Taxation Theory, Practice & Law: A Comprehensive Analysis

VerifiedAdded on 2020/07/22

|12

|3741

|29

Homework Assignment

AI Summary

This document provides a detailed analysis of a taxation assignment, addressing key aspects of taxation law, practice, and theory. The assignment explores various scenarios, including capital gains tax calculations based on asset acquisitions and disposals, the assessment of fringe benefits related to employee loans, and the implications of property ownership and profit-sharing agreements for tax liabilities. It examines specific cases, such as Eric's asset transactions, the calculation of taxable fringe benefits for an employee receiving a low-interest loan, and a partnership agreement between Jack and Jill regarding a rental property. The analysis incorporates relevant tax regulations, including capital gains tax rules, fringe benefit tax policies, and tax avoidance strategies, offering insights into the application of these rules in practical situations and providing a comprehensive understanding of the complexities of taxation.

Taxation Theory,

Practice & Law

Practice & Law

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1..................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting evidence:...................................................................................................................2

Conclusion:.................................................................................................................................2

QUESTION 2...................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................3

Supportive evidence:...................................................................................................................4

Conclusion: ................................................................................................................................4

QUESTION 3...................................................................................................................................4

Introduction.................................................................................................................................4

Critical evaluation:......................................................................................................................4

Supportive evidences: ................................................................................................................5

Conclusion:.................................................................................................................................5

QUESTION 4...................................................................................................................................5

Introduction:................................................................................................................................5

Critical analysis: .........................................................................................................................6

Supporting evidence: ..................................................................................................................6

Conclusion: ................................................................................................................................6

QUESTION 5...................................................................................................................................7

Introduction.................................................................................................................................7

Critical analysis: .........................................................................................................................7

Supporting evidence: ..................................................................................................................7

Conclusion...................................................................................................................................8

QUESTION 1..................................................................................................................................1

Introduction.................................................................................................................................1

Critical analysis:..........................................................................................................................1

Supporting evidence:...................................................................................................................2

Conclusion:.................................................................................................................................2

QUESTION 2...................................................................................................................................2

Introduction.................................................................................................................................2

Critical analysis:..........................................................................................................................3

Supportive evidence:...................................................................................................................4

Conclusion: ................................................................................................................................4

QUESTION 3...................................................................................................................................4

Introduction.................................................................................................................................4

Critical evaluation:......................................................................................................................4

Supportive evidences: ................................................................................................................5

Conclusion:.................................................................................................................................5

QUESTION 4...................................................................................................................................5

Introduction:................................................................................................................................5

Critical analysis: .........................................................................................................................6

Supporting evidence: ..................................................................................................................6

Conclusion: ................................................................................................................................6

QUESTION 5...................................................................................................................................7

Introduction.................................................................................................................................7

Critical analysis: .........................................................................................................................7

Supporting evidence: ..................................................................................................................7

Conclusion...................................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

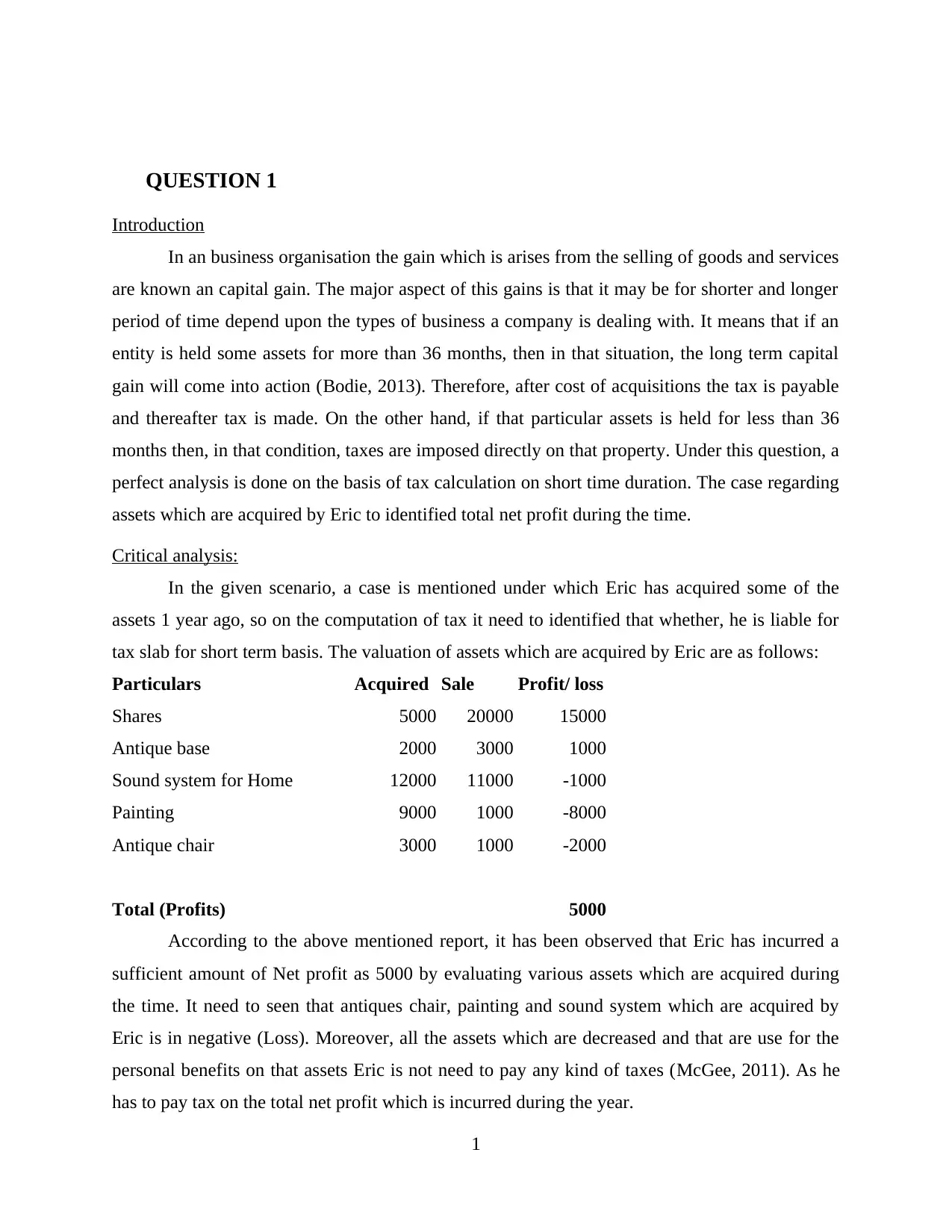

QUESTION 1

Introduction

In an business organisation the gain which is arises from the selling of goods and services

are known an capital gain. The major aspect of this gains is that it may be for shorter and longer

period of time depend upon the types of business a company is dealing with. It means that if an

entity is held some assets for more than 36 months, then in that situation, the long term capital

gain will come into action (Bodie, 2013). Therefore, after cost of acquisitions the tax is payable

and thereafter tax is made. On the other hand, if that particular assets is held for less than 36

months then, in that condition, taxes are imposed directly on that property. Under this question, a

perfect analysis is done on the basis of tax calculation on short time duration. The case regarding

assets which are acquired by Eric to identified total net profit during the time.

Critical analysis:

In the given scenario, a case is mentioned under which Eric has acquired some of the

assets 1 year ago, so on the computation of tax it need to identified that whether, he is liable for

tax slab for short term basis. The valuation of assets which are acquired by Eric are as follows:

Particulars Acquired Sale Profit/ loss

Shares 5000 20000 15000

Antique base 2000 3000 1000

Sound system for Home 12000 11000 -1000

Painting 9000 1000 -8000

Antique chair 3000 1000 -2000

Total (Profits) 5000

According to the above mentioned report, it has been observed that Eric has incurred a

sufficient amount of Net profit as 5000 by evaluating various assets which are acquired during

the time. It need to seen that antiques chair, painting and sound system which are acquired by

Eric is in negative (Loss). Moreover, all the assets which are decreased and that are use for the

personal benefits on that assets Eric is not need to pay any kind of taxes (McGee, 2011). As he

has to pay tax on the total net profit which is incurred during the year.

1

Introduction

In an business organisation the gain which is arises from the selling of goods and services

are known an capital gain. The major aspect of this gains is that it may be for shorter and longer

period of time depend upon the types of business a company is dealing with. It means that if an

entity is held some assets for more than 36 months, then in that situation, the long term capital

gain will come into action (Bodie, 2013). Therefore, after cost of acquisitions the tax is payable

and thereafter tax is made. On the other hand, if that particular assets is held for less than 36

months then, in that condition, taxes are imposed directly on that property. Under this question, a

perfect analysis is done on the basis of tax calculation on short time duration. The case regarding

assets which are acquired by Eric to identified total net profit during the time.

Critical analysis:

In the given scenario, a case is mentioned under which Eric has acquired some of the

assets 1 year ago, so on the computation of tax it need to identified that whether, he is liable for

tax slab for short term basis. The valuation of assets which are acquired by Eric are as follows:

Particulars Acquired Sale Profit/ loss

Shares 5000 20000 15000

Antique base 2000 3000 1000

Sound system for Home 12000 11000 -1000

Painting 9000 1000 -8000

Antique chair 3000 1000 -2000

Total (Profits) 5000

According to the above mentioned report, it has been observed that Eric has incurred a

sufficient amount of Net profit as 5000 by evaluating various assets which are acquired during

the time. It need to seen that antiques chair, painting and sound system which are acquired by

Eric is in negative (Loss). Moreover, all the assets which are decreased and that are use for the

personal benefits on that assets Eric is not need to pay any kind of taxes (McGee, 2011). As he

has to pay tax on the total net profit which is incurred during the year.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supporting evidence:

In 2016, edition of private investor's guide, it was mentioned that capital gains are

developed through selling of shares which are taken in that manner by the company. According

to rules, if a person needs to prepare a report of capital profit or loss in relation to his or her

return. All of them are liable to pay taxes on the total profit incurred during that particular year.

In the case of losses, individual can not be able to claim that amount against other financial gain.

These are implemented in order to decrease capital gain (Moser, 2012). According to the tax

rules which are based on total assets acquired before 20 September 1985 are come under the tax

slab and have to pay CGT, until it is not specific to do so. So many individual assets are

exempted from CGT. It does not get depreciate because to protect it from tax. Thus, the total tax

which is not payable on the above depreciate assets.

Conclusion:

Under this case report, it has been observed that a capital gain tax is paid according to the

rules which are categorised under income tax acts. Under the above analysis, it has been seen

that it is not need to assess the total disposing amount. The overall result are calculated on the

basis of tax policies which are charged on the assets which are acquired by the Eric. After the

proper evaluation it has been required to overcome the cost of acquisition in most appropriate

manner in coming time.

QUESTION 2

Introduction

Fringe benefits are the benefits paid by the employers for their employees. These benefits

comes in addition to the salary or other wage package. It is entirely different from the income tax

and is totally calculated on taxable value of the benefits which are rendered by an individual. In

the provided question, the fringe advantages are discussed in terms of loan. These are mostly

arises when an individual makes a loan to an employee at a very minimum rate of interest or

interest free rate (Baldwin, Cave and Lodge, 2012). The total taxable amount of a loan fringe

benefits are arise from the differences among the interest due on that particular loan at a

standard rate and those which are render by the employers. Brain's employer need to provide 3

year loan value to around 1 million @ of 1% per annum. It is very less than the actual rates.

2

In 2016, edition of private investor's guide, it was mentioned that capital gains are

developed through selling of shares which are taken in that manner by the company. According

to rules, if a person needs to prepare a report of capital profit or loss in relation to his or her

return. All of them are liable to pay taxes on the total profit incurred during that particular year.

In the case of losses, individual can not be able to claim that amount against other financial gain.

These are implemented in order to decrease capital gain (Moser, 2012). According to the tax

rules which are based on total assets acquired before 20 September 1985 are come under the tax

slab and have to pay CGT, until it is not specific to do so. So many individual assets are

exempted from CGT. It does not get depreciate because to protect it from tax. Thus, the total tax

which is not payable on the above depreciate assets.

Conclusion:

Under this case report, it has been observed that a capital gain tax is paid according to the

rules which are categorised under income tax acts. Under the above analysis, it has been seen

that it is not need to assess the total disposing amount. The overall result are calculated on the

basis of tax policies which are charged on the assets which are acquired by the Eric. After the

proper evaluation it has been required to overcome the cost of acquisition in most appropriate

manner in coming time.

QUESTION 2

Introduction

Fringe benefits are the benefits paid by the employers for their employees. These benefits

comes in addition to the salary or other wage package. It is entirely different from the income tax

and is totally calculated on taxable value of the benefits which are rendered by an individual. In

the provided question, the fringe advantages are discussed in terms of loan. These are mostly

arises when an individual makes a loan to an employee at a very minimum rate of interest or

interest free rate (Baldwin, Cave and Lodge, 2012). The total taxable amount of a loan fringe

benefits are arise from the differences among the interest due on that particular loan at a

standard rate and those which are render by the employers. Brain's employer need to provide 3

year loan value to around 1 million @ of 1% per annum. It is very less than the actual rates.

2

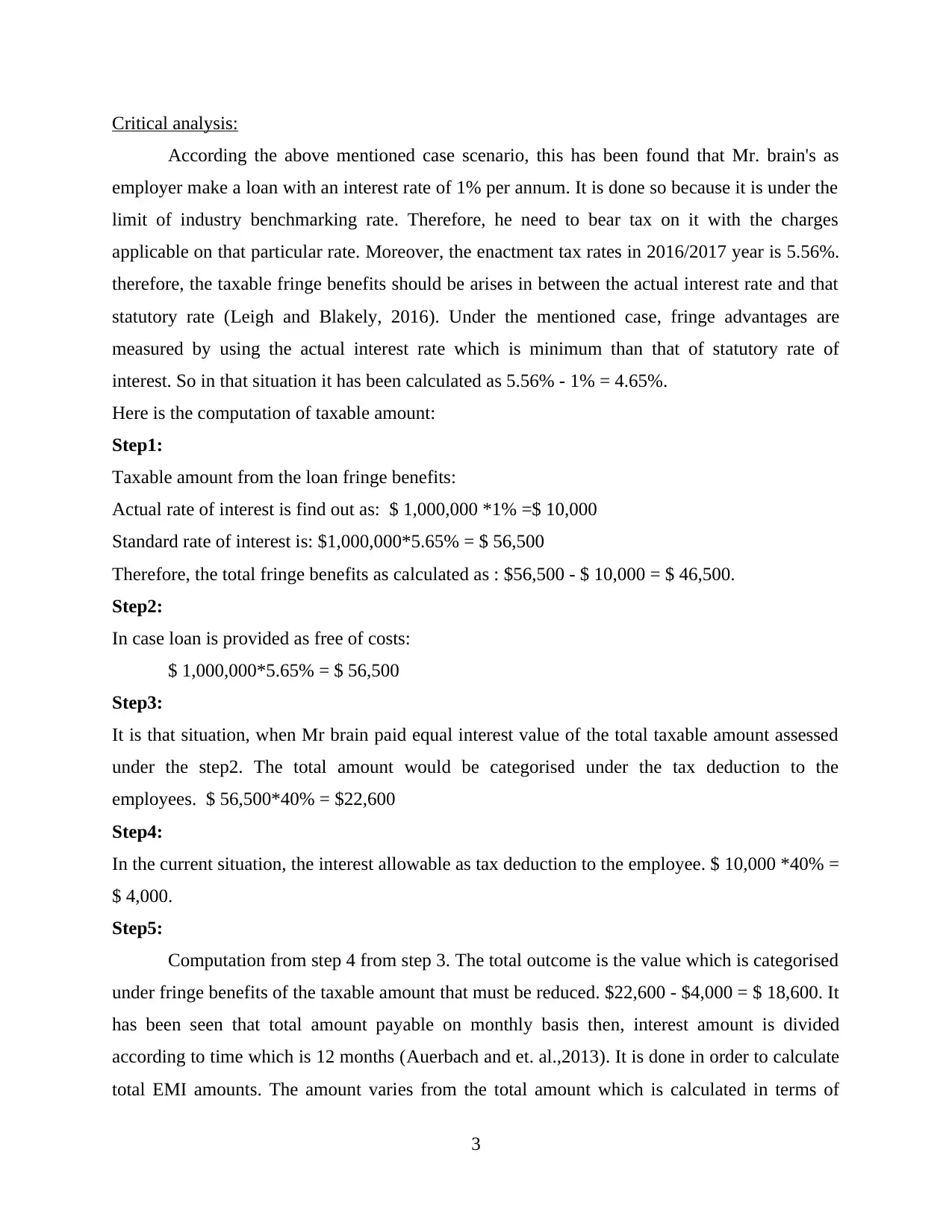

Critical analysis:

According the above mentioned case scenario, this has been found that Mr. brain's as

employer make a loan with an interest rate of 1% per annum. It is done so because it is under the

limit of industry benchmarking rate. Therefore, he need to bear tax on it with the charges

applicable on that particular rate. Moreover, the enactment tax rates in 2016/2017 year is 5.56%.

therefore, the taxable fringe benefits should be arises in between the actual interest rate and that

statutory rate (Leigh and Blakely, 2016). Under the mentioned case, fringe advantages are

measured by using the actual interest rate which is minimum than that of statutory rate of

interest. So in that situation it has been calculated as 5.56% - 1% = 4.65%.

Here is the computation of taxable amount:

Step1:

Taxable amount from the loan fringe benefits:

Actual rate of interest is find out as: $ 1,000,000 *1% =$ 10,000

Standard rate of interest is: $1,000,000*5.65% = $ 56,500

Therefore, the total fringe benefits as calculated as : $56,500 - $ 10,000 = $ 46,500.

Step2:

In case loan is provided as free of costs:

$ 1,000,000*5.65% = $ 56,500

Step3:

It is that situation, when Mr brain paid equal interest value of the total taxable amount assessed

under the step2. The total amount would be categorised under the tax deduction to the

employees. $ 56,500*40% = $22,600

Step4:

In the current situation, the interest allowable as tax deduction to the employee. $ 10,000 *40% =

$ 4,000.

Step5:

Computation from step 4 from step 3. The total outcome is the value which is categorised

under fringe benefits of the taxable amount that must be reduced. $22,600 - $4,000 = $ 18,600. It

has been seen that total amount payable on monthly basis then, interest amount is divided

according to time which is 12 months (Auerbach and et. al.,2013). It is done in order to calculate

total EMI amounts. The amount varies from the total amount which is calculated in terms of

3

According the above mentioned case scenario, this has been found that Mr. brain's as

employer make a loan with an interest rate of 1% per annum. It is done so because it is under the

limit of industry benchmarking rate. Therefore, he need to bear tax on it with the charges

applicable on that particular rate. Moreover, the enactment tax rates in 2016/2017 year is 5.56%.

therefore, the taxable fringe benefits should be arises in between the actual interest rate and that

statutory rate (Leigh and Blakely, 2016). Under the mentioned case, fringe advantages are

measured by using the actual interest rate which is minimum than that of statutory rate of

interest. So in that situation it has been calculated as 5.56% - 1% = 4.65%.

Here is the computation of taxable amount:

Step1:

Taxable amount from the loan fringe benefits:

Actual rate of interest is find out as: $ 1,000,000 *1% =$ 10,000

Standard rate of interest is: $1,000,000*5.65% = $ 56,500

Therefore, the total fringe benefits as calculated as : $56,500 - $ 10,000 = $ 46,500.

Step2:

In case loan is provided as free of costs:

$ 1,000,000*5.65% = $ 56,500

Step3:

It is that situation, when Mr brain paid equal interest value of the total taxable amount assessed

under the step2. The total amount would be categorised under the tax deduction to the

employees. $ 56,500*40% = $22,600

Step4:

In the current situation, the interest allowable as tax deduction to the employee. $ 10,000 *40% =

$ 4,000.

Step5:

Computation from step 4 from step 3. The total outcome is the value which is categorised

under fringe benefits of the taxable amount that must be reduced. $22,600 - $4,000 = $ 18,600. It

has been seen that total amount payable on monthly basis then, interest amount is divided

according to time which is 12 months (Auerbach and et. al.,2013). It is done in order to calculate

total EMI amounts. The amount varies from the total amount which is calculated in terms of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

annual basis. In the step 3, if the bank charges of interest free rates, under that situations: The

total fringe advantages would be: $ 1,000,000*5.65% = $56,500.

$56,500*40% = $ 22,600.

The total fringe benefits from that situations is: $22,600.

Supportive evidence:

According to the fringe tax policy, it is the total tax amount which is under the imaginary

funds of interest exceeds the actual cost of rate which is decrease on that taken loan. Under this

situation each loans are considered independently (KimLiu and Zheng, 2012).

Conclusion:

In the above case, its has been concluded that fringe benefits are that benefits which is

related with the employees and on behalf of this, the employment tax levied on the fringe

benefits as taxable amount. Fro this it has been seen that, company whether provide monthly or

yearly benefits to its people the rate of tax will remain the same. In order to provide a deductions,

there is a need to make a proper statements which are made in relation to employee to the

employer.

QUESTION 3

Introduction

In the mentioned case, a situation is based on the purchase of rental property by Jack

which is a architect and Jill they are borrowing money to do so. Both of them were agreed to

make a written contract which is categorised with the total number of profit sharing would be in

ratio of 9:1. It means that the agreement as in 10% of the profit is comes under Jacks and rest

90% would be transfer to Jill as his income. The major part of this contract is total of losses

would be beard by Jack only because he is only liable to do so. In is done in order to avoid tax

liabilities. Because, in the previous year the total losses incurred from the property was $10,000.

Critical evaluation:

under the given case study, both of them came into a contract for head off tax liabilities.

According the present scenario, Jill is the dependant lady working as a housewife. So, her

income is to attached together with Jack assessment (Feldman, 2011). The tax liabilities and

income both are categorised under the head of Jack account regarding this a covenant is made

between them. Thereafter, if the assets receive the loss, then such financial loss is to be carry

4

total fringe advantages would be: $ 1,000,000*5.65% = $56,500.

$56,500*40% = $ 22,600.

The total fringe benefits from that situations is: $22,600.

Supportive evidence:

According to the fringe tax policy, it is the total tax amount which is under the imaginary

funds of interest exceeds the actual cost of rate which is decrease on that taken loan. Under this

situation each loans are considered independently (KimLiu and Zheng, 2012).

Conclusion:

In the above case, its has been concluded that fringe benefits are that benefits which is

related with the employees and on behalf of this, the employment tax levied on the fringe

benefits as taxable amount. Fro this it has been seen that, company whether provide monthly or

yearly benefits to its people the rate of tax will remain the same. In order to provide a deductions,

there is a need to make a proper statements which are made in relation to employee to the

employer.

QUESTION 3

Introduction

In the mentioned case, a situation is based on the purchase of rental property by Jack

which is a architect and Jill they are borrowing money to do so. Both of them were agreed to

make a written contract which is categorised with the total number of profit sharing would be in

ratio of 9:1. It means that the agreement as in 10% of the profit is comes under Jacks and rest

90% would be transfer to Jill as his income. The major part of this contract is total of losses

would be beard by Jack only because he is only liable to do so. In is done in order to avoid tax

liabilities. Because, in the previous year the total losses incurred from the property was $10,000.

Critical evaluation:

under the given case study, both of them came into a contract for head off tax liabilities.

According the present scenario, Jill is the dependant lady working as a housewife. So, her

income is to attached together with Jack assessment (Feldman, 2011). The tax liabilities and

income both are categorised under the head of Jack account regarding this a covenant is made

between them. Thereafter, if the assets receive the loss, then such financial loss is to be carry

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

forward for the next year. It need to set off from the next succeeding profit for the year. After,

sale of property generate a capital gain or loss then, it will be treated under the Jack head. It has

been seen that Jill is fully dependent lady and not even earning any money. So in that phase she

is not able to pay any tax on any capital gain, only her husband need to pay all the taxes.

Supportive evidences:

According to the tax rules of the country, it is clearly mentioned under the laws that if

any one is not liable to get any benefits for which he/ she didn't need to pay any tax. On the

capital gains from sale or purchase of any assets they need to pay a tax (Lanis and Richardson,

2012). In the mentioned case, as the information is collected from the concern Australian tax

authority departments that, benefits can not provided to any one until they are not able to pay for

their products or assets. The tax deduction benefits can be avail only on that amounts which they

are not paying such as electric bills. In case of loss, jack has the option to deduct amount form

the capital gain during year. The overall results come form this case is that no any tax is been

paid by Jack.

Conclusion:

From the above case, it has been articulated that agreement between Jack and Jill was

perfectly balanced as 90% of the amount is collected as income for the Jill and only 10% goes to

Jack. Most of the losses would be bear by Jack, if any capital losses arises. As mentioned under

the case that last year losses should be set off from that capital gain which was generated from

the sale of property.

QUESTION 4

Introduction:

As indicated by Duke of Westminster's case which depended on tax avoidance. They

executed a deed of movement of covalent with his fellow worker including national partners,

nursery workers, and so forth. Under an extraordinary deed, duke chose to pay few amount of

capital for the administrations which he was rendering to him. In a composed letter which was

sent to the workers. In which, it was precisely said that Duke would pay compensation on

priority basis in addition to total, assuming if any administrations performed by the helper as a

5

sale of property generate a capital gain or loss then, it will be treated under the Jack head. It has

been seen that Jill is fully dependent lady and not even earning any money. So in that phase she

is not able to pay any tax on any capital gain, only her husband need to pay all the taxes.

Supportive evidences:

According to the tax rules of the country, it is clearly mentioned under the laws that if

any one is not liable to get any benefits for which he/ she didn't need to pay any tax. On the

capital gains from sale or purchase of any assets they need to pay a tax (Lanis and Richardson,

2012). In the mentioned case, as the information is collected from the concern Australian tax

authority departments that, benefits can not provided to any one until they are not able to pay for

their products or assets. The tax deduction benefits can be avail only on that amounts which they

are not paying such as electric bills. In case of loss, jack has the option to deduct amount form

the capital gain during year. The overall results come form this case is that no any tax is been

paid by Jack.

Conclusion:

From the above case, it has been articulated that agreement between Jack and Jill was

perfectly balanced as 90% of the amount is collected as income for the Jill and only 10% goes to

Jack. Most of the losses would be bear by Jack, if any capital losses arises. As mentioned under

the case that last year losses should be set off from that capital gain which was generated from

the sale of property.

QUESTION 4

Introduction:

As indicated by Duke of Westminster's case which depended on tax avoidance. They

executed a deed of movement of covalent with his fellow worker including national partners,

nursery workers, and so forth. Under an extraordinary deed, duke chose to pay few amount of

capital for the administrations which he was rendering to him. In a composed letter which was

sent to the workers. In which, it was precisely said that Duke would pay compensation on

priority basis in addition to total, assuming if any administrations performed by the helper as a

5

local assistant (Ashworth and Horder, 2013). After assessment of every circumstances Duke has

chosen to claim such defrayal for tax subtraction in arrangement for tax ignorance.

Critical analysis:

A deed is a referred to as an agreement same as lawful document which requires a

common assents of more than one individuals. It is typically used to allow an ideal approaches to

exchange of such property. The essential connection among a deed and an agreement is that,

deed is a composed contract that must be approved and get fixed in front of third party. Like

specialist. An understanding must be in composing, a dead is an agreement which doesn'st need

to be unenforceable (Buitelaar, Galle and Sorel, 2011). In a large portion of the cases, a deed has

a long term enforceable time span as a simple contract.

Supporting evidence:

As per the previously mentioned case, the significant issues lies on whether the deed of

composed statement would be seen or consumed as under work contract. Duke was not in any

case paying the nursery workers and hirelings not feebly compensation neither month to month

pay that was specified under the business contract. Along these lines, there is no any thought is

made towards the agreement which is said to be one of the central point in the advancement of

legitimately restricting contract. On account of understanding, capital is made in just related with

tax deductible. In the event that it is a yearly payment to nursery worker and labours (Taxation,

2017). They Duke have just the privilege to guarantee tax help for the annually payment or in the

circumstance where the sum paid for those administrations rendered in that specific year. With

the time is passing taxes are making a huge impact over the business of any parties. So under this

case, various judgement need to be evaluated in order to take maximum advantages from the

taxes. Some of the important decision need to be identified according to proper analysis of

written acts which are mentioned under the tax rules provisions.

Conclusion:

The entire case suggested that ignorance of tax must be permitted as long as it takes after

sanctioning law. Under this case the standards measure of that particular arrangement of the

contract can diminish the tax obligation. Therefore it it get sanctioned and demand for just yearly

year is made for the payment. There is conditions under which if a someone is taking unreal

6

chosen to claim such defrayal for tax subtraction in arrangement for tax ignorance.

Critical analysis:

A deed is a referred to as an agreement same as lawful document which requires a

common assents of more than one individuals. It is typically used to allow an ideal approaches to

exchange of such property. The essential connection among a deed and an agreement is that,

deed is a composed contract that must be approved and get fixed in front of third party. Like

specialist. An understanding must be in composing, a dead is an agreement which doesn'st need

to be unenforceable (Buitelaar, Galle and Sorel, 2011). In a large portion of the cases, a deed has

a long term enforceable time span as a simple contract.

Supporting evidence:

As per the previously mentioned case, the significant issues lies on whether the deed of

composed statement would be seen or consumed as under work contract. Duke was not in any

case paying the nursery workers and hirelings not feebly compensation neither month to month

pay that was specified under the business contract. Along these lines, there is no any thought is

made towards the agreement which is said to be one of the central point in the advancement of

legitimately restricting contract. On account of understanding, capital is made in just related with

tax deductible. In the event that it is a yearly payment to nursery worker and labours (Taxation,

2017). They Duke have just the privilege to guarantee tax help for the annually payment or in the

circumstance where the sum paid for those administrations rendered in that specific year. With

the time is passing taxes are making a huge impact over the business of any parties. So under this

case, various judgement need to be evaluated in order to take maximum advantages from the

taxes. Some of the important decision need to be identified according to proper analysis of

written acts which are mentioned under the tax rules provisions.

Conclusion:

The entire case suggested that ignorance of tax must be permitted as long as it takes after

sanctioning law. Under this case the standards measure of that particular arrangement of the

contract can diminish the tax obligation. Therefore it it get sanctioned and demand for just yearly

year is made for the payment. There is conditions under which if a someone is taking unreal

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

track which is not have any commercial objectives to save taxes. They need to pay on the overall

transaction done between the parties.

QUESTION 5

Introduction

The law relating to forest operation is contain various provisions. In this case, Bill owns a

land which is full of palm trees, he want to use it for the purpose of grazing sheep. A logging

company wanted to remove timber from his land and they are ready to pay $1000 for 100 each

100 meter. Their is another scenario where logging company want to get a right to remove as

much timber they require against a payment of $50,000. Taxable amount depends on the purpose

for which land is use, in both above cases the purpose for using timber is different so its

assessment will vary (Kaplow, 2011). As discussed, the land which is used for the purpose of

grazing his sheep but, it was going to happen becasue it was difficult to clean that particular area.

So in that context a logging company decided to pay some amount in order to clean 100 m of

areas and in that process they are going to pay $1000.

Critical analysis:

The total income incurred by the Mr. Bill is from selling of standing timber that would be

assessable at the time of filing return. If the major objectives of deal is to generate profit. The

company which is engarded under the process of cleaning that particular land is made a perfect

consideration of $1000 for 100m only. It is done so that he is exempted from paying tax on that

land whcih would help them during filing of tax return. On the other sitaution, if the company is

going to pay a decent amount of $ 50,000 as a lump sum amount then it would be assessable. As

that would be assessed for the value becaues, the case under which Bill is taking permit in order

to incur profitability. A situation of business is been done between the company and Mr. Bill as

they are allowing them to take away those timber as much as they need. It will arise chance of

royalty which is earned by bill because, he is not associated with the cutting down of trees. This

type of cases would goes into the head of captial gain, so under this situations the tax rate will be

analysed as treatment of normal income. It is done so because the activities which was discussed

under this case does not carries any forest business.

7

transaction done between the parties.

QUESTION 5

Introduction

The law relating to forest operation is contain various provisions. In this case, Bill owns a

land which is full of palm trees, he want to use it for the purpose of grazing sheep. A logging

company wanted to remove timber from his land and they are ready to pay $1000 for 100 each

100 meter. Their is another scenario where logging company want to get a right to remove as

much timber they require against a payment of $50,000. Taxable amount depends on the purpose

for which land is use, in both above cases the purpose for using timber is different so its

assessment will vary (Kaplow, 2011). As discussed, the land which is used for the purpose of

grazing his sheep but, it was going to happen becasue it was difficult to clean that particular area.

So in that context a logging company decided to pay some amount in order to clean 100 m of

areas and in that process they are going to pay $1000.

Critical analysis:

The total income incurred by the Mr. Bill is from selling of standing timber that would be

assessable at the time of filing return. If the major objectives of deal is to generate profit. The

company which is engarded under the process of cleaning that particular land is made a perfect

consideration of $1000 for 100m only. It is done so that he is exempted from paying tax on that

land whcih would help them during filing of tax return. On the other sitaution, if the company is

going to pay a decent amount of $ 50,000 as a lump sum amount then it would be assessable. As

that would be assessed for the value becaues, the case under which Bill is taking permit in order

to incur profitability. A situation of business is been done between the company and Mr. Bill as

they are allowing them to take away those timber as much as they need. It will arise chance of

royalty which is earned by bill because, he is not associated with the cutting down of trees. This

type of cases would goes into the head of captial gain, so under this situations the tax rate will be

analysed as treatment of normal income. It is done so because the activities which was discussed

under this case does not carries any forest business.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Supporting evidence:

The given conditions are categorised into tax rules and these rules is mostly associated to

that individual which is not operating in any forest business activities. As it was suppose to be

illegal in every part of the country. So any individuals who receive such kind of fees as royalties

for cutting down of trees form the land, as these are planted for the purpose of conducting any

business operations. In support of above case, a logging company was paying him an amount of

$ 1000 for clearning just 100m. The intention was not to get profit so it can be said as forest

business. There is a situation, if Bill is ready to take $ 50,000 and provide clear direction to

company to remove all shorts of timber (Yan and Luo, 2016). Then, only it will be said that

business operations and the total income is taken as computation of tax.

Conclusion

According to the mentioned case, it has been articulated that if a person is coming into a

deal that a company for clearning timber from a land, this type of income must be assessed in

accordance with the tax rules. That will be termed as total forest business.

8

The given conditions are categorised into tax rules and these rules is mostly associated to

that individual which is not operating in any forest business activities. As it was suppose to be

illegal in every part of the country. So any individuals who receive such kind of fees as royalties

for cutting down of trees form the land, as these are planted for the purpose of conducting any

business operations. In support of above case, a logging company was paying him an amount of

$ 1000 for clearning just 100m. The intention was not to get profit so it can be said as forest

business. There is a situation, if Bill is ready to take $ 50,000 and provide clear direction to

company to remove all shorts of timber (Yan and Luo, 2016). Then, only it will be said that

business operations and the total income is taken as computation of tax.

Conclusion

According to the mentioned case, it has been articulated that if a person is coming into a

deal that a company for clearning timber from a land, this type of income must be assessed in

accordance with the tax rules. That will be termed as total forest business.

8

REFERENCES

Books and Journals:

Ashworth, A. and Horder, J., 2013. Principles of criminal law. Oxford University Press.

Auerbach, A.J., Chetty, R., Feldstein, M. and Saez, E. eds., 2013. Handbook of public economics

(Vol. 5). Newnes.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand.

Bodie, Z., 2013. Investments. McGraw-Hill.

Buitelaar, E., Galle, M. and Sorel, N., 2011. Plan-led planning systems in development-led

practices: an empirical analysis into the (lack of) institutionalisation of planning law.

Environment and Planning A. 43(4). pp.928-941.

Feldman, Y., 2011. The complexity of disentangling intrinsic and extrinsic compliance

motivations: Theoretical and empirical insights from the behavioral analysis of law.

Kaplow, L., 2011. The theory of taxation and public economics. Princeton University Press.

Kim, J. B., Liu, X. and Zheng, L., 2012. The impact of mandatory IFRS adoption on audit fees:

Theory and evidence. The Accounting Review. 87(6). pp.2061-2094.

Lanis, R. and Richardson, G., 2012. Corporate social responsibility and tax aggressiveness: a test

of legitimacy theory. Accounting, Auditing & Accountability Journal. 26(1). pp.75-100.

Leigh, N. G. and Blakely, E. J., 2016. Planning local economic development: Theory and

practice. Sage Publications.

McGee, R.W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Moser, C., 2012. Gender planning and development: Theory, practice and training. Routledge.

Yan, A. and Luo, Y., 2016. International joint ventures: Theory and practice. Routledge.

Online

Taxation. 2017.[Online]. Available through: <http://www.ids.ac.uk/idsresearch/taxation> .

[Accessed on 18th September 2017].

9

Books and Journals:

Ashworth, A. and Horder, J., 2013. Principles of criminal law. Oxford University Press.

Auerbach, A.J., Chetty, R., Feldstein, M. and Saez, E. eds., 2013. Handbook of public economics

(Vol. 5). Newnes.

Baldwin, R., Cave, M. and Lodge, M., 2012. Understanding regulation: theory, strategy, and

practice. Oxford University Press on Demand.

Bodie, Z., 2013. Investments. McGraw-Hill.

Buitelaar, E., Galle, M. and Sorel, N., 2011. Plan-led planning systems in development-led

practices: an empirical analysis into the (lack of) institutionalisation of planning law.

Environment and Planning A. 43(4). pp.928-941.

Feldman, Y., 2011. The complexity of disentangling intrinsic and extrinsic compliance

motivations: Theoretical and empirical insights from the behavioral analysis of law.

Kaplow, L., 2011. The theory of taxation and public economics. Princeton University Press.

Kim, J. B., Liu, X. and Zheng, L., 2012. The impact of mandatory IFRS adoption on audit fees:

Theory and evidence. The Accounting Review. 87(6). pp.2061-2094.

Lanis, R. and Richardson, G., 2012. Corporate social responsibility and tax aggressiveness: a test

of legitimacy theory. Accounting, Auditing & Accountability Journal. 26(1). pp.75-100.

Leigh, N. G. and Blakely, E. J., 2016. Planning local economic development: Theory and

practice. Sage Publications.

McGee, R.W. ed., 2011. The ethics of tax evasion: Perspectives in theory and practice. Springer

Science & Business Media.

Moser, C., 2012. Gender planning and development: Theory, practice and training. Routledge.

Yan, A. and Luo, Y., 2016. International joint ventures: Theory and practice. Routledge.

Online

Taxation. 2017.[Online]. Available through: <http://www.ids.ac.uk/idsresearch/taxation> .

[Accessed on 18th September 2017].

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.