Taxation Law Assignment: Taxation Law Case Study Analysis, Australia

VerifiedAdded on 2022/12/27

|11

|2538

|83

Homework Assignment

AI Summary

This taxation law assignment provides a comprehensive analysis of Australian taxation principles, covering key aspects such as income tax assessment, capital gains tax (CGT), and the responsibilities of tax agents. The assignment delves into specific scenarios, including double taxation, the application of CGT to property transactions, and the deductibility of business expenses. It examines relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and explores case law to determine tax outcomes. Furthermore, the assignment addresses the role of the Australian Taxation Office (ATO) and ethical considerations for tax advisors. The assignment includes analysis of articles related to tax avoidance and policy, and concludes with a discussion of the tax advisor's responsibilities in advising clients on taxation matters.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Part 1:.....................................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Answer to part 2:........................................................................................................................2

Answer to question 4:.................................................................................................................2

Answer to question 5:.................................................................................................................2

Answer to question 6:.................................................................................................................2

Answer to question 7:.................................................................................................................2

Table of Contents

Answer to question 1:.................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Part 1:.....................................................................................................................................2

Requirement a:.......................................................................................................................2

Requirement b:.......................................................................................................................2

Answer to part 2:........................................................................................................................2

Answer to question 4:.................................................................................................................2

Answer to question 5:.................................................................................................................2

Answer to question 6:.................................................................................................................2

Answer to question 7:.................................................................................................................2

2TAXATION LAW

Answer to question 1:

Requirement a:

The legislative power of Australia is widely spread between the states and common

wealth and the country is seen as the federation. The section “Section 51 (ii)” provides and

give description about the power of commonwealth. This particular section allows the

common wealth power to make the laws concerning the taxation without making any kind of

differentiation between the states. The substance that is considered when commencing the

“Section 51” is that the commonwealth is entrusted with the power to impose tax on the

states with such substance providing the explanation that they are subjected to constitution

and comes with the right for power (Graetz & Warren, 2016). In addition to this, “section

90” gives an explanation of the excise duties which the Commonwealth imposes and

application of tax on custom.

Requirement b:

The government of Australia is responsible for making any progress in the policy of

taxation along with the application of the taxation rest in the hand of minister of treasury. The

crucial role in the process of legislation and formation of policy of taxation is played by ATO

(Australian taxation office) and such role reflects the policies and law interdependence and

taxation system in the aspects of managerial role. Execution of all such system and policies

along making all the administrative arrangement is done by ATO (Daniel et al., 2016).

Moreover, they are also entrusted with the responsibility of educating the tax payer about

their rights and duties toward taxation.

In the event of determining the cases that have significant federal influence, the

application of the taxation and its interpretation is done by the High court of Australia along

Answer to question 1:

Requirement a:

The legislative power of Australia is widely spread between the states and common

wealth and the country is seen as the federation. The section “Section 51 (ii)” provides and

give description about the power of commonwealth. This particular section allows the

common wealth power to make the laws concerning the taxation without making any kind of

differentiation between the states. The substance that is considered when commencing the

“Section 51” is that the commonwealth is entrusted with the power to impose tax on the

states with such substance providing the explanation that they are subjected to constitution

and comes with the right for power (Graetz & Warren, 2016). In addition to this, “section

90” gives an explanation of the excise duties which the Commonwealth imposes and

application of tax on custom.

Requirement b:

The government of Australia is responsible for making any progress in the policy of

taxation along with the application of the taxation rest in the hand of minister of treasury. The

crucial role in the process of legislation and formation of policy of taxation is played by ATO

(Australian taxation office) and such role reflects the policies and law interdependence and

taxation system in the aspects of managerial role. Execution of all such system and policies

along making all the administrative arrangement is done by ATO (Daniel et al., 2016).

Moreover, they are also entrusted with the responsibility of educating the tax payer about

their rights and duties toward taxation.

In the event of determining the cases that have significant federal influence, the

application of the taxation and its interpretation is done by the High court of Australia along

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

with the hearing the appeals of court territory and questioning the applicability and validity of

law.

Answer to question 2:

In the situation of imposition of double taxation for the transaction between two

countries, taxes would be levied on one state only when business carrying out the activities in

another nation has permanent residence. In the given case, the business contract between US

manufacturers and sales representative in Australia, the tax liability would be attracted for the

profits made only to the extent of having permanent residential establishment in Australia

(Davison et al., 2017). Under section 6-10, ITAA 1997”, the amount of income that is

sourced from Australia are liabilities to be paid taxes by non resident. On other hand, taxes

should be paid by residents in Australia from all the sources according to “section 6-5, ITAA

1997”. It is only when the business activities are carried out, and the income generated from

such business are held for taxation. It is explained by the commissioner of taxation “C of T

(NSW) v Hillsdon Watts Ltd (1937)” that it is only when the actual activities are carried out,

then the income derived is held for taxation. In the given case, any amount of profits that is

made by Australia because of sales made by US manufacturers would be taxable in Australia

as per the agreement of double taxation because the profits are sourced in Australia (Cooper,

2017).

Answer to question 3:

Part 1:

Requirement a:

Implementation of capital assets is done on the assets for the event that occur after

20th September, 1985 and therefore, the implementation of the term Post-CGT and pre CGT

for the assets that are acquired after or on that date. The capital gain would be treated for

with the hearing the appeals of court territory and questioning the applicability and validity of

law.

Answer to question 2:

In the situation of imposition of double taxation for the transaction between two

countries, taxes would be levied on one state only when business carrying out the activities in

another nation has permanent residence. In the given case, the business contract between US

manufacturers and sales representative in Australia, the tax liability would be attracted for the

profits made only to the extent of having permanent residential establishment in Australia

(Davison et al., 2017). Under section 6-10, ITAA 1997”, the amount of income that is

sourced from Australia are liabilities to be paid taxes by non resident. On other hand, taxes

should be paid by residents in Australia from all the sources according to “section 6-5, ITAA

1997”. It is only when the business activities are carried out, and the income generated from

such business are held for taxation. It is explained by the commissioner of taxation “C of T

(NSW) v Hillsdon Watts Ltd (1937)” that it is only when the actual activities are carried out,

then the income derived is held for taxation. In the given case, any amount of profits that is

made by Australia because of sales made by US manufacturers would be taxable in Australia

as per the agreement of double taxation because the profits are sourced in Australia (Cooper,

2017).

Answer to question 3:

Part 1:

Requirement a:

Implementation of capital assets is done on the assets for the event that occur after

20th September, 1985 and therefore, the implementation of the term Post-CGT and pre CGT

for the assets that are acquired after or on that date. The capital gain would be treated for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

assessing the profit when the property is divided into 80 lots for selling it off. The land will

not be treated for capital gain if it is purchased prior to the introduction of GST (Tran 2016).

Requirement b:

The provision of probable revenue is applicable if the land is purchased by Indianna

1st November 1986 and property developer are sold the undivided the property. Under the

“section 6-5, ITAA 1997” the profit gained from sales when the land is not regarded as

trading stock will be treated as taxable income (Morse & Deutsch, 2015).

The sub divided block of land would be treated as trading stock if the action for 80 lots of

land is taken as the different package to the person who bid the highest. The “section 6-5,

ITAA 1997”, the tax liability would be attracted from selling of lot of land.

Amount of money generated from selling the land would be treated as capital assets

and the gain from selling such asset would be treated as capital gain. In this case, sale of land

to the property developer and the gain derived from selling such land would be treated as

taxable income and such income would be subjected to GST (Mitchell et al., 2016).

Answer to part 2:

Scenario a:

The subdivision of land that would realise the capital asset would be regarded as the

capital asset and the same would be considered for developing the business. The sold land

will be treated as capital asset and the profits derived from it would be taxable in accordance

with the “section 6-5, ITAA 1997”.

Scenario b:

The subdivided land would be treated as trading stock from the data of

commencement of business and the disposal of land is done based on market value. The

assessing the profit when the property is divided into 80 lots for selling it off. The land will

not be treated for capital gain if it is purchased prior to the introduction of GST (Tran 2016).

Requirement b:

The provision of probable revenue is applicable if the land is purchased by Indianna

1st November 1986 and property developer are sold the undivided the property. Under the

“section 6-5, ITAA 1997” the profit gained from sales when the land is not regarded as

trading stock will be treated as taxable income (Morse & Deutsch, 2015).

The sub divided block of land would be treated as trading stock if the action for 80 lots of

land is taken as the different package to the person who bid the highest. The “section 6-5,

ITAA 1997”, the tax liability would be attracted from selling of lot of land.

Amount of money generated from selling the land would be treated as capital assets

and the gain from selling such asset would be treated as capital gain. In this case, sale of land

to the property developer and the gain derived from selling such land would be treated as

taxable income and such income would be subjected to GST (Mitchell et al., 2016).

Answer to part 2:

Scenario a:

The subdivision of land that would realise the capital asset would be regarded as the

capital asset and the same would be considered for developing the business. The sold land

will be treated as capital asset and the profits derived from it would be taxable in accordance

with the “section 6-5, ITAA 1997”.

Scenario b:

The subdivided land would be treated as trading stock from the data of

commencement of business and the disposal of land is done based on market value. The

5TAXATION LAW

disposal of land is done using the commercial approach which would make the tax payer to

make tax payment. As per “section 6-5, ITAA 1997”, the income that is derived would be

treated for the taxation purpose.

Scenario c:

The profit generated by Indianna from selling the property development land by sub

dividing it would be taxable.

Answer to question 4:

If any business operations generate loss or profit which is considered for allowable

deduction post termination of business expense that helps in producing taxable income. Tax

payer can obtained tax deductions when settling the dispute with customers for wrongly

supplying the defected conveyor belt as explained by the “FCT v Placer Pacific

Management Pty Ltd (1995)”. The assessable income is produced from business in the event

of ongoing expenditure. In the given case, Amity can claim for allowance deduction

according to “section 8-1, ITAA 1997” for interest on loan (Wurth & Braithwaite, 2016).

This was because taxable income was produced for the outgoing agreement of loan.

Answer to question 5:

For the assets that are purchased after or on 20th September 1985, implementation of

capital assets is done on the same. According to “section 104-10 (1)) of the ITAA 1997”,

when the assets are sold then there is occurrence of CGT events and there is exemption of tax

payer from paying taxes. Maurice can claim for exemption fully as the home was not used for

generating income.

In addition to this, the shares purchased by her for $15,000 in 1984 was disposed for

$19,000 and it can be viewed as the assets that is exempted from CGT. Personal used assets

are the assets that are used for enjoyment and private usage according to “section 108-20 (2),

disposal of land is done using the commercial approach which would make the tax payer to

make tax payment. As per “section 6-5, ITAA 1997”, the income that is derived would be

treated for the taxation purpose.

Scenario c:

The profit generated by Indianna from selling the property development land by sub

dividing it would be taxable.

Answer to question 4:

If any business operations generate loss or profit which is considered for allowable

deduction post termination of business expense that helps in producing taxable income. Tax

payer can obtained tax deductions when settling the dispute with customers for wrongly

supplying the defected conveyor belt as explained by the “FCT v Placer Pacific

Management Pty Ltd (1995)”. The assessable income is produced from business in the event

of ongoing expenditure. In the given case, Amity can claim for allowance deduction

according to “section 8-1, ITAA 1997” for interest on loan (Wurth & Braithwaite, 2016).

This was because taxable income was produced for the outgoing agreement of loan.

Answer to question 5:

For the assets that are purchased after or on 20th September 1985, implementation of

capital assets is done on the same. According to “section 104-10 (1)) of the ITAA 1997”,

when the assets are sold then there is occurrence of CGT events and there is exemption of tax

payer from paying taxes. Maurice can claim for exemption fully as the home was not used for

generating income.

In addition to this, the shares purchased by her for $15,000 in 1984 was disposed for

$19,000 and it can be viewed as the assets that is exempted from CGT. Personal used assets

are the assets that are used for enjoyment and private usage according to “section 108-20 (2),

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

ITAA 1997”. Furthermore, when the cost base of using personal asset is lower than $ 10000,

then the loss or gain should be ignored according to “section 118-10 (3), ITAA 1997”. In

addition to this, furniture was also purchased by Maurice on 20th may for $ 9500 and was

disposed for $ 5000. In the given case, Maurice should ignore the capital loss from selling off

the assets because the cost is lower than $ 10000.

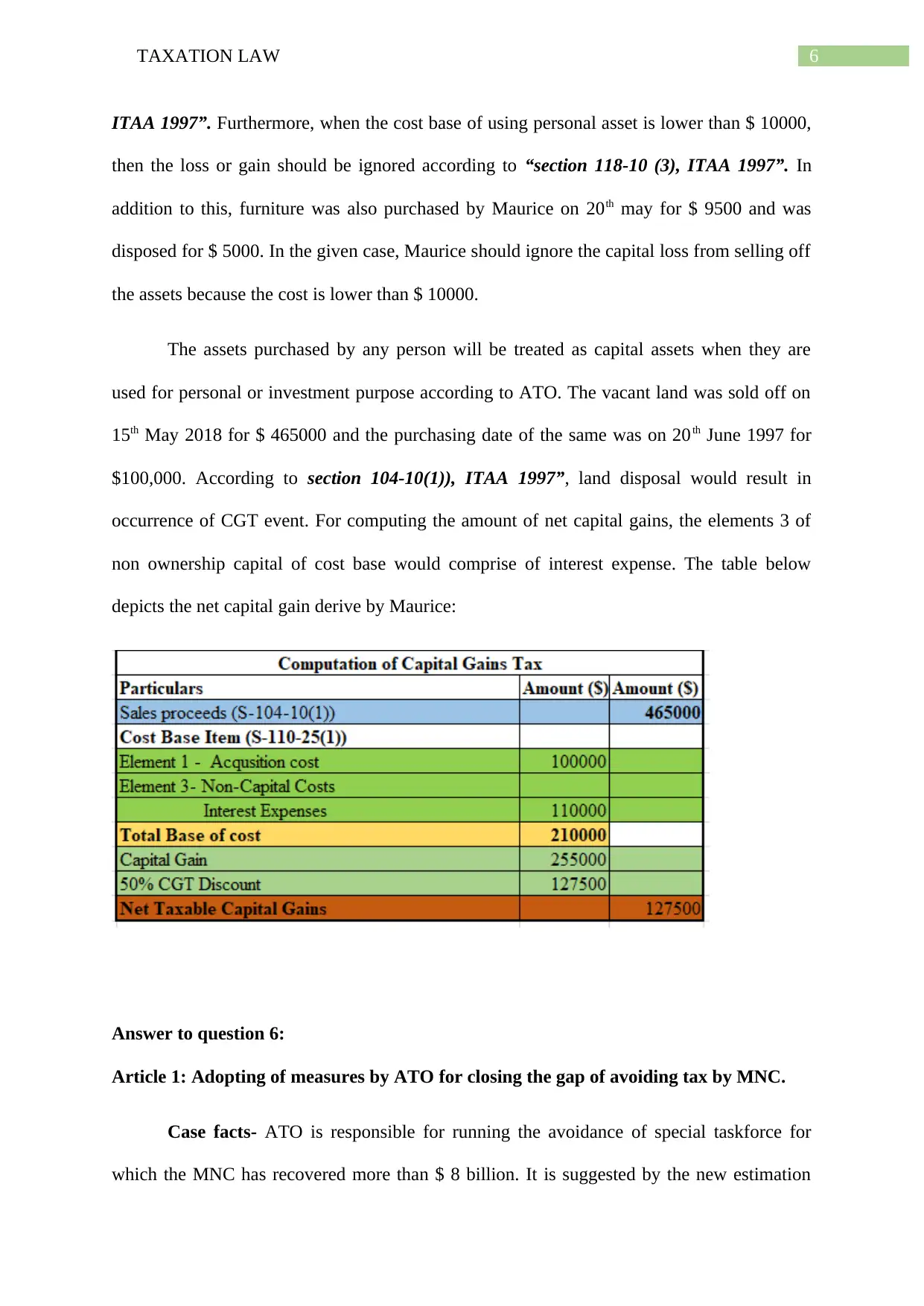

The assets purchased by any person will be treated as capital assets when they are

used for personal or investment purpose according to ATO. The vacant land was sold off on

15th May 2018 for $ 465000 and the purchasing date of the same was on 20th June 1997 for

$100,000. According to section 104-10(1)), ITAA 1997”, land disposal would result in

occurrence of CGT event. For computing the amount of net capital gains, the elements 3 of

non ownership capital of cost base would comprise of interest expense. The table below

depicts the net capital gain derive by Maurice:

Answer to question 6:

Article 1: Adopting of measures by ATO for closing the gap of avoiding tax by MNC.

Case facts- ATO is responsible for running the avoidance of special taskforce for

which the MNC has recovered more than $ 8 billion. It is suggested by the new estimation

ITAA 1997”. Furthermore, when the cost base of using personal asset is lower than $ 10000,

then the loss or gain should be ignored according to “section 118-10 (3), ITAA 1997”. In

addition to this, furniture was also purchased by Maurice on 20th may for $ 9500 and was

disposed for $ 5000. In the given case, Maurice should ignore the capital loss from selling off

the assets because the cost is lower than $ 10000.

The assets purchased by any person will be treated as capital assets when they are

used for personal or investment purpose according to ATO. The vacant land was sold off on

15th May 2018 for $ 465000 and the purchasing date of the same was on 20th June 1997 for

$100,000. According to section 104-10(1)), ITAA 1997”, land disposal would result in

occurrence of CGT event. For computing the amount of net capital gains, the elements 3 of

non ownership capital of cost base would comprise of interest expense. The table below

depicts the net capital gain derive by Maurice:

Answer to question 6:

Article 1: Adopting of measures by ATO for closing the gap of avoiding tax by MNC.

Case facts- ATO is responsible for running the avoidance of special taskforce for

which the MNC has recovered more than $ 8 billion. It is suggested by the new estimation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

that the entire liabilities are met by more than 95% of the companies. In addition to this, it is

also suggested that 29% of the company is paid by the tax payers and the top 100 companies

obtain 42% of the tax.

Explaining the concepts of taxation concisely- The article presents the trend

regarding the tax gap that the gap is getting reduced. Tax gap has improved considerably as

the majority of largest companies have paid approximately of $ 44 million as revenue of tax

in Australia (Sakurai & Braithwaite, 2019).

Description of connection between indicators and concepts of good policy of

taxation:

It is found that the companies in Australia have greater compliance along with the

country by country reporting and laws on multinational tax avoidance and laws that are anti

hybrid (Woellner et al., 2016).

Article 2: Removing inequitable enquiry using ATO measures

Case fact-

The parliament found the removal of refundable franking credit by the labours for the

self managed super funds to be highly defective and inequitable.

Explaining the concepts of taxation concisely- The removal of refundable franking

should be removed as per the recommendation of committee. Reformation in the policy

would be treated as the portion of package that resulting from the transformation of wholesale

tax.

Description of connection between indicators and concepts of good policy of taxation:

that the entire liabilities are met by more than 95% of the companies. In addition to this, it is

also suggested that 29% of the company is paid by the tax payers and the top 100 companies

obtain 42% of the tax.

Explaining the concepts of taxation concisely- The article presents the trend

regarding the tax gap that the gap is getting reduced. Tax gap has improved considerably as

the majority of largest companies have paid approximately of $ 44 million as revenue of tax

in Australia (Sakurai & Braithwaite, 2019).

Description of connection between indicators and concepts of good policy of

taxation:

It is found that the companies in Australia have greater compliance along with the

country by country reporting and laws on multinational tax avoidance and laws that are anti

hybrid (Woellner et al., 2016).

Article 2: Removing inequitable enquiry using ATO measures

Case fact-

The parliament found the removal of refundable franking credit by the labours for the

self managed super funds to be highly defective and inequitable.

Explaining the concepts of taxation concisely- The removal of refundable franking

should be removed as per the recommendation of committee. Reformation in the policy

would be treated as the portion of package that resulting from the transformation of wholesale

tax.

Description of connection between indicators and concepts of good policy of taxation:

8TAXATION LAW

It is clearly explained in the article that the moderate income was earned because of

the unfair policy. The criticism is stated by the parliament members after the inquiry is

reported that the whole exercise that resulted in wasting of money of tax payers.

Answer to question 7:

The tax advisor has the responsibility of making the tax payer aware with all the

taxation laws so that he performs his duties by adhering to all the regulations.

The leveraging points for customer are developed with the help of advisors in the

form of superannuation and vital intermediary taxation system.

Tax payers receive assistance from their advisors when it comes to managing the

taxation affairs by clarifying about the duties and rights of the clients.

Clients are suggested on development of compliance strategies and managing their

risk in a batter manner with the help of tax agents for exchanging the ideas and

transparent information communication.

It is clearly explained in the article that the moderate income was earned because of

the unfair policy. The criticism is stated by the parliament members after the inquiry is

reported that the whole exercise that resulted in wasting of money of tax payers.

Answer to question 7:

The tax advisor has the responsibility of making the tax payer aware with all the

taxation laws so that he performs his duties by adhering to all the regulations.

The leveraging points for customer are developed with the help of advisors in the

form of superannuation and vital intermediary taxation system.

Tax payers receive assistance from their advisors when it comes to managing the

taxation affairs by clarifying about the duties and rights of the clients.

Clients are suggested on development of compliance strategies and managing their

risk in a batter manner with the help of tax agents for exchanging the ideas and

transparent information communication.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References list:

Cooper, G. S. (2017). Implementing BEPS, or Maybe Not—the Australian Experience One

Year On. New Zealand Law Review, 2017(2), 145-174.

Daniel, P., Keen, M., Świstak, A., & Thuronyi, V. (Eds.). (2016). International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davison, M., Monotti, A., & Wiseman, L. (2015). Australian intellectual property law.

Cambridge University Press.

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Graetz, M. J., & Warren, A. C. (2016). Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, 16-36.

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and

Securities Law Journal, 33, 555-580.

Mitchell, R., O'Donnell, A., Marshall, S., & Ramsay, I. (2016). Law, corporate governance

and partnerships at work: a study of Australian regulatory style and business

practice. Routledge.

Morse, S. C., & Deutsch, R. (2015). Tax Anti-Avoidance Law in Australia and the United

States. The International Lawyer, 49(2), 111-148.

References list:

Cooper, G. S. (2017). Implementing BEPS, or Maybe Not—the Australian Experience One

Year On. New Zealand Law Review, 2017(2), 145-174.

Daniel, P., Keen, M., Świstak, A., & Thuronyi, V. (Eds.). (2016). International Taxation and

the Extractive Industries: Resources Without Borders. Taylor & Francis.

Davison, M., Monotti, A., & Wiseman, L. (2015). Australian intellectual property law.

Cambridge University Press.

Freudenberg, B., Chardon, T., Brimble, M., & Isle, M. B. (2017). Tax literacy of Australian

small businesses. J. Austl. Tax'n, 19, 21.

Graetz, M. J., & Warren, A. C. (2016). Integration of corporate and shareholder

taxes. National Tax Journal, Forthcoming, 16-36.

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and

Securities Law Journal, 33, 555-580.

Mitchell, R., O'Donnell, A., Marshall, S., & Ramsay, I. (2016). Law, corporate governance

and partnerships at work: a study of Australian regulatory style and business

practice. Routledge.

Morse, S. C., & Deutsch, R. (2015). Tax Anti-Avoidance Law in Australia and the United

States. The International Lawyer, 49(2), 111-148.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Sakurai, Y., & Braithwaite, V. (2019). Taxpayers' perceptions of the ideal tax adviser:

Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Tran-Nam, B. (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan, London.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Wurth, E., & Braithwaite, V. (2016). Tax practitioners and tax avoidance: gaming through

authorities, cultures and markets. RegNet Research Paper, (2016/119).

Sakurai, Y., & Braithwaite, V. (2019). Taxpayers' perceptions of the ideal tax adviser:

Playing safe or saving dollars?. Centre for Tax System Integrity (CTSI), Research

School of Social Sciences, The Australian National University.

Tran-Nam, B. (2016). Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-

44). Palgrave Macmillan, London.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Wurth, E., & Braithwaite, V. (2016). Tax practitioners and tax avoidance: gaming through

authorities, cultures and markets. RegNet Research Paper, (2016/119).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.