HI6028 Taxation Theory, Practice & Law Individual Assignment T2 2017

VerifiedAdded on 2020/02/18

|12

|2782

|200

Homework Assignment

AI Summary

This document presents a comprehensive analysis of a taxation assignment, addressing five distinct case studies within the framework of Australian taxation law. The assignment begins with an evaluation of capital gains and losses arising from asset transactions, applying relevant legal provisions to determine tax liabilities. The second case study focuses on fringe benefits tax (FBT) related to employee loans, calculating taxable values and considering scenarios involving interest payments and waivers. The third case study examines the allocation of rental income and losses between joint tenants, clarifying the application of tax regulations to property ownership arrangements. The fourth case study delves into tax avoidance schemes, referencing the Duke of Westminster principle and its implications. Finally, the fifth case study provides guidance on the taxation of timber disposal, including the application of ruling TR 95/6 to determine assessable income from timber sales. Each case study utilizes the ILAC (Issue, Law, Application, Conclusion) approach to provide structured and well-reasoned solutions, supported by relevant legal provisions and calculations.

HI6028 Taxation Theory, Practice &

Law

T2 2017 Individual Assignment

Law

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction................................................................................................................................4

Case study 1...............................................................................................................................4

Description of issues..............................................................................................................4

Legal provisions.....................................................................................................................4

Application of described provisions.......................................................................................4

Conclusion..............................................................................................................................5

Case study 2...............................................................................................................................5

Description of issues..............................................................................................................5

Legal provisions.....................................................................................................................5

Application of described provisions.......................................................................................5

Conclusion..............................................................................................................................6

Case study 3...............................................................................................................................6

Description of issues..............................................................................................................6

Legal provisions.....................................................................................................................6

Application of described provisions.......................................................................................6

Conclusion..............................................................................................................................7

Case study 4...............................................................................................................................7

Description of issues..............................................................................................................7

Legal provisions.....................................................................................................................7

Application of described provisions.......................................................................................7

Conclusion..............................................................................................................................8

Case study 5...............................................................................................................................8

Description of issues..............................................................................................................8

Legal provisions.....................................................................................................................8

Application of described provisions.......................................................................................9

Conclusion..............................................................................................................................9

Introduction................................................................................................................................4

Case study 1...............................................................................................................................4

Description of issues..............................................................................................................4

Legal provisions.....................................................................................................................4

Application of described provisions.......................................................................................4

Conclusion..............................................................................................................................5

Case study 2...............................................................................................................................5

Description of issues..............................................................................................................5

Legal provisions.....................................................................................................................5

Application of described provisions.......................................................................................5

Conclusion..............................................................................................................................6

Case study 3...............................................................................................................................6

Description of issues..............................................................................................................6

Legal provisions.....................................................................................................................6

Application of described provisions.......................................................................................6

Conclusion..............................................................................................................................7

Case study 4...............................................................................................................................7

Description of issues..............................................................................................................7

Legal provisions.....................................................................................................................7

Application of described provisions.......................................................................................7

Conclusion..............................................................................................................................8

Case study 5...............................................................................................................................8

Description of issues..............................................................................................................8

Legal provisions.....................................................................................................................8

Application of described provisions.......................................................................................9

Conclusion..............................................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LIST OF TABLES

Table 1: Other method for computation of net capital gain or loss...........................................4

Table 2: computation of net capital gain or loss by considering transactions of Eric...............4

Table 3: Statement showing computation of taxable value on which FBT will be payable......5

Table 4: Application of ruling TR 95/6 on the cited case..........................................................9

Table 1: Other method for computation of net capital gain or loss...........................................4

Table 2: computation of net capital gain or loss by considering transactions of Eric...............4

Table 3: Statement showing computation of taxable value on which FBT will be payable......5

Table 4: Application of ruling TR 95/6 on the cited case..........................................................9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

The present study is based evaluation of given 5 case scenarios by applying Australian

taxation provisions. For the solution of each case study, ILAC approach will be applied in to

provide a viable solution to the taxpayer.

CASE STUDY 1

Description of issues

In the previous twelve months, Eric had acquired, and sold capital assets thus present part of

study deals with computation of net capital gain or loss for the year by considering the

transaction value of each item.

Legal provisions

Other method

Table 1: Other method for computation of net capital gain or loss

Method Description How to calculate

Individual who hold assets for less

than a year, this method is for them

(Harding, 2013). To identify if

individual obtained the asset at the

least 1 year before the capital tax gain

event, exclusive of both acquisition

and event date (Australian Taxation

office, 2017).

This method is

considered to be the

most common method

to calculate CGT.

Deduct the cost of

the asset from the

sale price.

Application of described provisions

Table 2: computation of net capital gain or loss by considering transactions of Eric

Assets Purchase

value

Sales

value

Loss or Gain

Antique vase $2 000 $3 000 $3 000.00 - $2 000.00 $1 000.00

The present study is based evaluation of given 5 case scenarios by applying Australian

taxation provisions. For the solution of each case study, ILAC approach will be applied in to

provide a viable solution to the taxpayer.

CASE STUDY 1

Description of issues

In the previous twelve months, Eric had acquired, and sold capital assets thus present part of

study deals with computation of net capital gain or loss for the year by considering the

transaction value of each item.

Legal provisions

Other method

Table 1: Other method for computation of net capital gain or loss

Method Description How to calculate

Individual who hold assets for less

than a year, this method is for them

(Harding, 2013). To identify if

individual obtained the asset at the

least 1 year before the capital tax gain

event, exclusive of both acquisition

and event date (Australian Taxation

office, 2017).

This method is

considered to be the

most common method

to calculate CGT.

Deduct the cost of

the asset from the

sale price.

Application of described provisions

Table 2: computation of net capital gain or loss by considering transactions of Eric

Assets Purchase

value

Sales

value

Loss or Gain

Antique vase $2 000 $3 000 $3 000.00 - $2 000.00 $1 000.00

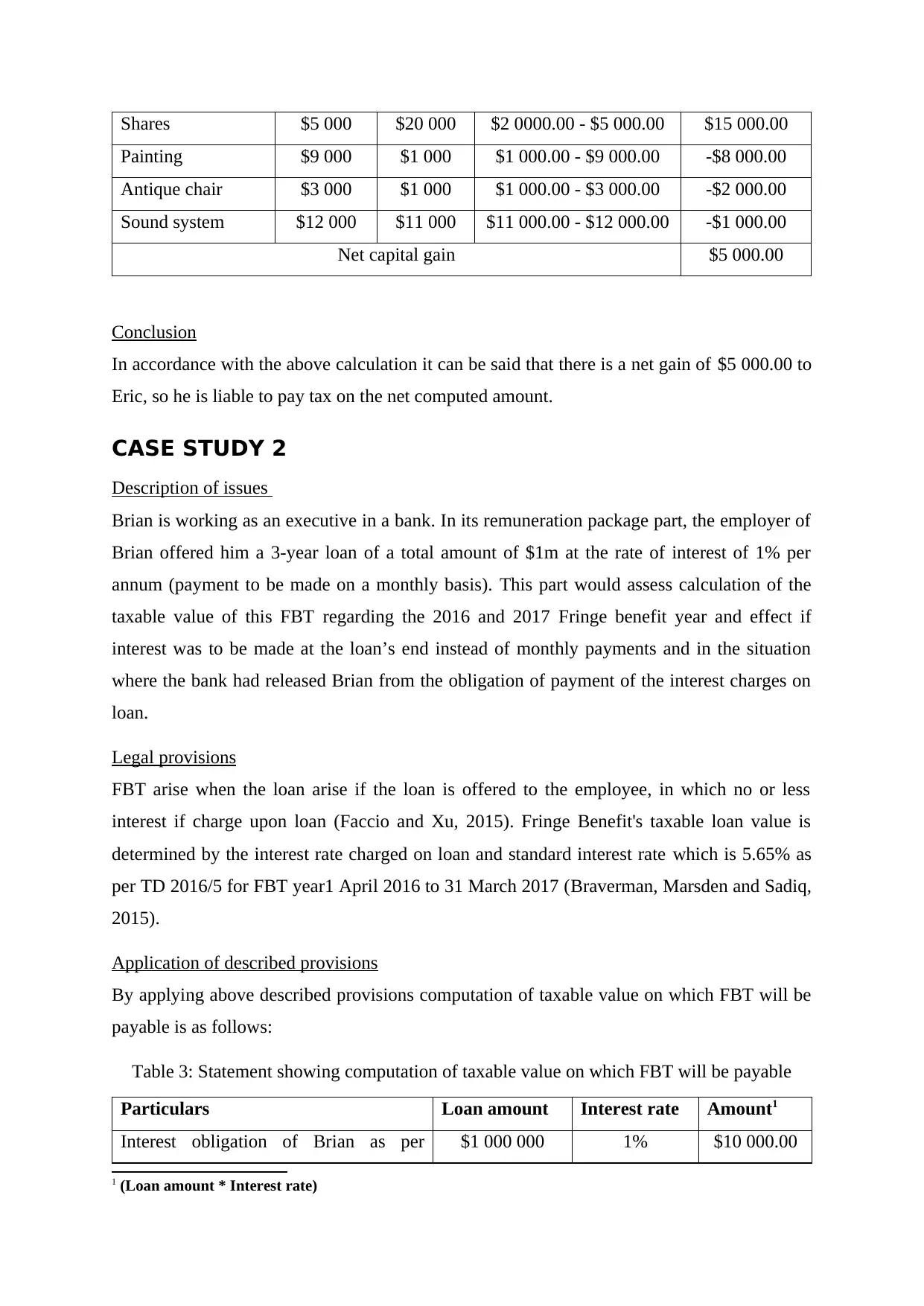

Shares $5 000 $20 000 $2 0000.00 - $5 000.00 $15 000.00

Painting $9 000 $1 000 $1 000.00 - $9 000.00 -$8 000.00

Antique chair $3 000 $1 000 $1 000.00 - $3 000.00 -$2 000.00

Sound system $12 000 $11 000 $11 000.00 - $12 000.00 -$1 000.00

Net capital gain $5 000.00

Conclusion

In accordance with the above calculation it can be said that there is a net gain of $5 000.00 to

Eric, so he is liable to pay tax on the net computed amount.

CASE STUDY 2

Description of issues

Brian is working as an executive in a bank. In its remuneration package part, the employer of

Brian offered him a 3-year loan of a total amount of $1m at the rate of interest of 1% per

annum (payment to be made on a monthly basis). This part would assess calculation of the

taxable value of this FBT regarding the 2016 and 2017 Fringe benefit year and effect if

interest was to be made at the loan’s end instead of monthly payments and in the situation

where the bank had released Brian from the obligation of payment of the interest charges on

loan.

Legal provisions

FBT arise when the loan arise if the loan is offered to the employee, in which no or less

interest if charge upon loan (Faccio and Xu, 2015). Fringe Benefit's taxable loan value is

determined by the interest rate charged on loan and standard interest rate which is 5.65% as

per TD 2016/5 for FBT year1 April 2016 to 31 March 2017 (Braverman, Marsden and Sadiq,

2015).

Application of described provisions

By applying above described provisions computation of taxable value on which FBT will be

payable is as follows:

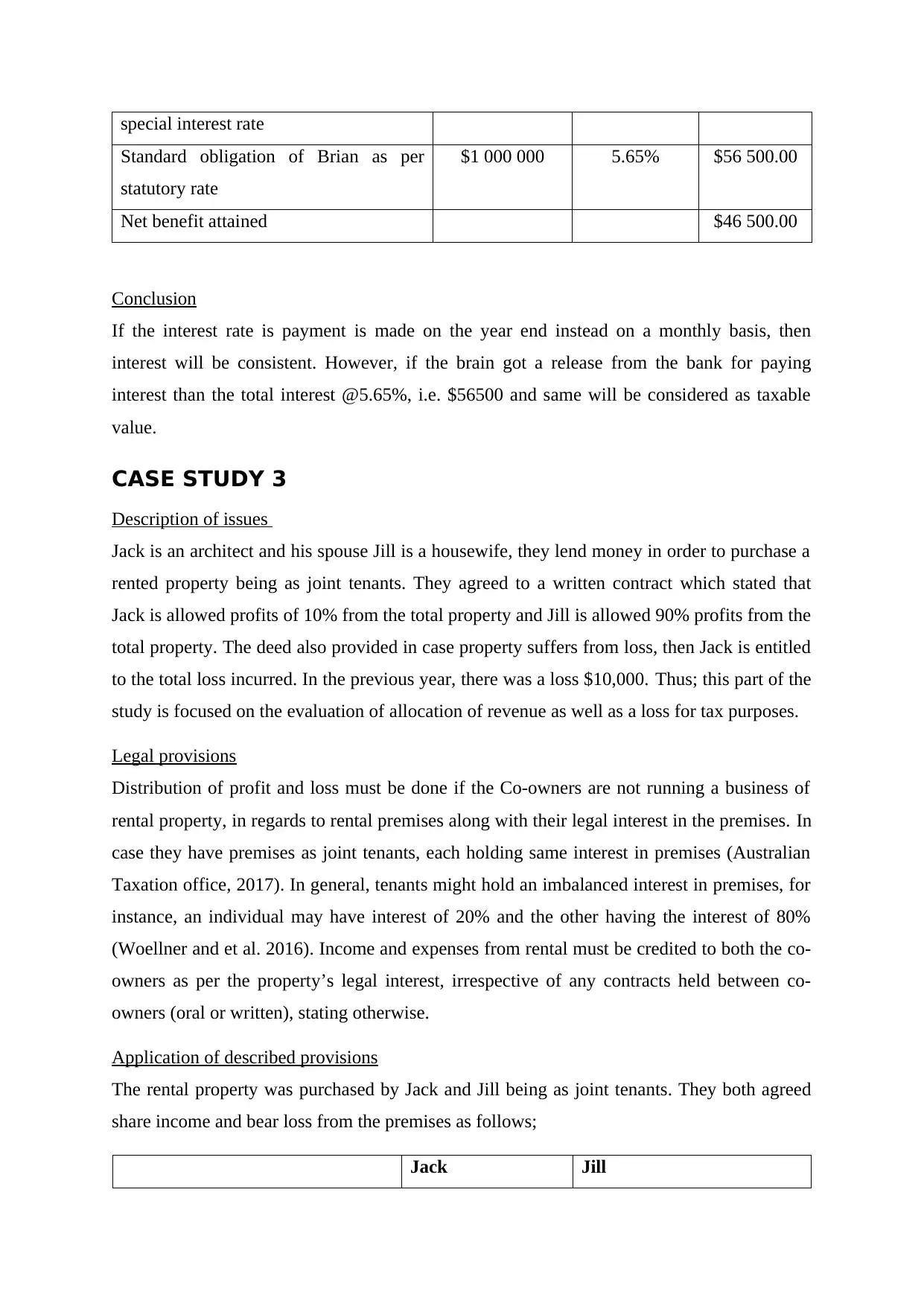

Table 3: Statement showing computation of taxable value on which FBT will be payable

Particulars Loan amount Interest rate Amount1

Interest obligation of Brian as per $1 000 000 1% $10 000.00

1 (Loan amount * Interest rate)

Painting $9 000 $1 000 $1 000.00 - $9 000.00 -$8 000.00

Antique chair $3 000 $1 000 $1 000.00 - $3 000.00 -$2 000.00

Sound system $12 000 $11 000 $11 000.00 - $12 000.00 -$1 000.00

Net capital gain $5 000.00

Conclusion

In accordance with the above calculation it can be said that there is a net gain of $5 000.00 to

Eric, so he is liable to pay tax on the net computed amount.

CASE STUDY 2

Description of issues

Brian is working as an executive in a bank. In its remuneration package part, the employer of

Brian offered him a 3-year loan of a total amount of $1m at the rate of interest of 1% per

annum (payment to be made on a monthly basis). This part would assess calculation of the

taxable value of this FBT regarding the 2016 and 2017 Fringe benefit year and effect if

interest was to be made at the loan’s end instead of monthly payments and in the situation

where the bank had released Brian from the obligation of payment of the interest charges on

loan.

Legal provisions

FBT arise when the loan arise if the loan is offered to the employee, in which no or less

interest if charge upon loan (Faccio and Xu, 2015). Fringe Benefit's taxable loan value is

determined by the interest rate charged on loan and standard interest rate which is 5.65% as

per TD 2016/5 for FBT year1 April 2016 to 31 March 2017 (Braverman, Marsden and Sadiq,

2015).

Application of described provisions

By applying above described provisions computation of taxable value on which FBT will be

payable is as follows:

Table 3: Statement showing computation of taxable value on which FBT will be payable

Particulars Loan amount Interest rate Amount1

Interest obligation of Brian as per $1 000 000 1% $10 000.00

1 (Loan amount * Interest rate)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

special interest rate

Standard obligation of Brian as per

statutory rate

$1 000 000 5.65% $56 500.00

Net benefit attained $46 500.00

Conclusion

If the interest rate is payment is made on the year end instead on a monthly basis, then

interest will be consistent. However, if the brain got a release from the bank for paying

interest than the total interest @5.65%, i.e. $56500 and same will be considered as taxable

value.

CASE STUDY 3

Description of issues

Jack is an architect and his spouse Jill is a housewife, they lend money in order to purchase a

rented property being as joint tenants. They agreed to a written contract which stated that

Jack is allowed profits of 10% from the total property and Jill is allowed 90% profits from the

total property. The deed also provided in case property suffers from loss, then Jack is entitled

to the total loss incurred. In the previous year, there was a loss $10,000. Thus; this part of the

study is focused on the evaluation of allocation of revenue as well as a loss for tax purposes.

Legal provisions

Distribution of profit and loss must be done if the Co-owners are not running a business of

rental property, in regards to rental premises along with their legal interest in the premises. In

case they have premises as joint tenants, each holding same interest in premises (Australian

Taxation office, 2017). In general, tenants might hold an imbalanced interest in premises, for

instance, an individual may have interest of 20% and the other having the interest of 80%

(Woellner and et al. 2016). Income and expenses from rental must be credited to both the co-

owners as per the property’s legal interest, irrespective of any contracts held between co-

owners (oral or written), stating otherwise.

Application of described provisions

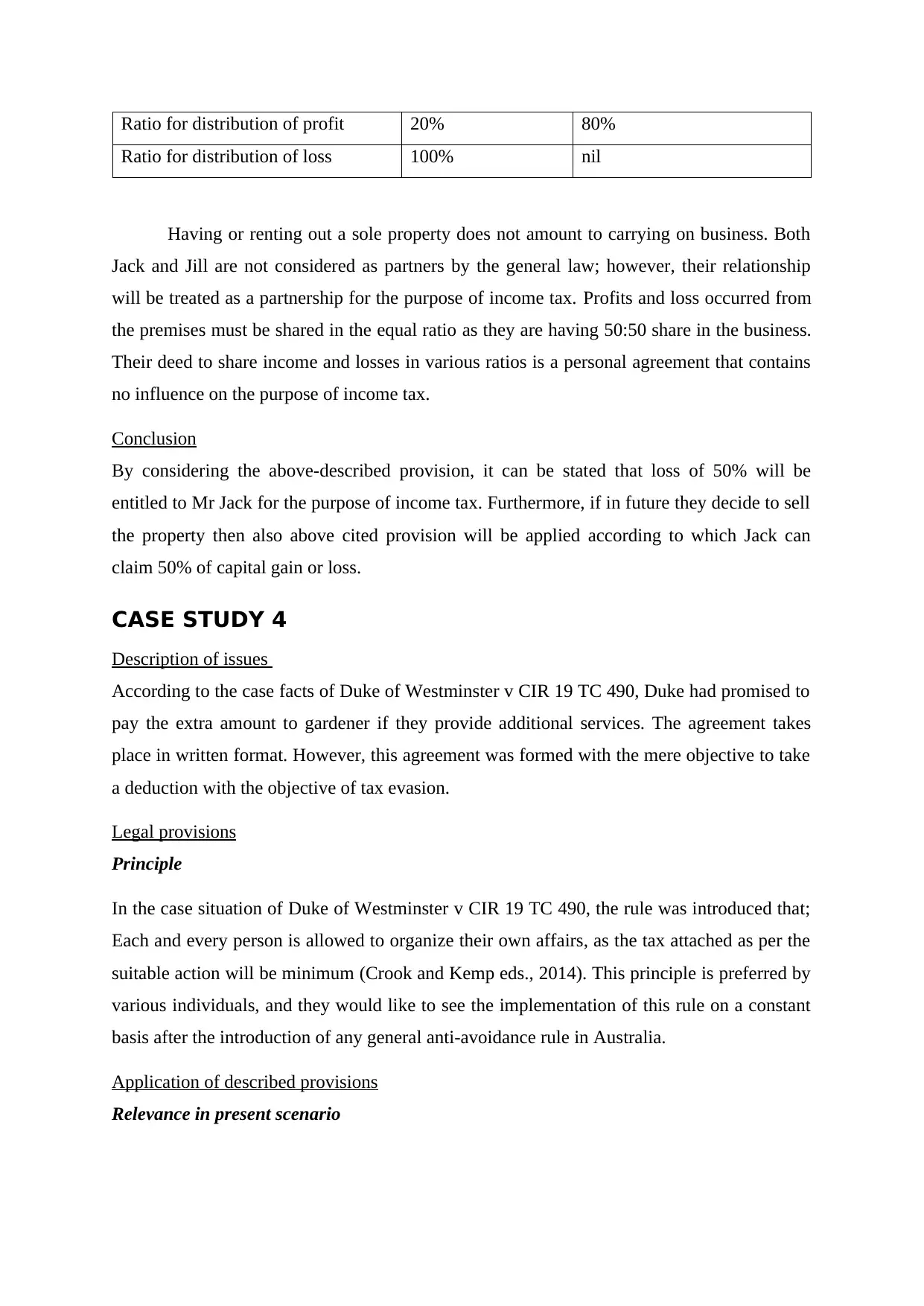

The rental property was purchased by Jack and Jill being as joint tenants. They both agreed

share income and bear loss from the premises as follows;

Jack Jill

Standard obligation of Brian as per

statutory rate

$1 000 000 5.65% $56 500.00

Net benefit attained $46 500.00

Conclusion

If the interest rate is payment is made on the year end instead on a monthly basis, then

interest will be consistent. However, if the brain got a release from the bank for paying

interest than the total interest @5.65%, i.e. $56500 and same will be considered as taxable

value.

CASE STUDY 3

Description of issues

Jack is an architect and his spouse Jill is a housewife, they lend money in order to purchase a

rented property being as joint tenants. They agreed to a written contract which stated that

Jack is allowed profits of 10% from the total property and Jill is allowed 90% profits from the

total property. The deed also provided in case property suffers from loss, then Jack is entitled

to the total loss incurred. In the previous year, there was a loss $10,000. Thus; this part of the

study is focused on the evaluation of allocation of revenue as well as a loss for tax purposes.

Legal provisions

Distribution of profit and loss must be done if the Co-owners are not running a business of

rental property, in regards to rental premises along with their legal interest in the premises. In

case they have premises as joint tenants, each holding same interest in premises (Australian

Taxation office, 2017). In general, tenants might hold an imbalanced interest in premises, for

instance, an individual may have interest of 20% and the other having the interest of 80%

(Woellner and et al. 2016). Income and expenses from rental must be credited to both the co-

owners as per the property’s legal interest, irrespective of any contracts held between co-

owners (oral or written), stating otherwise.

Application of described provisions

The rental property was purchased by Jack and Jill being as joint tenants. They both agreed

share income and bear loss from the premises as follows;

Jack Jill

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ratio for distribution of profit 20% 80%

Ratio for distribution of loss 100% nil

Having or renting out a sole property does not amount to carrying on business. Both

Jack and Jill are not considered as partners by the general law; however, their relationship

will be treated as a partnership for the purpose of income tax. Profits and loss occurred from

the premises must be shared in the equal ratio as they are having 50:50 share in the business.

Their deed to share income and losses in various ratios is a personal agreement that contains

no influence on the purpose of income tax.

Conclusion

By considering the above-described provision, it can be stated that loss of 50% will be

entitled to Mr Jack for the purpose of income tax. Furthermore, if in future they decide to sell

the property then also above cited provision will be applied according to which Jack can

claim 50% of capital gain or loss.

CASE STUDY 4

Description of issues

According to the case facts of Duke of Westminster v CIR 19 TC 490, Duke had promised to

pay the extra amount to gardener if they provide additional services. The agreement takes

place in written format. However, this agreement was formed with the mere objective to take

a deduction with the objective of tax evasion.

Legal provisions

Principle

In the case situation of Duke of Westminster v CIR 19 TC 490, the rule was introduced that;

Each and every person is allowed to organize their own affairs, as the tax attached as per the

suitable action will be minimum (Crook and Kemp eds., 2014). This principle is preferred by

various individuals, and they would like to see the implementation of this rule on a constant

basis after the introduction of any general anti-avoidance rule in Australia.

Application of described provisions

Relevance in present scenario

Ratio for distribution of loss 100% nil

Having or renting out a sole property does not amount to carrying on business. Both

Jack and Jill are not considered as partners by the general law; however, their relationship

will be treated as a partnership for the purpose of income tax. Profits and loss occurred from

the premises must be shared in the equal ratio as they are having 50:50 share in the business.

Their deed to share income and losses in various ratios is a personal agreement that contains

no influence on the purpose of income tax.

Conclusion

By considering the above-described provision, it can be stated that loss of 50% will be

entitled to Mr Jack for the purpose of income tax. Furthermore, if in future they decide to sell

the property then also above cited provision will be applied according to which Jack can

claim 50% of capital gain or loss.

CASE STUDY 4

Description of issues

According to the case facts of Duke of Westminster v CIR 19 TC 490, Duke had promised to

pay the extra amount to gardener if they provide additional services. The agreement takes

place in written format. However, this agreement was formed with the mere objective to take

a deduction with the objective of tax evasion.

Legal provisions

Principle

In the case situation of Duke of Westminster v CIR 19 TC 490, the rule was introduced that;

Each and every person is allowed to organize their own affairs, as the tax attached as per the

suitable action will be minimum (Crook and Kemp eds., 2014). This principle is preferred by

various individuals, and they would like to see the implementation of this rule on a constant

basis after the introduction of any general anti-avoidance rule in Australia.

Application of described provisions

Relevance in present scenario

In the previous year, the constitution has been establishing that needs advisors to inform

HMRC of some scheme kind that can form tax evasion. However, this will be not be seen in

the all over the board, and it stays to be observed that what actions will be taken while

receiving such type of notifications (AbdulRazaq and Adam, 2015). It might be observed in

settlement of time when these rule will act as an originator to the establishment of new

provisions rather more wide-ranging existing provisions.

Conclusion

Lord Wilberforce found that even though the principle of Duke of Westminster prevented the

court from looking after a real transaction to certain supposed fundamental substance, it will

not ‘oblige the court to look over the document in blinkers, inaccessible from any context to

which it properly belongs’.

The court must determine the transaction’s legal nature by which it is required to make

attachment of a attach a tax or a tax result and in case it comes out as series or mixture of

transactions, aimed to work as such, it is that combination or series which is required to be

considered by regulatory authorities in case analysis.

In such type of cases, the representative ‘must search out facts and further make a decision by

considering the matter (reviewable) of law to categories whether the issue is covered in the

composite transaction and it is supported by the independent transaction.

By considering this fact, it has been made clear that the scheme was only for the tax

avoidance, without commercial justification, the purpose was to pursue all it stages to

complete end. It would thus be irrelevant to assess just one step in the process of isolation.

CASE STUDY 5

Description of issues

Bill owns a huge land of which there are extensive tall pine trees. Bill aims to make use of

land by grazing their sheep and thus desires to make it clear from the start. He discovered that

a sorting business is arranged to pay him $1,000 for every 100 metres of timber to logging

company which it can take from his land. Thus present part of study deals with providing

advice to Bill as to inform him would be assessed from the receipts from this cited

arrangement and consequence if he gets lump sum payment of $50,000 for granting a right to

the logging company for removal of timber as much as required for his land.

HMRC of some scheme kind that can form tax evasion. However, this will be not be seen in

the all over the board, and it stays to be observed that what actions will be taken while

receiving such type of notifications (AbdulRazaq and Adam, 2015). It might be observed in

settlement of time when these rule will act as an originator to the establishment of new

provisions rather more wide-ranging existing provisions.

Conclusion

Lord Wilberforce found that even though the principle of Duke of Westminster prevented the

court from looking after a real transaction to certain supposed fundamental substance, it will

not ‘oblige the court to look over the document in blinkers, inaccessible from any context to

which it properly belongs’.

The court must determine the transaction’s legal nature by which it is required to make

attachment of a attach a tax or a tax result and in case it comes out as series or mixture of

transactions, aimed to work as such, it is that combination or series which is required to be

considered by regulatory authorities in case analysis.

In such type of cases, the representative ‘must search out facts and further make a decision by

considering the matter (reviewable) of law to categories whether the issue is covered in the

composite transaction and it is supported by the independent transaction.

By considering this fact, it has been made clear that the scheme was only for the tax

avoidance, without commercial justification, the purpose was to pursue all it stages to

complete end. It would thus be irrelevant to assess just one step in the process of isolation.

CASE STUDY 5

Description of issues

Bill owns a huge land of which there are extensive tall pine trees. Bill aims to make use of

land by grazing their sheep and thus desires to make it clear from the start. He discovered that

a sorting business is arranged to pay him $1,000 for every 100 metres of timber to logging

company which it can take from his land. Thus present part of study deals with providing

advice to Bill as to inform him would be assessed from the receipts from this cited

arrangement and consequence if he gets lump sum payment of $50,000 for granting a right to

the logging company for removal of timber as much as required for his land.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Legal provisions

Disposal of standing timber, not in the ordinary course of business

According to point 22 of ruling TR 95/6; a taxpayer owning disposal of trees, that is planted

and have a tendency for the sale purpose might result in the inclusion of sale value in the

assessable income in the year in which disposal takes the place of taxpayer under subsection

36(1) (Sceales, 2015). This might so if or if not the taxpayer is running a business of forest

work, from the time the taxpayer is running the business and disposal of trees is not done in

the regular business course.

For applicability of this provision, primary requirement is that the trees must represent the

business entirely or part of it. Next, the point 2s of ruling TR 95/6 reveals that the tree’s value

must be either;

On the day of disposal the market value will be considered; or

According to paragraph 36(8) (a) if Commissioner has an opinion that there is lack of

evidence of the MV –that value which is considered by the Commissioner.

Disposal of rights to standing timber

As per the point 25 of ruling TR 95/6, a taxpayer who is running the forest operations might

put its standing timber into a sale by providing permission to a person to remove it, either

having the right or not to cut the timber. The income has been generated from the sale

purpose can be assessable according to subsection 25(1). Furthermore, royalty will be

received by the taxpayer in regards to providing right for procurement of timber on land

possessed by the taxpayer will be part of the assessable income of the taxpayer according to

(subsection 25(1)) (Barkoczy, 2016). This provisions will be considered in the computation

of assessable income of the recipient irrespective of the fact that granting the right by the

taxpayer is not carrying on a business of forest operations.

Application of described provisions

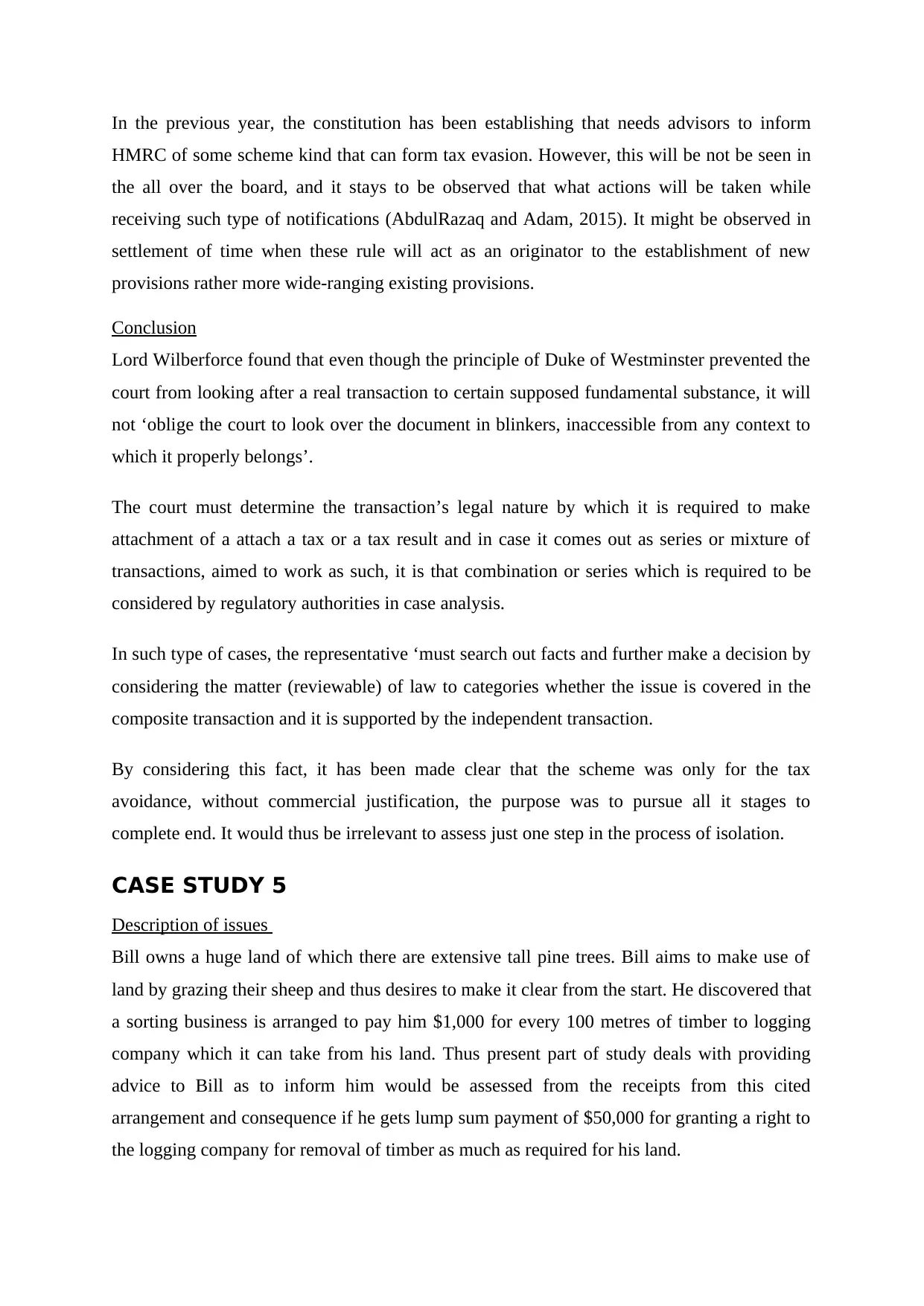

Table 4: Application of ruling TR 95/6 on the cited case

Transaction Applicable

section

Assessability

of income

Situation 1 Disposal of standing timber by Bill for $1,000

for every 100 metres of timber to logging

company, not in the ordinary course of business

36(1) Yes

Disposal of standing timber, not in the ordinary course of business

According to point 22 of ruling TR 95/6; a taxpayer owning disposal of trees, that is planted

and have a tendency for the sale purpose might result in the inclusion of sale value in the

assessable income in the year in which disposal takes the place of taxpayer under subsection

36(1) (Sceales, 2015). This might so if or if not the taxpayer is running a business of forest

work, from the time the taxpayer is running the business and disposal of trees is not done in

the regular business course.

For applicability of this provision, primary requirement is that the trees must represent the

business entirely or part of it. Next, the point 2s of ruling TR 95/6 reveals that the tree’s value

must be either;

On the day of disposal the market value will be considered; or

According to paragraph 36(8) (a) if Commissioner has an opinion that there is lack of

evidence of the MV –that value which is considered by the Commissioner.

Disposal of rights to standing timber

As per the point 25 of ruling TR 95/6, a taxpayer who is running the forest operations might

put its standing timber into a sale by providing permission to a person to remove it, either

having the right or not to cut the timber. The income has been generated from the sale

purpose can be assessable according to subsection 25(1). Furthermore, royalty will be

received by the taxpayer in regards to providing right for procurement of timber on land

possessed by the taxpayer will be part of the assessable income of the taxpayer according to

(subsection 25(1)) (Barkoczy, 2016). This provisions will be considered in the computation

of assessable income of the recipient irrespective of the fact that granting the right by the

taxpayer is not carrying on a business of forest operations.

Application of described provisions

Table 4: Application of ruling TR 95/6 on the cited case

Transaction Applicable

section

Assessability

of income

Situation 1 Disposal of standing timber by Bill for $1,000

for every 100 metres of timber to logging

company, not in the ordinary course of business

36(1) Yes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Situation 2 Disposal of rights to standing timber 25(1) Yes

Conclusion

In accordance with the applicability of above-described provisions, if only timber is sold than

income will be assessable under section 36(1) and in case of rights for lump sum amount is

sold then taxability will be under section 25(1) and computation will be according to point 25

of ruling TR 95/6.

CONCLUSION

In accordance with the present case study; conclusion can be drawn that tax payers are

required to consider relevant provisions to determine tax liability and should comply with the

same to discharge their obligation in an appropriate manner.

Conclusion

In accordance with the applicability of above-described provisions, if only timber is sold than

income will be assessable under section 36(1) and in case of rights for lump sum amount is

sold then taxability will be under section 25(1) and computation will be according to point 25

of ruling TR 95/6.

CONCLUSION

In accordance with the present case study; conclusion can be drawn that tax payers are

required to consider relevant provisions to determine tax liability and should comply with the

same to discharge their obligation in an appropriate manner.

REFERENCES

Books and Journals

AbdulRazaq, M.T. and Adam, K.I., 2015. Anti-Avoidance Legislations: Issues & Doubts in

the Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17,

p.1.

Crook, T. and Kemp, P.A. eds., 2014. Private rental housing: Comparative perspectives.

Edward Elgar Publishing.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Sceales, R.W.F., 2015. A review of the trend in the judicial interpretation, and judicial

attitudes towards tax avoidance in the United Kingdom, Australia and South Africa, with

reference to the" declaratory" and" choice" theories of jurisprudence (Doctoral dissertation).

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Online

Australian Taxation office. 2017. Co-ownership of rental property. [Online]. Available

through <https://www.ato.gov.au/Forms/Rental-properties-2013-14/?page=5>. [Accessed on

14th September 2017].

Australian Taxation office. 2017. Working out your capital gain. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 14th September 2017].

Books and Journals

AbdulRazaq, M.T. and Adam, K.I., 2015. Anti-Avoidance Legislations: Issues & Doubts in

the Application of Tax Rules in Nigeria. AGORA Int'l J. Jurid. Sci., p.1.

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Braverman, D., Marsden, S. and Sadiq, K., 2015. Assessing Taxpayer Response to

Legislative Changes: A Case Study of In-House Fringe Benefits Rules. J. Austl. Tax'n, 17,

p.1.

Crook, T. and Kemp, P.A. eds., 2014. Private rental housing: Comparative perspectives.

Edward Elgar Publishing.

Faccio, M. and Xu, J., 2015. Taxes and capital structure. Journal of Financial and

Quantitative Analysis, 50(3), pp.277-300.

Harding, M., 2013. Taxation of dividend, interest, and capital gain income.

Sceales, R.W.F., 2015. A review of the trend in the judicial interpretation, and judicial

attitudes towards tax avoidance in the United Kingdom, Australia and South Africa, with

reference to the" declaratory" and" choice" theories of jurisprudence (Doctoral dissertation).

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Online

Australian Taxation office. 2017. Co-ownership of rental property. [Online]. Available

through <https://www.ato.gov.au/Forms/Rental-properties-2013-14/?page=5>. [Accessed on

14th September 2017].

Australian Taxation office. 2017. Working out your capital gain. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/

Working-out-your-capital-gain/>. [Accessed on 14th September 2017].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.