HI6028 Taxation Assignment: Goods and Service Tax & CGT Analysis

VerifiedAdded on 2022/12/19

|9

|2824

|62

Homework Assignment

AI Summary

This assignment solution for HI6028, Taxation Theory, Practice & Law, addresses Goods and Service Tax (GST) and Capital Gains Tax (CGT) in the Australian context. The GST section explains the tax's nature, application, and reverse charge mechanism, using a case study involving a company using legal services. It clarifies how GST is levied, paid, and how tax credits are claimed. The CGT section defines capital gains and losses, detailing the tax implications of asset sales, including shares and real estate. It covers exemptions, the tax calculation process, and the impact of holding periods on tax rates. The solution also provides detailed calculations for determining the cost base of assets, including allowable expenses. This assignment aims to demonstrate understanding of the Australian income tax system, critical analysis of taxation issues, interpretation of relevant legislation, and application of taxation principles to real-life problems.

ASSIGNMENT

TAX THEORY, PRACTICES AND LAWS

HI6028

SUBMITTED BY:

11

TAX THEORY, PRACTICES AND LAWS

HI6028

SUBMITTED BY:

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

SOLUTION 1......................................................................................................................3

GOODS AND SEVICE TAX...........................................................................................3

SOLUTION 2......................................................................................................................4

CAPITAL GAIN TAX.......................................................................................................4

References.........................................................................................................................8

2

SOLUTION 1......................................................................................................................3

GOODS AND SEVICE TAX...........................................................................................3

SOLUTION 2......................................................................................................................4

CAPITAL GAIN TAX.......................................................................................................4

References.........................................................................................................................8

2

SOLUTION 1

GOODS AND SERVICE TAX

This tax is also known as the value-added tax. This is a tax which adds further values to

the commodities or services. The tax is imposed with a rate of 10%. Although this is not

the fixed-rate most of the commodities attract this rate only. This is the tax which is paid

by every one person present in the chain who is paying the tax receives his tax amount

back except the person who is the ultimate consumer of the goods or services. This tax

is a destination-based tax or other words it can be said that this is consumption-based

tax and its burden is borne by the person who will actually consume it. [GST Law]

Each and every organization which has registered itself under this tax or is liable to

register in this tax is liable for charging the tax as per the schemes and rules defined in

the act. These sellers have to charge the tax from the buyer and need to deposit this to

the government and they can claim credits for the tax they have given. There are a

number of ways this credit could be utilized in the business. (When to charge GST (and when

not to))

In Australia, all the persons or organization registered under this tax are liable for the

tax collection and further it is the duty for the person so registered to pay the collected

taxes to the government. There is number of distinct policies and rules made under the

GST law for distinct taxpayers as well as for distinct goods and services too.

From the case study, the basic things one could observe is that the company named

City Sky is taking legal services from a lawyer and those services are for the purpose of

business. The company is paying the fees of the lawyer to him. The annual income of

the lawyer is near to about $300,000. The income earned by the lawyer is taxable in the

country as it is above the exemption limit.

The company will pay the fees to the lawyer and the government has levied the GST on

the fees of the lawyers. The company is liable for the GST to the government as the

company is a registered business entity under the law of GST and the services of the

lawyer are charged under the scheme of Reverse Charge Mechanism. This is the

mechanism which states that there are few cases in which the person or entity who is

paying the amount to the other party is liable to pay tax on their basis. Similarly, the

services of the lawyer are also mentioned under the list of Reverse Charge. (GST)

The company will pay the fees to the lawyer and the company is liable for the GST

payable on the basis of the lawyer to the government. The company City Sky is paying

the fees to the lawyer and this tax would be paid by the City Sky only as the tax is

payable by the registered entity on the basis of the services they receive which are of

3

GOODS AND SERVICE TAX

This tax is also known as the value-added tax. This is a tax which adds further values to

the commodities or services. The tax is imposed with a rate of 10%. Although this is not

the fixed-rate most of the commodities attract this rate only. This is the tax which is paid

by every one person present in the chain who is paying the tax receives his tax amount

back except the person who is the ultimate consumer of the goods or services. This tax

is a destination-based tax or other words it can be said that this is consumption-based

tax and its burden is borne by the person who will actually consume it. [GST Law]

Each and every organization which has registered itself under this tax or is liable to

register in this tax is liable for charging the tax as per the schemes and rules defined in

the act. These sellers have to charge the tax from the buyer and need to deposit this to

the government and they can claim credits for the tax they have given. There are a

number of ways this credit could be utilized in the business. (When to charge GST (and when

not to))

In Australia, all the persons or organization registered under this tax are liable for the

tax collection and further it is the duty for the person so registered to pay the collected

taxes to the government. There is number of distinct policies and rules made under the

GST law for distinct taxpayers as well as for distinct goods and services too.

From the case study, the basic things one could observe is that the company named

City Sky is taking legal services from a lawyer and those services are for the purpose of

business. The company is paying the fees of the lawyer to him. The annual income of

the lawyer is near to about $300,000. The income earned by the lawyer is taxable in the

country as it is above the exemption limit.

The company will pay the fees to the lawyer and the government has levied the GST on

the fees of the lawyers. The company is liable for the GST to the government as the

company is a registered business entity under the law of GST and the services of the

lawyer are charged under the scheme of Reverse Charge Mechanism. This is the

mechanism which states that there are few cases in which the person or entity who is

paying the amount to the other party is liable to pay tax on their basis. Similarly, the

services of the lawyer are also mentioned under the list of Reverse Charge. (GST)

The company will pay the fees to the lawyer and the company is liable for the GST

payable on the basis of the lawyer to the government. The company City Sky is paying

the fees to the lawyer and this tax would be paid by the City Sky only as the tax is

payable by the registered entity on the basis of the services they receive which are of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

complete use to the business or are partially utilized by the business. As the services of

the lawyer are under the list of Reverse Charge, so the GST is payable by the other

party which is involved in the transaction.

As the tax is paid by the company so, therefore, all the credits will be received by the

company itself. That is the company is the one which would be entitled to the credits.

The company will pay the tax on the lawyer services and hence the credits would be

entitled to the company. The company will receive this credit because the services they

have received are for the use of the business and therefore it involves further sales and

these services are further given to the customers. The services of the lawyer are been

utilized by the organization for the apartments and these apartments are constructed for

further sale. The company can claim the credits for the tax they have paid on the behalf

of the lawyer and they would be receiving the credits of the GST they have paid. (GST)

The GST would be paid at the time when the fees t the lawyer is paid and the Input Tax

Credit would be received by the company in the upcoming year that is the year next to

the year when the GST is paid to the government. The tax is paid by the company as

the services of lawyer are covered under the head of Reverse Charge Mechanism; a

mechanism in which the tax is paid by the person who is paying the charges is liable to

pay the tax also. The tax credits would be availed by the company as the company is

the tax bearer and the law of GST says that the benefits of credit should be availed by

the person who is bearing the pain of taxpaying. The law says that the person who is

paying the tax would get the benefit of the credit otherwise the double benefit could be

availed by any person. In this case, the tax is paid by the company and the credit should

be availed by the company itself otherwise if the credit is availed by the lawyer than he

would get the double benefits, first one is the tax-saving and the other one is the

availing of the credits, so because of this reason the tax credit would be availed by the

company.

Therefore, from the above-prepared study based on the case, it could be concluded that

the liability of tax, in this case, would be borne by the company as this service falls

under the reverse charge mechanism. As the tax is paid by the company, so the tax

credit given by the government would be availed by the company only as it has borne

the liability of paying tax. The amount of the tax would be calculated on the fees of the

lawyer. [When to charge GST and when not] (When to charge GST (and when not to))

SOLUTION 2

CAPITAL GAIN TAX

If the sale made by assessing involves any of the goods such as shares and real estate

then there would either occur capital loss or capital gain on the sale made by him. A

4

the lawyer are under the list of Reverse Charge, so the GST is payable by the other

party which is involved in the transaction.

As the tax is paid by the company so, therefore, all the credits will be received by the

company itself. That is the company is the one which would be entitled to the credits.

The company will pay the tax on the lawyer services and hence the credits would be

entitled to the company. The company will receive this credit because the services they

have received are for the use of the business and therefore it involves further sales and

these services are further given to the customers. The services of the lawyer are been

utilized by the organization for the apartments and these apartments are constructed for

further sale. The company can claim the credits for the tax they have paid on the behalf

of the lawyer and they would be receiving the credits of the GST they have paid. (GST)

The GST would be paid at the time when the fees t the lawyer is paid and the Input Tax

Credit would be received by the company in the upcoming year that is the year next to

the year when the GST is paid to the government. The tax is paid by the company as

the services of lawyer are covered under the head of Reverse Charge Mechanism; a

mechanism in which the tax is paid by the person who is paying the charges is liable to

pay the tax also. The tax credits would be availed by the company as the company is

the tax bearer and the law of GST says that the benefits of credit should be availed by

the person who is bearing the pain of taxpaying. The law says that the person who is

paying the tax would get the benefit of the credit otherwise the double benefit could be

availed by any person. In this case, the tax is paid by the company and the credit should

be availed by the company itself otherwise if the credit is availed by the lawyer than he

would get the double benefits, first one is the tax-saving and the other one is the

availing of the credits, so because of this reason the tax credit would be availed by the

company.

Therefore, from the above-prepared study based on the case, it could be concluded that

the liability of tax, in this case, would be borne by the company as this service falls

under the reverse charge mechanism. As the tax is paid by the company, so the tax

credit given by the government would be availed by the company only as it has borne

the liability of paying tax. The amount of the tax would be calculated on the fees of the

lawyer. [When to charge GST and when not] (When to charge GST (and when not to))

SOLUTION 2

CAPITAL GAIN TAX

If the sale made by assessing involves any of the goods such as shares and real estate

then there would either occur capital loss or capital gain on the sale made by him. A

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

capital gain or loss can be defined as the difference between the cost that is incurred on

the acquisition of the assets and the amount which the assessee has received at the

time when they made the sale. This is the difference in the amount of acquisition and

the amount of disposing of. The gains that the assessee has from these capital assets

had to be noted in his return of income and they have to pay the capital gain taxes over

the incomes or gains they have earned from the disposing of the assets. These taxes

are to be paid in the year when the gain has occurred. This tax is considered as part of

the income tax. Capital losses that had occurred cannot be settled from any of the other

heads of income and thus can be adjusted from the head of Capital Gains only. [Capital

Gain assets and exemptions] (CGT assets and exemptions)

The acquisition of assets which are taken up after the date September 20, 1985, would

attract the capital gain taxes. There are certain exemptions also claimed under this act

and these exemptions include the Personal Assets of the person and other is the assets

which are depreciating assets. For instance, furniture, house, and personal cars doe not

attract the taxes of capital gain. These assets are applicable on the date when the

obligation of the contract is been fulfilled and not on the date of the physical transfer.

[Calculation of the cost base of Real Estate]

If the person is the resident of Australia, then each and every asset of the person is

taxable under capital gain no matter where the location of the asset is. Sale of assets

anywhere all around the world attracts the capital gain tax in Australia.

All the gains have to be disclosed in the financial year they have occurred. In a financial

year, if both capital gains, as well as losses, have occurred then the assessee has to

pay the amount net off the losses and gains and hence should be paid in the same

year. If the asset is been held with the assessee for the period of more than one year

than, the capital tax is discounted by 50%. This discount is only given in the case when

the assessee is either an individual or a small business. [Capital Gain Taxes]

The treatment for the units of shares is been done in the same way as that for the other

assets. The calculations are done in the same as other assets. The person whose

business is trading of shares then this is not considered as the capital gain and would

be treated as the income of the person. For investors sale of shares and the gains

attained would be treated as the capital gain and hence chargeable to taxes. [Base of

cost]

For the acquisition at costs, the formula based upon the cost of assets involves the

aggregate of the costs which are incurred in the acquisition and are directly related to

the asset acquisition. These costs include all the charges such as purchase price, the

brokerage service charge, stamp duties which are to be paid. The transfers of the

5

the acquisition of the assets and the amount which the assessee has received at the

time when they made the sale. This is the difference in the amount of acquisition and

the amount of disposing of. The gains that the assessee has from these capital assets

had to be noted in his return of income and they have to pay the capital gain taxes over

the incomes or gains they have earned from the disposing of the assets. These taxes

are to be paid in the year when the gain has occurred. This tax is considered as part of

the income tax. Capital losses that had occurred cannot be settled from any of the other

heads of income and thus can be adjusted from the head of Capital Gains only. [Capital

Gain assets and exemptions] (CGT assets and exemptions)

The acquisition of assets which are taken up after the date September 20, 1985, would

attract the capital gain taxes. There are certain exemptions also claimed under this act

and these exemptions include the Personal Assets of the person and other is the assets

which are depreciating assets. For instance, furniture, house, and personal cars doe not

attract the taxes of capital gain. These assets are applicable on the date when the

obligation of the contract is been fulfilled and not on the date of the physical transfer.

[Calculation of the cost base of Real Estate]

If the person is the resident of Australia, then each and every asset of the person is

taxable under capital gain no matter where the location of the asset is. Sale of assets

anywhere all around the world attracts the capital gain tax in Australia.

All the gains have to be disclosed in the financial year they have occurred. In a financial

year, if both capital gains, as well as losses, have occurred then the assessee has to

pay the amount net off the losses and gains and hence should be paid in the same

year. If the asset is been held with the assessee for the period of more than one year

than, the capital tax is discounted by 50%. This discount is only given in the case when

the assessee is either an individual or a small business. [Capital Gain Taxes]

The treatment for the units of shares is been done in the same way as that for the other

assets. The calculations are done in the same as other assets. The person whose

business is trading of shares then this is not considered as the capital gain and would

be treated as the income of the person. For investors sale of shares and the gains

attained would be treated as the capital gain and hence chargeable to taxes. [Base of

cost]

For the acquisition at costs, the formula based upon the cost of assets involves the

aggregate of the costs which are incurred in the acquisition and are directly related to

the asset acquisition. These costs include all the charges such as purchase price, the

brokerage service charge, stamp duties which are to be paid. The transfers of the

5

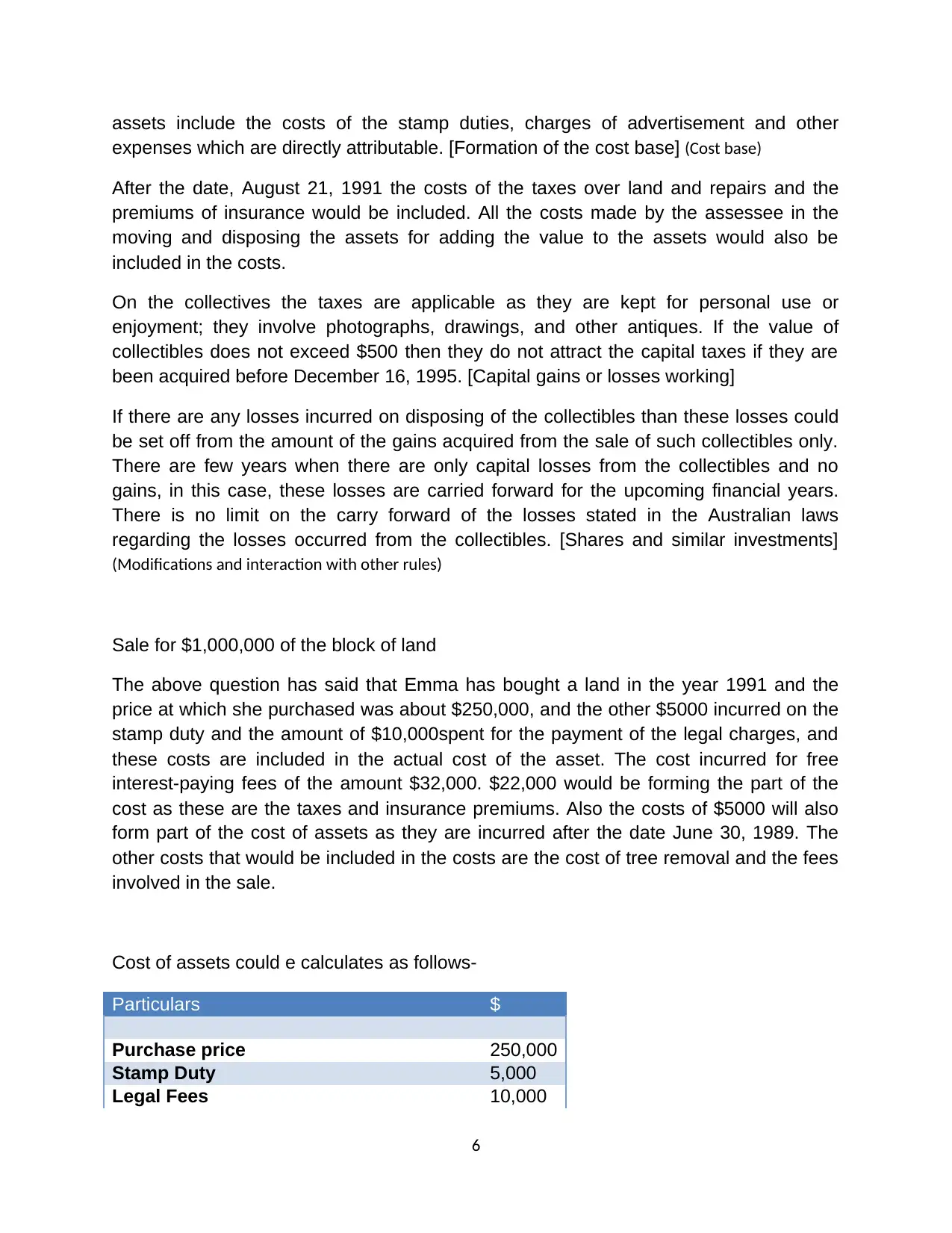

assets include the costs of the stamp duties, charges of advertisement and other

expenses which are directly attributable. [Formation of the cost base] (Cost base)

After the date, August 21, 1991 the costs of the taxes over land and repairs and the

premiums of insurance would be included. All the costs made by the assessee in the

moving and disposing the assets for adding the value to the assets would also be

included in the costs.

On the collectives the taxes are applicable as they are kept for personal use or

enjoyment; they involve photographs, drawings, and other antiques. If the value of

collectibles does not exceed $500 then they do not attract the capital taxes if they are

been acquired before December 16, 1995. [Capital gains or losses working]

If there are any losses incurred on disposing of the collectibles than these losses could

be set off from the amount of the gains acquired from the sale of such collectibles only.

There are few years when there are only capital losses from the collectibles and no

gains, in this case, these losses are carried forward for the upcoming financial years.

There is no limit on the carry forward of the losses stated in the Australian laws

regarding the losses occurred from the collectibles. [Shares and similar investments]

(Modifications and interaction with other rules)

Sale for $1,000,000 of the block of land

The above question has said that Emma has bought a land in the year 1991 and the

price at which she purchased was about $250,000, and the other $5000 incurred on the

stamp duty and the amount of $10,000spent for the payment of the legal charges, and

these costs are included in the actual cost of the asset. The cost incurred for free

interest-paying fees of the amount $32,000. $22,000 would be forming the part of the

cost as these are the taxes and insurance premiums. Also the costs of $5000 will also

form part of the cost of assets as they are incurred after the date June 30, 1989. The

other costs that would be included in the costs are the cost of tree removal and the fees

involved in the sale.

Cost of assets could e calculates as follows-

Particulars $

Purchase price 250,000

Stamp Duty 5,000

Legal Fees 10,000

6

expenses which are directly attributable. [Formation of the cost base] (Cost base)

After the date, August 21, 1991 the costs of the taxes over land and repairs and the

premiums of insurance would be included. All the costs made by the assessee in the

moving and disposing the assets for adding the value to the assets would also be

included in the costs.

On the collectives the taxes are applicable as they are kept for personal use or

enjoyment; they involve photographs, drawings, and other antiques. If the value of

collectibles does not exceed $500 then they do not attract the capital taxes if they are

been acquired before December 16, 1995. [Capital gains or losses working]

If there are any losses incurred on disposing of the collectibles than these losses could

be set off from the amount of the gains acquired from the sale of such collectibles only.

There are few years when there are only capital losses from the collectibles and no

gains, in this case, these losses are carried forward for the upcoming financial years.

There is no limit on the carry forward of the losses stated in the Australian laws

regarding the losses occurred from the collectibles. [Shares and similar investments]

(Modifications and interaction with other rules)

Sale for $1,000,000 of the block of land

The above question has said that Emma has bought a land in the year 1991 and the

price at which she purchased was about $250,000, and the other $5000 incurred on the

stamp duty and the amount of $10,000spent for the payment of the legal charges, and

these costs are included in the actual cost of the asset. The cost incurred for free

interest-paying fees of the amount $32,000. $22,000 would be forming the part of the

cost as these are the taxes and insurance premiums. Also the costs of $5000 will also

form part of the cost of assets as they are incurred after the date June 30, 1989. The

other costs that would be included in the costs are the cost of tree removal and the fees

involved in the sale.

Cost of assets could e calculates as follows-

Particulars $

Purchase price 250,000

Stamp Duty 5,000

Legal Fees 10,000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

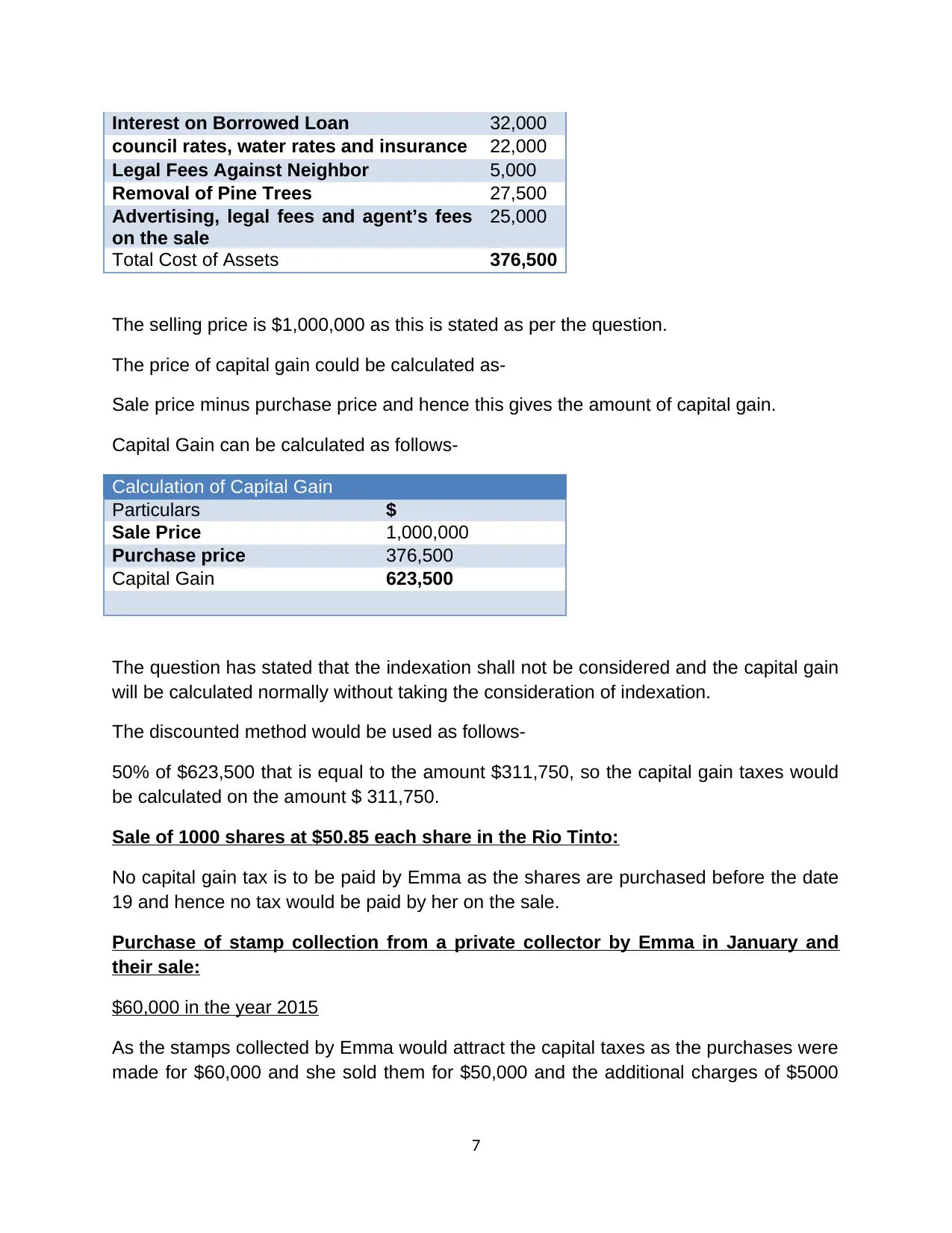

Interest on Borrowed Loan 32,000

council rates, water rates and insurance 22,000

Legal Fees Against Neighbor 5,000

Removal of Pine Trees 27,500

Advertising, legal fees and agent’s fees

on the sale

25,000

Total Cost of Assets 376,500

The selling price is $1,000,000 as this is stated as per the question.

The price of capital gain could be calculated as-

Sale price minus purchase price and hence this gives the amount of capital gain.

Capital Gain can be calculated as follows-

Calculation of Capital Gain

Particulars $

Sale Price 1,000,000

Purchase price 376,500

Capital Gain 623,500

The question has stated that the indexation shall not be considered and the capital gain

will be calculated normally without taking the consideration of indexation.

The discounted method would be used as follows-

50% of $623,500 that is equal to the amount $311,750, so the capital gain taxes would

be calculated on the amount $ 311,750.

Sale of 1000 shares at $50.85 each share in the Rio Tinto:

No capital gain tax is to be paid by Emma as the shares are purchased before the date

19 and hence no tax would be paid by her on the sale.

Purchase of stamp collection from a private collector by Emma in January and

their sale:

$60,000 in the year 2015

As the stamps collected by Emma would attract the capital taxes as the purchases were

made for $60,000 and she sold them for $50,000 and the additional charges of $5000

7

council rates, water rates and insurance 22,000

Legal Fees Against Neighbor 5,000

Removal of Pine Trees 27,500

Advertising, legal fees and agent’s fees

on the sale

25,000

Total Cost of Assets 376,500

The selling price is $1,000,000 as this is stated as per the question.

The price of capital gain could be calculated as-

Sale price minus purchase price and hence this gives the amount of capital gain.

Capital Gain can be calculated as follows-

Calculation of Capital Gain

Particulars $

Sale Price 1,000,000

Purchase price 376,500

Capital Gain 623,500

The question has stated that the indexation shall not be considered and the capital gain

will be calculated normally without taking the consideration of indexation.

The discounted method would be used as follows-

50% of $623,500 that is equal to the amount $311,750, so the capital gain taxes would

be calculated on the amount $ 311,750.

Sale of 1000 shares at $50.85 each share in the Rio Tinto:

No capital gain tax is to be paid by Emma as the shares are purchased before the date

19 and hence no tax would be paid by her on the sale.

Purchase of stamp collection from a private collector by Emma in January and

their sale:

$60,000 in the year 2015

As the stamps collected by Emma would attract the capital taxes as the purchases were

made for $60,000 and she sold them for $50,000 and the additional charges of $5000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

for auction charges would also be included. The capital loss could be calculated as-

(50000-60000-5000) that is equivalent to $15,000.

These losses could be settled only from the gains of the collectibles and if there are no

gains than these losses would be carried forward in the future years and no specific

time limit is given for carrying forward of these losses. [Working of Capital losses and

gains] (Working out your capital gain or loss)

Grand Piano sold for $30,000

Emma purchased a piano in the year 2000 for the amount of $80,000 and this piano

was sold for about $30,000. This asset was purchased by Emma for the personal use

so that it does not attract any of the capital losses or gains as it is utilized for personal

purpose. No capital gains or losses would be attracted by this transaction in this

financial year. [Modification rules of the law] (Capital gains tax)

References

Calculating the cost base for real estate. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Calculating-the-cost-base-for-real-estate/

Capital gains tax. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/

CGT assets and exemptions. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#collectables

Cost base. (n.d.). Retrieved from www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Cost-base/

Elements of the cost base and reduced cost base. (n.d.). Retrieved from

https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-

your-capital-gain-or-loss/cost-base/elements-of-the-cost-base-and-reduced-cost-base/

GST. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/Business/GST/

Modifications and interaction with other rules. (n.d.). Retrieved from

https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-

your-capital-gain-or-loss/cost-base/modifications-and-interaction-with-other-rules/

8

(50000-60000-5000) that is equivalent to $15,000.

These losses could be settled only from the gains of the collectibles and if there are no

gains than these losses would be carried forward in the future years and no specific

time limit is given for carrying forward of these losses. [Working of Capital losses and

gains] (Working out your capital gain or loss)

Grand Piano sold for $30,000

Emma purchased a piano in the year 2000 for the amount of $80,000 and this piano

was sold for about $30,000. This asset was purchased by Emma for the personal use

so that it does not attract any of the capital losses or gains as it is utilized for personal

purpose. No capital gains or losses would be attracted by this transaction in this

financial year. [Modification rules of the law] (Capital gains tax)

References

Calculating the cost base for real estate. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Calculating-the-cost-base-for-real-estate/

Capital gains tax. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/

CGT assets and exemptions. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#collectables

Cost base. (n.d.). Retrieved from www.ato.gov.au:

https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-

loss/Cost-base/

Elements of the cost base and reduced cost base. (n.d.). Retrieved from

https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-

your-capital-gain-or-loss/cost-base/elements-of-the-cost-base-and-reduced-cost-base/

GST. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/Business/GST/

Modifications and interaction with other rules. (n.d.). Retrieved from

https://www.ato.gov.au: https://www.ato.gov.au/general/capital-gains-tax/working-out-

your-capital-gain-or-loss/cost-base/modifications-and-interaction-with-other-rules/

8

Shares, units and similar investments. (n.d.). Retrieved from

https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/:

https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/

When to charge GST (and when not to). (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/Business/GST/When-to-charge-GST-%28and-when-not-to%29/

Working out your capital gain or loss. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-gain-or-loss/

9

https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/:

https://www.ato.gov.au/general/capital-gains-tax/shares,-units-and-similar-investments/

When to charge GST (and when not to). (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/Business/GST/When-to-charge-GST-%28and-when-not-to%29/

Working out your capital gain or loss. (n.d.). Retrieved from https://www.ato.gov.au:

https://www.ato.gov.au/general/capital-gains-tax/working-out-your-capital-gain-or-loss/

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.