La Trobe University ACC3TAX: Taxation Assignment Solution - SP1 2019

VerifiedAdded on 2023/03/17

|8

|1656

|94

Homework Assignment

AI Summary

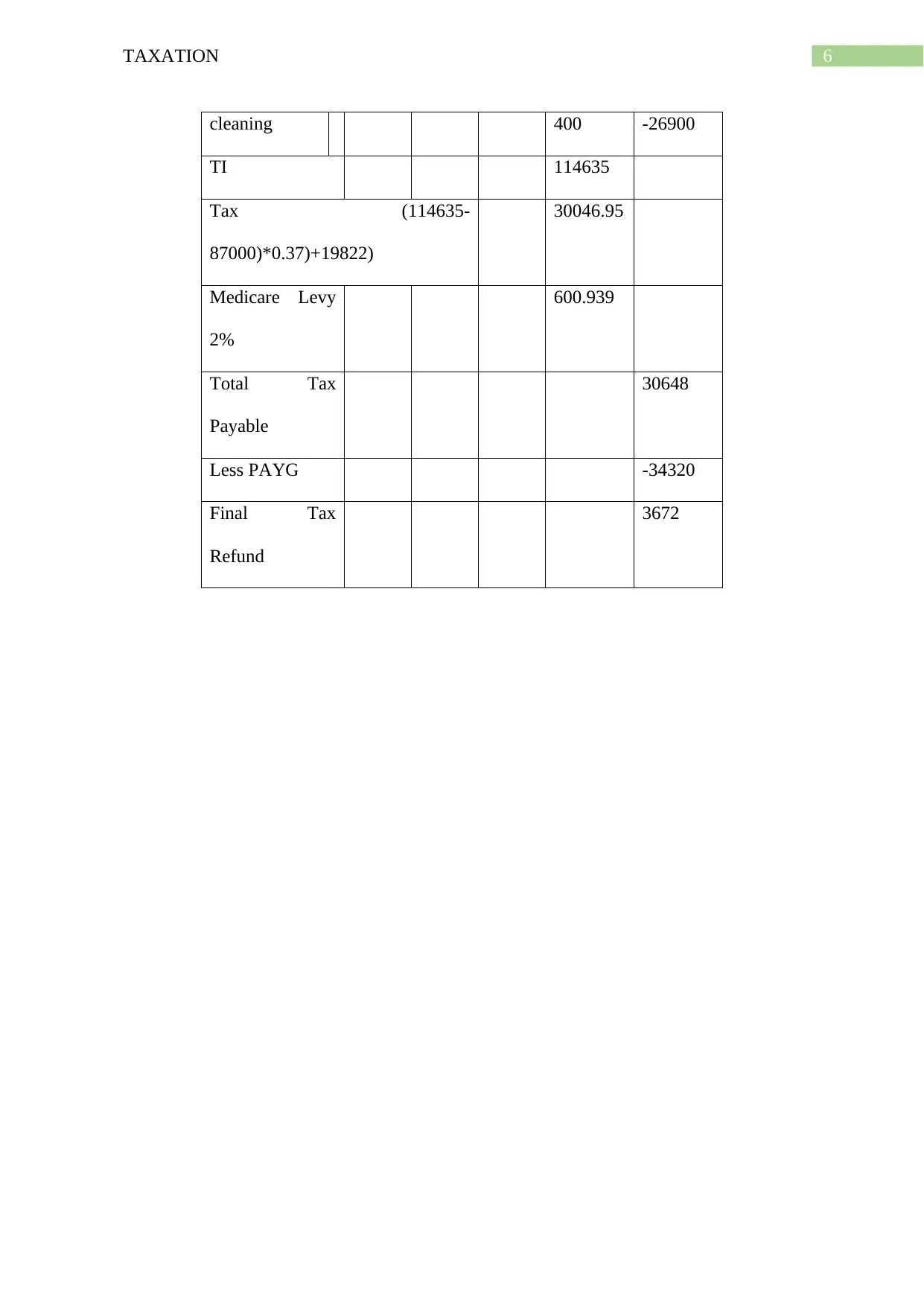

This document provides a comprehensive solution to a taxation assignment, focusing on the tax implications for Chris Matthews. The analysis begins with determining the capital gains tax (CGT) liability arising from the sale of a house, including calculations for capital proceeds, cost base, and applicable discounts. It then addresses the deductibility of legal fees incurred for defending a lawsuit, referencing relevant legislation and case law to determine if such expenses can be deducted from taxable income. Finally, the solution outlines the appropriate accounting method for professionals, specifically the cash basis method, and includes detailed calculations of Mr. Matthews's taxable income, deductions, and tax payable, incorporating relevant tax brackets and levies. The document concludes with a bibliography of the cited legal and case references.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.