Taxation for Business Assignment Solution - 2020/21, ARU London

VerifiedAdded on 2022/12/30

|8

|1075

|80

Homework Assignment

AI Summary

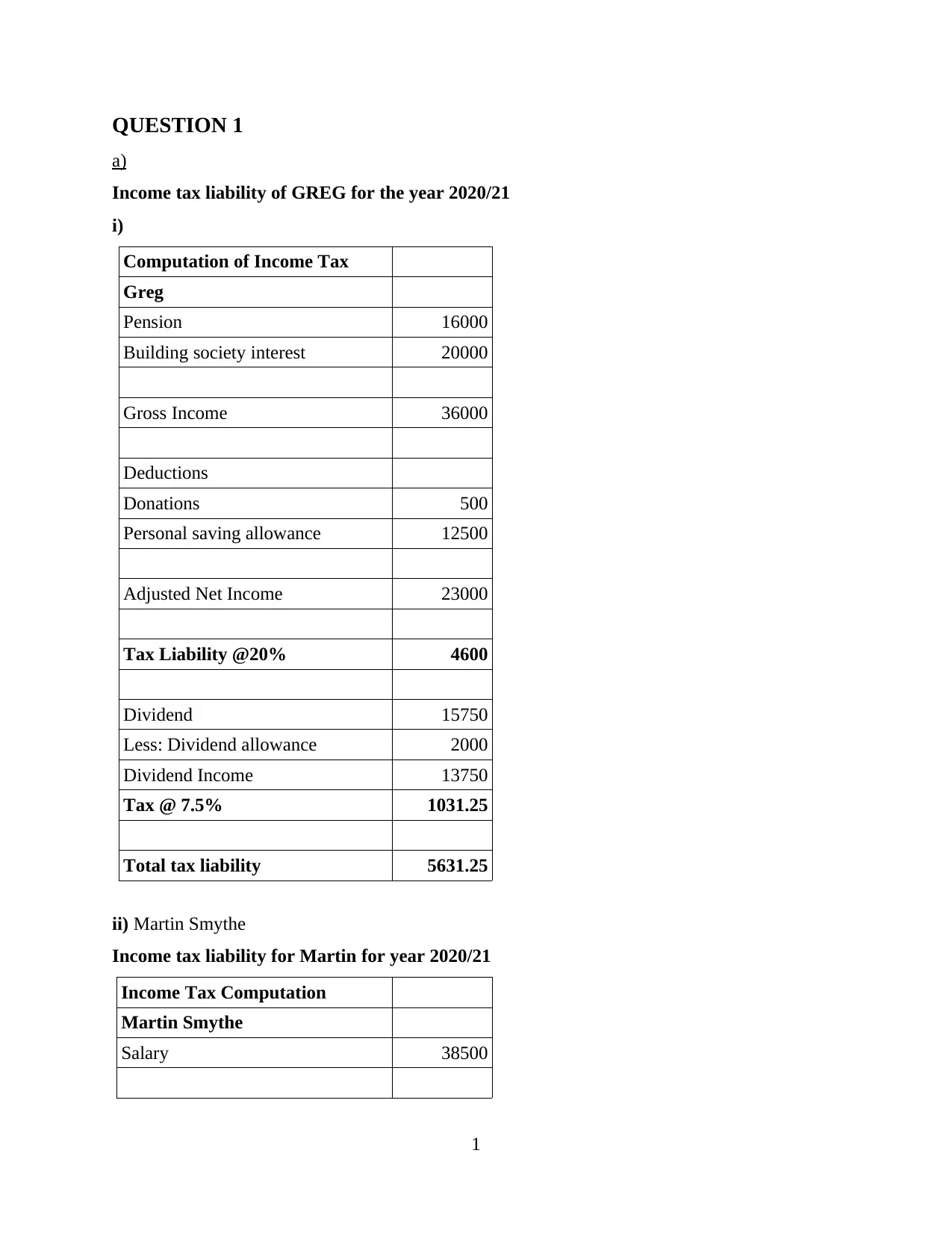

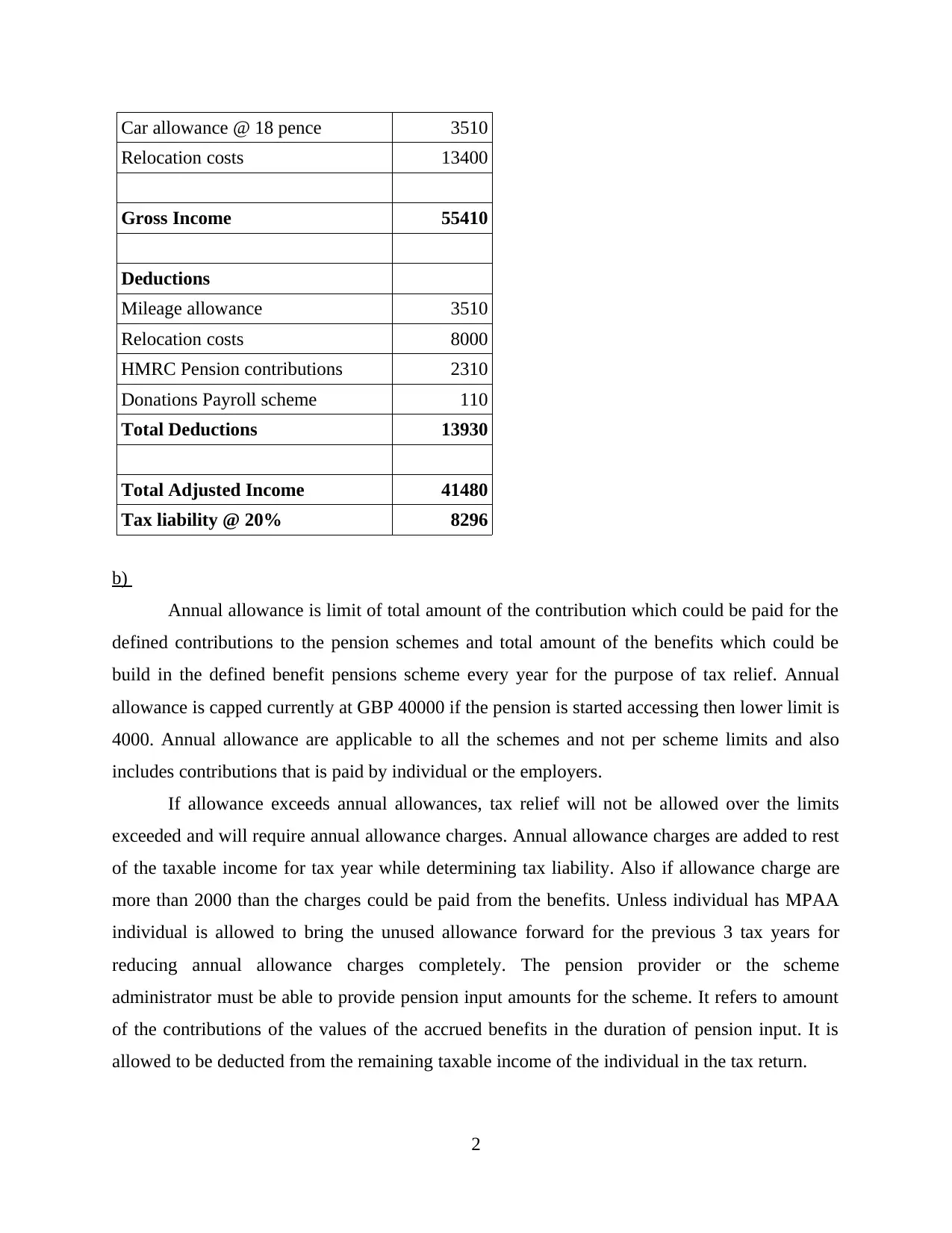

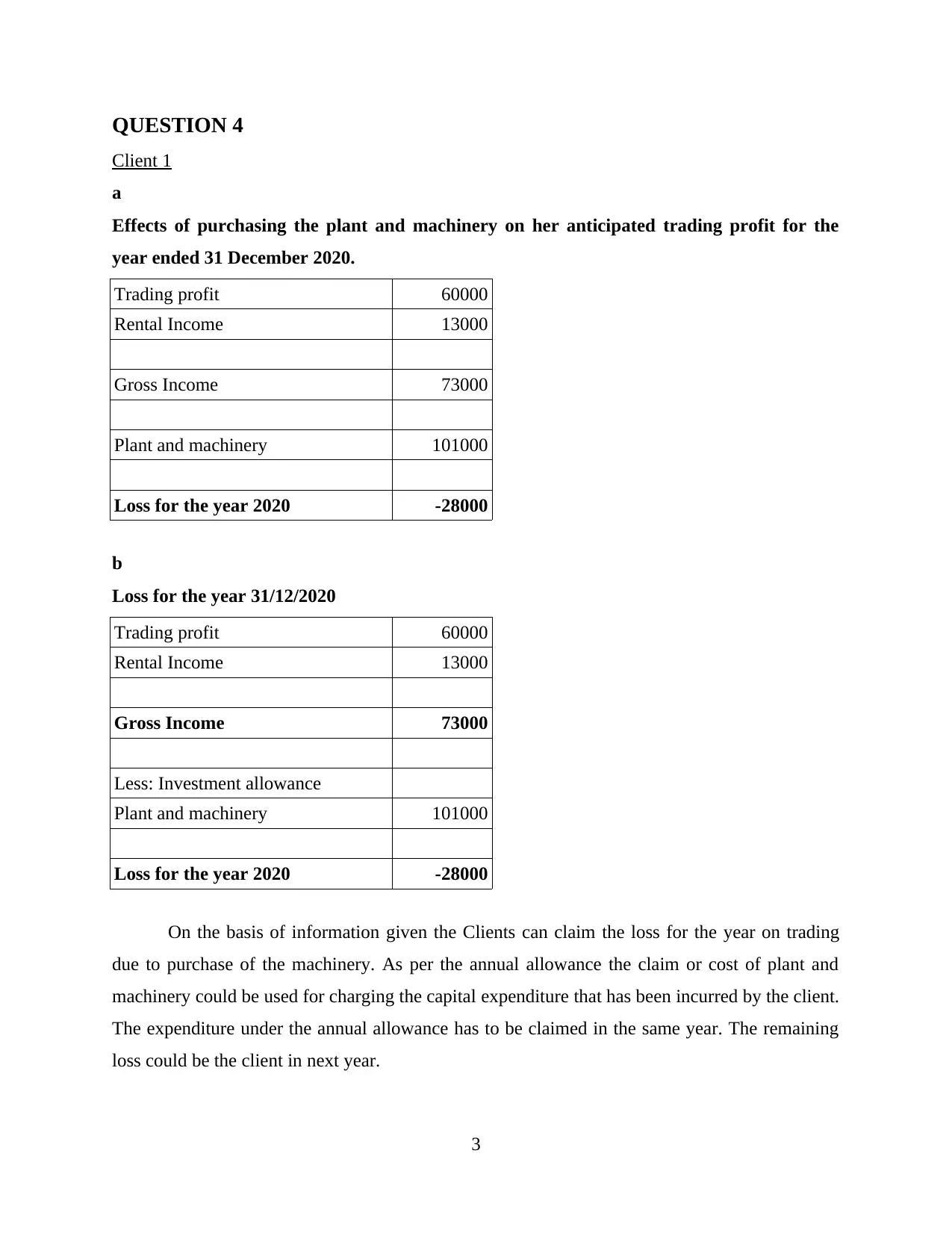

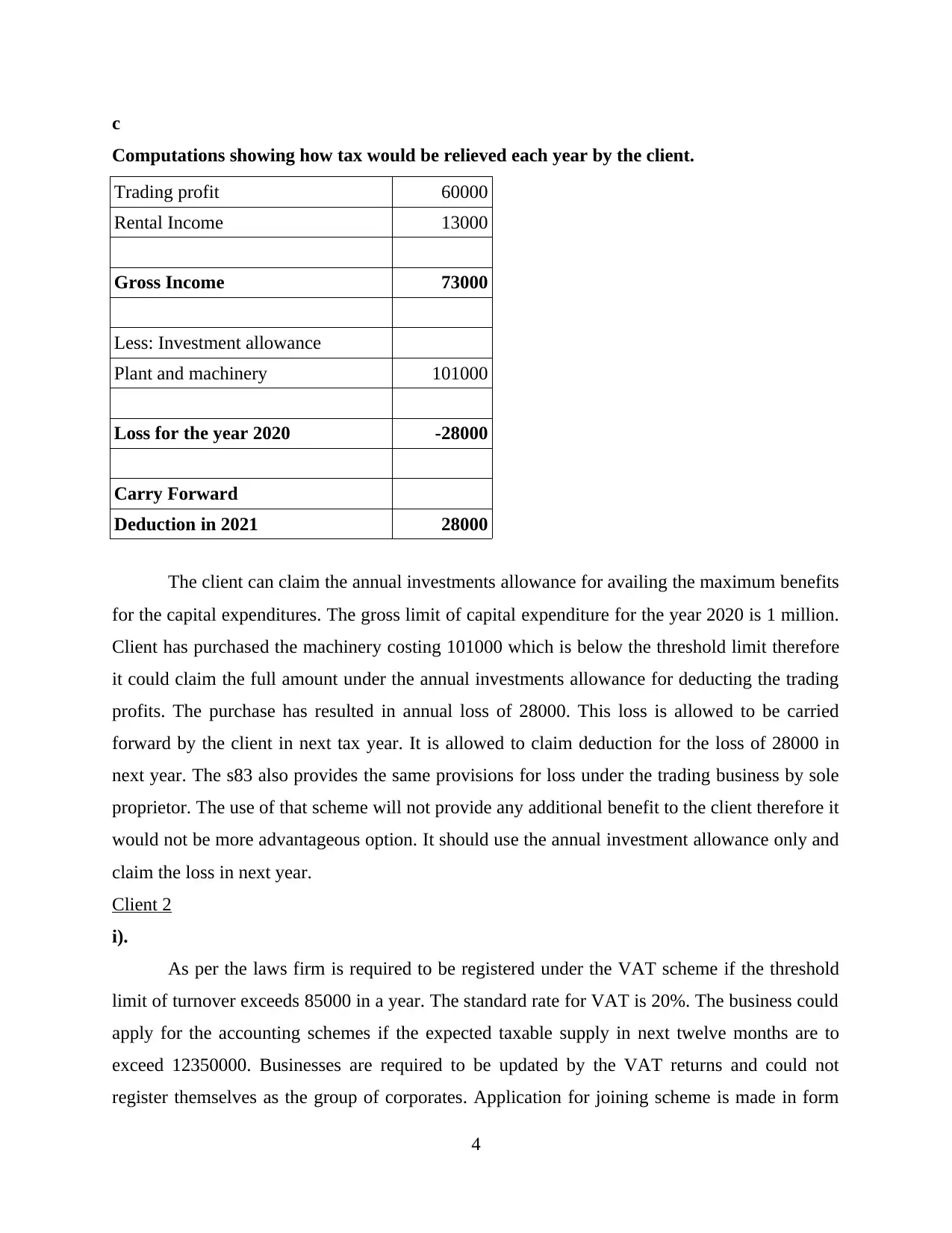

This document presents a comprehensive solution to a Taxation for Business assignment, addressing various aspects of taxation. It includes detailed calculations of income tax liability for individuals, such as Greg and Martin Smythe, considering factors like pension contributions, building society interest, salary, car allowance, and relocation costs. The solution also explains the concept of annual allowance for pension schemes and its implications for tax relief, along with the annual investment allowance for plant and machinery purchases, demonstrating how losses can be carried forward. Furthermore, it covers VAT schemes, including registration thresholds, accounting schemes, and their advantages and disadvantages, providing insights into VAT returns and payment options for businesses. The assignment provides a detailed analysis of the provided scenarios, offering a complete understanding of taxation principles and their practical application.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.