Taxation Law Assessment 2 (2018): Complete Solution Guide

VerifiedAdded on 2023/06/07

|10

|1317

|468

Homework Assignment

AI Summary

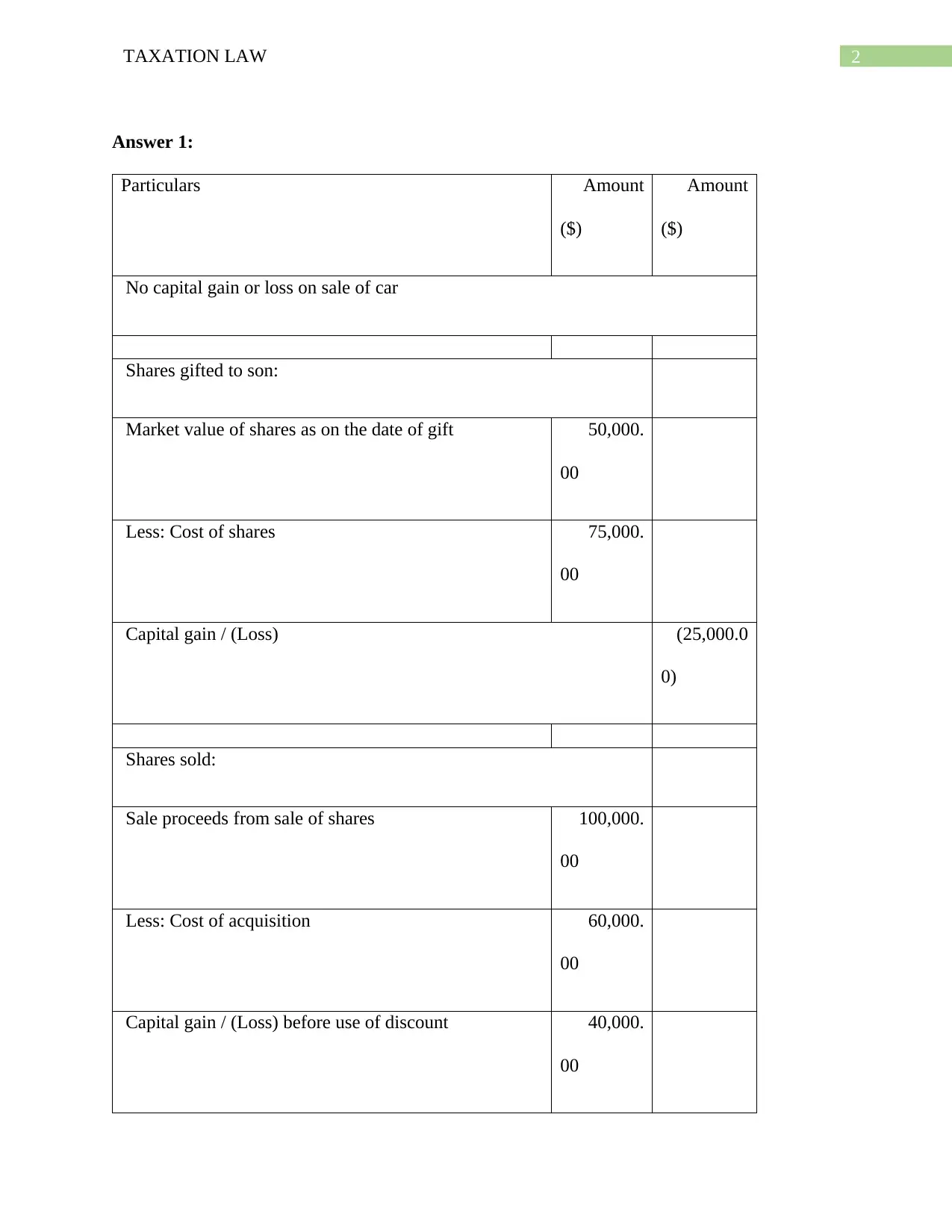

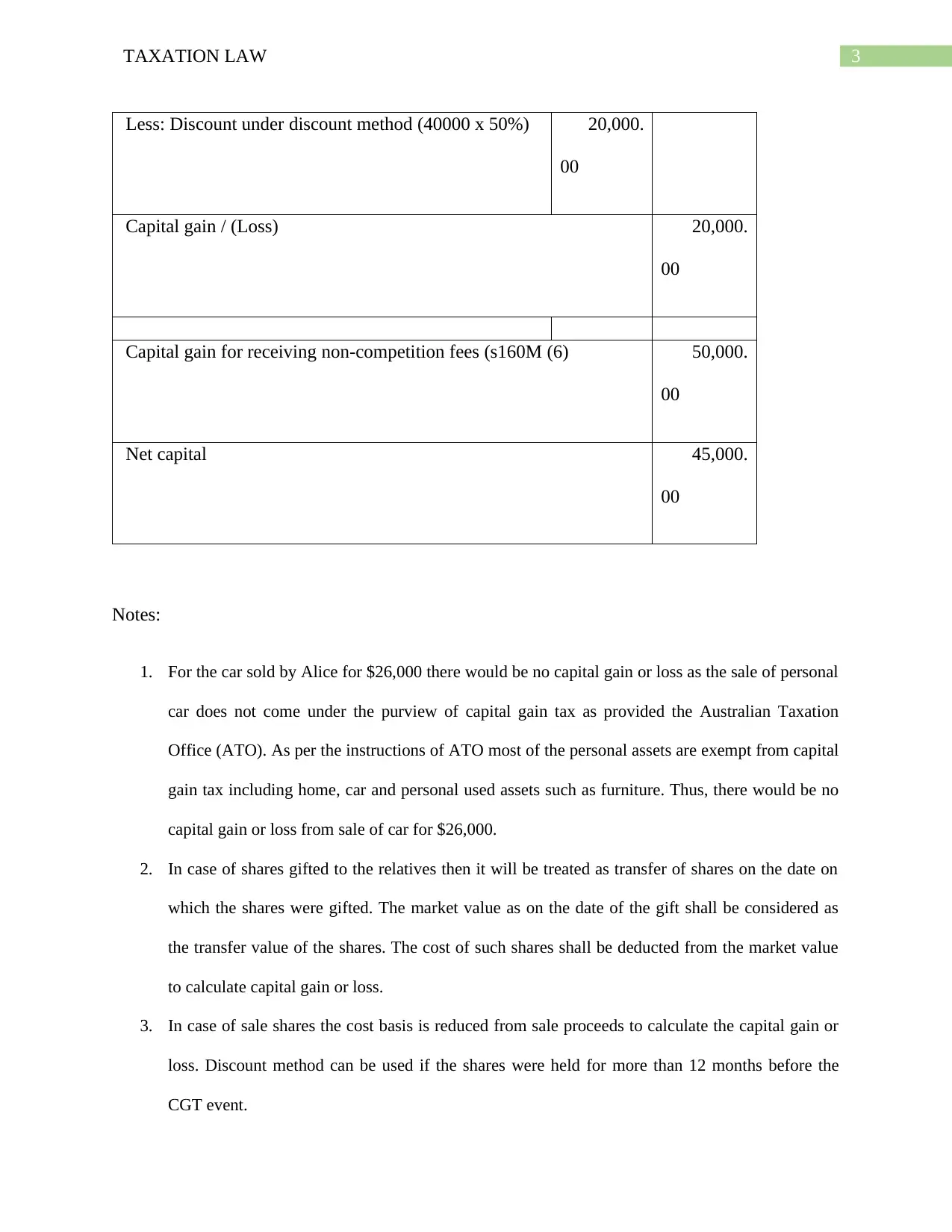

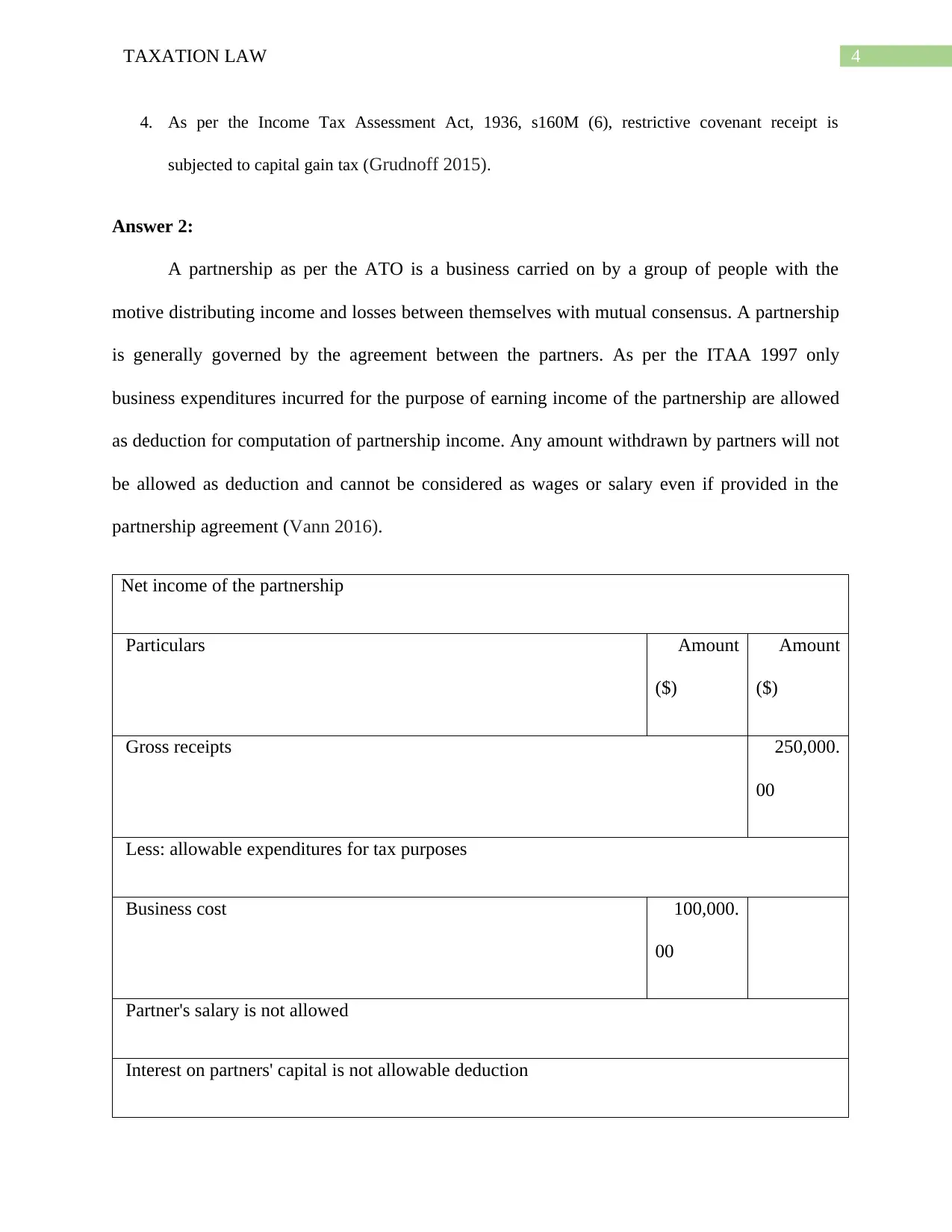

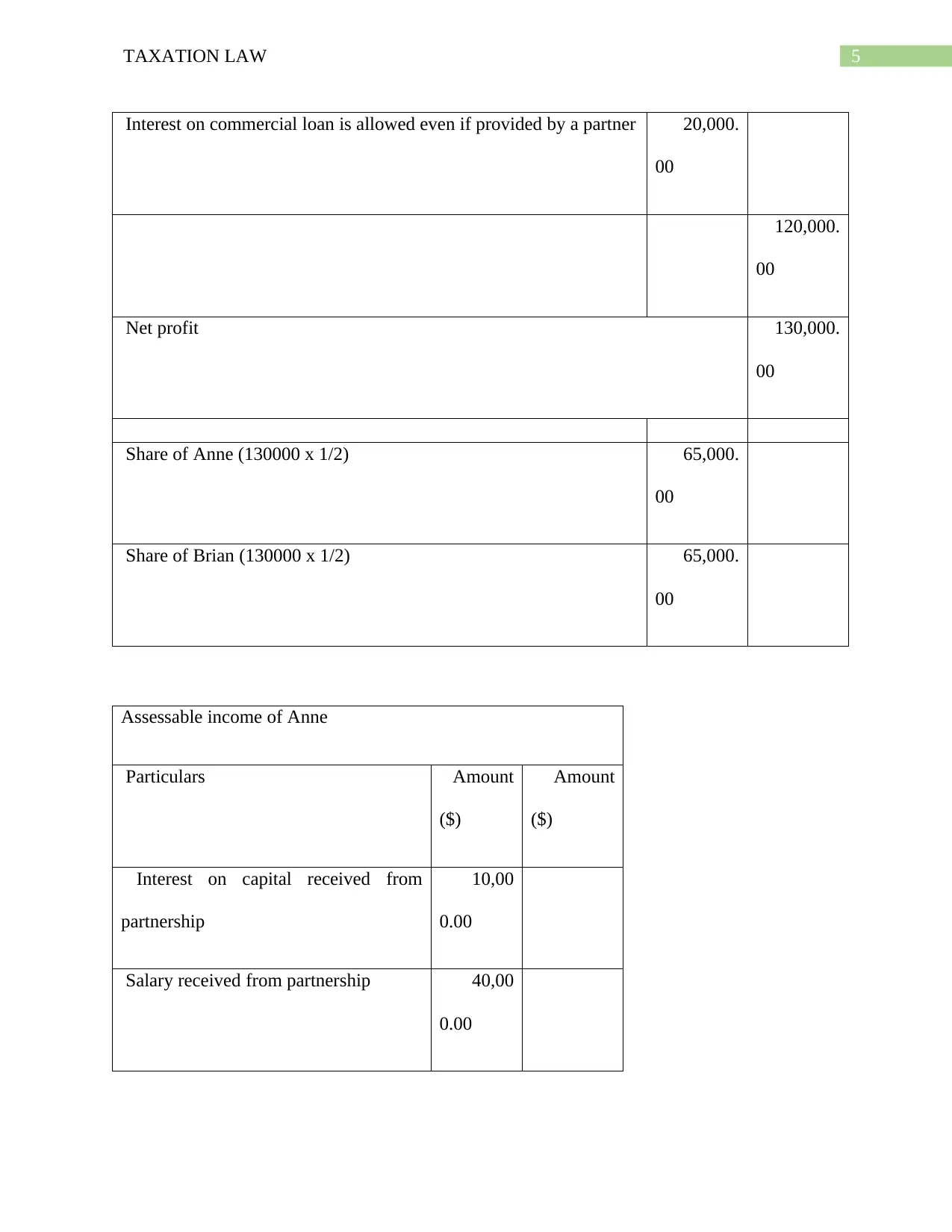

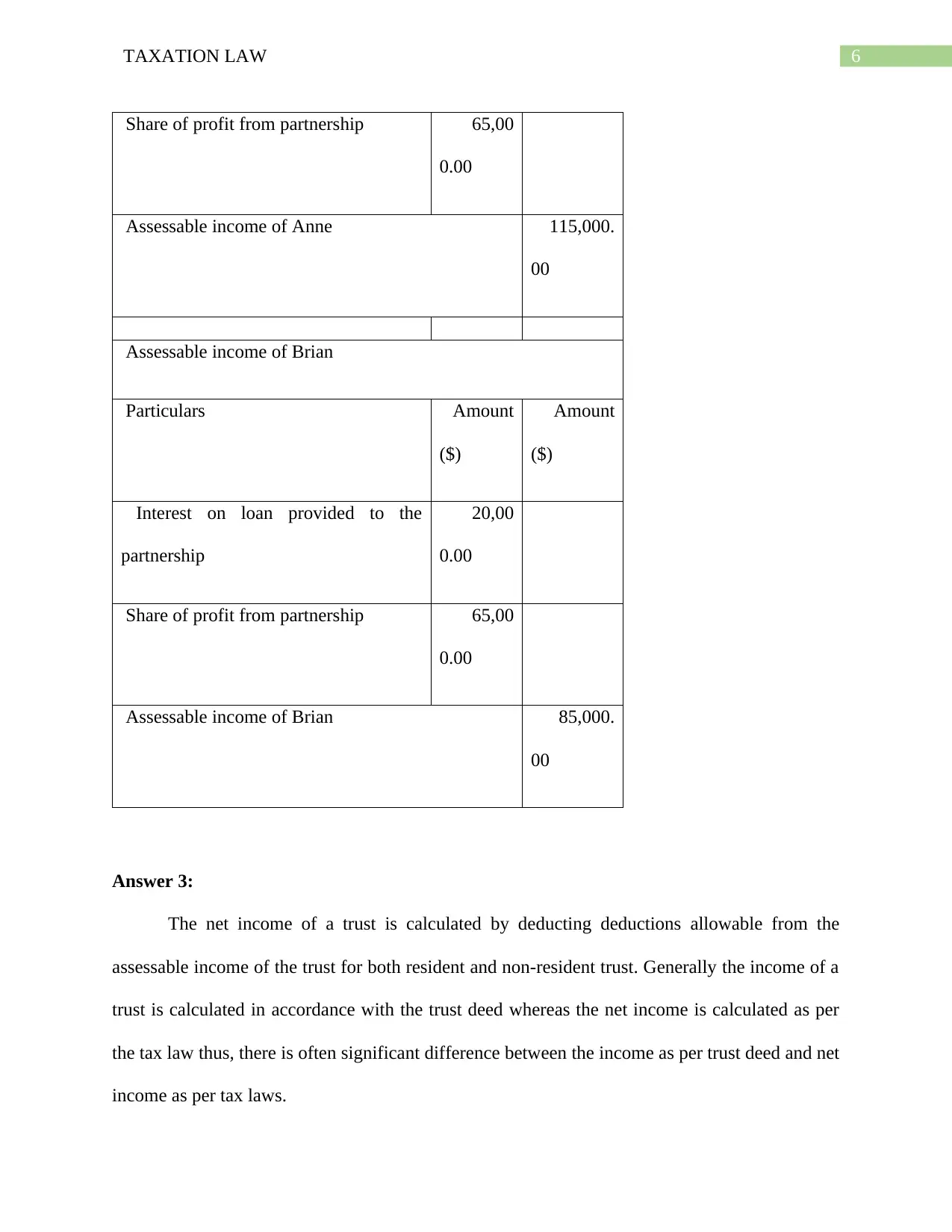

This document provides a comprehensive solution to a Taxation Law assessment, addressing various aspects of Australian taxation. The solution begins by calculating Alice's net capital gain or loss, considering the sale of a car, gifted shares, sold shares, and a restrictive covenant payment. It then analyzes a partnership's income, calculating the assessable income for partners Anne and Brian, including interest and salary. The solution further explores trust income, determining the tax liabilities of beneficiaries Mr. Luke, Pauline, and Jane, and the treatment of medical expenses. Finally, it examines redundancy payments, differentiating between genuine and non-genuine redundancy payments and their tax implications based on ATO guidelines. The document offers detailed calculations and explanations, referencing relevant tax laws and providing a thorough understanding of the concepts.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.