Taxation Assignment: Analysis of Australian Taxation Laws

VerifiedAdded on 2021/02/19

|9

|2527

|19

Homework Assignment

AI Summary

This assignment delves into various aspects of Australian taxation law, examining the taxation consequences of different financial transactions. It begins by defining capital gains tax and illustrating its application through several scenarios involving the sale of assets like antique impressions, historical sculptures, and jewelry, calculating the taxable capital gains based on ATO provisions and indexation rules. The assignment then explores individual income tax, specifically addressing the tax implications of income derived from writing and selling a book, including income from contracts, sales, and interviews, and how the ATO treats such income. Furthermore, it analyzes a loan scenario between family members, detailing the tax implications of interest income received on a loan, the importance of evidence like bank statements, and the taxability of the interest earned. The conclusion summarizes the key takeaways, emphasizing the role of the Australian Taxation Office (ATO) in managing tax payments and the application of tax principles to capital gains, income from various sources, and family loans.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................3

Question 3........................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................1

Question 1........................................................................................................................................1

Question 2........................................................................................................................................3

Question 3........................................................................................................................................5

CONCLUSION................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Taxation refers to a way of Government for collecting funds from general public and

several corporate entities so as to manage and finance all the expenditure for welfare of whole

country. In Australia, there is a separate body namely Australian Taxation Office (ATO) that

deals with developing various laws, rules and regulations that would be applicable over each

individual business, and other body corporate who performs several activities for the purpose of

earning profit. The present study includes taxation consequences of various taxation laws on

various transaction incurred by a business entities or individuals. It also shows a sum to be paid

by them as tax to the government for the gain generated through those transactions. It also shows

numerous provisions through which the the amount of tax shall be calculated for the individual

or body corporate.

Question 1

Capital gain

The term capital gain refers to excess of sum received by an individual or a body

corporate as a sale proceed over the cost of purchase if such asset. The Australian Taxation

Office has developed separate provisions for determining the taxable amount of such capital

gain.

Capital gain tax

Capital gain is a tax that is levied upon a business entity or an individual when they sale

any asset and generates profit from the sales (Brown, 2018). As per the provisions of Australian

Taxation Office, the assets under capital gain tax includes shares, any contractual rights,

personal collections such as antiques, historical properties and license, etc. in this order, income

earned from the sale of such assets shall be liable to pay tax under the capital gain tax head of

Australian taxation system.

Provisions

Sale of any assets of the assets shall attract the provisions of capital gain tax towards it.

The capital gain tax includes several clauses for sale of different assets in diofferent situations.

An individual or a company or any other corporation who sales its assets, shall needs to consider

all such provisions through for the purpose of calculating the amount of capital gain tax levied

upon such sale.

1

Taxation refers to a way of Government for collecting funds from general public and

several corporate entities so as to manage and finance all the expenditure for welfare of whole

country. In Australia, there is a separate body namely Australian Taxation Office (ATO) that

deals with developing various laws, rules and regulations that would be applicable over each

individual business, and other body corporate who performs several activities for the purpose of

earning profit. The present study includes taxation consequences of various taxation laws on

various transaction incurred by a business entities or individuals. It also shows a sum to be paid

by them as tax to the government for the gain generated through those transactions. It also shows

numerous provisions through which the the amount of tax shall be calculated for the individual

or body corporate.

Question 1

Capital gain

The term capital gain refers to excess of sum received by an individual or a body

corporate as a sale proceed over the cost of purchase if such asset. The Australian Taxation

Office has developed separate provisions for determining the taxable amount of such capital

gain.

Capital gain tax

Capital gain is a tax that is levied upon a business entity or an individual when they sale

any asset and generates profit from the sales (Brown, 2018). As per the provisions of Australian

Taxation Office, the assets under capital gain tax includes shares, any contractual rights,

personal collections such as antiques, historical properties and license, etc. in this order, income

earned from the sale of such assets shall be liable to pay tax under the capital gain tax head of

Australian taxation system.

Provisions

Sale of any assets of the assets shall attract the provisions of capital gain tax towards it.

The capital gain tax includes several clauses for sale of different assets in diofferent situations.

An individual or a company or any other corporation who sales its assets, shall needs to consider

all such provisions through for the purpose of calculating the amount of capital gain tax levied

upon such sale.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

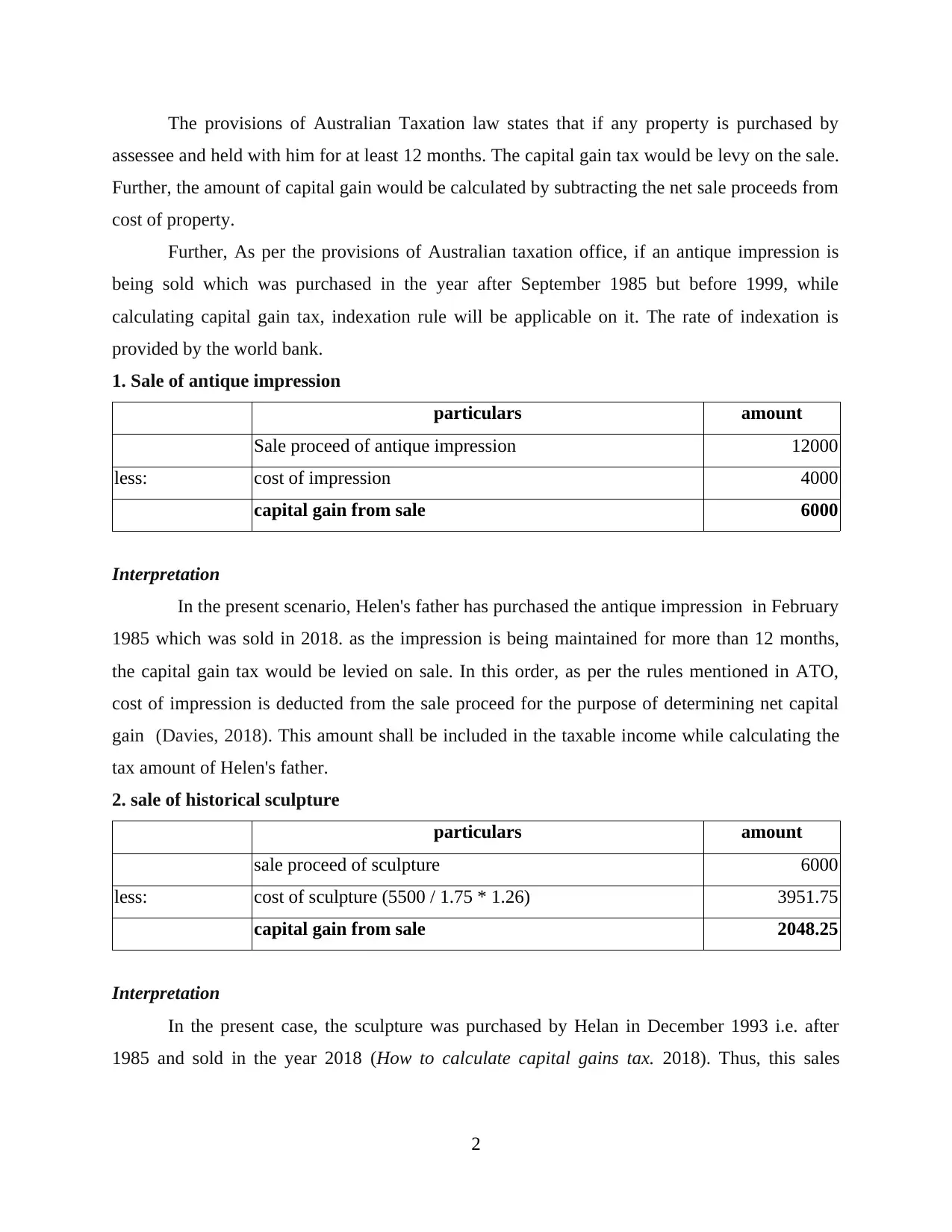

The provisions of Australian Taxation law states that if any property is purchased by

assessee and held with him for at least 12 months. The capital gain tax would be levy on the sale.

Further, the amount of capital gain would be calculated by subtracting the net sale proceeds from

cost of property.

Further, As per the provisions of Australian taxation office, if an antique impression is

being sold which was purchased in the year after September 1985 but before 1999, while

calculating capital gain tax, indexation rule will be applicable on it. The rate of indexation is

provided by the world bank.

1. Sale of antique impression

particulars amount

Sale proceed of antique impression 12000

less: cost of impression 4000

capital gain from sale 6000

Interpretation

In the present scenario, Helen's father has purchased the antique impression in February

1985 which was sold in 2018. as the impression is being maintained for more than 12 months,

the capital gain tax would be levied on sale. In this order, as per the rules mentioned in ATO,

cost of impression is deducted from the sale proceed for the purpose of determining net capital

gain (Davies, 2018). This amount shall be included in the taxable income while calculating the

tax amount of Helen's father.

2. sale of historical sculpture

particulars amount

sale proceed of sculpture 6000

less: cost of sculpture (5500 / 1.75 * 1.26) 3951.75

capital gain from sale 2048.25

Interpretation

In the present case, the sculpture was purchased by Helan in December 1993 i.e. after

1985 and sold in the year 2018 (How to calculate capital gains tax. 2018). Thus, this sales

2

assessee and held with him for at least 12 months. The capital gain tax would be levy on the sale.

Further, the amount of capital gain would be calculated by subtracting the net sale proceeds from

cost of property.

Further, As per the provisions of Australian taxation office, if an antique impression is

being sold which was purchased in the year after September 1985 but before 1999, while

calculating capital gain tax, indexation rule will be applicable on it. The rate of indexation is

provided by the world bank.

1. Sale of antique impression

particulars amount

Sale proceed of antique impression 12000

less: cost of impression 4000

capital gain from sale 6000

Interpretation

In the present scenario, Helen's father has purchased the antique impression in February

1985 which was sold in 2018. as the impression is being maintained for more than 12 months,

the capital gain tax would be levied on sale. In this order, as per the rules mentioned in ATO,

cost of impression is deducted from the sale proceed for the purpose of determining net capital

gain (Davies, 2018). This amount shall be included in the taxable income while calculating the

tax amount of Helen's father.

2. sale of historical sculpture

particulars amount

sale proceed of sculpture 6000

less: cost of sculpture (5500 / 1.75 * 1.26) 3951.75

capital gain from sale 2048.25

Interpretation

In the present case, the sculpture was purchased by Helan in December 1993 i.e. after

1985 and sold in the year 2018 (How to calculate capital gains tax. 2018). Thus, this sales

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

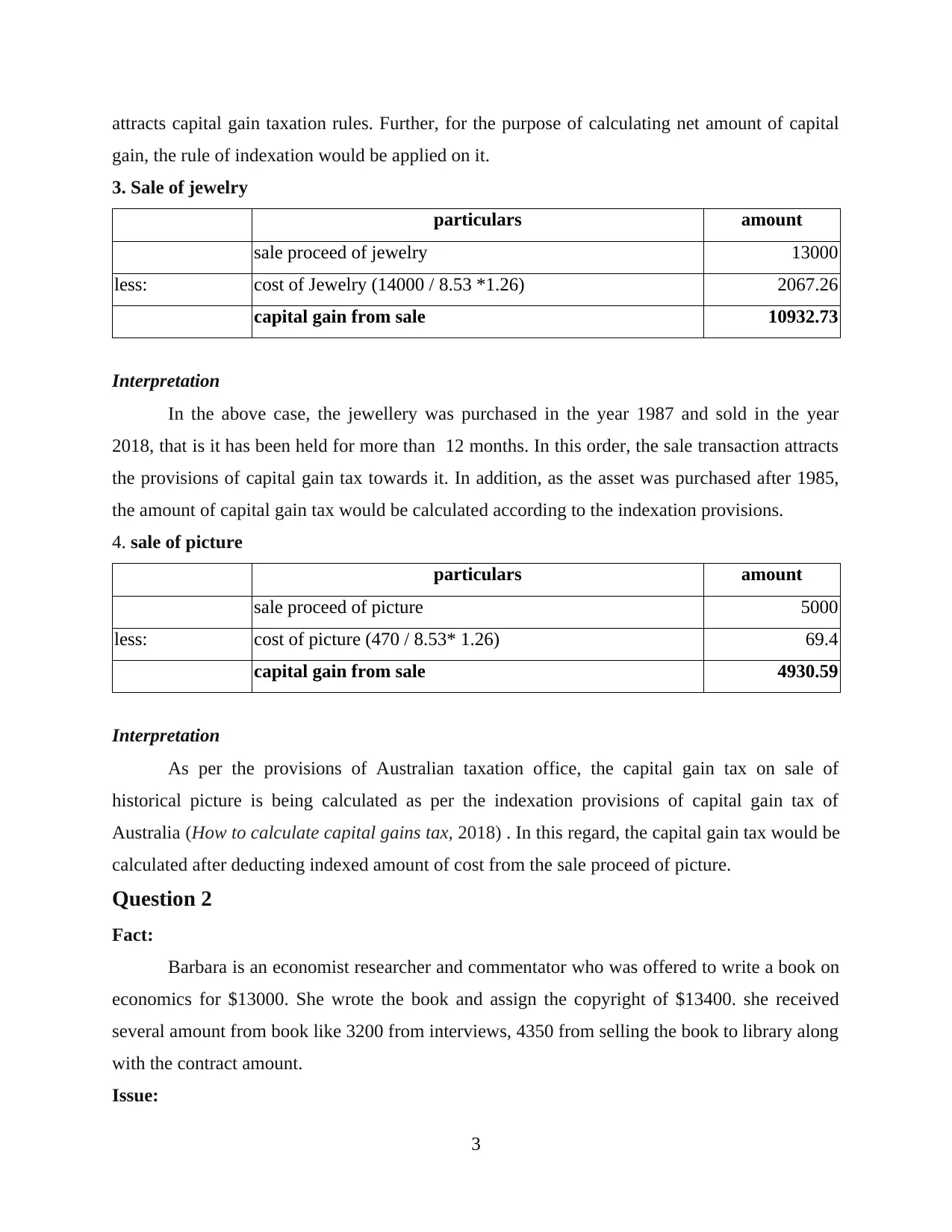

attracts capital gain taxation rules. Further, for the purpose of calculating net amount of capital

gain, the rule of indexation would be applied on it.

3. Sale of jewelry

particulars amount

sale proceed of jewelry 13000

less: cost of Jewelry (14000 / 8.53 *1.26) 2067.26

capital gain from sale 10932.73

Interpretation

In the above case, the jewellery was purchased in the year 1987 and sold in the year

2018, that is it has been held for more than 12 months. In this order, the sale transaction attracts

the provisions of capital gain tax towards it. In addition, as the asset was purchased after 1985,

the amount of capital gain tax would be calculated according to the indexation provisions.

4. sale of picture

particulars amount

sale proceed of picture 5000

less: cost of picture (470 / 8.53* 1.26) 69.4

capital gain from sale 4930.59

Interpretation

As per the provisions of Australian taxation office, the capital gain tax on sale of

historical picture is being calculated as per the indexation provisions of capital gain tax of

Australia (How to calculate capital gains tax, 2018) . In this regard, the capital gain tax would be

calculated after deducting indexed amount of cost from the sale proceed of picture.

Question 2

Fact:

Barbara is an economist researcher and commentator who was offered to write a book on

economics for $13000. She wrote the book and assign the copyright of $13400. she received

several amount from book like 3200 from interviews, 4350 from selling the book to library along

with the contract amount.

Issue:

3

gain, the rule of indexation would be applied on it.

3. Sale of jewelry

particulars amount

sale proceed of jewelry 13000

less: cost of Jewelry (14000 / 8.53 *1.26) 2067.26

capital gain from sale 10932.73

Interpretation

In the above case, the jewellery was purchased in the year 1987 and sold in the year

2018, that is it has been held for more than 12 months. In this order, the sale transaction attracts

the provisions of capital gain tax towards it. In addition, as the asset was purchased after 1985,

the amount of capital gain tax would be calculated according to the indexation provisions.

4. sale of picture

particulars amount

sale proceed of picture 5000

less: cost of picture (470 / 8.53* 1.26) 69.4

capital gain from sale 4930.59

Interpretation

As per the provisions of Australian taxation office, the capital gain tax on sale of

historical picture is being calculated as per the indexation provisions of capital gain tax of

Australia (How to calculate capital gains tax, 2018) . In this regard, the capital gain tax would be

calculated after deducting indexed amount of cost from the sale proceed of picture.

Question 2

Fact:

Barbara is an economist researcher and commentator who was offered to write a book on

economics for $13000. She wrote the book and assign the copyright of $13400. she received

several amount from book like 3200 from interviews, 4350 from selling the book to library along

with the contract amount.

Issue:

3

effect of incomes received by Barbara from publishing book on his personal income

exertion. Further, effect of such income in case the Barbara wrote the book in her spare time.

Rules:

Individual Income tax: Individual income tax refers to income tax levied upon tax

income earned by an individual within a specific time period (Harrison, 2018). All income

earned by an individual who is resident of Australia would be liable to pay tax after deducting all

the eligible expenses and tax deductible investments.

Income from sale of book: As per the provisions of Australian taxation office, if an

individual writes a book for the and generates income by selling the books into market, the

individual will be liable to pay tax on such income. Although, the person would be eligible to

deduct the expenses relating to the publish of book from the income generated from sale.

Income from hobby: The ATO has made different provisions for income generated by

performing any activity performed as hobby. ATO states that hobby is an activity which is

performed in spare time. Although, if the intention behind performing hobby is to generate profit

from it, it would be treated as business and income generated it would be taxable under

Australian taxation system.

Case law:

In Judgment by J C Kelly, Senior Member Case, if any activity is being carried out by an

assessee as a part of hobby and if he starts earning profit from it, such activity shall be treated as

a part of business (NKCX v FC of T, 2018). Further, the amount of profit generated from such

activity shall be taxable under the Australian taxation system.

Conclusion: From the analysis of above rules of Australian taxation office (ATO) and

the relevant case law, it can be concluded that as the Barbara has signed a contract of writing a

book on principles of economics, for which she has made a contract with Eco Book Ltd. Worth

$13000, she would be liable to pay tax on the income generated from the sale of book. As, she

has earned a sum from the sale of it. Further, the copy right expenses incurred by it is covered

under depreciable assets as per the provisions of ATO.

Thus, Barbara would be liable to pay tax on the total income generated from sale that is

sum of income from contract amount, sale to library and income from interview (Murray, 2018)

. In addition, the amount of depreciation for the year would be able to deduct from the income.

4

exertion. Further, effect of such income in case the Barbara wrote the book in her spare time.

Rules:

Individual Income tax: Individual income tax refers to income tax levied upon tax

income earned by an individual within a specific time period (Harrison, 2018). All income

earned by an individual who is resident of Australia would be liable to pay tax after deducting all

the eligible expenses and tax deductible investments.

Income from sale of book: As per the provisions of Australian taxation office, if an

individual writes a book for the and generates income by selling the books into market, the

individual will be liable to pay tax on such income. Although, the person would be eligible to

deduct the expenses relating to the publish of book from the income generated from sale.

Income from hobby: The ATO has made different provisions for income generated by

performing any activity performed as hobby. ATO states that hobby is an activity which is

performed in spare time. Although, if the intention behind performing hobby is to generate profit

from it, it would be treated as business and income generated it would be taxable under

Australian taxation system.

Case law:

In Judgment by J C Kelly, Senior Member Case, if any activity is being carried out by an

assessee as a part of hobby and if he starts earning profit from it, such activity shall be treated as

a part of business (NKCX v FC of T, 2018). Further, the amount of profit generated from such

activity shall be taxable under the Australian taxation system.

Conclusion: From the analysis of above rules of Australian taxation office (ATO) and

the relevant case law, it can be concluded that as the Barbara has signed a contract of writing a

book on principles of economics, for which she has made a contract with Eco Book Ltd. Worth

$13000, she would be liable to pay tax on the income generated from the sale of book. As, she

has earned a sum from the sale of it. Further, the copy right expenses incurred by it is covered

under depreciable assets as per the provisions of ATO.

Thus, Barbara would be liable to pay tax on the total income generated from sale that is

sum of income from contract amount, sale to library and income from interview (Murray, 2018)

. In addition, the amount of depreciation for the year would be able to deduct from the income.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In addition, as the provisions of ATO states that if an individual generate profits from

performing his hobby and if the motive of performing any hobby is to earn profit from it, the

income generated in through such activity shall be liable to pay tax.

Thus, in the present case scenario, if Barbara writes book for Eco Book Ltd. As hobby,

the income from sale of such book shall also be taxable as per the provisions of ATO. As such

book shall be written with a motive to generate profits from it.

Question 3

Fact:

Patrick paid assistance fee to his son David of $ 52000. the agreement was to repay the

sum at the end of 5 years of $58000. Further, there was no formal agreement or security deposit

for the amount lent. David repay the whole amount after 2 years through cheque along with 5%

interest on amount borrowed.

Issue:

To discuss the effect of agreement made on the income of Patrick.

Rules:

Income tax from interest on loan: As per the provisions of ATO, if an individual or a

body corporate provides a loan to another person, the principle amount received as repayment of

loan shall not be eligible to pay tax (Pert, Chen and Carvosso, 2018) . Although, in case, the

income received as a part of interest on such loan shall be taxable with the income of such

individual or body corporate in the assessment year in which the interest income has been

earned.

Loan provided to family members: In case, a loan has been provided to any family

member of the assessee, the amount received from repayment shall be treated as a part of

income. Although, only the amount of interest received shall be taxable under the Australian

taxation law in the hands of assessee (Funding and finance, 2019) .

For the purpose of determining the amount of interest, several evidences are needed, as

such as contractual agreement between parties, bank statements, working papers of tax, loan

account of assessee, etc. would be treated as evidence (Funding and finance, 2019). On the basis

of such evidences, the taxable amount are being determined for the assessee.

Conclusion:

5

performing his hobby and if the motive of performing any hobby is to earn profit from it, the

income generated in through such activity shall be liable to pay tax.

Thus, in the present case scenario, if Barbara writes book for Eco Book Ltd. As hobby,

the income from sale of such book shall also be taxable as per the provisions of ATO. As such

book shall be written with a motive to generate profits from it.

Question 3

Fact:

Patrick paid assistance fee to his son David of $ 52000. the agreement was to repay the

sum at the end of 5 years of $58000. Further, there was no formal agreement or security deposit

for the amount lent. David repay the whole amount after 2 years through cheque along with 5%

interest on amount borrowed.

Issue:

To discuss the effect of agreement made on the income of Patrick.

Rules:

Income tax from interest on loan: As per the provisions of ATO, if an individual or a

body corporate provides a loan to another person, the principle amount received as repayment of

loan shall not be eligible to pay tax (Pert, Chen and Carvosso, 2018) . Although, in case, the

income received as a part of interest on such loan shall be taxable with the income of such

individual or body corporate in the assessment year in which the interest income has been

earned.

Loan provided to family members: In case, a loan has been provided to any family

member of the assessee, the amount received from repayment shall be treated as a part of

income. Although, only the amount of interest received shall be taxable under the Australian

taxation law in the hands of assessee (Funding and finance, 2019) .

For the purpose of determining the amount of interest, several evidences are needed, as

such as contractual agreement between parties, bank statements, working papers of tax, loan

account of assessee, etc. would be treated as evidence (Funding and finance, 2019). On the basis

of such evidences, the taxable amount are being determined for the assessee.

Conclusion:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the analysis of above rules and applying them on the present case scenraio, it can

be evaluated that the as the loan has been provided by Patricks to his son, the interest amount

received will attract the provisions relating to loan provided to family member. Furthermore, as

the amount has been repaid by the David through cheque, Patricks can use his bank statements as

an evidence for determining the taxable amount i.e. the interest received on loan provided by

him.

In addition, it can be concluded that as the Patricks has received the amount which is sum

of principle amount along with 5% interest on it, which is equal to $54600 ( $52000 + 5% ).

although, by evaluating the taxation provisions regarding taxability of amount received as

repayment of law, it can be concluded that the principle amount received by him shall not be

taxable. Moreover, the interest amount of such loan shall be considered as an taxable income of

Patricks. In this regard, Patrcks shall be liable to pay tax on the interest amount ( i.e. 52000 * 5%

= $ 2600).

CONCLUSION

From the analysis of the above study it can be concluded that the Australian Taxation

Office is a governing that operates monitoring and controlling of various activities relating to

payment of tax to the Australian government. Further, it can be concluded that if any asset has

been hold by an individual or a body corporate, the sale of such property shall attract the

principles of capital gain tax towards it.

Further, the amount received from the sale of books shall be taxable for the assessee. If

the individual receives income from performance of hobby, such income shall also be taxable

under Australian taxation system. Moreover, if an individual or business provides loan to another

person, interest received on such loan shall be taxable.

6

be evaluated that the as the loan has been provided by Patricks to his son, the interest amount

received will attract the provisions relating to loan provided to family member. Furthermore, as

the amount has been repaid by the David through cheque, Patricks can use his bank statements as

an evidence for determining the taxable amount i.e. the interest received on loan provided by

him.

In addition, it can be concluded that as the Patricks has received the amount which is sum

of principle amount along with 5% interest on it, which is equal to $54600 ( $52000 + 5% ).

although, by evaluating the taxation provisions regarding taxability of amount received as

repayment of law, it can be concluded that the principle amount received by him shall not be

taxable. Moreover, the interest amount of such loan shall be considered as an taxable income of

Patricks. In this regard, Patrcks shall be liable to pay tax on the interest amount ( i.e. 52000 * 5%

= $ 2600).

CONCLUSION

From the analysis of the above study it can be concluded that the Australian Taxation

Office is a governing that operates monitoring and controlling of various activities relating to

payment of tax to the Australian government. Further, it can be concluded that if any asset has

been hold by an individual or a body corporate, the sale of such property shall attract the

principles of capital gain tax towards it.

Further, the amount received from the sale of books shall be taxable for the assessee. If

the individual receives income from performance of hobby, such income shall also be taxable

under Australian taxation system. Moreover, if an individual or business provides loan to another

person, interest received on such loan shall be taxable.

6

REFERENCES

Books and Journals

Brown, C., 2018. Submission to the Inspector-General of Taxation, Review into the Australian

Taxation Office’s use of Garnishee Notices.

Davies, L. W., 2018. ‘LOOK’AND LOOK BACK: Using an auto/biographical lens to study the

Australian documentary film industry, 1970-2010.

Harrison, J., 2018. Assessing the Taxation of Superannuation in Terms of Horizontal and

Vertical Equity. J. Australasian Tax Tchrs. Ass'n. 13. p.114.

Murray, I., 2018, December. Regulating Charity in a Federated State: The Australian

Perspective. In Nonprofit Policy Forum(Vol. 9, No. 4). De Gruyter.

Pert, A., Chen, H. and Carvosso, R., 2018. 'Tech Mahindra Ltd v Federal Commissioner of

Taxation'(2016) 250 FCR 287. Australian Year Book of International Law. 35. p.276.

Online

How to calculate capital gains tax. 2018. [Online]. Available through :

<https://www.echoice.com.au/guides/capital-gains-tax-calculated/>

NKCX v FC of T. 2018. [Online]. Available through :

<https://www.ato.gov.au/law/view/document?

src=hs&pit=99991231235958&arc=false&start=1&pageSize=10&total=1865&num=0&d

ocid=JUD%2F2019ATC10-488%2F00001&dc=false&stype=find&cat=CA%2BCB

%2BCC%2BCD%2BCE%2BCF%3A%3A%3ACases%20Australian&tm=and-basic-

income%20from%20sale%20of%20book>

Funding and finance. 2019. [Online]. Available through :

<https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/Tax-

governance/Funding-and-finance/>

7

Books and Journals

Brown, C., 2018. Submission to the Inspector-General of Taxation, Review into the Australian

Taxation Office’s use of Garnishee Notices.

Davies, L. W., 2018. ‘LOOK’AND LOOK BACK: Using an auto/biographical lens to study the

Australian documentary film industry, 1970-2010.

Harrison, J., 2018. Assessing the Taxation of Superannuation in Terms of Horizontal and

Vertical Equity. J. Australasian Tax Tchrs. Ass'n. 13. p.114.

Murray, I., 2018, December. Regulating Charity in a Federated State: The Australian

Perspective. In Nonprofit Policy Forum(Vol. 9, No. 4). De Gruyter.

Pert, A., Chen, H. and Carvosso, R., 2018. 'Tech Mahindra Ltd v Federal Commissioner of

Taxation'(2016) 250 FCR 287. Australian Year Book of International Law. 35. p.276.

Online

How to calculate capital gains tax. 2018. [Online]. Available through :

<https://www.echoice.com.au/guides/capital-gains-tax-calculated/>

NKCX v FC of T. 2018. [Online]. Available through :

<https://www.ato.gov.au/law/view/document?

src=hs&pit=99991231235958&arc=false&start=1&pageSize=10&total=1865&num=0&d

ocid=JUD%2F2019ATC10-488%2F00001&dc=false&stype=find&cat=CA%2BCB

%2BCC%2BCD%2BCE%2BCF%3A%3A%3ACases%20Australian&tm=and-basic-

income%20from%20sale%20of%20book>

Funding and finance. 2019. [Online]. Available through :

<https://www.ato.gov.au/Business/Privately-owned-and-wealthy-groups/Tax-

governance/Funding-and-finance/>

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.