Semester 2 ACC3009 Taxation in Accounting Assignment Solution

VerifiedAdded on 2022/11/28

|12

|2336

|185

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation in Accounting assignment, likely for a university course. It addresses various aspects of taxation, including questions on motor vehicle depreciation and overlap profits, employment income calculations, and VAT computations, offering a detailed breakdown of output and input VAT. The assignment also covers group relief, capital gains tax on the sale of shares and residential property, and inheritance tax liabilities. Furthermore, it explores the ethical principles in business, analyzing a case study, and evaluating the merits and demerits of corporate tax incentives. The solution includes detailed calculations, explanations, and answers to each question, providing a valuable resource for students studying taxation.

TAXATION IN ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................4

Question 4..................................................................................................................................5

Question 5..................................................................................................................................6

QUESTION- 6...........................................................................................................................6

1) Sale of shares in Halliday Limited.....................................................................................6

2) Sale of residential property................................................................................................9

QUESTION- 7...........................................................................................................................9

Merits and demerits of the corporate tax incentives as a means of promoting business

growth, investment and entrepreneurship..............................................................................9

REFERENCES.........................................................................................................................11

Question 1..................................................................................................................................3

Question 2..................................................................................................................................4

Question 3..................................................................................................................................4

Question 4..................................................................................................................................5

Question 5..................................................................................................................................6

QUESTION- 6...........................................................................................................................6

1) Sale of shares in Halliday Limited.....................................................................................6

2) Sale of residential property................................................................................................9

QUESTION- 7...........................................................................................................................9

Merits and demerits of the corporate tax incentives as a means of promoting business

growth, investment and entrepreneurship..............................................................................9

REFERENCES.........................................................................................................................11

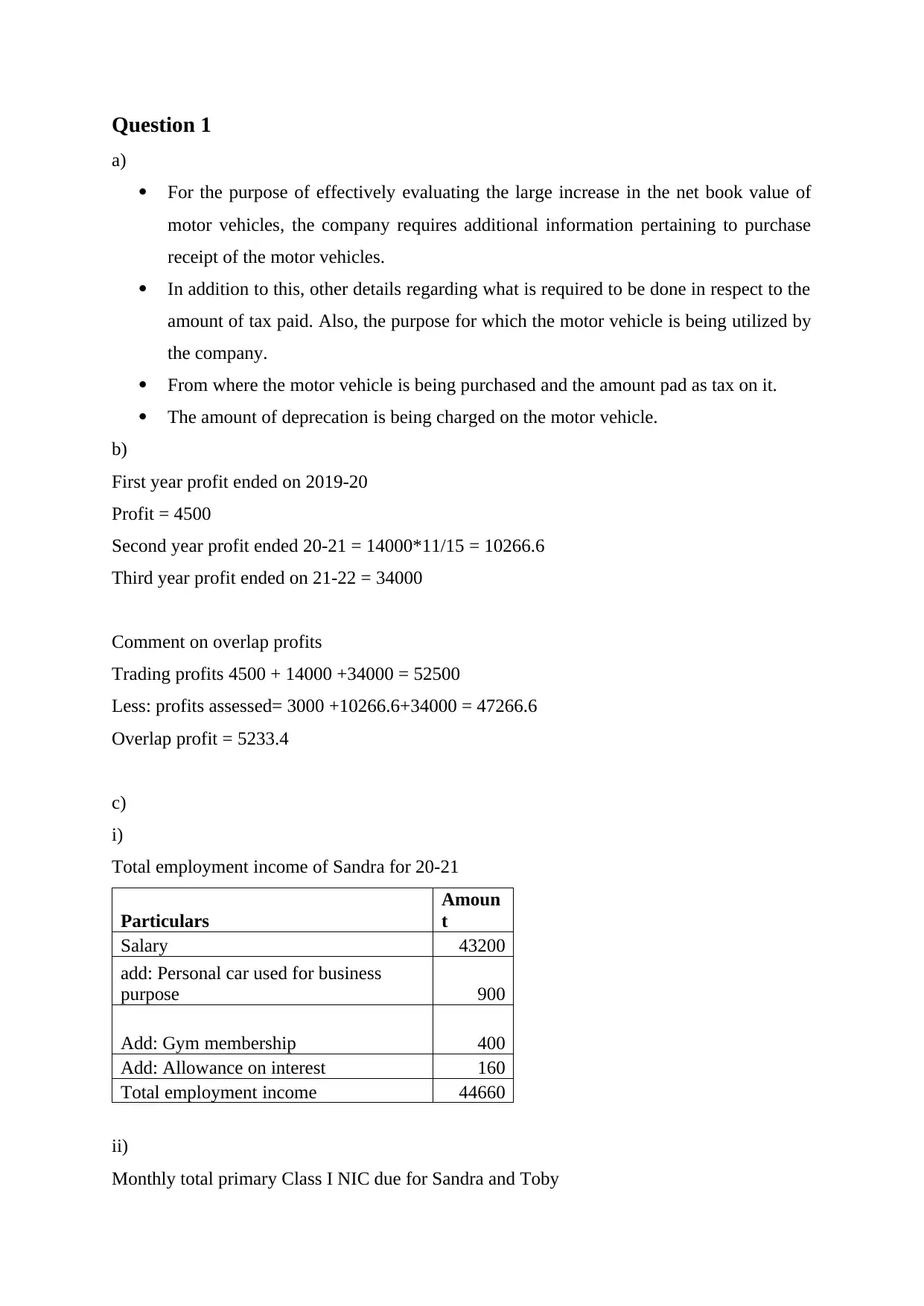

Question 1

a)

For the purpose of effectively evaluating the large increase in the net book value of

motor vehicles, the company requires additional information pertaining to purchase

receipt of the motor vehicles.

In addition to this, other details regarding what is required to be done in respect to the

amount of tax paid. Also, the purpose for which the motor vehicle is being utilized by

the company.

From where the motor vehicle is being purchased and the amount pad as tax on it.

The amount of deprecation is being charged on the motor vehicle.

b)

First year profit ended on 2019-20

Profit = 4500

Second year profit ended 20-21 = 14000*11/15 = 10266.6

Third year profit ended on 21-22 = 34000

Comment on overlap profits

Trading profits 4500 + 14000 +34000 = 52500

Less: profits assessed= 3000 +10266.6+34000 = 47266.6

Overlap profit = 5233.4

c)

i)

Total employment income of Sandra for 20-21

Particulars

Amoun

t

Salary 43200

add: Personal car used for business

purpose 900

Add: Gym membership 400

Add: Allowance on interest 160

Total employment income 44660

ii)

Monthly total primary Class I NIC due for Sandra and Toby

a)

For the purpose of effectively evaluating the large increase in the net book value of

motor vehicles, the company requires additional information pertaining to purchase

receipt of the motor vehicles.

In addition to this, other details regarding what is required to be done in respect to the

amount of tax paid. Also, the purpose for which the motor vehicle is being utilized by

the company.

From where the motor vehicle is being purchased and the amount pad as tax on it.

The amount of deprecation is being charged on the motor vehicle.

b)

First year profit ended on 2019-20

Profit = 4500

Second year profit ended 20-21 = 14000*11/15 = 10266.6

Third year profit ended on 21-22 = 34000

Comment on overlap profits

Trading profits 4500 + 14000 +34000 = 52500

Less: profits assessed= 3000 +10266.6+34000 = 47266.6

Overlap profit = 5233.4

c)

i)

Total employment income of Sandra for 20-21

Particulars

Amoun

t

Salary 43200

add: Personal car used for business

purpose 900

Add: Gym membership 400

Add: Allowance on interest 160

Total employment income 44660

ii)

Monthly total primary Class I NIC due for Sandra and Toby

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

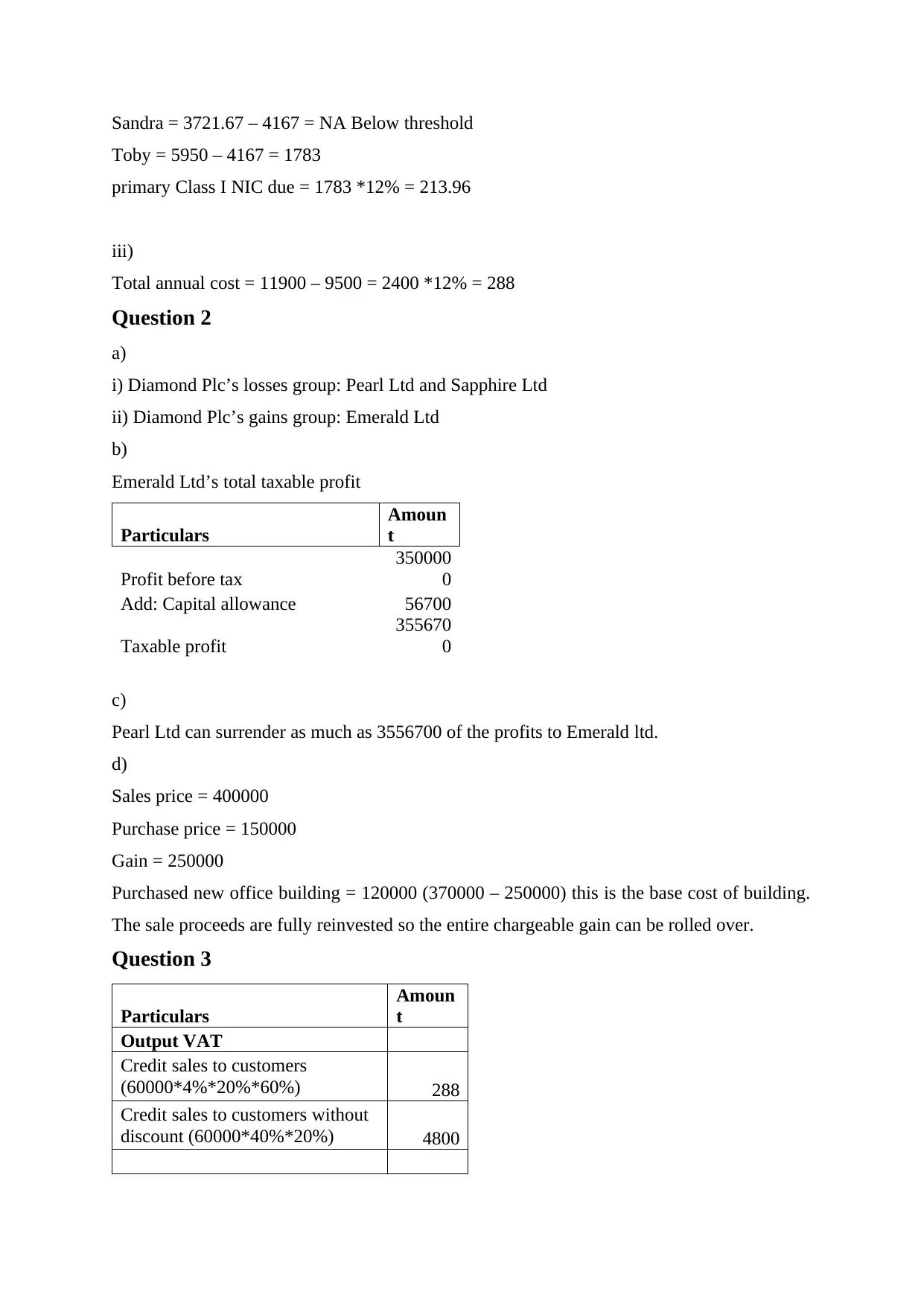

Sandra = 3721.67 – 4167 = NA Below threshold

Toby = 5950 – 4167 = 1783

primary Class I NIC due = 1783 *12% = 213.96

iii)

Total annual cost = 11900 – 9500 = 2400 *12% = 288

Question 2

a)

i) Diamond Plc’s losses group: Pearl Ltd and Sapphire Ltd

ii) Diamond Plc’s gains group: Emerald Ltd

b)

Emerald Ltd’s total taxable profit

Particulars

Amoun

t

Profit before tax

350000

0

Add: Capital allowance 56700

Taxable profit

355670

0

c)

Pearl Ltd can surrender as much as 3556700 of the profits to Emerald ltd.

d)

Sales price = 400000

Purchase price = 150000

Gain = 250000

Purchased new office building = 120000 (370000 – 250000) this is the base cost of building.

The sale proceeds are fully reinvested so the entire chargeable gain can be rolled over.

Question 3

Particulars

Amoun

t

Output VAT

Credit sales to customers

(60000*4%*20%*60%) 288

Credit sales to customers without

discount (60000*40%*20%) 4800

Toby = 5950 – 4167 = 1783

primary Class I NIC due = 1783 *12% = 213.96

iii)

Total annual cost = 11900 – 9500 = 2400 *12% = 288

Question 2

a)

i) Diamond Plc’s losses group: Pearl Ltd and Sapphire Ltd

ii) Diamond Plc’s gains group: Emerald Ltd

b)

Emerald Ltd’s total taxable profit

Particulars

Amoun

t

Profit before tax

350000

0

Add: Capital allowance 56700

Taxable profit

355670

0

c)

Pearl Ltd can surrender as much as 3556700 of the profits to Emerald ltd.

d)

Sales price = 400000

Purchase price = 150000

Gain = 250000

Purchased new office building = 120000 (370000 – 250000) this is the base cost of building.

The sale proceeds are fully reinvested so the entire chargeable gain can be rolled over.

Question 3

Particulars

Amoun

t

Output VAT

Credit sales to customers

(60000*4%*20%*60%) 288

Credit sales to customers without

discount (60000*40%*20%) 4800

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

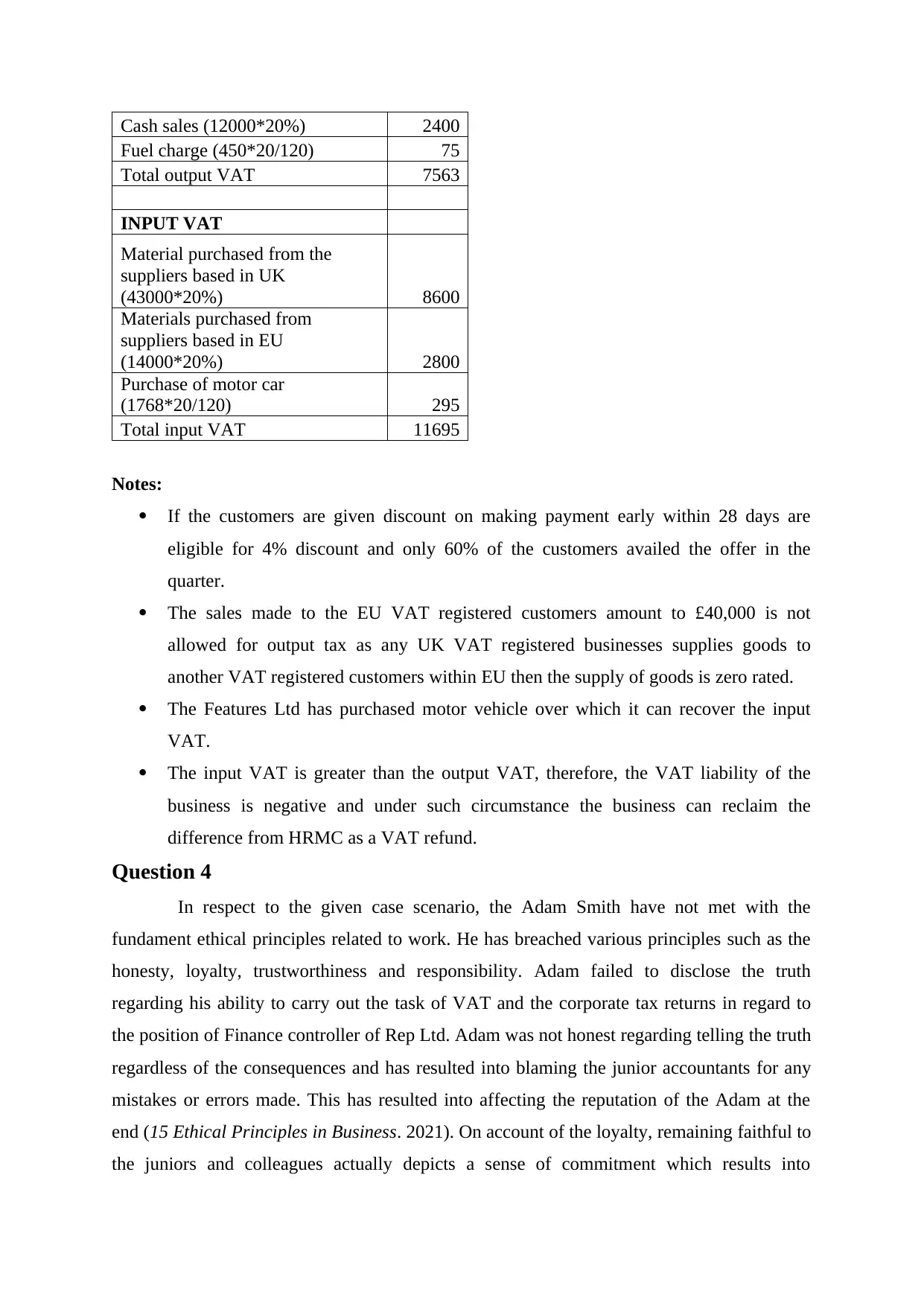

Cash sales (12000*20%) 2400

Fuel charge (450*20/120) 75

Total output VAT 7563

INPUT VAT

Material purchased from the

suppliers based in UK

(43000*20%) 8600

Materials purchased from

suppliers based in EU

(14000*20%) 2800

Purchase of motor car

(1768*20/120) 295

Total input VAT 11695

Notes:

If the customers are given discount on making payment early within 28 days are

eligible for 4% discount and only 60% of the customers availed the offer in the

quarter.

The sales made to the EU VAT registered customers amount to £40,000 is not

allowed for output tax as any UK VAT registered businesses supplies goods to

another VAT registered customers within EU then the supply of goods is zero rated.

The Features Ltd has purchased motor vehicle over which it can recover the input

VAT.

The input VAT is greater than the output VAT, therefore, the VAT liability of the

business is negative and under such circumstance the business can reclaim the

difference from HRMC as a VAT refund.

Question 4

In respect to the given case scenario, the Adam Smith have not met with the

fundament ethical principles related to work. He has breached various principles such as the

honesty, loyalty, trustworthiness and responsibility. Adam failed to disclose the truth

regarding his ability to carry out the task of VAT and the corporate tax returns in regard to

the position of Finance controller of Rep Ltd. Adam was not honest regarding telling the truth

regardless of the consequences and has resulted into blaming the junior accountants for any

mistakes or errors made. This has resulted into affecting the reputation of the Adam at the

end (15 Ethical Principles in Business. 2021). On account of the loyalty, remaining faithful to

the juniors and colleagues actually depicts a sense of commitment which results into

Fuel charge (450*20/120) 75

Total output VAT 7563

INPUT VAT

Material purchased from the

suppliers based in UK

(43000*20%) 8600

Materials purchased from

suppliers based in EU

(14000*20%) 2800

Purchase of motor car

(1768*20/120) 295

Total input VAT 11695

Notes:

If the customers are given discount on making payment early within 28 days are

eligible for 4% discount and only 60% of the customers availed the offer in the

quarter.

The sales made to the EU VAT registered customers amount to £40,000 is not

allowed for output tax as any UK VAT registered businesses supplies goods to

another VAT registered customers within EU then the supply of goods is zero rated.

The Features Ltd has purchased motor vehicle over which it can recover the input

VAT.

The input VAT is greater than the output VAT, therefore, the VAT liability of the

business is negative and under such circumstance the business can reclaim the

difference from HRMC as a VAT refund.

Question 4

In respect to the given case scenario, the Adam Smith have not met with the

fundament ethical principles related to work. He has breached various principles such as the

honesty, loyalty, trustworthiness and responsibility. Adam failed to disclose the truth

regarding his ability to carry out the task of VAT and the corporate tax returns in regard to

the position of Finance controller of Rep Ltd. Adam was not honest regarding telling the truth

regardless of the consequences and has resulted into blaming the junior accountants for any

mistakes or errors made. This has resulted into affecting the reputation of the Adam at the

end (15 Ethical Principles in Business. 2021). On account of the loyalty, remaining faithful to

the juniors and colleagues actually depicts a sense of commitment which results into

developing long lasting relationship and attaining future success. The company has even

asked Adam if he wants to undertake the specific training regarding it, to which he denied

with the only reason that he did not want to lose face so he refused to take the training and

also put the blame on the junior assistant accountant and has continued to submit the return

with the expectation that no error will occur.

Another fundamental ethical principle breached is the trustworthiness which also

involves being dependable and meeting with the obligations. It involves arriving at time,

meeting with the deadlines and highlighting consistency in work. But Adam failed to be

committed towards his work as it was not having relevant skills and knowledge in relation to

the position given which affected the work. The last principle breached is responsibility

which involves the taking ownership of the tasks and the responsibility pertaining to the

effect of the actions being undertaken as the employer and employees are mainly depend

upon the responsible workers in order to undertake the decisions. Therefore, all these factors

have resulted into breach in the appointment Adam Smith and his role as financial controller.

Question 5

IHT liabilities are as follows:

Lifetime transfers

Net chargeable transfer on December 2011 280000

Net chargeable transfer in May 2018 227000

Total 507000

IHT liability

325000 at nil%

182000 (507000 - 325000) *20% 36400

IHT liability already paid 36400

Additional liability arising on death

Chargeable estate 1500000

IHT liability @40% 600000

QUESTION- 6

1) Sale of shares in Halliday Limited

Assessee- Gordon

Shares acquired on 1st January, 2018 in Halliday Limited

15000 shares * 1 per unit of share= £15000

On 1st March, 2019 became a full time worker in Halliday Limited at an annual salary of

£100000 per year

asked Adam if he wants to undertake the specific training regarding it, to which he denied

with the only reason that he did not want to lose face so he refused to take the training and

also put the blame on the junior assistant accountant and has continued to submit the return

with the expectation that no error will occur.

Another fundamental ethical principle breached is the trustworthiness which also

involves being dependable and meeting with the obligations. It involves arriving at time,

meeting with the deadlines and highlighting consistency in work. But Adam failed to be

committed towards his work as it was not having relevant skills and knowledge in relation to

the position given which affected the work. The last principle breached is responsibility

which involves the taking ownership of the tasks and the responsibility pertaining to the

effect of the actions being undertaken as the employer and employees are mainly depend

upon the responsible workers in order to undertake the decisions. Therefore, all these factors

have resulted into breach in the appointment Adam Smith and his role as financial controller.

Question 5

IHT liabilities are as follows:

Lifetime transfers

Net chargeable transfer on December 2011 280000

Net chargeable transfer in May 2018 227000

Total 507000

IHT liability

325000 at nil%

182000 (507000 - 325000) *20% 36400

IHT liability already paid 36400

Additional liability arising on death

Chargeable estate 1500000

IHT liability @40% 600000

QUESTION- 6

1) Sale of shares in Halliday Limited

Assessee- Gordon

Shares acquired on 1st January, 2018 in Halliday Limited

15000 shares * 1 per unit of share= £15000

On 1st March, 2019 became a full time worker in Halliday Limited at an annual salary of

£100000 per year

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

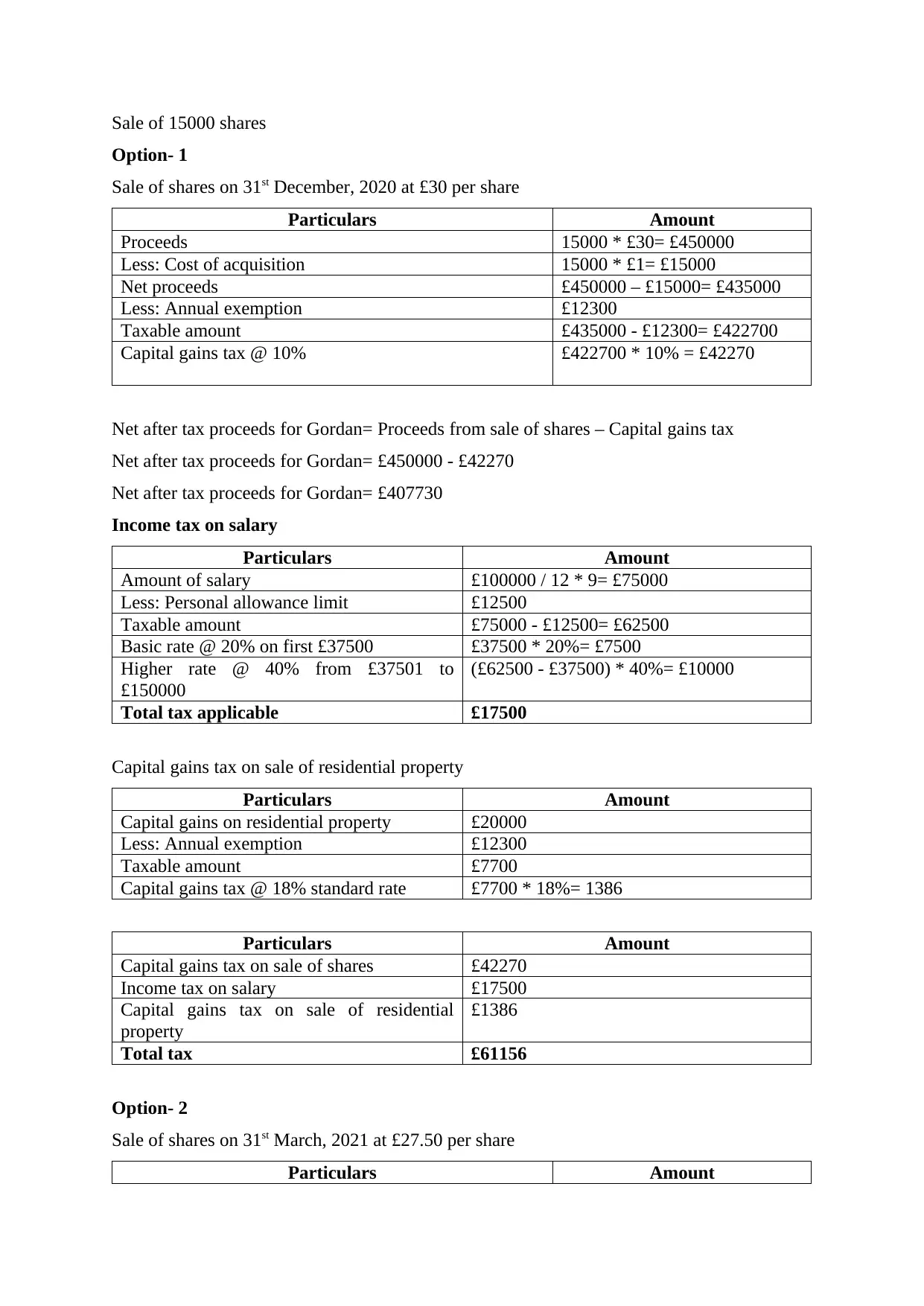

Sale of 15000 shares

Option- 1

Sale of shares on 31st December, 2020 at £30 per share

Particulars Amount

Proceeds 15000 * £30= £450000

Less: Cost of acquisition 15000 * £1= £15000

Net proceeds £450000 – £15000= £435000

Less: Annual exemption £12300

Taxable amount £435000 - £12300= £422700

Capital gains tax @ 10% £422700 * 10% = £42270

Net after tax proceeds for Gordan= Proceeds from sale of shares – Capital gains tax

Net after tax proceeds for Gordan= £450000 - £42270

Net after tax proceeds for Gordan= £407730

Income tax on salary

Particulars Amount

Amount of salary £100000 / 12 * 9= £75000

Less: Personal allowance limit £12500

Taxable amount £75000 - £12500= £62500

Basic rate @ 20% on first £37500 £37500 * 20%= £7500

Higher rate @ 40% from £37501 to

£150000

(£62500 - £37500) * 40%= £10000

Total tax applicable £17500

Capital gains tax on sale of residential property

Particulars Amount

Capital gains on residential property £20000

Less: Annual exemption £12300

Taxable amount £7700

Capital gains tax @ 18% standard rate £7700 * 18%= 1386

Particulars Amount

Capital gains tax on sale of shares £42270

Income tax on salary £17500

Capital gains tax on sale of residential

property

£1386

Total tax £61156

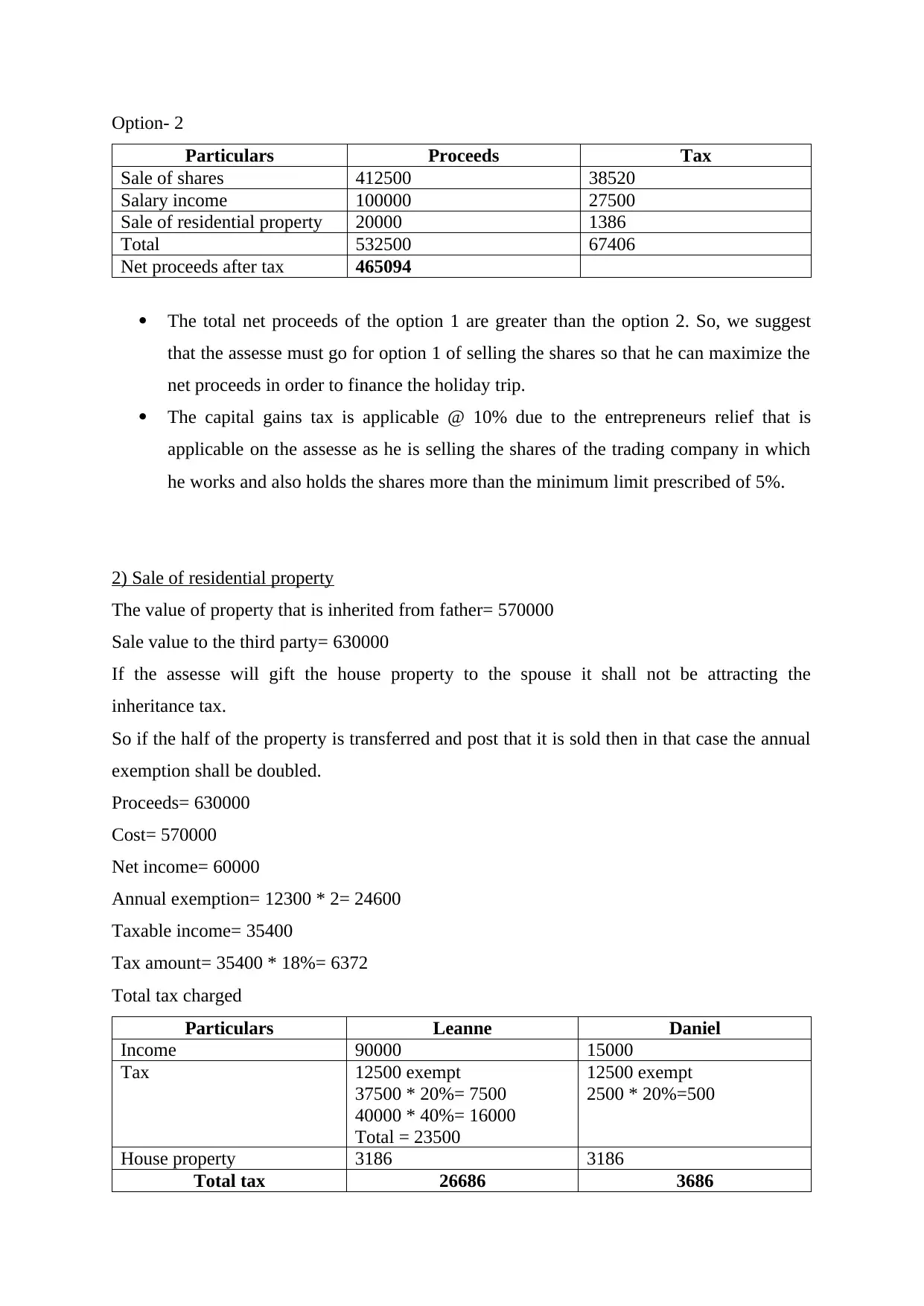

Option- 2

Sale of shares on 31st March, 2021 at £27.50 per share

Particulars Amount

Option- 1

Sale of shares on 31st December, 2020 at £30 per share

Particulars Amount

Proceeds 15000 * £30= £450000

Less: Cost of acquisition 15000 * £1= £15000

Net proceeds £450000 – £15000= £435000

Less: Annual exemption £12300

Taxable amount £435000 - £12300= £422700

Capital gains tax @ 10% £422700 * 10% = £42270

Net after tax proceeds for Gordan= Proceeds from sale of shares – Capital gains tax

Net after tax proceeds for Gordan= £450000 - £42270

Net after tax proceeds for Gordan= £407730

Income tax on salary

Particulars Amount

Amount of salary £100000 / 12 * 9= £75000

Less: Personal allowance limit £12500

Taxable amount £75000 - £12500= £62500

Basic rate @ 20% on first £37500 £37500 * 20%= £7500

Higher rate @ 40% from £37501 to

£150000

(£62500 - £37500) * 40%= £10000

Total tax applicable £17500

Capital gains tax on sale of residential property

Particulars Amount

Capital gains on residential property £20000

Less: Annual exemption £12300

Taxable amount £7700

Capital gains tax @ 18% standard rate £7700 * 18%= 1386

Particulars Amount

Capital gains tax on sale of shares £42270

Income tax on salary £17500

Capital gains tax on sale of residential

property

£1386

Total tax £61156

Option- 2

Sale of shares on 31st March, 2021 at £27.50 per share

Particulars Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

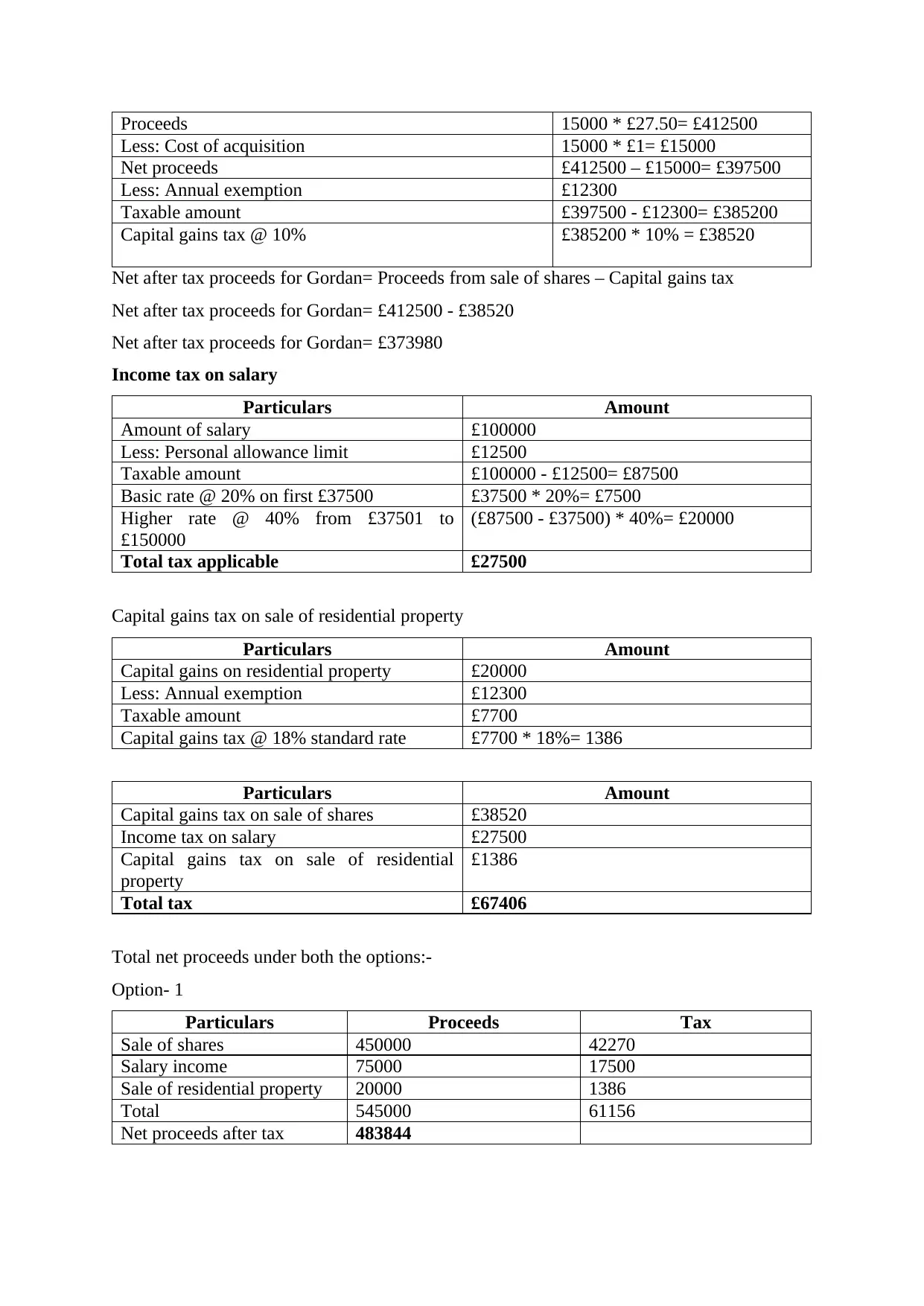

Proceeds 15000 * £27.50= £412500

Less: Cost of acquisition 15000 * £1= £15000

Net proceeds £412500 – £15000= £397500

Less: Annual exemption £12300

Taxable amount £397500 - £12300= £385200

Capital gains tax @ 10% £385200 * 10% = £38520

Net after tax proceeds for Gordan= Proceeds from sale of shares – Capital gains tax

Net after tax proceeds for Gordan= £412500 - £38520

Net after tax proceeds for Gordan= £373980

Income tax on salary

Particulars Amount

Amount of salary £100000

Less: Personal allowance limit £12500

Taxable amount £100000 - £12500= £87500

Basic rate @ 20% on first £37500 £37500 * 20%= £7500

Higher rate @ 40% from £37501 to

£150000

(£87500 - £37500) * 40%= £20000

Total tax applicable £27500

Capital gains tax on sale of residential property

Particulars Amount

Capital gains on residential property £20000

Less: Annual exemption £12300

Taxable amount £7700

Capital gains tax @ 18% standard rate £7700 * 18%= 1386

Particulars Amount

Capital gains tax on sale of shares £38520

Income tax on salary £27500

Capital gains tax on sale of residential

property

£1386

Total tax £67406

Total net proceeds under both the options:-

Option- 1

Particulars Proceeds Tax

Sale of shares 450000 42270

Salary income 75000 17500

Sale of residential property 20000 1386

Total 545000 61156

Net proceeds after tax 483844

Less: Cost of acquisition 15000 * £1= £15000

Net proceeds £412500 – £15000= £397500

Less: Annual exemption £12300

Taxable amount £397500 - £12300= £385200

Capital gains tax @ 10% £385200 * 10% = £38520

Net after tax proceeds for Gordan= Proceeds from sale of shares – Capital gains tax

Net after tax proceeds for Gordan= £412500 - £38520

Net after tax proceeds for Gordan= £373980

Income tax on salary

Particulars Amount

Amount of salary £100000

Less: Personal allowance limit £12500

Taxable amount £100000 - £12500= £87500

Basic rate @ 20% on first £37500 £37500 * 20%= £7500

Higher rate @ 40% from £37501 to

£150000

(£87500 - £37500) * 40%= £20000

Total tax applicable £27500

Capital gains tax on sale of residential property

Particulars Amount

Capital gains on residential property £20000

Less: Annual exemption £12300

Taxable amount £7700

Capital gains tax @ 18% standard rate £7700 * 18%= 1386

Particulars Amount

Capital gains tax on sale of shares £38520

Income tax on salary £27500

Capital gains tax on sale of residential

property

£1386

Total tax £67406

Total net proceeds under both the options:-

Option- 1

Particulars Proceeds Tax

Sale of shares 450000 42270

Salary income 75000 17500

Sale of residential property 20000 1386

Total 545000 61156

Net proceeds after tax 483844

Option- 2

Particulars Proceeds Tax

Sale of shares 412500 38520

Salary income 100000 27500

Sale of residential property 20000 1386

Total 532500 67406

Net proceeds after tax 465094

The total net proceeds of the option 1 are greater than the option 2. So, we suggest

that the assesse must go for option 1 of selling the shares so that he can maximize the

net proceeds in order to finance the holiday trip.

The capital gains tax is applicable @ 10% due to the entrepreneurs relief that is

applicable on the assesse as he is selling the shares of the trading company in which

he works and also holds the shares more than the minimum limit prescribed of 5%.

2) Sale of residential property

The value of property that is inherited from father= 570000

Sale value to the third party= 630000

If the assesse will gift the house property to the spouse it shall not be attracting the

inheritance tax.

So if the half of the property is transferred and post that it is sold then in that case the annual

exemption shall be doubled.

Proceeds= 630000

Cost= 570000

Net income= 60000

Annual exemption= 12300 * 2= 24600

Taxable income= 35400

Tax amount= 35400 * 18%= 6372

Total tax charged

Particulars Leanne Daniel

Income 90000 15000

Tax 12500 exempt

37500 * 20%= 7500

40000 * 40%= 16000

Total = 23500

12500 exempt

2500 * 20%=500

House property 3186 3186

Total tax 26686 3686

Particulars Proceeds Tax

Sale of shares 412500 38520

Salary income 100000 27500

Sale of residential property 20000 1386

Total 532500 67406

Net proceeds after tax 465094

The total net proceeds of the option 1 are greater than the option 2. So, we suggest

that the assesse must go for option 1 of selling the shares so that he can maximize the

net proceeds in order to finance the holiday trip.

The capital gains tax is applicable @ 10% due to the entrepreneurs relief that is

applicable on the assesse as he is selling the shares of the trading company in which

he works and also holds the shares more than the minimum limit prescribed of 5%.

2) Sale of residential property

The value of property that is inherited from father= 570000

Sale value to the third party= 630000

If the assesse will gift the house property to the spouse it shall not be attracting the

inheritance tax.

So if the half of the property is transferred and post that it is sold then in that case the annual

exemption shall be doubled.

Proceeds= 630000

Cost= 570000

Net income= 60000

Annual exemption= 12300 * 2= 24600

Taxable income= 35400

Tax amount= 35400 * 18%= 6372

Total tax charged

Particulars Leanne Daniel

Income 90000 15000

Tax 12500 exempt

37500 * 20%= 7500

40000 * 40%= 16000

Total = 23500

12500 exempt

2500 * 20%=500

House property 3186 3186

Total tax 26686 3686

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

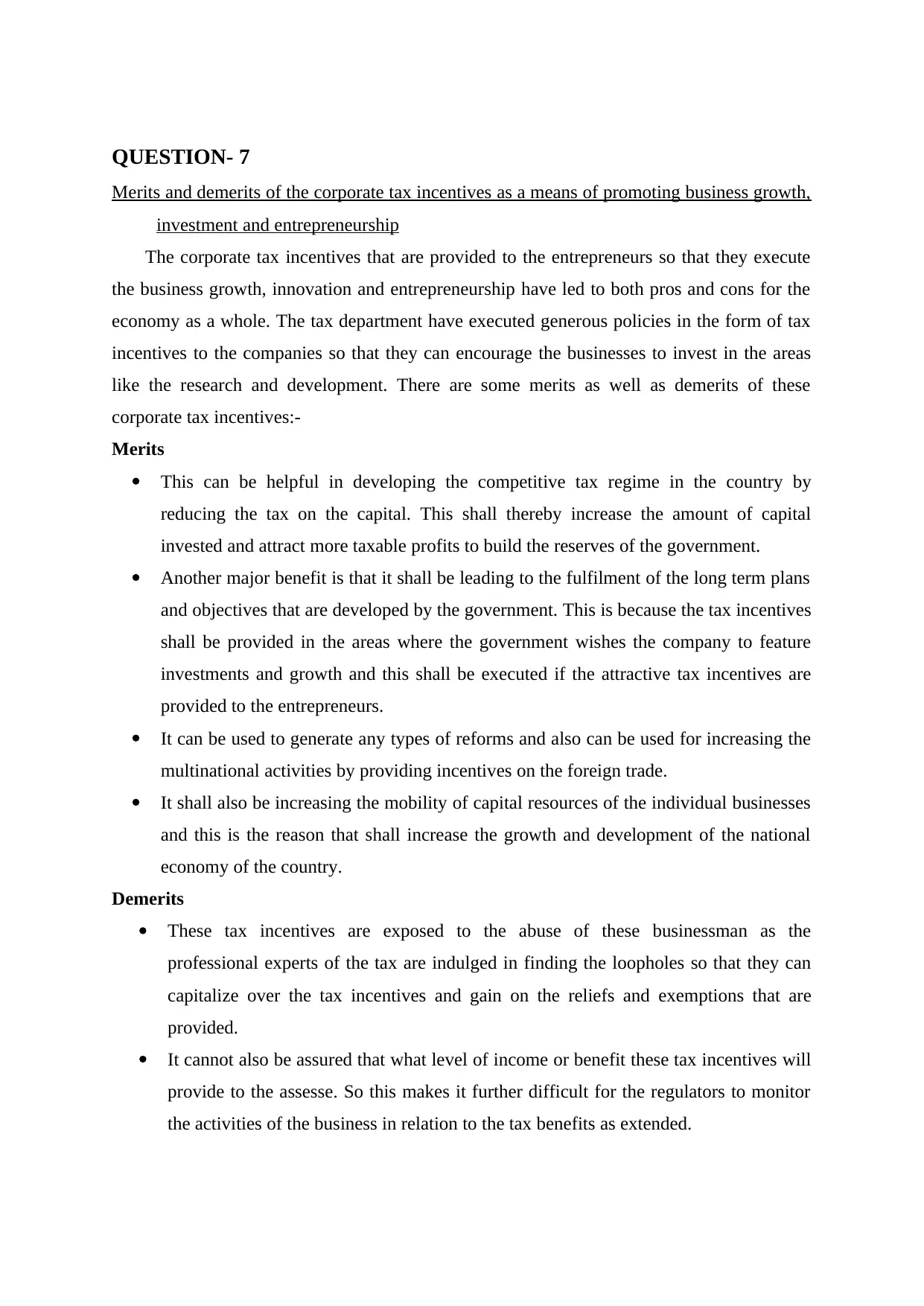

QUESTION- 7

Merits and demerits of the corporate tax incentives as a means of promoting business growth,

investment and entrepreneurship

The corporate tax incentives that are provided to the entrepreneurs so that they execute

the business growth, innovation and entrepreneurship have led to both pros and cons for the

economy as a whole. The tax department have executed generous policies in the form of tax

incentives to the companies so that they can encourage the businesses to invest in the areas

like the research and development. There are some merits as well as demerits of these

corporate tax incentives:-

Merits

This can be helpful in developing the competitive tax regime in the country by

reducing the tax on the capital. This shall thereby increase the amount of capital

invested and attract more taxable profits to build the reserves of the government.

Another major benefit is that it shall be leading to the fulfilment of the long term plans

and objectives that are developed by the government. This is because the tax incentives

shall be provided in the areas where the government wishes the company to feature

investments and growth and this shall be executed if the attractive tax incentives are

provided to the entrepreneurs.

It can be used to generate any types of reforms and also can be used for increasing the

multinational activities by providing incentives on the foreign trade.

It shall also be increasing the mobility of capital resources of the individual businesses

and this is the reason that shall increase the growth and development of the national

economy of the country.

Demerits

These tax incentives are exposed to the abuse of these businessman as the

professional experts of the tax are indulged in finding the loopholes so that they can

capitalize over the tax incentives and gain on the reliefs and exemptions that are

provided.

It cannot also be assured that what level of income or benefit these tax incentives will

provide to the assesse. So this makes it further difficult for the regulators to monitor

the activities of the business in relation to the tax benefits as extended.

Merits and demerits of the corporate tax incentives as a means of promoting business growth,

investment and entrepreneurship

The corporate tax incentives that are provided to the entrepreneurs so that they execute

the business growth, innovation and entrepreneurship have led to both pros and cons for the

economy as a whole. The tax department have executed generous policies in the form of tax

incentives to the companies so that they can encourage the businesses to invest in the areas

like the research and development. There are some merits as well as demerits of these

corporate tax incentives:-

Merits

This can be helpful in developing the competitive tax regime in the country by

reducing the tax on the capital. This shall thereby increase the amount of capital

invested and attract more taxable profits to build the reserves of the government.

Another major benefit is that it shall be leading to the fulfilment of the long term plans

and objectives that are developed by the government. This is because the tax incentives

shall be provided in the areas where the government wishes the company to feature

investments and growth and this shall be executed if the attractive tax incentives are

provided to the entrepreneurs.

It can be used to generate any types of reforms and also can be used for increasing the

multinational activities by providing incentives on the foreign trade.

It shall also be increasing the mobility of capital resources of the individual businesses

and this is the reason that shall increase the growth and development of the national

economy of the country.

Demerits

These tax incentives are exposed to the abuse of these businessman as the

professional experts of the tax are indulged in finding the loopholes so that they can

capitalize over the tax incentives and gain on the reliefs and exemptions that are

provided.

It cannot also be assured that what level of income or benefit these tax incentives will

provide to the assesse. So this makes it further difficult for the regulators to monitor

the activities of the business in relation to the tax benefits as extended.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Another major disadvantage is that the businesses are not sure about the earnings they

shall be getting on the investments made in the new projects, so these incentives

might not encourage them to make the necessary decisions for the welfare of the

economy.

shall be getting on the investments made in the new projects, so these incentives

might not encourage them to make the necessary decisions for the welfare of the

economy.

REFERENCES

Books and Journals

Online

15 Ethical Principles in Business. 2021. [Online]. Available Through:<

https://www.indeed.com/career-advice/career-development/ethical-principles-in-business>.

Books and Journals

Online

15 Ethical Principles in Business. 2021. [Online]. Available Through:<

https://www.indeed.com/career-advice/career-development/ethical-principles-in-business>.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.