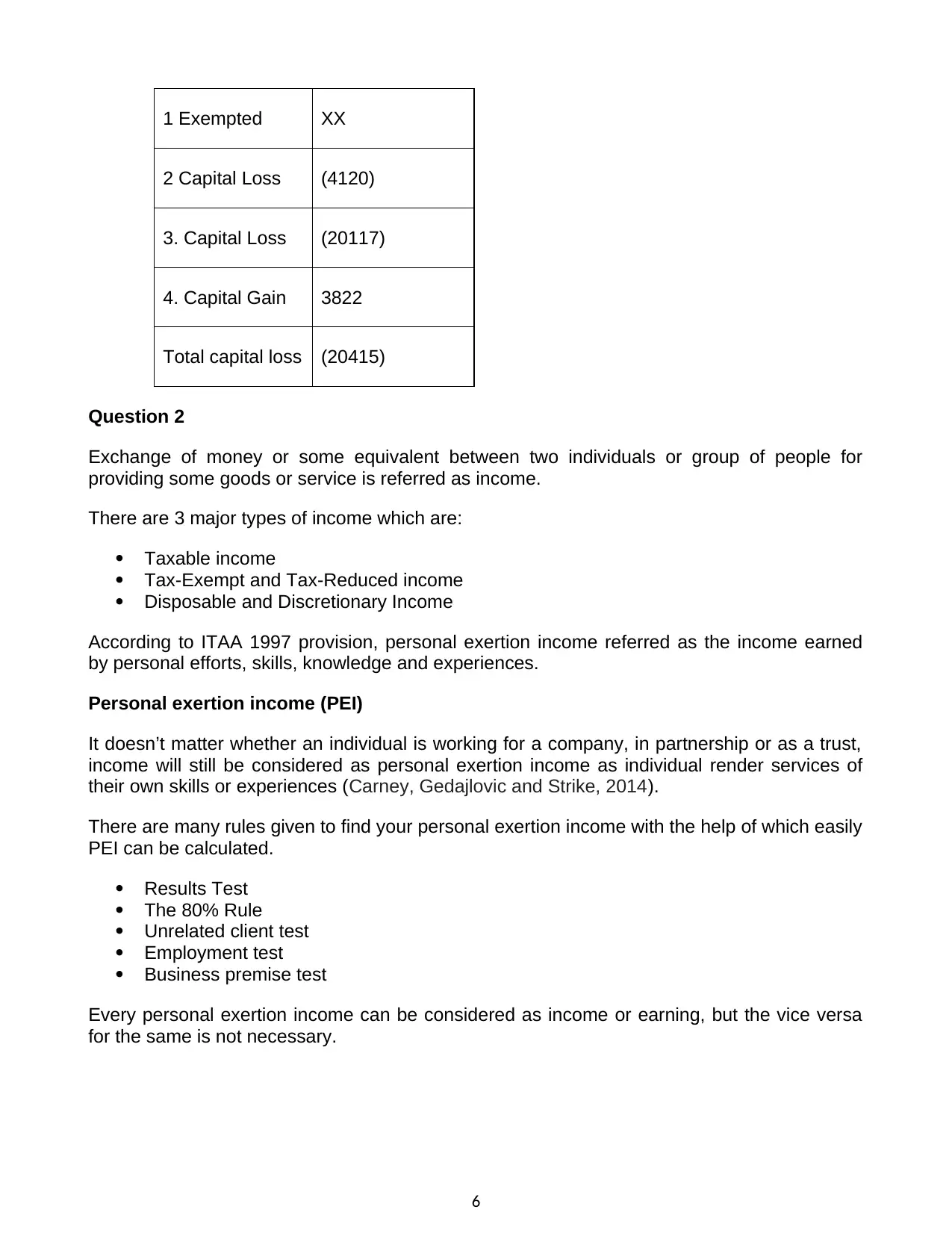

Thus, it can be concluded that from all the four transaction first three transaction shows that

an assessee suffers from loss, but in last fourth transaction assessee resulted in Capital gain

profit. Those losses which assesssee suffered on regular basis will be set off with current year

profit. Thus, remaining loss will be carried out forwards so that when again an assessee will

result in capital gain then whole loss will get set off (Evans, Minas, and Lim, 2015). Hence the

whole summary of all four transaction of an assessee are being given below:

Particular Amount $

5

Purchased price 33117

Capital loss/gain (20117)

Working Note:

Purchased price of an asset: 112.6 /47.6*13000=$33117.

Therefore, the transaction loss suffered by an assessee were of $ 20117.

4. For $470 on March, 1987 assessee made purchase of a picture and it was acquired

before 21st September 1999. So in this case as well, indexation method will be applied

to calculate capital gain/loss.

Particulars Amount $

Selling Price 5000

Purchased price 1177

Capital loss/gain 3822

Working Note:

Purchased price value of an asset: 113.5/45.3*470=1177

Acquired asset for $470 by an assessee has reached to $1177 and further sold out the asset

for $5000. This specifies that Helen has resulted to achieve a capital gain for $3822 by selling

out the purchased assets.

Thus, it can be concluded that from all the four transaction first three transaction shows that

an assessee suffers from loss, but in last fourth transaction assessee resulted in Capital gain

profit. Those losses which assesssee suffered on regular basis will be set off with current year

profit. Thus, remaining loss will be carried out forwards so that when again an assessee will

result in capital gain then whole loss will get set off (Evans, Minas, and Lim, 2015). Hence the

whole summary of all four transaction of an assessee are being given below:

Particular Amount $

5

1 Exempted XX

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

Exchange of money or some equivalent between two individuals or group of people for

providing some goods or service is referred as income.

There are 3 major types of income which are:

Taxable income

Tax-Exempt and Tax-Reduced income

Disposable and Discretionary Income

According to ITAA 1997 provision, personal exertion income referred as the income earned

by personal efforts, skills, knowledge and experiences.

Personal exertion income (PEI)

It doesn’t matter whether an individual is working for a company, in partnership or as a trust,

income will still be considered as personal exertion income as individual render services of

their own skills or experiences (Carney, Gedajlovic and Strike, 2014).

There are many rules given to find your personal exertion income with the help of which easily

PEI can be calculated.

Results Test

The 80% Rule

Unrelated client test

Employment test

Business premise test

Every personal exertion income can be considered as income or earning, but the vice versa

for the same is not necessary.

6

2 Capital Loss (4120)

3. Capital Loss (20117)

4. Capital Gain 3822

Total capital loss (20415)

Question 2

Exchange of money or some equivalent between two individuals or group of people for

providing some goods or service is referred as income.

There are 3 major types of income which are:

Taxable income

Tax-Exempt and Tax-Reduced income

Disposable and Discretionary Income

According to ITAA 1997 provision, personal exertion income referred as the income earned

by personal efforts, skills, knowledge and experiences.

Personal exertion income (PEI)

It doesn’t matter whether an individual is working for a company, in partnership or as a trust,

income will still be considered as personal exertion income as individual render services of

their own skills or experiences (Carney, Gedajlovic and Strike, 2014).

There are many rules given to find your personal exertion income with the help of which easily

PEI can be calculated.

Results Test

The 80% Rule

Unrelated client test

Employment test

Business premise test

Every personal exertion income can be considered as income or earning, but the vice versa

for the same is not necessary.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASE 1

As per the case study of ‘Brent v FCT(1971) 125 CLR 418’ (Snape,2015) in which writer sold

copyright of his book named ‘Husband story of life’ to a newspaper agency. So the money

earned by the writer can be referred as personal exertion income because the book was

written by his own knowledge and experiences which does not involve any other individual or

group as a part of this book (Braunerhjelm and Eklund, 2014). So similarly the amount

earned i.e. $13,400 by writing books is definitely considered as personal exertion income.

Barbara writer of a book named as ‘Economics Principles’ sold his book to Eco Books Ltd

library for which she received $4350 from the publisher. Following this, Barbara had many

interviews for gathering multiple manuscripts while working for the book which in return gave

her a huge amount of $3200 which can also be considered as her personal exertion income.

All the above mentioned cases are the proof of the statement i.e. personal exertion income is

the income earned by personal skills, experiences (Pellegrinoa, Perbolib, and Squillerod,

2019).

CASE-2

Signing a contract does not play any role in personal exertion income as Barbara has its own

choice of writing the book whenever she wants.

Signing a contract is nothing but just buying patent for your book (doesn’t matter before or

after writing books) to avoid copyright issues which have nothing to relate with personal

exertion income. Barbara will get her PEI only after publishing the book, while signing of

contract can be done anytime as it depends on your matter of choice. She could have her

personal exertion income even if she did not sign the contract also, because the work she has

done was still considered as her own based on her skills and experiences ( Weber, 2014).

Wherever or whenever Barbara will sell her own skills and experiences her income will term

to be personal not the capital gain (Faccio and Xu, 2015).

Question 3

Gift Taxation Law has elaborated that if any asset transferred by parent to his son/ daughter,

will be taxable in the hand of parent itself. As this would not counted as transfer and does not

taxable in the hand of son/daughter. ‘Hayes v FCT (1956) CLR 47’, mentioned that if

assessee transfer shares to his associates without paying anything or no formal agreement

between them, in that case, transfer does not treated as transfer and taxable in the hand of

assesse (Smith, 2015).

According to The Australian Income Tax Authority, If the parents help their children financially

by rendering them cash in the form of loan. Then as per this case the money received by the

parents from their Daughters or Sons will be taxable income of their parents.

Similarly to start up a business, Patrick helps his Son by giving financial help i.e. ($52000) as

a loan. After five years, David (Son) returned the amount to Patrick of $6000 ($58,000-

$52,000) would be termed as taxable income. So the Patrick son gives a taxable amount to

Patrick because the amount which he gets from Patrick is a loan amount not a gift.

7

As per the case study of ‘Brent v FCT(1971) 125 CLR 418’ (Snape,2015) in which writer sold

copyright of his book named ‘Husband story of life’ to a newspaper agency. So the money

earned by the writer can be referred as personal exertion income because the book was

written by his own knowledge and experiences which does not involve any other individual or

group as a part of this book (Braunerhjelm and Eklund, 2014). So similarly the amount

earned i.e. $13,400 by writing books is definitely considered as personal exertion income.

Barbara writer of a book named as ‘Economics Principles’ sold his book to Eco Books Ltd

library for which she received $4350 from the publisher. Following this, Barbara had many

interviews for gathering multiple manuscripts while working for the book which in return gave

her a huge amount of $3200 which can also be considered as her personal exertion income.

All the above mentioned cases are the proof of the statement i.e. personal exertion income is

the income earned by personal skills, experiences (Pellegrinoa, Perbolib, and Squillerod,

2019).

CASE-2

Signing a contract does not play any role in personal exertion income as Barbara has its own

choice of writing the book whenever she wants.

Signing a contract is nothing but just buying patent for your book (doesn’t matter before or

after writing books) to avoid copyright issues which have nothing to relate with personal

exertion income. Barbara will get her PEI only after publishing the book, while signing of

contract can be done anytime as it depends on your matter of choice. She could have her

personal exertion income even if she did not sign the contract also, because the work she has

done was still considered as her own based on her skills and experiences ( Weber, 2014).

Wherever or whenever Barbara will sell her own skills and experiences her income will term

to be personal not the capital gain (Faccio and Xu, 2015).

Question 3

Gift Taxation Law has elaborated that if any asset transferred by parent to his son/ daughter,

will be taxable in the hand of parent itself. As this would not counted as transfer and does not

taxable in the hand of son/daughter. ‘Hayes v FCT (1956) CLR 47’, mentioned that if

assessee transfer shares to his associates without paying anything or no formal agreement

between them, in that case, transfer does not treated as transfer and taxable in the hand of

assesse (Smith, 2015).

According to The Australian Income Tax Authority, If the parents help their children financially

by rendering them cash in the form of loan. Then as per this case the money received by the

parents from their Daughters or Sons will be taxable income of their parents.

Similarly to start up a business, Patrick helps his Son by giving financial help i.e. ($52000) as

a loan. After five years, David (Son) returned the amount to Patrick of $6000 ($58,000-

$52,000) would be termed as taxable income. So the Patrick son gives a taxable amount to

Patrick because the amount which he gets from Patrick is a loan amount not a gift.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, with interest the whole amount which will be received by Patrick at the end of fifth

year will be will not be considered as accessible income but will be term to be an taxable

income for Patrick . Thus, as per Australian income tax authority department the excess

amount which Patrick will receive from his son over a loan which was rendered by Patrick to

his son will be charged under the heading of taxable income (Smithies and Uppal, 2019).

After re-assessment of above situation in case when Patrick render loan to his son without

any contract signing and without demanding for any kind of commission or security and

simply just do a verbal communication with son. Then in such type of case the excess

returned value by son to Patrick of $52000 will not be considered as taxable income and nor

that income will term to be gift tax liability income. But the repayment which will be done by

Patrick son to Patrick after 2 years along with interest of $2400 (S6, 000/5*2) will be

considered under the head of taxable income of Patrick account (Martin, 2019).

In order to be ensured off that income liability accessibility does not get affected then an

assessee must take cheque method into consideration. Beside this as per the view point of

Australian income tax authority intention of all parties matters a lot. In addition to this it can be

said that payment of pension can also get affected if the income will term to be under gift tax

liability and this can result an outcome of assessable income increment of Patrick. Certain

limit are being set by Australian income tax authority in respect of gift tax liability and such

limit is that an assessee can avail up to $10000 per month or $30000 per annum which ever

will be less. In case if gif tax liability limit get exceeded than in assessment year it would b

considered as assessable income for parent (Minas, Lim, and Evans, 2018).

8

year will be will not be considered as accessible income but will be term to be an taxable

income for Patrick . Thus, as per Australian income tax authority department the excess

amount which Patrick will receive from his son over a loan which was rendered by Patrick to

his son will be charged under the heading of taxable income (Smithies and Uppal, 2019).

After re-assessment of above situation in case when Patrick render loan to his son without

any contract signing and without demanding for any kind of commission or security and

simply just do a verbal communication with son. Then in such type of case the excess

returned value by son to Patrick of $52000 will not be considered as taxable income and nor

that income will term to be gift tax liability income. But the repayment which will be done by

Patrick son to Patrick after 2 years along with interest of $2400 (S6, 000/5*2) will be

considered under the head of taxable income of Patrick account (Martin, 2019).

In order to be ensured off that income liability accessibility does not get affected then an

assessee must take cheque method into consideration. Beside this as per the view point of

Australian income tax authority intention of all parties matters a lot. In addition to this it can be

said that payment of pension can also get affected if the income will term to be under gift tax

liability and this can result an outcome of assessable income increment of Patrick. Certain

limit are being set by Australian income tax authority in respect of gift tax liability and such

limit is that an assessee can avail up to $10000 per month or $30000 per annum which ever

will be less. In case if gif tax liability limit get exceeded than in assessment year it would b

considered as assessable income for parent (Minas, Lim, and Evans, 2018).

8

CONCLUSION

From the above mentioned cases, it can easily conclude that various detailed information on

Australian Income Tax authorities and their terms and conditions are discussed in this report.

Capital gain provisions are used in question one, while in the second question, provisions

related to personal exertion income is discussed. In third case, lastly it is being discussed that

how assessable income are being settled out in an appropriate manner as per Australian

income tax authority. Finally it is concluded that any income which covers under Australian

taxation law then the assesse is liable to pay tax on such income.

.

9

From the above mentioned cases, it can easily conclude that various detailed information on

Australian Income Tax authorities and their terms and conditions are discussed in this report.

Capital gain provisions are used in question one, while in the second question, provisions

related to personal exertion income is discussed. In third case, lastly it is being discussed that

how assessable income are being settled out in an appropriate manner as per Australian

income tax authority. Finally it is concluded that any income which covers under Australian

taxation law then the assesse is liable to pay tax on such income.

.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design.Cambridge University Press.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Carney, M., Gedajlovic, E. and Strike, V.M., 2014. Dead money: Inheritance law and the

longevity of family firms. Entrepreneurship Theory and Practice, 38(6), pp.1261-1283.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Goldin, J., 2015. Optimal tax salience. Journal of Public Economics, 131, pp.115-123.

Martin, F., 2019. Unincorporated associations: Legal and tax consequences. Taxation in

Australia, 53(8), p.420.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Pellegrinoa, S., Perbolib, G. and Squillerod, G., 2019. Balancing the Equity-efficiency Trade-

off in Personal Income Taxation: An Evolutionary Approach.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Smithies, J. and Uppal, S., 2019. Australia. In Cultural Governance in a Global

Context (pp.127-158). Palgrave Macmillan, Cham.

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2014. Australian Taxation

Law 2014 (pp. 1-81).

10

Auerbach, A.J. and Hassett, K., 2015. Capital taxation in the twenty-first century. American

Economic Review, 105(5), pp.38-42.

Brabazon, M., 2019. International Taxation of Trust Income: Principles, Planning and

Design.Cambridge University Press.

Braunerhjelm, P. and Eklund, J.E., 2014. Taxes, tax administrative burdens and new firm

formation. Kyklos, 67(1), pp.1-11.

Carney, M., Gedajlovic, E. and Strike, V.M., 2014. Dead money: Inheritance law and the

longevity of family firms. Entrepreneurship Theory and Practice, 38(6), pp.1261-1283.

Edmonds, R., 2015. Structural tax reform: What should be brought to the table. Austl. Tax

F., 30, p.393.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: an

alternative way forward. Austl. Tax F., 30, p.735.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and Quantitative

Analysis, 50(3), pp.277-300.

Goldin, J., 2015. Optimal tax salience. Journal of Public Economics, 131, pp.115-123.

Martin, F., 2019. Unincorporated associations: Legal and tax consequences. Taxation in

Australia, 53(8), p.420.

Minas, J., Lim, Y. and Evans, C., 2018, August. The impact of tax rate changes on capital

gains realisations: evidence from Australia. In Australian Tax Forum (Vol. 33, No. 4).

Pellegrinoa, S., Perbolib, G. and Squillerod, G., 2019. Balancing the Equity-efficiency Trade-

off in Personal Income Taxation: An Evolutionary Approach.

Smith, J.P., 2015. Australian state income taxation: A historical perspective. Austl. Tax

F., 30,p.679.

Smithies, J. and Uppal, S., 2019. Australia. In Cultural Governance in a Global

Context (pp.127-158). Palgrave Macmillan, Cham.

Weber, R., 2014. Tax increment financing in theory and practice. In Financing economic

development in the 21st century (pp. 297-315). Routledge.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2014. Australian Taxation

Law 2014 (pp. 1-81).

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.