Taxation Assignment - Case Studies and Tax Calculation Analysis

VerifiedAdded on 2020/04/13

|6

|281

|42

Homework Assignment

AI Summary

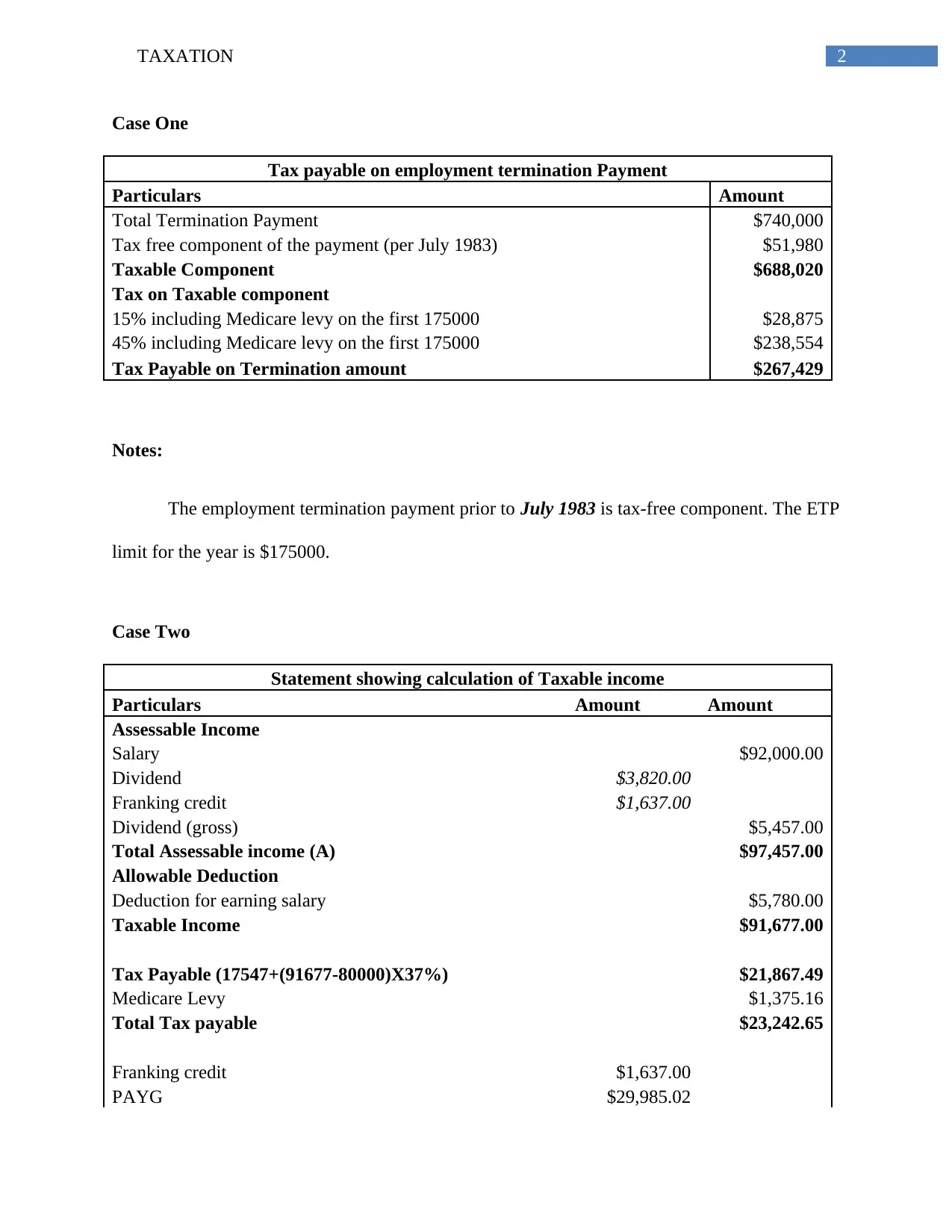

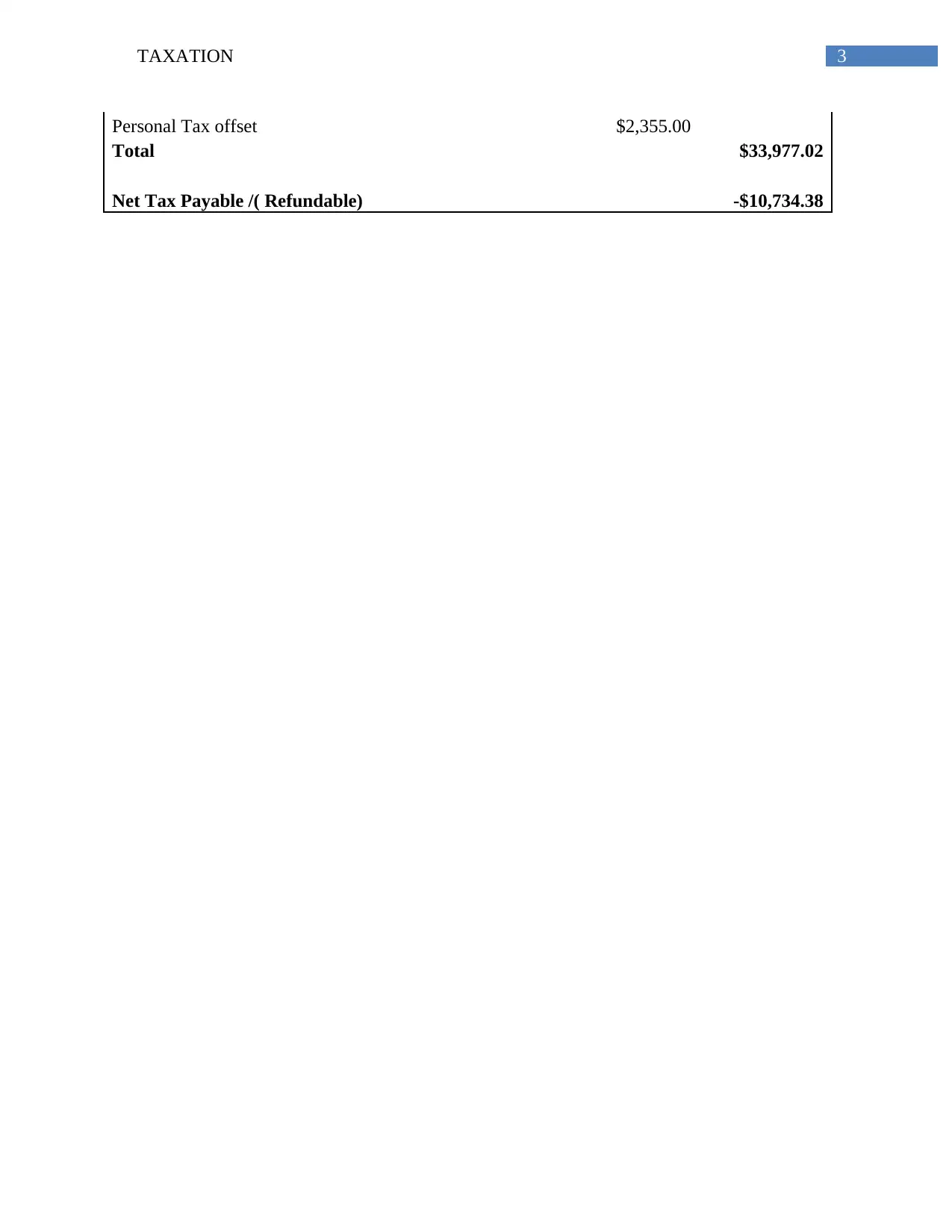

This assignment provides a detailed analysis of taxation, including calculations and case studies. The first case study focuses on employment termination, calculating the tax payable on a termination payment, considering the tax-free component and the taxable component, and the application of tax rates. The second case study involves calculating taxable income, including assessable income from salary and dividends, allowable deductions, and the calculation of tax payable, considering the Medicare levy and franking credits. The assignment also includes a reference list of sources used in the analysis. This assignment is designed to help students understand the practical application of tax laws and calculations in various financial scenarios.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.