HI6028 Taxation Theory Practice & Law Individual Assignment T2 2017

VerifiedAdded on 2020/03/28

|9

|2542

|403

Homework Assignment

AI Summary

This document presents a comprehensive solution to a taxation assignment, HI6028 Taxation Theory, Practice & Law, from T2 2017. The assignment explores several key taxation issues through different scenarios. The first solution focuses on calculating net capital gains and losses, considering asset disposal and capital gains tax implications. The second solution delves into fringe benefits tax, specifically concerning a loan provided to an employee, calculating the taxable value based on statutory interest rates. The third solution examines the tax implications of a rental property owned by joint tenants, addressing profit and loss allocation. The fourth solution presents a case study on tax avoidance principles, referencing the Duke of Westminster case. Finally, the fifth solution analyzes the taxation of timber sales, differentiating between regular business operations and one-off disposals, and applying relevant tax provisions. The solutions provide detailed calculations, regulations, and applicability analyses, offering a complete understanding of the tax principles involved.

HI6028 Taxation Theory Practice & Law

T2 2017 Individual Assignment

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Solution 1...................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Solution 2...................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

Solution 3...................................................................................................................................5

Issue........................................................................................................................................5

Regulations.............................................................................................................................5

Applicability...........................................................................................................................5

Conclusion..............................................................................................................................6

Solution 4...................................................................................................................................6

Case........................................................................................................................................6

Provisions and Regulations....................................................................................................6

Application of cited provisions..............................................................................................6

Conclusion..............................................................................................................................6

Solution 5...................................................................................................................................7

Issue........................................................................................................................................7

Legal provisions for taxation.................................................................................................7

Application.............................................................................................................................7

Conclusion..............................................................................................................................7

Solution 1...................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Solution 2...................................................................................................................................4

Issue........................................................................................................................................4

Regulations.............................................................................................................................4

Applicability...........................................................................................................................4

Conclusion..............................................................................................................................4

Solution 3...................................................................................................................................5

Issue........................................................................................................................................5

Regulations.............................................................................................................................5

Applicability...........................................................................................................................5

Conclusion..............................................................................................................................6

Solution 4...................................................................................................................................6

Case........................................................................................................................................6

Provisions and Regulations....................................................................................................6

Application of cited provisions..............................................................................................6

Conclusion..............................................................................................................................6

Solution 5...................................................................................................................................7

Issue........................................................................................................................................7

Legal provisions for taxation.................................................................................................7

Application.............................................................................................................................7

Conclusion..............................................................................................................................7

References..................................................................................................................................8

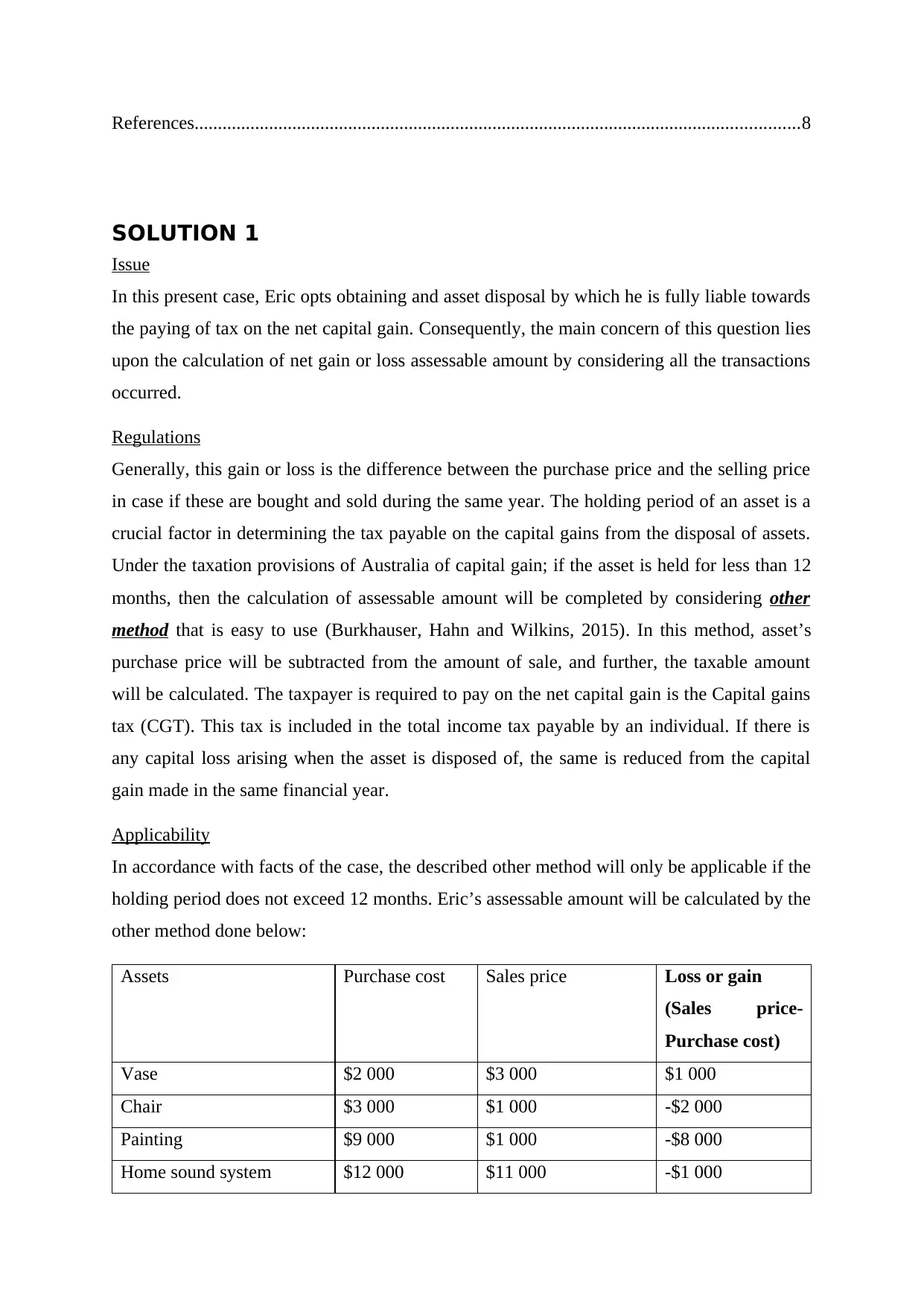

SOLUTION 1

Issue

In this present case, Eric opts obtaining and asset disposal by which he is fully liable towards

the paying of tax on the net capital gain. Consequently, the main concern of this question lies

upon the calculation of net gain or loss assessable amount by considering all the transactions

occurred.

Regulations

Generally, this gain or loss is the difference between the purchase price and the selling price

in case if these are bought and sold during the same year. The holding period of an asset is a

crucial factor in determining the tax payable on the capital gains from the disposal of assets.

Under the taxation provisions of Australia of capital gain; if the asset is held for less than 12

months, then the calculation of assessable amount will be completed by considering other

method that is easy to use (Burkhauser, Hahn and Wilkins, 2015). In this method, asset’s

purchase price will be subtracted from the amount of sale, and further, the taxable amount

will be calculated. The taxpayer is required to pay on the net capital gain is the Capital gains

tax (CGT). This tax is included in the total income tax payable by an individual. If there is

any capital loss arising when the asset is disposed of, the same is reduced from the capital

gain made in the same financial year.

Applicability

In accordance with facts of the case, the described other method will only be applicable if the

holding period does not exceed 12 months. Eric’s assessable amount will be calculated by the

other method done below:

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Vase $2 000 $3 000 $1 000

Chair $3 000 $1 000 -$2 000

Painting $9 000 $1 000 -$8 000

Home sound system $12 000 $11 000 -$1 000

SOLUTION 1

Issue

In this present case, Eric opts obtaining and asset disposal by which he is fully liable towards

the paying of tax on the net capital gain. Consequently, the main concern of this question lies

upon the calculation of net gain or loss assessable amount by considering all the transactions

occurred.

Regulations

Generally, this gain or loss is the difference between the purchase price and the selling price

in case if these are bought and sold during the same year. The holding period of an asset is a

crucial factor in determining the tax payable on the capital gains from the disposal of assets.

Under the taxation provisions of Australia of capital gain; if the asset is held for less than 12

months, then the calculation of assessable amount will be completed by considering other

method that is easy to use (Burkhauser, Hahn and Wilkins, 2015). In this method, asset’s

purchase price will be subtracted from the amount of sale, and further, the taxable amount

will be calculated. The taxpayer is required to pay on the net capital gain is the Capital gains

tax (CGT). This tax is included in the total income tax payable by an individual. If there is

any capital loss arising when the asset is disposed of, the same is reduced from the capital

gain made in the same financial year.

Applicability

In accordance with facts of the case, the described other method will only be applicable if the

holding period does not exceed 12 months. Eric’s assessable amount will be calculated by the

other method done below:

Assets Purchase cost Sales price Loss or gain

(Sales price-

Purchase cost)

Vase $2 000 $3 000 $1 000

Chair $3 000 $1 000 -$2 000

Painting $9 000 $1 000 -$8 000

Home sound system $12 000 $11 000 -$1 000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Shares of listed company $5 000 $20 000 $15 000

Net capital gain $5 000

Conclusion

By the assessable calculation amount for capital gain for Eric is $5 000.00.

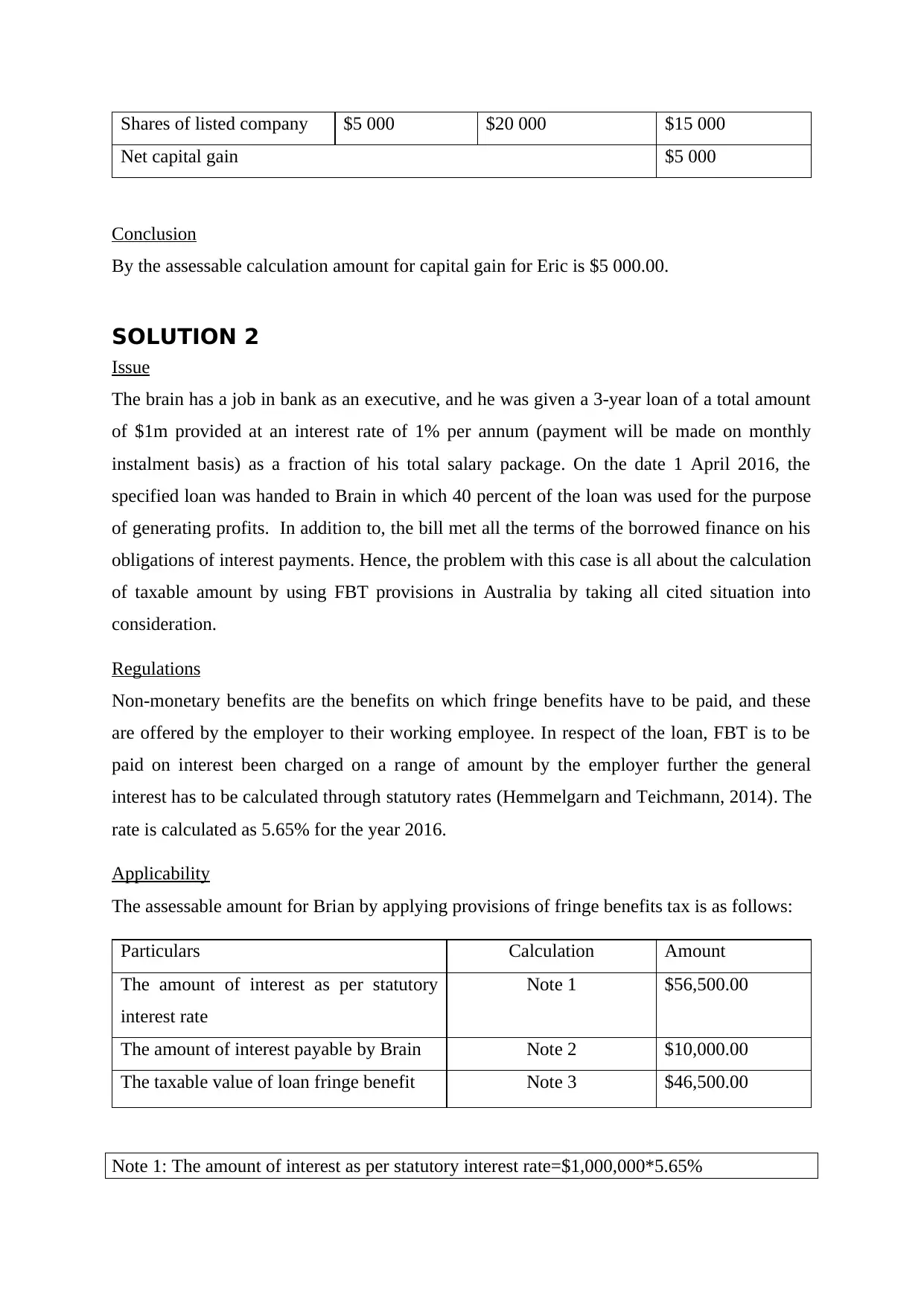

SOLUTION 2

Issue

The brain has a job in bank as an executive, and he was given a 3-year loan of a total amount

of $1m provided at an interest rate of 1% per annum (payment will be made on monthly

instalment basis) as a fraction of his total salary package. On the date 1 April 2016, the

specified loan was handed to Brain in which 40 percent of the loan was used for the purpose

of generating profits. In addition to, the bill met all the terms of the borrowed finance on his

obligations of interest payments. Hence, the problem with this case is all about the calculation

of taxable amount by using FBT provisions in Australia by taking all cited situation into

consideration.

Regulations

Non-monetary benefits are the benefits on which fringe benefits have to be paid, and these

are offered by the employer to their working employee. In respect of the loan, FBT is to be

paid on interest been charged on a range of amount by the employer further the general

interest has to be calculated through statutory rates (Hemmelgarn and Teichmann, 2014). The

rate is calculated as 5.65% for the year 2016.

Applicability

The assessable amount for Brian by applying provisions of fringe benefits tax is as follows:

Particulars Calculation Amount

The amount of interest as per statutory

interest rate

Note 1 $56,500.00

The amount of interest payable by Brain Note 2 $10,000.00

The taxable value of loan fringe benefit Note 3 $46,500.00

Note 1: The amount of interest as per statutory interest rate=$1,000,000*5.65%

Net capital gain $5 000

Conclusion

By the assessable calculation amount for capital gain for Eric is $5 000.00.

SOLUTION 2

Issue

The brain has a job in bank as an executive, and he was given a 3-year loan of a total amount

of $1m provided at an interest rate of 1% per annum (payment will be made on monthly

instalment basis) as a fraction of his total salary package. On the date 1 April 2016, the

specified loan was handed to Brain in which 40 percent of the loan was used for the purpose

of generating profits. In addition to, the bill met all the terms of the borrowed finance on his

obligations of interest payments. Hence, the problem with this case is all about the calculation

of taxable amount by using FBT provisions in Australia by taking all cited situation into

consideration.

Regulations

Non-monetary benefits are the benefits on which fringe benefits have to be paid, and these

are offered by the employer to their working employee. In respect of the loan, FBT is to be

paid on interest been charged on a range of amount by the employer further the general

interest has to be calculated through statutory rates (Hemmelgarn and Teichmann, 2014). The

rate is calculated as 5.65% for the year 2016.

Applicability

The assessable amount for Brian by applying provisions of fringe benefits tax is as follows:

Particulars Calculation Amount

The amount of interest as per statutory

interest rate

Note 1 $56,500.00

The amount of interest payable by Brain Note 2 $10,000.00

The taxable value of loan fringe benefit Note 3 $46,500.00

Note 1: The amount of interest as per statutory interest rate=$1,000,000*5.65%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Note 2: The amount of interest payable by Brain=$1,000,000*1%

Note 3: The taxable value of loan fringe benefit= $56,500.00-$10,000.00

Conclusion Taxability if interest amount is paid in instalment: The calculated assessable amount

of fringe benefit’s loan is $46,500.00. Taxability if interest amount paid together: The assessable amount of fringe benefit’s

loan is calculated as $46,500.00, but it will not affect in case the interest is payable on

the basis of monthly instalments or in lump-sum. Taxability if Brian gets exempted from payment of interest by the bank: The

assessable amount of fringe benefit’s loan is calculated as $56,500.00 in this specified

case brain is obliged to pay no interest, after that the total statutory interest will be

assessable value.

The 40% of the loan amount used for income generating purposes will not may any impact of

computation of tax. The payment of interest does not seem to have any impact on the

calculation of fringe benefits tax.

SOLUTION 3

Issue

Jack is an architect by profession and his spouse Jill being a housewife decided to be joint

tenants and took a loan in order to purchase rental premises. Jack agreed on the profit

percentage that 10% of the total profits and his wife Jill agreed the remaining 90% of the total

profits from the premises for the specified deed.by stating in the deed that Jack is entitled to

the total loss (100%) in case the premises incurred loss. However, they bear a loss of $10,000

last year. Therefore, this issue concerns the impact caused by a loss in the calculation of

assessable amount and tax implications in a situation where if the cited premise is sold by the

parties.

Regulations

The tax provision applicable for the purpose would be TR 93/32 which deals with the

distribution of net profit and loss among co-owners. The co-owners of the rental property are

not to be considered as partners as per the law unless the partnership is for the purpose of

carrying on some business (Winer, Profeta and Hettich, 2013). If they are considered as a

partner merely for taxation charges, this would be irrelevant since it is an unreal partnership

Note 3: The taxable value of loan fringe benefit= $56,500.00-$10,000.00

Conclusion Taxability if interest amount is paid in instalment: The calculated assessable amount

of fringe benefit’s loan is $46,500.00. Taxability if interest amount paid together: The assessable amount of fringe benefit’s

loan is calculated as $46,500.00, but it will not affect in case the interest is payable on

the basis of monthly instalments or in lump-sum. Taxability if Brian gets exempted from payment of interest by the bank: The

assessable amount of fringe benefit’s loan is calculated as $56,500.00 in this specified

case brain is obliged to pay no interest, after that the total statutory interest will be

assessable value.

The 40% of the loan amount used for income generating purposes will not may any impact of

computation of tax. The payment of interest does not seem to have any impact on the

calculation of fringe benefits tax.

SOLUTION 3

Issue

Jack is an architect by profession and his spouse Jill being a housewife decided to be joint

tenants and took a loan in order to purchase rental premises. Jack agreed on the profit

percentage that 10% of the total profits and his wife Jill agreed the remaining 90% of the total

profits from the premises for the specified deed.by stating in the deed that Jack is entitled to

the total loss (100%) in case the premises incurred loss. However, they bear a loss of $10,000

last year. Therefore, this issue concerns the impact caused by a loss in the calculation of

assessable amount and tax implications in a situation where if the cited premise is sold by the

parties.

Regulations

The tax provision applicable for the purpose would be TR 93/32 which deals with the

distribution of net profit and loss among co-owners. The co-owners of the rental property are

not to be considered as partners as per the law unless the partnership is for the purpose of

carrying on some business (Winer, Profeta and Hettich, 2013). If they are considered as a

partner merely for taxation charges, this would be irrelevant since it is an unreal partnership

and not according to the provisions for partnership. This form of unreal partnership would

entail many other implications and not just share of profit and loss. In partnership, any event

of loss does not mean the loss of their interest. Hence, their mutual interest in their rented

place is retained even after the loss.

Applicability

The agreement formed by Jack and Jill is summarised as follows:

Jack Jill

Profit will be distributed in ratio of 10% 90%

Loss will be distributed in ratio of 100% Nil

Although, they both Jack and Jill are not running the business operations on a regular

basis so for this reason, the terms specified in the deed will not be applied for the calculation

of taxation purposes.

Conclusion

Allocation of revenue loss

The loss incurred in the last year will be payable in the ratio of 1:1 because they are

not carrying the business on the ordinary course due to which deed terms will not apply for

the calculation of taxation purposes.

Allocation of capital gain or loss

Same provisions will be appropriate for tax implications regarding in situation where if the

cited premise is sold by the parties.

SOLUTION 4

Case

In the case of IRC and Duke of Westminster, Duke executed an agreement regarding

their associates which include house helpers, gardener and other servants. According to the

agreement, Duke was liable to pay additional money as a reward for the additional work

done. Affidavit regarding the same was submitted which declared that Duke would have to

pay extra wages to all the servants if they provide additional services apart from work already

set for them. In spite of an official written agreement, Duke did not pay any additional

entail many other implications and not just share of profit and loss. In partnership, any event

of loss does not mean the loss of their interest. Hence, their mutual interest in their rented

place is retained even after the loss.

Applicability

The agreement formed by Jack and Jill is summarised as follows:

Jack Jill

Profit will be distributed in ratio of 10% 90%

Loss will be distributed in ratio of 100% Nil

Although, they both Jack and Jill are not running the business operations on a regular

basis so for this reason, the terms specified in the deed will not be applied for the calculation

of taxation purposes.

Conclusion

Allocation of revenue loss

The loss incurred in the last year will be payable in the ratio of 1:1 because they are

not carrying the business on the ordinary course due to which deed terms will not apply for

the calculation of taxation purposes.

Allocation of capital gain or loss

Same provisions will be appropriate for tax implications regarding in situation where if the

cited premise is sold by the parties.

SOLUTION 4

Case

In the case of IRC and Duke of Westminster, Duke executed an agreement regarding

their associates which include house helpers, gardener and other servants. According to the

agreement, Duke was liable to pay additional money as a reward for the additional work

done. Affidavit regarding the same was submitted which declared that Duke would have to

pay extra wages to all the servants if they provide additional services apart from work already

set for them. In spite of an official written agreement, Duke did not pay any additional

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount to the workers for receiving a benefit in tax liability which came to him as a result of

the affidavit created. The workers did not receive any additional sum.

Provisions and Regulations

Principle established in the cited case

The tax laws of the time allowed the Duke for claiming a deduction in tax for reducing his

taxable income; thereby his income tax and surtax liability was reduced. Lord Tomlin,

handling the case said in this regard that every individual is entitled to make possible legal

adjustments in his tax affairs in a way so as to reduce his liability than it would have been

otherwise. If the person successfully accomplishes the same then, he cannot be forced to pay

more tax; though this task is unappreciative.

Application of cited provisions

This case was handled by Lord Wilberforce who concluded that this specific case is ruling

restrained court by assessing the actual transaction made so as to maintain the nature of the

transaction (Pearce and Pinto, 2015). Thus, it was stated that the legal nature of transaction

should be considered and in case there are several transactions held then also the similar

method will be taken into account.

Conclusion

Relevance in present

This principle is often known as the Westminster principle. This case was the most

famous case which was at the heart of the tax evasion and avoidance. It was understood by

later decisions that allow individuals and corporations can structure their financial

arrangements in a way that minimizes their tax liability. The structure must be within the law

of four corners of the black letter. This principle can be viewed as a contrast to the modern

Ramsay Principle. This law states that it is the work of the court to analyze the legal nature of

any transaction carried on for the purpose of tax evasion. This is opposite to the

Westminster’s case in which the transaction was carried out for the sole purpose of avoiding

legitimate tax liability. Thus, the Ramsay Principle emerged in response to increasing

practice of self-cancelling transactions.

the affidavit created. The workers did not receive any additional sum.

Provisions and Regulations

Principle established in the cited case

The tax laws of the time allowed the Duke for claiming a deduction in tax for reducing his

taxable income; thereby his income tax and surtax liability was reduced. Lord Tomlin,

handling the case said in this regard that every individual is entitled to make possible legal

adjustments in his tax affairs in a way so as to reduce his liability than it would have been

otherwise. If the person successfully accomplishes the same then, he cannot be forced to pay

more tax; though this task is unappreciative.

Application of cited provisions

This case was handled by Lord Wilberforce who concluded that this specific case is ruling

restrained court by assessing the actual transaction made so as to maintain the nature of the

transaction (Pearce and Pinto, 2015). Thus, it was stated that the legal nature of transaction

should be considered and in case there are several transactions held then also the similar

method will be taken into account.

Conclusion

Relevance in present

This principle is often known as the Westminster principle. This case was the most

famous case which was at the heart of the tax evasion and avoidance. It was understood by

later decisions that allow individuals and corporations can structure their financial

arrangements in a way that minimizes their tax liability. The structure must be within the law

of four corners of the black letter. This principle can be viewed as a contrast to the modern

Ramsay Principle. This law states that it is the work of the court to analyze the legal nature of

any transaction carried on for the purpose of tax evasion. This is opposite to the

Westminster’s case in which the transaction was carried out for the sole purpose of avoiding

legitimate tax liability. Thus, the Ramsay Principle emerged in response to increasing

practice of self-cancelling transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SOLUTION 5

Issue

This case shows the concern of considering the premises receipt and the attached tax in it.

Bill (landowner) the land full of pine trees, received an offer to utilize the whole land for

cattle feed. However, the company asked bill and offered him a deal of $1,000 for each 100

metres of the land’s timber. Further another deal bill received was that the company would

pay him a lump sum amount of $50,000 for granting the right to cut off all the timber (as per

the requirement) from the land. Bill faced the problem of whether to make payment of tax on

the land against the income generated in both cited cases.

Legal provisions for taxation

Case1: Disposal of standing timber that is not related to regular business course

According to the rule of taxation as per the TR 95/, the taxpayer having a land for the purpose

of disposing of timber, however, tree planting decision was meant for sale. As per the

subsection 36(1), income generated from disposing of timber in the where the taxpayer is not

carrying on the business of forest on a regular basis (Brody and et al., 2014). Further,

Subsection 36(1) stated that planting of trees on leased land gives an overall possession of

leased assets.

Case 2: Rights disposal to standing timber

Owner holding a forest operation business must cut off the standing timber, the specified case

stated revealed against cutting the standing timber. The applied section for this case is

subsection 25(1) as the income is generated from carrying the business on a regular basis.

The cited situation will be applied in this particular issue during the occurrence of disposal

(TD 96/35 CGT: time of disposal of a grant of a right to cut and remove timber from the

grantor’s land, 2017). It also states that if income is generated by providing the right to

another individual for extraction of timber than such income will be taxable.

Application and Conclusion

Nonetheless, subsection 36(1) and 25(1) of TR 95/6, will be taken into account for this cited

case and Bill has to make tax payment in both cases, section 36(1) will apply if he has

obtained the amount of $1000 as income and subsection 25(1) will applicable if the payment

is made in full.

Issue

This case shows the concern of considering the premises receipt and the attached tax in it.

Bill (landowner) the land full of pine trees, received an offer to utilize the whole land for

cattle feed. However, the company asked bill and offered him a deal of $1,000 for each 100

metres of the land’s timber. Further another deal bill received was that the company would

pay him a lump sum amount of $50,000 for granting the right to cut off all the timber (as per

the requirement) from the land. Bill faced the problem of whether to make payment of tax on

the land against the income generated in both cited cases.

Legal provisions for taxation

Case1: Disposal of standing timber that is not related to regular business course

According to the rule of taxation as per the TR 95/, the taxpayer having a land for the purpose

of disposing of timber, however, tree planting decision was meant for sale. As per the

subsection 36(1), income generated from disposing of timber in the where the taxpayer is not

carrying on the business of forest on a regular basis (Brody and et al., 2014). Further,

Subsection 36(1) stated that planting of trees on leased land gives an overall possession of

leased assets.

Case 2: Rights disposal to standing timber

Owner holding a forest operation business must cut off the standing timber, the specified case

stated revealed against cutting the standing timber. The applied section for this case is

subsection 25(1) as the income is generated from carrying the business on a regular basis.

The cited situation will be applied in this particular issue during the occurrence of disposal

(TD 96/35 CGT: time of disposal of a grant of a right to cut and remove timber from the

grantor’s land, 2017). It also states that if income is generated by providing the right to

another individual for extraction of timber than such income will be taxable.

Application and Conclusion

Nonetheless, subsection 36(1) and 25(1) of TR 95/6, will be taken into account for this cited

case and Bill has to make tax payment in both cases, section 36(1) will apply if he has

obtained the amount of $1000 as income and subsection 25(1) will applicable if the payment

is made in full.

REFERENCES

Books and Journals

Brody, E., Breen, O.B., McGregor-Lowndes, M. and Turnour, M., 2014. 5 An Unrelated

Income Tax for Australia?. Performance Management in Nonprofit Organizations: Global

Perspectives, 17, p.87.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Hemmelgarn, T. and Teichmann, D., 2014. Tax reforms and the Capital structure of

banks. International Tax and Public Finance, 21(4), pp.645-693.

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Winer, S.L., Profeta, P. and Hettich, W., 2013. The political economy of taxation. Oxford

University Press.

Online

Tax Evasion, Avoidance or Mitigation: That is the question! 2012. [Online]. Available

through < http://www.myersfletcher.com/resources/item/tax-evasion-avoidance-or-

mitigation-that-is-the-question.html>. [Accessed on 26th September 2017].

TD 96/35 CGT: time of disposal of a grant of a right to cut and remove timber from the

grantor’s land. 2017. [Online]. Available through <

http://www.iknow.cch.com.au/document/atagUio567791sl17289954/time-of-disposal-of-a-

grant-of-a-right-to-cut-and-remove-timber-from-the-grantor-s-land>. [Accessed on 26th

September 2017].

Books and Journals

Brody, E., Breen, O.B., McGregor-Lowndes, M. and Turnour, M., 2014. 5 An Unrelated

Income Tax for Australia?. Performance Management in Nonprofit Organizations: Global

Perspectives, 17, p.87.

Burkhauser, R.V., Hahn, M.H. and Wilkins, R., 2015. Measuring top incomes using tax

record data: A cautionary tale from Australia. The Journal of Economic Inequality, 13(2),

pp.181-205.

Hemmelgarn, T. and Teichmann, D., 2014. Tax reforms and the Capital structure of

banks. International Tax and Public Finance, 21(4), pp.645-693.

Pearce, P. and Pinto, D., 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), pp.146-153.

Winer, S.L., Profeta, P. and Hettich, W., 2013. The political economy of taxation. Oxford

University Press.

Online

Tax Evasion, Avoidance or Mitigation: That is the question! 2012. [Online]. Available

through < http://www.myersfletcher.com/resources/item/tax-evasion-avoidance-or-

mitigation-that-is-the-question.html>. [Accessed on 26th September 2017].

TD 96/35 CGT: time of disposal of a grant of a right to cut and remove timber from the

grantor’s land. 2017. [Online]. Available through <

http://www.iknow.cch.com.au/document/atagUio567791sl17289954/time-of-disposal-of-a-

grant-of-a-right-to-cut-and-remove-timber-from-the-grantor-s-land>. [Accessed on 26th

September 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.