Taxation Theory, Practice & Law Assignment: Analysis and Calculations

VerifiedAdded on 2023/01/06

|8

|2291

|59

Homework Assignment

AI Summary

This assignment delves into various aspects of Australian taxation law. It begins with an analysis of Pablo's tax liability in Australia based on his salary, considering non-resident taxation rules. The assignment then examines the case of Californian Copper Syndicate Ltd v Harris, outlining the court's decision and its implications. Further, it explores the GST consequences for companies in a given arrangement, detailing the impact on both Surf Up P/L and Billapong P/L. The assignment continues with a calculation of the net payable tax for Melbourne Awesome Ltd, including the computation of taxable income and tax liability. It also discusses the ATO's Test Case Litigation Program, explaining its purpose, funding criteria, and application process. Finally, the assignment concludes with a calculation of the net income of a partnership, including the allocation of income to each partner, along with relevant legislation or case law.

Taxation Theory,

Practice & Law

Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

Tac liability of Pablo in Australia on his salary...........................................................................1

QUESTION 2...................................................................................................................................1

The respective outcome reached by the courts in the case of Californian Copper Syndicate Ltd

V Harris........................................................................................................................................1

QUESTION 3...................................................................................................................................3

GST consequences of the arrangement for the companies..........................................................3

QUESTION 4...................................................................................................................................4

Calculation of the net payable tax by the Melbourne Awesome Ltd for the year ended 30th

June 2019.....................................................................................................................................4

QUESTION 5...................................................................................................................................4

Discussion of ATO's Test Case Litigation Program....................................................................4

QUESTION 6...................................................................................................................................5

Calculate the net income of the partnership.................................................................................5

Allocation of net income to each of the three partner..................................................................6

Discuss relevant legislation or case law.......................................................................................6

QUESTION 1...................................................................................................................................1

Tac liability of Pablo in Australia on his salary...........................................................................1

QUESTION 2...................................................................................................................................1

The respective outcome reached by the courts in the case of Californian Copper Syndicate Ltd

V Harris........................................................................................................................................1

QUESTION 3...................................................................................................................................3

GST consequences of the arrangement for the companies..........................................................3

QUESTION 4...................................................................................................................................4

Calculation of the net payable tax by the Melbourne Awesome Ltd for the year ended 30th

June 2019.....................................................................................................................................4

QUESTION 5...................................................................................................................................4

Discussion of ATO's Test Case Litigation Program....................................................................4

QUESTION 6...................................................................................................................................5

Calculate the net income of the partnership.................................................................................5

Allocation of net income to each of the three partner..................................................................6

Discuss relevant legislation or case law.......................................................................................6

QUESTION 1

Tac liability of Pablo in Australia on his salary

Taxation is the total amount which is required to be paid by the individuals as well as

businesses on the income which is generated during the year. The legal authorities of the

countries are responsible for imposing the taxation rules on the entities and persons so that they

can pay the appropriate amount of tax on their income. If they will not be able to pay the

accurate value of taxation then it may result in punishment by law. Pablo is a Portuguese who

worked in Australia for one month and received salary fro the working. He was sent by the

company for this short period in Australia to the he can assist the project with establishment of a

branch office in the country. Salary of Pablo was credited in Portuguese bank account. During

the year total earning of Pablo was around 120000 Australian dollars. He will be responsible for

making payment of income tax on the Australian sourced income. According to the Australian

Taxation law, if a person is receiving salary for working within the country then the generated

income will be taxable within the nation. Apart from this, there is another rule related to interest,

unfranked dividend and royalty. According to this rule, these incomes will not be taxable in

Australian as these are already been taxed correctly within the country.

The taxation rate at which Pablo will be required to pay tax on the salary which was

generated by working in Australia will be 32.5%. It is the rate at which all the non-residents pay

tax in Australia on the income which is generated in Australia. It will be very important for Pablo

to pay tax on the non-resident withholding rats on the part of income which is generated in

Australia. For example, as total yearly income of Pablo is 120000 and if it will be divided in

months then for one month it will be (120000 / 12) 10000. So the taxable salary of Pablo in

Australia will be 10000. The amount of tax which will be required to be paid on this income will

be (10000 * 32.5%) 3250. It will be the total tax which tax which will be required to be paid by

Pablo on the salary. Rest of the salary will be taxable according to Portuguese taxation laws.

QUESTION 2

The respective outcome reached by the courts in the case of Californian Copper Syndicate Ltd V

Harris

The opinion which was provided by Lord Justioce Clerk uin the case of Californian

Copper Syndicate Ltd was that the principle in dealing with the questions in the assessment

1

Tac liability of Pablo in Australia on his salary

Taxation is the total amount which is required to be paid by the individuals as well as

businesses on the income which is generated during the year. The legal authorities of the

countries are responsible for imposing the taxation rules on the entities and persons so that they

can pay the appropriate amount of tax on their income. If they will not be able to pay the

accurate value of taxation then it may result in punishment by law. Pablo is a Portuguese who

worked in Australia for one month and received salary fro the working. He was sent by the

company for this short period in Australia to the he can assist the project with establishment of a

branch office in the country. Salary of Pablo was credited in Portuguese bank account. During

the year total earning of Pablo was around 120000 Australian dollars. He will be responsible for

making payment of income tax on the Australian sourced income. According to the Australian

Taxation law, if a person is receiving salary for working within the country then the generated

income will be taxable within the nation. Apart from this, there is another rule related to interest,

unfranked dividend and royalty. According to this rule, these incomes will not be taxable in

Australian as these are already been taxed correctly within the country.

The taxation rate at which Pablo will be required to pay tax on the salary which was

generated by working in Australia will be 32.5%. It is the rate at which all the non-residents pay

tax in Australia on the income which is generated in Australia. It will be very important for Pablo

to pay tax on the non-resident withholding rats on the part of income which is generated in

Australia. For example, as total yearly income of Pablo is 120000 and if it will be divided in

months then for one month it will be (120000 / 12) 10000. So the taxable salary of Pablo in

Australia will be 10000. The amount of tax which will be required to be paid on this income will

be (10000 * 32.5%) 3250. It will be the total tax which tax which will be required to be paid by

Pablo on the salary. Rest of the salary will be taxable according to Portuguese taxation laws.

QUESTION 2

The respective outcome reached by the courts in the case of Californian Copper Syndicate Ltd V

Harris

The opinion which was provided by Lord Justioce Clerk uin the case of Californian

Copper Syndicate Ltd was that the principle in dealing with the questions in the assessment

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

process of income tax was focused with obtaining greater price by owner which was higher than

the value of acquisition. According to the Schedule D of p. 166 which is related to income tax act

1842 the increased price is not the profit. Apart from this, the increased value was obtained from

the conversion of the securities which could be assessable where all the activities that are

performed are not change or realisation of investment. Additionally, it was also mentioned by

Clerk that a person or a firm which is buying or selling properties speculatively for the purpose

of making profits and dealing in this type of investment as the business and looking to make

profits. The syndicate was formed with the capital of 30000 so that the copper and other mines

could be acquired. Main purpose of it was to carry on the commercial, trading, mercantile and

financing business. There are various purposes of the entity that are pointing at the highly

speculative execution of business. The shares which were subscribed at 24000 were realised at

28332 which were invested in the copper bearing field of US. The entity was successful in

selling property to Frensco company and cost of it was around 30000 and its payment was made

in fully paid up shares. It was the turning investment to the account which was not to be

incidental merely but it was, as the Lord President concludes that the main means of the

company for selling the property for higher cost was for the purpose of speculation. Apart from

this, it was also mentioned by Clerk that all the findings of commissioners were right.

Lord Trayner said that the aspects that were determined by commissioners were right.

Apart from this, it was also said by the Lord that it was neither the case of company selling its

property for a higher price than the price which was paid by it nor the case of changing the

investment of the capital for the purpose of attaining pecuniary advantage. Trayner said that the

sale on which advantage was gained in relation to the income tax which was required to be paid

on the same was a transaction which was related to proper trading. Apart from this, he is also

satisfied that the Appellant Company was formulated for the purpose of acquiring specific

mineral working not to work for benefit of the business. It was focused with reselling the

property at a higher profit. The purchasing price of property was 24000 and the selling value of it

was 28332. It is analysed that the entity was commenced the business shortly right after its

formulation in the year 1901 in month of February. In opinion of Trayner dos it leave impart

upon liability fro taxation that the Appellant company left its profit in hands of the entity it sold

to and took the shares of the entity as the voucher.

2

the value of acquisition. According to the Schedule D of p. 166 which is related to income tax act

1842 the increased price is not the profit. Apart from this, the increased value was obtained from

the conversion of the securities which could be assessable where all the activities that are

performed are not change or realisation of investment. Additionally, it was also mentioned by

Clerk that a person or a firm which is buying or selling properties speculatively for the purpose

of making profits and dealing in this type of investment as the business and looking to make

profits. The syndicate was formed with the capital of 30000 so that the copper and other mines

could be acquired. Main purpose of it was to carry on the commercial, trading, mercantile and

financing business. There are various purposes of the entity that are pointing at the highly

speculative execution of business. The shares which were subscribed at 24000 were realised at

28332 which were invested in the copper bearing field of US. The entity was successful in

selling property to Frensco company and cost of it was around 30000 and its payment was made

in fully paid up shares. It was the turning investment to the account which was not to be

incidental merely but it was, as the Lord President concludes that the main means of the

company for selling the property for higher cost was for the purpose of speculation. Apart from

this, it was also mentioned by Clerk that all the findings of commissioners were right.

Lord Trayner said that the aspects that were determined by commissioners were right.

Apart from this, it was also said by the Lord that it was neither the case of company selling its

property for a higher price than the price which was paid by it nor the case of changing the

investment of the capital for the purpose of attaining pecuniary advantage. Trayner said that the

sale on which advantage was gained in relation to the income tax which was required to be paid

on the same was a transaction which was related to proper trading. Apart from this, he is also

satisfied that the Appellant Company was formulated for the purpose of acquiring specific

mineral working not to work for benefit of the business. It was focused with reselling the

property at a higher profit. The purchasing price of property was 24000 and the selling value of it

was 28332. It is analysed that the entity was commenced the business shortly right after its

formulation in the year 1901 in month of February. In opinion of Trayner dos it leave impart

upon liability fro taxation that the Appellant company left its profit in hands of the entity it sold

to and took the shares of the entity as the voucher.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

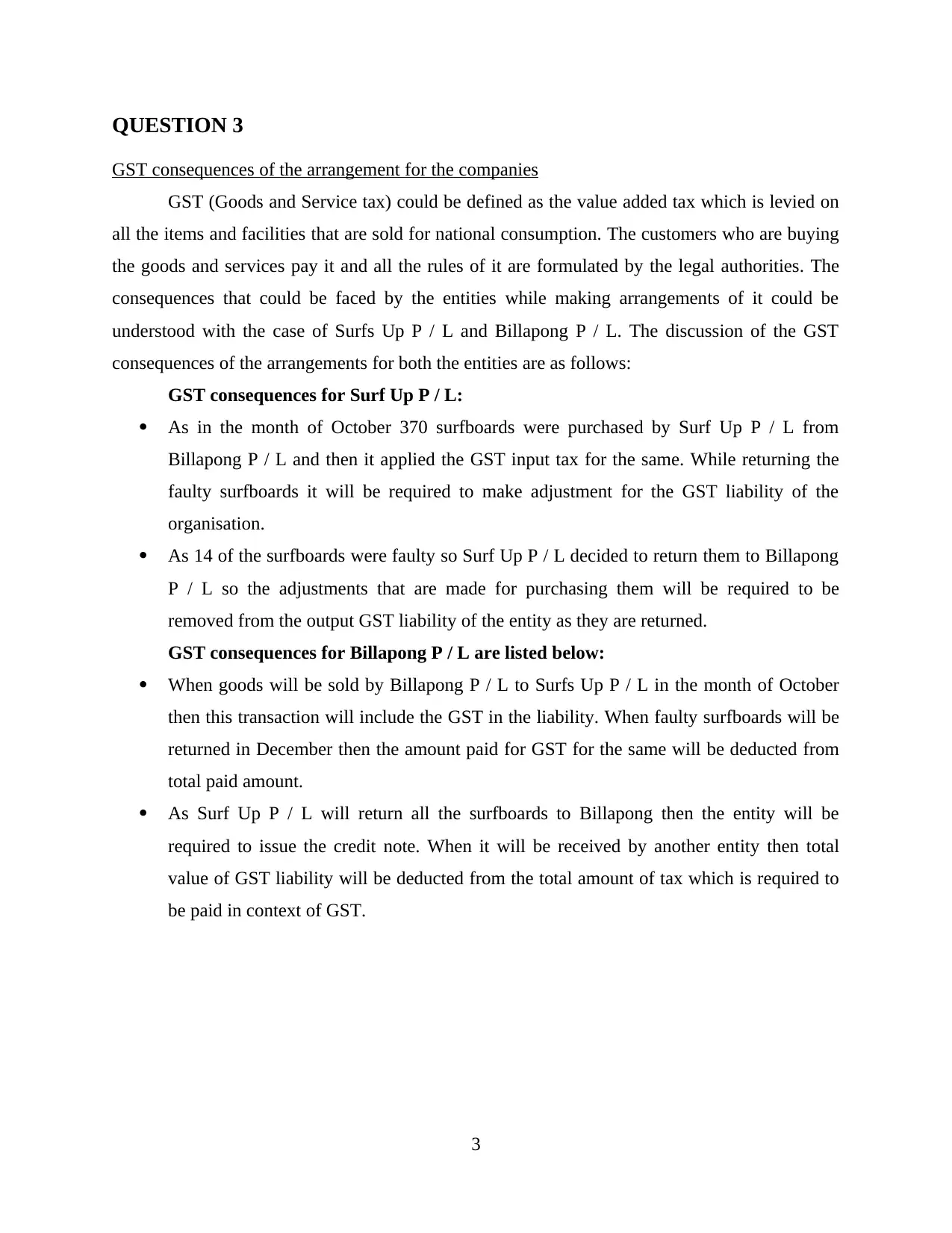

QUESTION 3

GST consequences of the arrangement for the companies

GST (Goods and Service tax) could be defined as the value added tax which is levied on

all the items and facilities that are sold for national consumption. The customers who are buying

the goods and services pay it and all the rules of it are formulated by the legal authorities. The

consequences that could be faced by the entities while making arrangements of it could be

understood with the case of Surfs Up P / L and Billapong P / L. The discussion of the GST

consequences of the arrangements for both the entities are as follows:

GST consequences for Surf Up P / L:

As in the month of October 370 surfboards were purchased by Surf Up P / L from

Billapong P / L and then it applied the GST input tax for the same. While returning the

faulty surfboards it will be required to make adjustment for the GST liability of the

organisation.

As 14 of the surfboards were faulty so Surf Up P / L decided to return them to Billapong

P / L so the adjustments that are made for purchasing them will be required to be

removed from the output GST liability of the entity as they are returned.

GST consequences for Billapong P / L are listed below:

When goods will be sold by Billapong P / L to Surfs Up P / L in the month of October

then this transaction will include the GST in the liability. When faulty surfboards will be

returned in December then the amount paid for GST for the same will be deducted from

total paid amount.

As Surf Up P / L will return all the surfboards to Billapong then the entity will be

required to issue the credit note. When it will be received by another entity then total

value of GST liability will be deducted from the total amount of tax which is required to

be paid in context of GST.

3

GST consequences of the arrangement for the companies

GST (Goods and Service tax) could be defined as the value added tax which is levied on

all the items and facilities that are sold for national consumption. The customers who are buying

the goods and services pay it and all the rules of it are formulated by the legal authorities. The

consequences that could be faced by the entities while making arrangements of it could be

understood with the case of Surfs Up P / L and Billapong P / L. The discussion of the GST

consequences of the arrangements for both the entities are as follows:

GST consequences for Surf Up P / L:

As in the month of October 370 surfboards were purchased by Surf Up P / L from

Billapong P / L and then it applied the GST input tax for the same. While returning the

faulty surfboards it will be required to make adjustment for the GST liability of the

organisation.

As 14 of the surfboards were faulty so Surf Up P / L decided to return them to Billapong

P / L so the adjustments that are made for purchasing them will be required to be

removed from the output GST liability of the entity as they are returned.

GST consequences for Billapong P / L are listed below:

When goods will be sold by Billapong P / L to Surfs Up P / L in the month of October

then this transaction will include the GST in the liability. When faulty surfboards will be

returned in December then the amount paid for GST for the same will be deducted from

total paid amount.

As Surf Up P / L will return all the surfboards to Billapong then the entity will be

required to issue the credit note. When it will be received by another entity then total

value of GST liability will be deducted from the total amount of tax which is required to

be paid in context of GST.

3

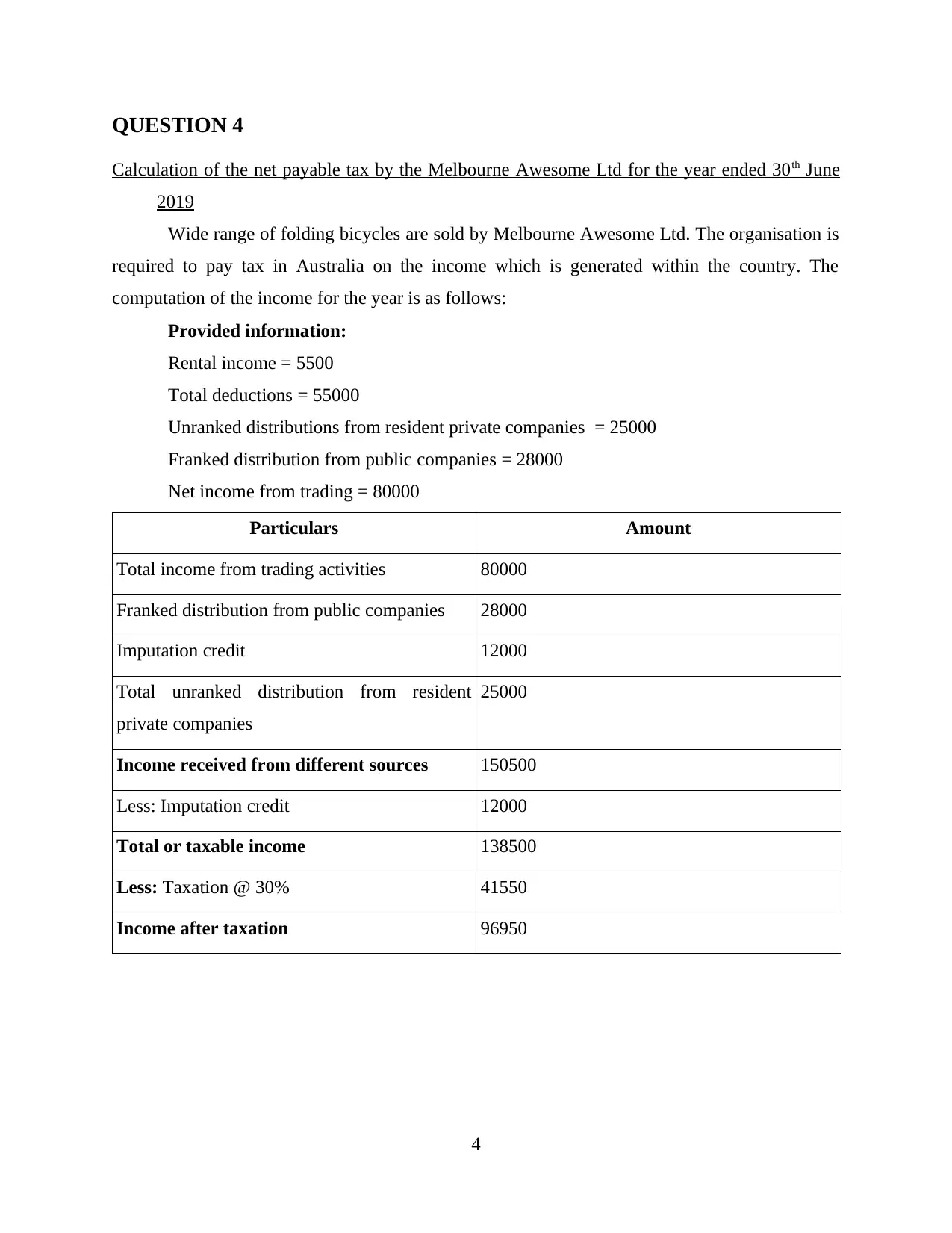

QUESTION 4

Calculation of the net payable tax by the Melbourne Awesome Ltd for the year ended 30th June

2019

Wide range of folding bicycles are sold by Melbourne Awesome Ltd. The organisation is

required to pay tax in Australia on the income which is generated within the country. The

computation of the income for the year is as follows:

Provided information:

Rental income = 5500

Total deductions = 55000

Unranked distributions from resident private companies = 25000

Franked distribution from public companies = 28000

Net income from trading = 80000

Particulars Amount

Total income from trading activities 80000

Franked distribution from public companies 28000

Imputation credit 12000

Total unranked distribution from resident

private companies

25000

Income received from different sources 150500

Less: Imputation credit 12000

Total or taxable income 138500

Less: Taxation @ 30% 41550

Income after taxation 96950

4

Calculation of the net payable tax by the Melbourne Awesome Ltd for the year ended 30th June

2019

Wide range of folding bicycles are sold by Melbourne Awesome Ltd. The organisation is

required to pay tax in Australia on the income which is generated within the country. The

computation of the income for the year is as follows:

Provided information:

Rental income = 5500

Total deductions = 55000

Unranked distributions from resident private companies = 25000

Franked distribution from public companies = 28000

Net income from trading = 80000

Particulars Amount

Total income from trading activities 80000

Franked distribution from public companies 28000

Imputation credit 12000

Total unranked distribution from resident

private companies

25000

Income received from different sources 150500

Less: Imputation credit 12000

Total or taxable income 138500

Less: Taxation @ 30% 41550

Income after taxation 96950

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

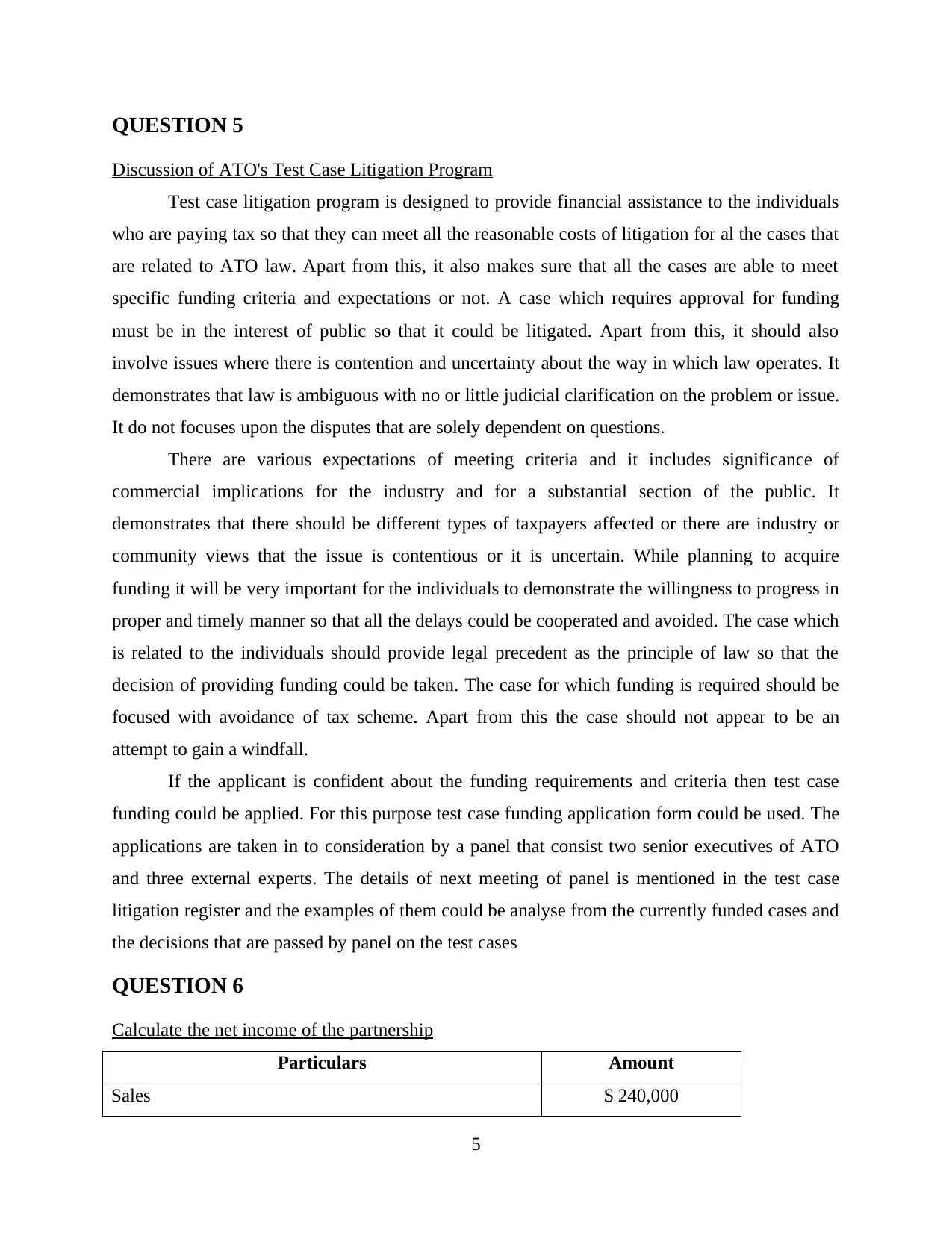

QUESTION 5

Discussion of ATO's Test Case Litigation Program

Test case litigation program is designed to provide financial assistance to the individuals

who are paying tax so that they can meet all the reasonable costs of litigation for al the cases that

are related to ATO law. Apart from this, it also makes sure that all the cases are able to meet

specific funding criteria and expectations or not. A case which requires approval for funding

must be in the interest of public so that it could be litigated. Apart from this, it should also

involve issues where there is contention and uncertainty about the way in which law operates. It

demonstrates that law is ambiguous with no or little judicial clarification on the problem or issue.

It do not focuses upon the disputes that are solely dependent on questions.

There are various expectations of meeting criteria and it includes significance of

commercial implications for the industry and for a substantial section of the public. It

demonstrates that there should be different types of taxpayers affected or there are industry or

community views that the issue is contentious or it is uncertain. While planning to acquire

funding it will be very important for the individuals to demonstrate the willingness to progress in

proper and timely manner so that all the delays could be cooperated and avoided. The case which

is related to the individuals should provide legal precedent as the principle of law so that the

decision of providing funding could be taken. The case for which funding is required should be

focused with avoidance of tax scheme. Apart from this the case should not appear to be an

attempt to gain a windfall.

If the applicant is confident about the funding requirements and criteria then test case

funding could be applied. For this purpose test case funding application form could be used. The

applications are taken in to consideration by a panel that consist two senior executives of ATO

and three external experts. The details of next meeting of panel is mentioned in the test case

litigation register and the examples of them could be analyse from the currently funded cases and

the decisions that are passed by panel on the test cases

QUESTION 6

Calculate the net income of the partnership

Particulars Amount

Sales $ 240,000

5

Discussion of ATO's Test Case Litigation Program

Test case litigation program is designed to provide financial assistance to the individuals

who are paying tax so that they can meet all the reasonable costs of litigation for al the cases that

are related to ATO law. Apart from this, it also makes sure that all the cases are able to meet

specific funding criteria and expectations or not. A case which requires approval for funding

must be in the interest of public so that it could be litigated. Apart from this, it should also

involve issues where there is contention and uncertainty about the way in which law operates. It

demonstrates that law is ambiguous with no or little judicial clarification on the problem or issue.

It do not focuses upon the disputes that are solely dependent on questions.

There are various expectations of meeting criteria and it includes significance of

commercial implications for the industry and for a substantial section of the public. It

demonstrates that there should be different types of taxpayers affected or there are industry or

community views that the issue is contentious or it is uncertain. While planning to acquire

funding it will be very important for the individuals to demonstrate the willingness to progress in

proper and timely manner so that all the delays could be cooperated and avoided. The case which

is related to the individuals should provide legal precedent as the principle of law so that the

decision of providing funding could be taken. The case for which funding is required should be

focused with avoidance of tax scheme. Apart from this the case should not appear to be an

attempt to gain a windfall.

If the applicant is confident about the funding requirements and criteria then test case

funding could be applied. For this purpose test case funding application form could be used. The

applications are taken in to consideration by a panel that consist two senior executives of ATO

and three external experts. The details of next meeting of panel is mentioned in the test case

litigation register and the examples of them could be analyse from the currently funded cases and

the decisions that are passed by panel on the test cases

QUESTION 6

Calculate the net income of the partnership

Particulars Amount

Sales $ 240,000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

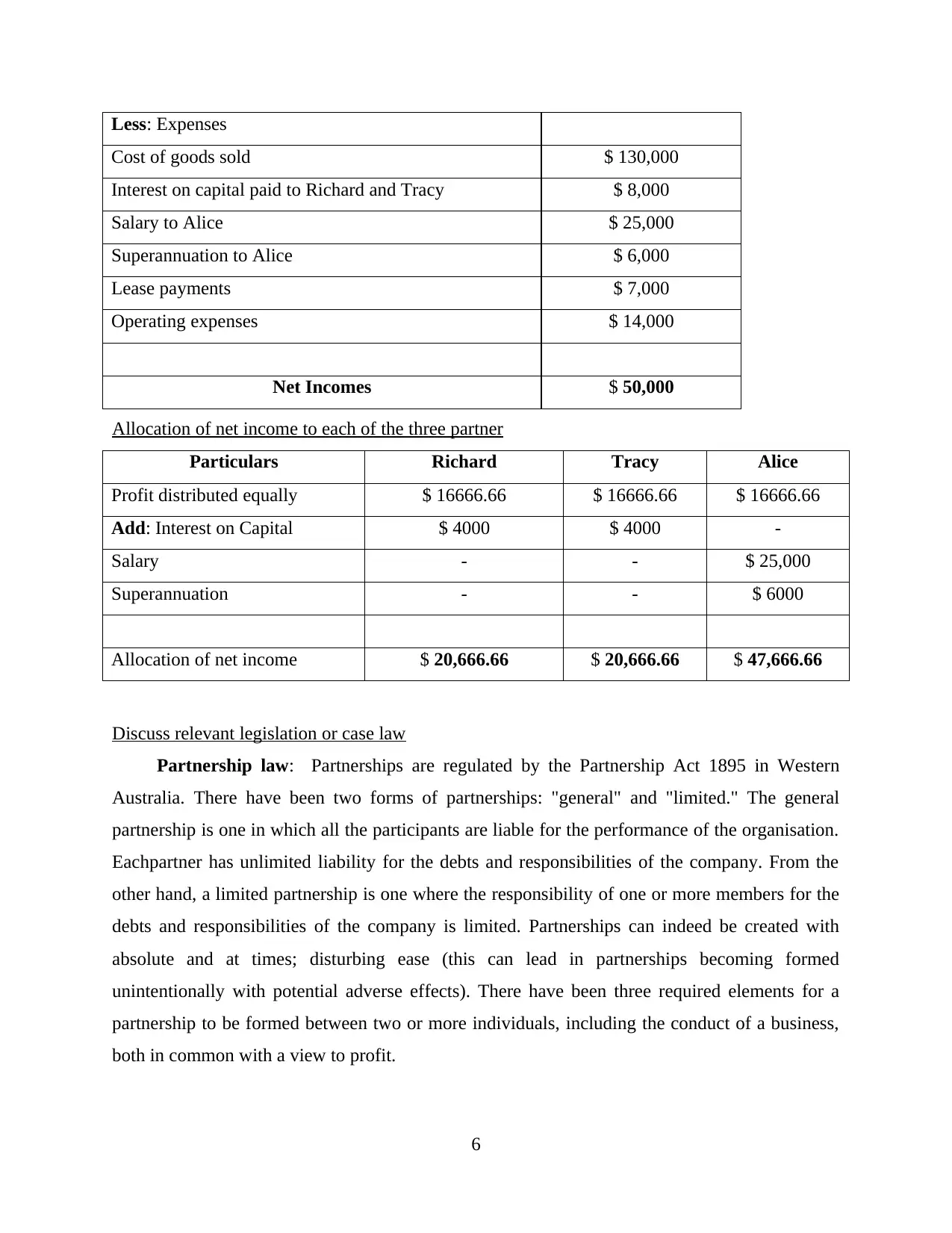

Less: Expenses

Cost of goods sold $ 130,000

Interest on capital paid to Richard and Tracy $ 8,000

Salary to Alice $ 25,000

Superannuation to Alice $ 6,000

Lease payments $ 7,000

Operating expenses $ 14,000

Net Incomes $ 50,000

Allocation of net income to each of the three partner

Particulars Richard Tracy Alice

Profit distributed equally $ 16666.66 $ 16666.66 $ 16666.66

Add: Interest on Capital $ 4000 $ 4000 -

Salary - - $ 25,000

Superannuation - - $ 6000

Allocation of net income $ 20,666.66 $ 20,666.66 $ 47,666.66

Discuss relevant legislation or case law

Partnership law: Partnerships are regulated by the Partnership Act 1895 in Western

Australia. There have been two forms of partnerships: "general" and "limited." The general

partnership is one in which all the participants are liable for the performance of the organisation.

Eachpartner has unlimited liability for the debts and responsibilities of the company. From the

other hand, a limited partnership is one where the responsibility of one or more members for the

debts and responsibilities of the company is limited. Partnerships can indeed be created with

absolute and at times; disturbing ease (this can lead in partnerships becoming formed

unintentionally with potential adverse effects). There have been three required elements for a

partnership to be formed between two or more individuals, including the conduct of a business,

both in common with a view to profit.

6

Cost of goods sold $ 130,000

Interest on capital paid to Richard and Tracy $ 8,000

Salary to Alice $ 25,000

Superannuation to Alice $ 6,000

Lease payments $ 7,000

Operating expenses $ 14,000

Net Incomes $ 50,000

Allocation of net income to each of the three partner

Particulars Richard Tracy Alice

Profit distributed equally $ 16666.66 $ 16666.66 $ 16666.66

Add: Interest on Capital $ 4000 $ 4000 -

Salary - - $ 25,000

Superannuation - - $ 6000

Allocation of net income $ 20,666.66 $ 20,666.66 $ 47,666.66

Discuss relevant legislation or case law

Partnership law: Partnerships are regulated by the Partnership Act 1895 in Western

Australia. There have been two forms of partnerships: "general" and "limited." The general

partnership is one in which all the participants are liable for the performance of the organisation.

Eachpartner has unlimited liability for the debts and responsibilities of the company. From the

other hand, a limited partnership is one where the responsibility of one or more members for the

debts and responsibilities of the company is limited. Partnerships can indeed be created with

absolute and at times; disturbing ease (this can lead in partnerships becoming formed

unintentionally with potential adverse effects). There have been three required elements for a

partnership to be formed between two or more individuals, including the conduct of a business,

both in common with a view to profit.

6

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.