Taxation Law: Calculating Tax Liabilities for John and Frank

VerifiedAdded on 2021/11/01

|10

|1477

|25

Homework Assignment

AI Summary

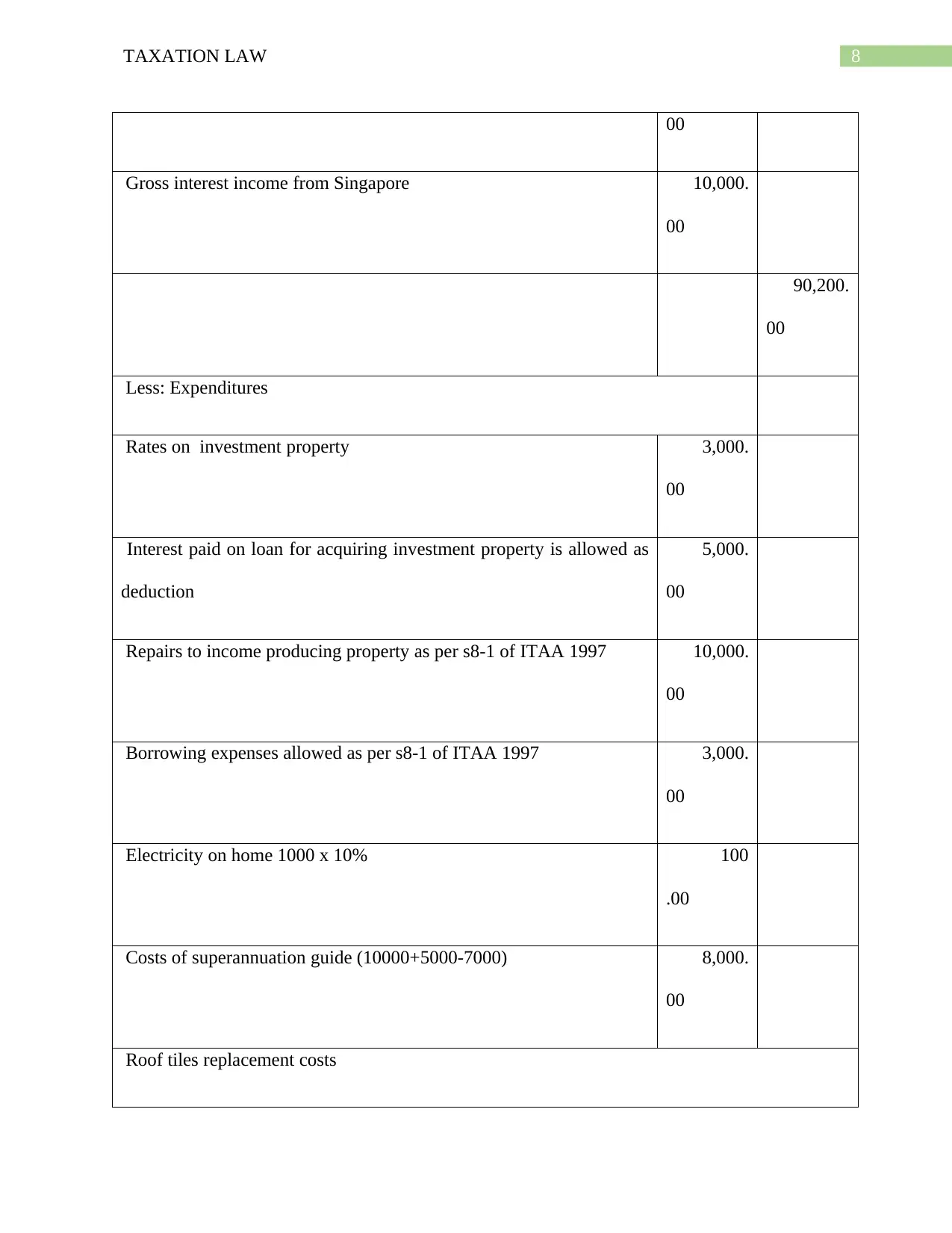

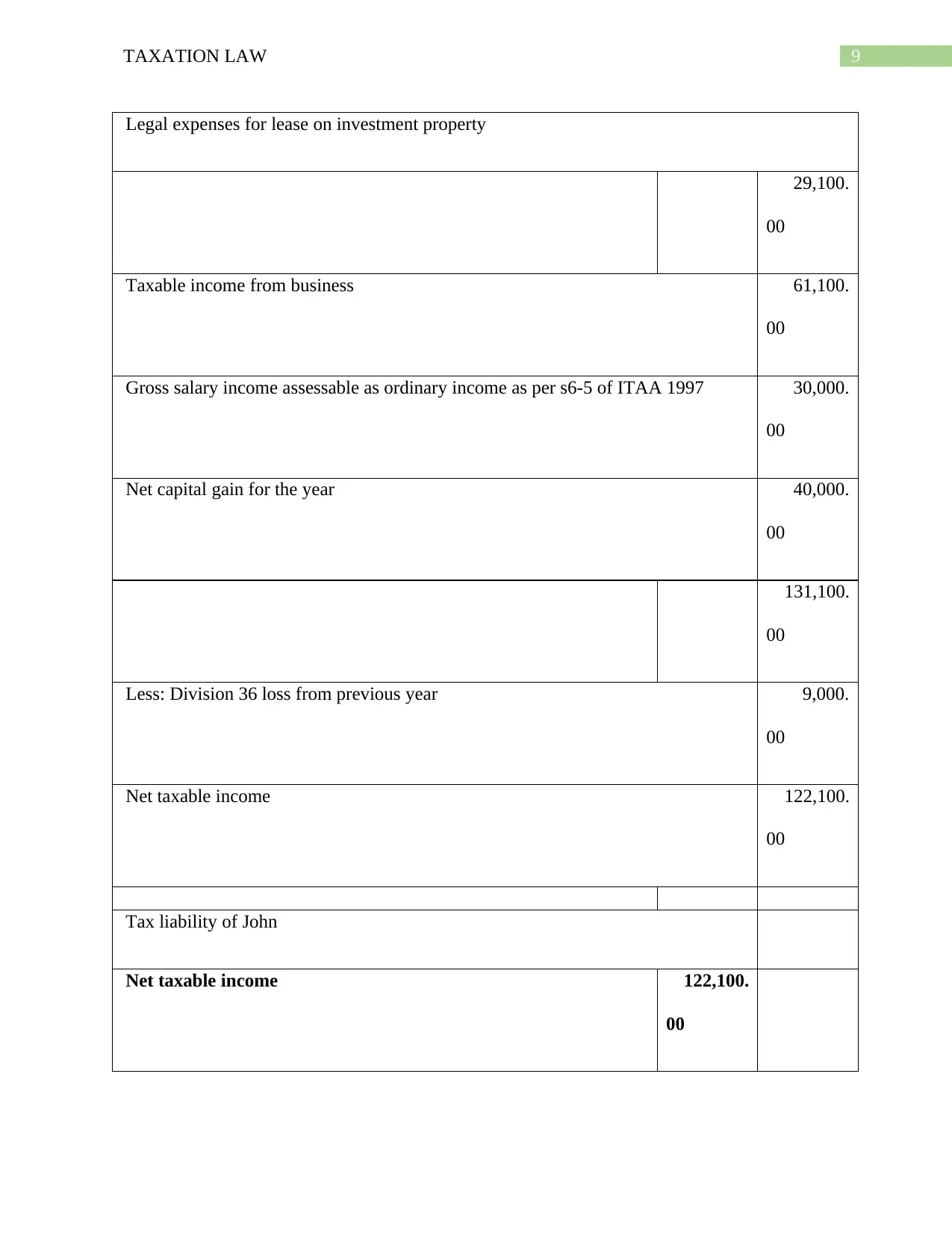

This assignment provides a detailed solution to a taxation law problem, focusing on the calculation of income tax liabilities for two individuals, John and Frank, under the Australian tax system. The solution meticulously calculates their taxable incomes, considering various income sources such as professional fees, sales, dividends, interest, salary, and rental income. It also includes a thorough analysis of deductible expenses, such as office rent, employee salaries, depreciation, legal expenses, and interest on loans. The assignment further addresses capital gains tax, including short-term and long-term capital gains, and incorporates relevant tax rates and regulations. The calculations adhere to the Income Tax Assessment Act 1997 (ITAA 1997) and relevant case law, providing a comprehensive understanding of the taxation principles involved. The assignment also includes working notes and references to support the calculations and conclusions.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.