Taxation Law Assignment: Income, Capital Gains, and CGT

VerifiedAdded on 2022/08/20

|11

|2883

|11

Homework Assignment

AI Summary

This taxation law assignment analyzes various aspects of Australian taxation, including the assessment of income from part-time employment, the application of capital gains tax (CGT), and fringe benefits tax (FBT). The assignment examines whether tips and gifts received by an employee constitute assessable income, referencing relevant case law and legislation such as ITAA 1997 and ITAA 1936. It further explores CGT implications for the sale of assets, differentiating between pre-CGT and post-CGT assets, personal use assets, and collectables, with specific examples. The assignment also covers small business CGT concessions and the tax treatment of fringe benefits provided by an employer. Key concepts include ordinary income, CGT events, and the application of specific sections of the tax legislation to different scenarios. The assignment provides a comprehensive overview of taxation principles and their practical application.

Running head: TAXATION LAW

TAXATION LAW

Name of Student

Name of University

Author note

Word count

TAXATION LAW

Name of Student

Name of University

Author note

Word count

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question A................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..................................................................................................................................5

Answer B:...................................................................................................................................6

Answer C:...................................................................................................................................6

Answer D:..................................................................................................................................7

Answer E:...................................................................................................................................8

References..................................................................................................................................9

Table of Contents

Answer to Question A................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................3

Conclusion:................................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..................................................................................................................................5

Answer B:...................................................................................................................................6

Answer C:...................................................................................................................................6

Answer D:..................................................................................................................................7

Answer E:...................................................................................................................................8

References..................................................................................................................................9

2TAXATION LAW

Answer to Question A

Issues:

This case study discusses about whether various receipts from part time employment

will be considered as taxable for the taxpayer or not.

Rule:

Assessable income has an important portion of ordinary income. It is very important

to assess the ordinary earning during the year under tax calculation. Assessable income

contains ordinary income of every individual taxpayer and it is in the agreements with

ordinary concepts (Burton, 2017). This definition of ordinary income is provided under “sec-

6-5 ITAA 1997”. The taxpayer gets voluntary payment for a part of their service and this

service amount is considered as income under ordinary income representing the incidence of

employment. “Calvert v Wainwright (1947)” described that if third party provides any tips

to the taxpayer as gift then it is signified as voluntary payment as the tip is provided for

services provided and it establishes a link between the services provided. It is usually

assumed as ordinary income (Barkoczy, 2016).

There is no such proper definition of income under the laws, “sec-6(1) ITAA 1936”

defines income from personal services as something that is received other than salary,

bonuses, wages or commission by the taxpayer for providing any personal service. “FCT v

Brown (2002)” describes it as any receipts that is connected for providing service is treated

as product or reward for activity or occurrence of employment. This type of receipts should

be amounted to ordinary income under taxation.

“Sect-6-5 ITAA 1997” noted that any personal gift is to be treated as taxable earning

when the gift are opposite to any voluntary payment relating to the services or employment

Answer to Question A

Issues:

This case study discusses about whether various receipts from part time employment

will be considered as taxable for the taxpayer or not.

Rule:

Assessable income has an important portion of ordinary income. It is very important

to assess the ordinary earning during the year under tax calculation. Assessable income

contains ordinary income of every individual taxpayer and it is in the agreements with

ordinary concepts (Burton, 2017). This definition of ordinary income is provided under “sec-

6-5 ITAA 1997”. The taxpayer gets voluntary payment for a part of their service and this

service amount is considered as income under ordinary income representing the incidence of

employment. “Calvert v Wainwright (1947)” described that if third party provides any tips

to the taxpayer as gift then it is signified as voluntary payment as the tip is provided for

services provided and it establishes a link between the services provided. It is usually

assumed as ordinary income (Barkoczy, 2016).

There is no such proper definition of income under the laws, “sec-6(1) ITAA 1936”

defines income from personal services as something that is received other than salary,

bonuses, wages or commission by the taxpayer for providing any personal service. “FCT v

Brown (2002)” describes it as any receipts that is connected for providing service is treated

as product or reward for activity or occurrence of employment. This type of receipts should

be amounted to ordinary income under taxation.

“Sect-6-5 ITAA 1997” noted that any personal gift is to be treated as taxable earning

when the gift are opposite to any voluntary payment relating to the services or employment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

provided. This type of gifts is not treated as taxable income. In view of that, in “Scott v FCT

(1996)” case, a huge amount of 10,000 pound was paid by the advocate as the lawyer acted

for the widowed wife and as a gesture of friendship. Under “sec-25(1) of ITAA 1936” this

type of amounts are to be treated as non-taxable income.

As termed under “sec-66 (1) FBTAA” that FBT is levied on the employer and the

taxes under fringe benefits are not provided on the receiver of benefit rather it is provided on

the basis of fringe benefit (Butler and Calcott, 2018). Fringe benefit are referred to any rights,

services, privilege that is provided for carrying out works in respect of employment. FBT is

provided only when there is an employment relationship and the employee is provided with

non-cash benefits rather than salary or wages as noted under “sec-137 FBTAA 1986”. The

“sec 23L” describes that if the employee is provided with fringe benefits by the employer

then the employer should be liable to pay tax for the same. “Essenboourne Pty Ltd v FCT

(2002)” noted that the benefits should be given with relation to employee only (Cooper,

2018).

ATO described that any cash gift that is given during the birthday occasion as a

present or any special occasion should not be treated as taxable for the recipient (Blakelock

and King, 2017). An example, gift from son to father will not be treated as taxable income.

“Hayes v FCT (1956)” described that if there is any gifts or presents are connected with

payments then it will not be treated as taxable income (Braithwaite and Reinhard, 2019).

Application:

From this case study, it can be observed that Emmi is the taxpayer who is working

part time in Crown Melbourne restaurant along with studying in Holmes Institution. During

the year, Emmi received $335 as a cash gift from a customer while working in the restaurant.

This tip should be treated as voluntary payment as it is treated as the part of her service

provided. This type of gifts is not treated as taxable income. In view of that, in “Scott v FCT

(1996)” case, a huge amount of 10,000 pound was paid by the advocate as the lawyer acted

for the widowed wife and as a gesture of friendship. Under “sec-25(1) of ITAA 1936” this

type of amounts are to be treated as non-taxable income.

As termed under “sec-66 (1) FBTAA” that FBT is levied on the employer and the

taxes under fringe benefits are not provided on the receiver of benefit rather it is provided on

the basis of fringe benefit (Butler and Calcott, 2018). Fringe benefit are referred to any rights,

services, privilege that is provided for carrying out works in respect of employment. FBT is

provided only when there is an employment relationship and the employee is provided with

non-cash benefits rather than salary or wages as noted under “sec-137 FBTAA 1986”. The

“sec 23L” describes that if the employee is provided with fringe benefits by the employer

then the employer should be liable to pay tax for the same. “Essenboourne Pty Ltd v FCT

(2002)” noted that the benefits should be given with relation to employee only (Cooper,

2018).

ATO described that any cash gift that is given during the birthday occasion as a

present or any special occasion should not be treated as taxable for the recipient (Blakelock

and King, 2017). An example, gift from son to father will not be treated as taxable income.

“Hayes v FCT (1956)” described that if there is any gifts or presents are connected with

payments then it will not be treated as taxable income (Braithwaite and Reinhard, 2019).

Application:

From this case study, it can be observed that Emmi is the taxpayer who is working

part time in Crown Melbourne restaurant along with studying in Holmes Institution. During

the year, Emmi received $335 as a cash gift from a customer while working in the restaurant.

This tip should be treated as voluntary payment as it is treated as the part of her service

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(Hasen, 2018). This amount of cash it to be calculated under ordinary income as the benefits

are provided to Emmi as an incidence of Employment. “Calvert v wainwright (1947)”

judged that this tip that is given to Emmi is a voluntary payment as the tip is given to her as a

part of her personal service. Under “section 6-5 ITAA 1997” described that this amount of

payment established a connection among the services and it is taxable as the income is to be

treated as ordinary income (Acquilina, 2019).

Emmi also received an income worth $25,000 during the year as a part of her

employment. The “sec 6(1) ITAA 1936” described this amount of $25,000 as income from

personal effort. “Brown v FCT (2002)” judges that the amount which Emmi received is

connected to carry out employment service. Under “sec 6-5 ITAA 1997” described this

amount as a product of her employment and treated it under taxable ordinary income (Arnold,

Ault and Cooper, 2019).

In the other scenario, Emmi reported that a customer gifted her a expensive luxury

perfume worth $250 in the Christmas. The gift is a part of voluntary payment and it is related

to the personal service provided to the customer and should not be treated as taxable income.

“Scott v FCT (1966) noted that the gift received by Emmi is not taxable under “sec-25(1) of

ITAA 1936”. Further, this gift of perfume cannot be converted into cash and therefore it

fails to meet the criteria to be under ordinary income (Bankman et.al, 2018).

During the year, an employer of Emmi provided Emmi with monthly entertainment

expenses. The owner also provided Emmi with a meal worth $380. This monthly expenses

and meal expenses paid by the employer should be treated as fringe benefit as it was given to

Emmi for a part of Emploment noted under “sec 136(1) FBTAA 1986” Mentioning the

judgements of “Essenboourne Pty Ltd v FCT (2002)” this fringe benefits will be taxable

under “sec-137 FBTAA 1986” as there is a work relation between the employer and

(Hasen, 2018). This amount of cash it to be calculated under ordinary income as the benefits

are provided to Emmi as an incidence of Employment. “Calvert v wainwright (1947)”

judged that this tip that is given to Emmi is a voluntary payment as the tip is given to her as a

part of her personal service. Under “section 6-5 ITAA 1997” described that this amount of

payment established a connection among the services and it is taxable as the income is to be

treated as ordinary income (Acquilina, 2019).

Emmi also received an income worth $25,000 during the year as a part of her

employment. The “sec 6(1) ITAA 1936” described this amount of $25,000 as income from

personal effort. “Brown v FCT (2002)” judges that the amount which Emmi received is

connected to carry out employment service. Under “sec 6-5 ITAA 1997” described this

amount as a product of her employment and treated it under taxable ordinary income (Arnold,

Ault and Cooper, 2019).

In the other scenario, Emmi reported that a customer gifted her a expensive luxury

perfume worth $250 in the Christmas. The gift is a part of voluntary payment and it is related

to the personal service provided to the customer and should not be treated as taxable income.

“Scott v FCT (1966) noted that the gift received by Emmi is not taxable under “sec-25(1) of

ITAA 1936”. Further, this gift of perfume cannot be converted into cash and therefore it

fails to meet the criteria to be under ordinary income (Bankman et.al, 2018).

During the year, an employer of Emmi provided Emmi with monthly entertainment

expenses. The owner also provided Emmi with a meal worth $380. This monthly expenses

and meal expenses paid by the employer should be treated as fringe benefit as it was given to

Emmi for a part of Emploment noted under “sec 136(1) FBTAA 1986” Mentioning the

judgements of “Essenboourne Pty Ltd v FCT (2002)” this fringe benefits will be taxable

under “sec-137 FBTAA 1986” as there is a work relation between the employer and

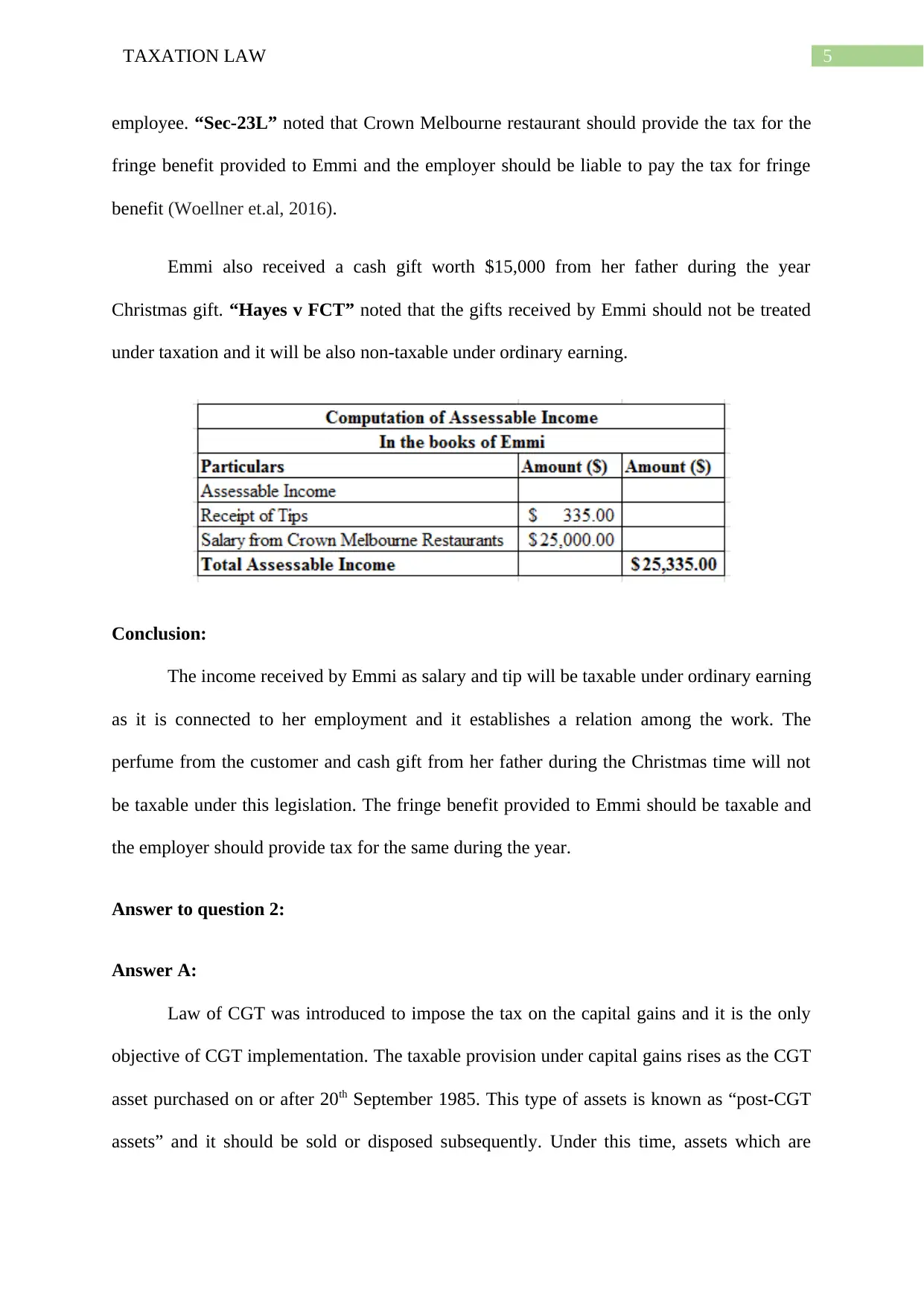

5TAXATION LAW

employee. “Sec-23L” noted that Crown Melbourne restaurant should provide the tax for the

fringe benefit provided to Emmi and the employer should be liable to pay the tax for fringe

benefit (Woellner et.al, 2016).

Emmi also received a cash gift worth $15,000 from her father during the year

Christmas gift. “Hayes v FCT” noted that the gifts received by Emmi should not be treated

under taxation and it will be also non-taxable under ordinary earning.

Conclusion:

The income received by Emmi as salary and tip will be taxable under ordinary earning

as it is connected to her employment and it establishes a relation among the work. The

perfume from the customer and cash gift from her father during the Christmas time will not

be taxable under this legislation. The fringe benefit provided to Emmi should be taxable and

the employer should provide tax for the same during the year.

Answer to question 2:

Answer A:

Law of CGT was introduced to impose the tax on the capital gains and it is the only

objective of CGT implementation. The taxable provision under capital gains rises as the CGT

asset purchased on or after 20th September 1985. This type of assets is known as “post-CGT

assets” and it should be sold or disposed subsequently. Under this time, assets which are

employee. “Sec-23L” noted that Crown Melbourne restaurant should provide the tax for the

fringe benefit provided to Emmi and the employer should be liable to pay the tax for fringe

benefit (Woellner et.al, 2016).

Emmi also received a cash gift worth $15,000 from her father during the year

Christmas gift. “Hayes v FCT” noted that the gifts received by Emmi should not be treated

under taxation and it will be also non-taxable under ordinary earning.

Conclusion:

The income received by Emmi as salary and tip will be taxable under ordinary earning

as it is connected to her employment and it establishes a relation among the work. The

perfume from the customer and cash gift from her father during the Christmas time will not

be taxable under this legislation. The fringe benefit provided to Emmi should be taxable and

the employer should provide tax for the same during the year.

Answer to question 2:

Answer A:

Law of CGT was introduced to impose the tax on the capital gains and it is the only

objective of CGT implementation. The taxable provision under capital gains rises as the CGT

asset purchased on or after 20th September 1985. This type of assets is known as “post-CGT

assets” and it should be sold or disposed subsequently. Under this time, assets which are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

purchased before 20th September 1985 are known as “pre CGT assets”. If there is any capital

gain or loss from the sale of asset, it should be ignored or levied (Teo, Barros and Hinchliffe,

2016).

In this scenario, Liu decides to sell her house that she has been using for her main

residency. She purchased the house in 1981 for $55,000. Liu sold the house in the previous

year for $630,000. The house was bought before 20th September 1985 therefore this house

should be treated as “Pre-CGT Assets”. As per CGT laws, the capital gain from the sale of

asset should be levied under this law.

Answer B:

“Sec-108-5 ITAA 1997” defines asset as a form of property of rights that cannot be

held as property. “CGT event A1” occurs when the CGT assets are sold. It comes under

“sec-104-10”. Subdivision 108-C defined asset which a taxpayer uses for their personal

purpose. The example of personal use asset noted under “sec-108-20 (2) & (3) ITAA 1997”

are furniture, electrical items, motor vehicles and boats. The capital loss from the sale of

personal use asset should be levied by the taxpayer under “sec 108-20(1)”.

Liu sold her car she purchased in 2011 at Australia with acquisition cost of $37,000 as

she moved to china. She sold the car for approximately $8,000. Under “sec-108-20 (2) &

(3)” the car is treated as personal use asset and the sale of car arised from “CGT event A1”

under “sec-104-10”. Under “sec-108-20 (1)” special rules, Liu should ignore the loss from

the sale of capital asset that he met from the sale of car (Crossingham, 2018).

Answer C:

Small business concessions under CGT event is dealt under “Div-152” that occurred on

or after 21th September 1999. As described under “Sec-152-10” , if any business has asset

purchased before 20th September 1985 are known as “pre CGT assets”. If there is any capital

gain or loss from the sale of asset, it should be ignored or levied (Teo, Barros and Hinchliffe,

2016).

In this scenario, Liu decides to sell her house that she has been using for her main

residency. She purchased the house in 1981 for $55,000. Liu sold the house in the previous

year for $630,000. The house was bought before 20th September 1985 therefore this house

should be treated as “Pre-CGT Assets”. As per CGT laws, the capital gain from the sale of

asset should be levied under this law.

Answer B:

“Sec-108-5 ITAA 1997” defines asset as a form of property of rights that cannot be

held as property. “CGT event A1” occurs when the CGT assets are sold. It comes under

“sec-104-10”. Subdivision 108-C defined asset which a taxpayer uses for their personal

purpose. The example of personal use asset noted under “sec-108-20 (2) & (3) ITAA 1997”

are furniture, electrical items, motor vehicles and boats. The capital loss from the sale of

personal use asset should be levied by the taxpayer under “sec 108-20(1)”.

Liu sold her car she purchased in 2011 at Australia with acquisition cost of $37,000 as

she moved to china. She sold the car for approximately $8,000. Under “sec-108-20 (2) &

(3)” the car is treated as personal use asset and the sale of car arised from “CGT event A1”

under “sec-104-10”. Under “sec-108-20 (1)” special rules, Liu should ignore the loss from

the sale of capital asset that he met from the sale of car (Crossingham, 2018).

Answer C:

Small business concessions under CGT event is dealt under “Div-152” that occurred on

or after 21th September 1999. As described under “Sec-152-10” , if any business has asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

value less than $6 million then the CGT assets meets the “active asset test” allowing four

concessions to the taxpayer. The concessions are discussed below

Under “Subdivision 152-B”, 15-year exemption of capital gains of assets when the

ownership of asset exceeds 15 year.

Under “subdivision 152-C”, 50% reduction from capital gains.

Under “subdivision 152-D”, Retirement capital gains are exempt up to a sum worth

$500,000.

“CGT event A1” comes in the act when the business goodwill is lost.

A “loss or destruction of goodwill” comes in the place when a business is

permanently ceased or closed whether it is for voluntary or involuntary.

It this situation, Liu owns a small business which she decides to sell off and retire

from her business. She sold the business for $125,000 after the business was ceased

permanently. Liu will be eligible for concession under CGT act as the value of her business is

not more than $6 million as noted under “section 152-10”. The value of her asset is less than

$6 million. Moreover, Liu can also obtain a 15-year exemption from capital gains that she

can earn from the sale of photography equipment and the equipment was held for 15 years.

“CGT event A1” occurred when the business goodwill was disposed by Liu and as a result,

she can obtain a retirement concession as the value of goodwill is less than $500,000.

Answer D:

“Sec-118-10” described that special rule is there for the use of personal use asset and

the capital gain from the sale of asset must be ignored if the taxpayer purchased the asset for

an acquisition cost less than $10,000. Liu also sold the furniture for $4,800 which was

purchased for approximately $2,000.

value less than $6 million then the CGT assets meets the “active asset test” allowing four

concessions to the taxpayer. The concessions are discussed below

Under “Subdivision 152-B”, 15-year exemption of capital gains of assets when the

ownership of asset exceeds 15 year.

Under “subdivision 152-C”, 50% reduction from capital gains.

Under “subdivision 152-D”, Retirement capital gains are exempt up to a sum worth

$500,000.

“CGT event A1” comes in the act when the business goodwill is lost.

A “loss or destruction of goodwill” comes in the place when a business is

permanently ceased or closed whether it is for voluntary or involuntary.

It this situation, Liu owns a small business which she decides to sell off and retire

from her business. She sold the business for $125,000 after the business was ceased

permanently. Liu will be eligible for concession under CGT act as the value of her business is

not more than $6 million as noted under “section 152-10”. The value of her asset is less than

$6 million. Moreover, Liu can also obtain a 15-year exemption from capital gains that she

can earn from the sale of photography equipment and the equipment was held for 15 years.

“CGT event A1” occurred when the business goodwill was disposed by Liu and as a result,

she can obtain a retirement concession as the value of goodwill is less than $500,000.

Answer D:

“Sec-118-10” described that special rule is there for the use of personal use asset and

the capital gain from the sale of asset must be ignored if the taxpayer purchased the asset for

an acquisition cost less than $10,000. Liu also sold the furniture for $4,800 which was

purchased for approximately $2,000.

8TAXATION LAW

The above mentioned furniture is categorized under personal use asset under “sec-

108-20 (2) & (3)”. Capital gain from the sale of asset occurred when Liu sold the furniture

and as noted under “sec-118-10”, Liu must levy the capital gain from the sale of furniture as

the cost of the furniture is less than $10,000.

Answer E:

Collectables are a form of CGT asset that is held by the taxpayer for personal purpose

and enjoyment. This definition of collectables are given under “subdiv-108-B”. The

examples of collectables as given under “sec 108-10 (2) & (3)” are jewellery, paintings,

stamps antiques and coins (Rappaport, 2016). It is important to mention the special rules

under “Sec118-10 (1)” that the capital gains and loss from collectables should be ignored and

levied when the cost of the asset is less than $500.

Liu purchased some used paintings from second hand shop worth $500 each. Liu sold

those paintings in the current year for $28,000. Under “sec 108-10 (2) & (3)”, these paintings

should be treated as collectables as Liu purchased those for her personal enjoyment. This type

of gains should be ignored under “sec-118-10 (1)” as the cost of the asset is $500. Liu also

sold another painting for $8,000 which she bought for $1,000. Under “section 102-5”, the

capital gain earned from the sale of this painting should be Liu’s part of assessable income

and it will be taxable as statutory income.

The above mentioned furniture is categorized under personal use asset under “sec-

108-20 (2) & (3)”. Capital gain from the sale of asset occurred when Liu sold the furniture

and as noted under “sec-118-10”, Liu must levy the capital gain from the sale of furniture as

the cost of the furniture is less than $10,000.

Answer E:

Collectables are a form of CGT asset that is held by the taxpayer for personal purpose

and enjoyment. This definition of collectables are given under “subdiv-108-B”. The

examples of collectables as given under “sec 108-10 (2) & (3)” are jewellery, paintings,

stamps antiques and coins (Rappaport, 2016). It is important to mention the special rules

under “Sec118-10 (1)” that the capital gains and loss from collectables should be ignored and

levied when the cost of the asset is less than $500.

Liu purchased some used paintings from second hand shop worth $500 each. Liu sold

those paintings in the current year for $28,000. Under “sec 108-10 (2) & (3)”, these paintings

should be treated as collectables as Liu purchased those for her personal enjoyment. This type

of gains should be ignored under “sec-118-10 (1)” as the cost of the asset is $500. Liu also

sold another painting for $8,000 which she bought for $1,000. Under “section 102-5”, the

capital gain earned from the sale of this painting should be Liu’s part of assessable income

and it will be taxable as statutory income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

Arnold, B.J., Ault, H.J. and Cooper, G. eds., 2019. Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Crossingham, D., 2018. Business sale contracts: CGT and timing issues. Taxation in

Australia, 52(9), p.497.

References

Aquilina, J., 2019, November. Reforming and realigning Division 855 of the Income Tax

Assessment Act 1997 to give better effect to its policy objectives. In Australian Tax

Forum (Vol. 34, No. 1).

Arnold, B.J., Ault, H.J. and Cooper, G. eds., 2019. Comparative income taxation: a

structural analysis. Kluwer Law International BV.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), p.18.

Braithwaite, V. and Reinhart, M., 2019. The Taxpayers' Charter: Does the Australian Tax

Office comply and who benefits?. Centre for Tax System Integrity (CTSI), Research School

of Social Sciences, The Australian National University.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Butler, C. and Calcott, P., 2018. Optimal fringe benefit taxes: the implications of business

use. International Tax and Public Finance, 25(3), pp.654-672.

Cooper, R., 2018. Recent changes to fringe benefits. TAXtalk, 2018(71), pp.52-55.

Crossingham, D., 2018. Business sale contracts: CGT and timing issues. Taxation in

Australia, 52(9), p.497.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Hasen, D., 2018. How Should Gifts Be Treated under the Federal Income Tax. Mich. St. L.

Rev., p.81.

Rappaport, M.E., 2016. The Unique Income Tax Issues of Collectibles. Journal of Taxation

of Investments, 33(2).

TEO, E., Barros, C. and Hinchliffe, S.A., 2016. Clash of the Deeming Provisions: Pre-Capital

Gains Tax Concessions, Tax Consolidation and Policy in the Federal Court.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Hasen, D., 2018. How Should Gifts Be Treated under the Federal Income Tax. Mich. St. L.

Rev., p.81.

Rappaport, M.E., 2016. The Unique Income Tax Issues of Collectibles. Journal of Taxation

of Investments, 33(2).

TEO, E., Barros, C. and Hinchliffe, S.A., 2016. Clash of the Deeming Provisions: Pre-Capital

Gains Tax Concessions, Tax Consolidation and Policy in the Federal Court.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.