Taxation Assignment: Capital Gains, Fringe Benefits, and Tax Planning

VerifiedAdded on 2020/02/18

|10

|2537

|46

Homework Assignment

AI Summary

This assignment solution addresses several taxation scenarios. It begins with a computation of net capital gains or losses, classifying assets and applying relevant tax rules. The second part examines loan fringe benefits, calculating taxable values based on statutory and actual interest rates, considering deductible interest expenses. The third section explores the allocation of losses and gains in a property rental scenario between Jack and Jill. The fourth part discusses the principle of tax avoidance and the legal right to minimize tax liabilities. Finally, the assignment concludes by analyzing the tax implications of revenue and capital receipts from timber sales and the sale of an asset, differentiating between recurring and lump-sum payments.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Answer to 1

Computation of net capital gain or loss for the year:

Since the past one year, Eric had taken various attempts to procure some assets and based on the

question, it can be assumed that he has held these assets for less than one year. As per Kenny et.

al (2017) taxability of capital gain arises when the selling price of an asset exceeds its cost base.

The indexation benefit will not accrue to Eric, as the assets are not held for more than a year.

The classification of the assets procured by Eric must be done based on their respective heads:

a. Assets intended for personal use

A person for their own enjoyment or use buys these assets but it does not include collectibles.

Besides, when these assets are sold to another person, taxability of capital gain does not incur

when the procurement cost of such assets is less than or equal to $10000. Based on the question,

the following personal assets have been acquired by Eric (Kenny et. al, 2017). The first asset is a

home sound system with an acquisition cost of $12000 and the second asset is the shares of a

listed company with an acquisition cost of $5000.

b. Collectibles

A person purchases these assets for enjoyment or personal efficacies and taxability of capital

gain does not accrue if the procurement cost is less than or equal to $500. Further, based on the

given information, the following collectibles have been acquired by Eric. The first asset is

painting with an acquisition cost of $9000, the second asset is an antique chair with an

acquisition cost of $3000, and the last asset is an antique vase with an acquisition cost of $2000

respectively (Renton, 2005).

Considering the above scenario, the following formula can be utilized for the computation of

capital gain for assets held for less than a year.

Capital Proceeds of the above assets

(Amounts in dollars)

Particulars Cost Base of Assets Capital Proceeds of Net Capital Gain/

2

Answer to 1

Computation of net capital gain or loss for the year:

Since the past one year, Eric had taken various attempts to procure some assets and based on the

question, it can be assumed that he has held these assets for less than one year. As per Kenny et.

al (2017) taxability of capital gain arises when the selling price of an asset exceeds its cost base.

The indexation benefit will not accrue to Eric, as the assets are not held for more than a year.

The classification of the assets procured by Eric must be done based on their respective heads:

a. Assets intended for personal use

A person for their own enjoyment or use buys these assets but it does not include collectibles.

Besides, when these assets are sold to another person, taxability of capital gain does not incur

when the procurement cost of such assets is less than or equal to $10000. Based on the question,

the following personal assets have been acquired by Eric (Kenny et. al, 2017). The first asset is a

home sound system with an acquisition cost of $12000 and the second asset is the shares of a

listed company with an acquisition cost of $5000.

b. Collectibles

A person purchases these assets for enjoyment or personal efficacies and taxability of capital

gain does not accrue if the procurement cost is less than or equal to $500. Further, based on the

given information, the following collectibles have been acquired by Eric. The first asset is

painting with an acquisition cost of $9000, the second asset is an antique chair with an

acquisition cost of $3000, and the last asset is an antique vase with an acquisition cost of $2000

respectively (Renton, 2005).

Considering the above scenario, the following formula can be utilized for the computation of

capital gain for assets held for less than a year.

Capital Proceeds of the above assets

(Amounts in dollars)

Particulars Cost Base of Assets Capital Proceeds of Net Capital Gain/

2

Taxation

Assets (Net Capital Loss)

Home Sound System 12,000 11000 (1000) Loss

Shares in listed

company

5,000 20000 15000 Gain

Painting 9,000 1000 (8000) Loss

Antique Chair 3,000 1000 (2000) Loss

Antique Vase 2,000 3000 1000 Gain

Net Capital Gain/Loss 5000 Gain

Important notes:

a. All assets intended for personal use are acquired for more than $10000 and therefore,

taxability of capital gain is applicable.

b. All collectibles are acquired for more than $500 and therefore, taxability of capital gain is

applicable.

c. Capital losses for the entire year have been set-off with capital gain to ascertain the net

gain or loss.

3

Assets (Net Capital Loss)

Home Sound System 12,000 11000 (1000) Loss

Shares in listed

company

5,000 20000 15000 Gain

Painting 9,000 1000 (8000) Loss

Antique Chair 3,000 1000 (2000) Loss

Antique Vase 2,000 3000 1000 Gain

Net Capital Gain/Loss 5000 Gain

Important notes:

a. All assets intended for personal use are acquired for more than $10000 and therefore,

taxability of capital gain is applicable.

b. All collectibles are acquired for more than $500 and therefore, taxability of capital gain is

applicable.

c. Capital losses for the entire year have been set-off with capital gain to ascertain the net

gain or loss.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

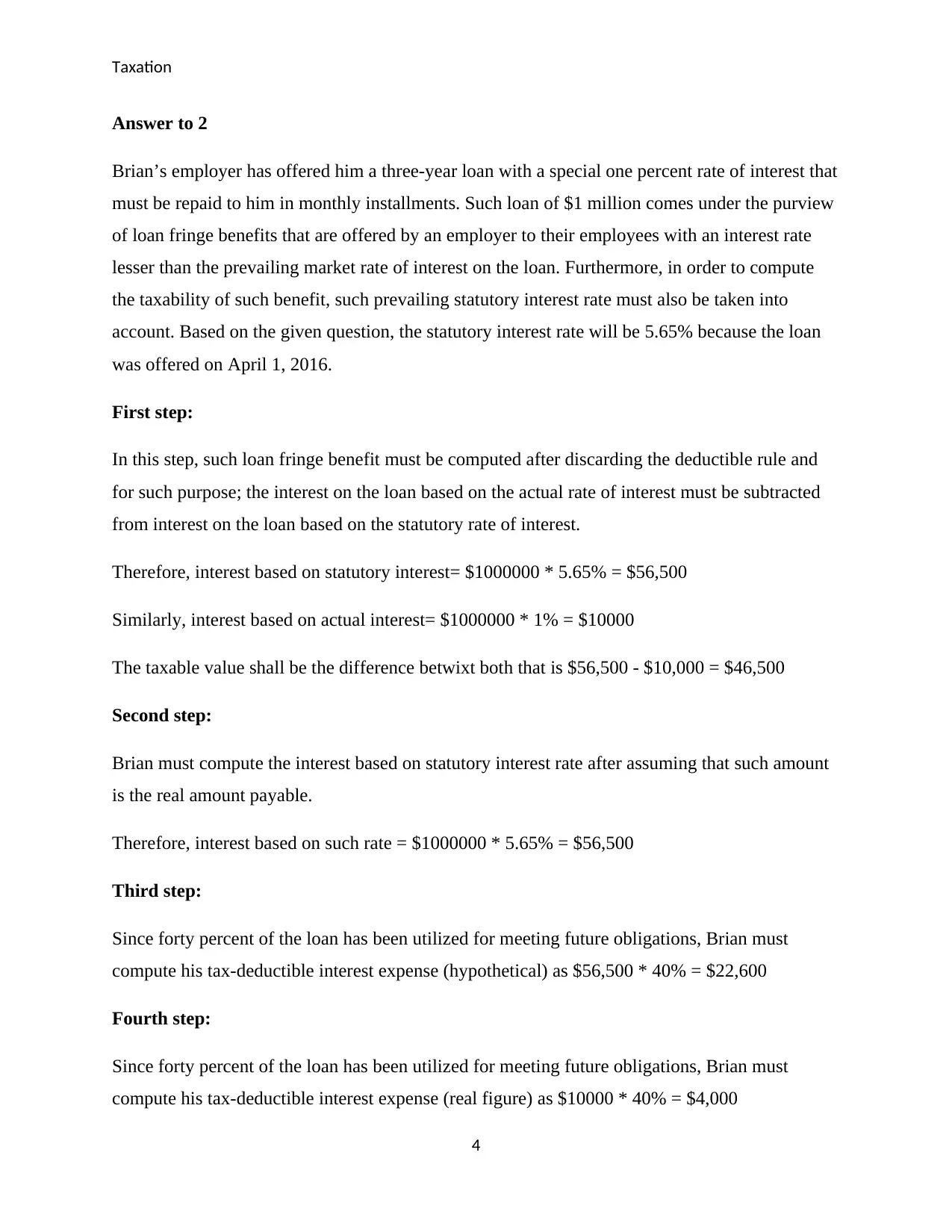

Answer to 2

Brian’s employer has offered him a three-year loan with a special one percent rate of interest that

must be repaid to him in monthly installments. Such loan of $1 million comes under the purview

of loan fringe benefits that are offered by an employer to their employees with an interest rate

lesser than the prevailing market rate of interest on the loan. Furthermore, in order to compute

the taxability of such benefit, such prevailing statutory interest rate must also be taken into

account. Based on the given question, the statutory interest rate will be 5.65% because the loan

was offered on April 1, 2016.

First step:

In this step, such loan fringe benefit must be computed after discarding the deductible rule and

for such purpose; the interest on the loan based on the actual rate of interest must be subtracted

from interest on the loan based on the statutory rate of interest.

Therefore, interest based on statutory interest= $1000000 * 5.65% = $56,500

Similarly, interest based on actual interest= $1000000 * 1% = $10000

The taxable value shall be the difference betwixt both that is $56,500 - $10,000 = $46,500

Second step:

Brian must compute the interest based on statutory interest rate after assuming that such amount

is the real amount payable.

Therefore, interest based on such rate = $1000000 * 5.65% = $56,500

Third step:

Since forty percent of the loan has been utilized for meeting future obligations, Brian must

compute his tax-deductible interest expense (hypothetical) as $56,500 * 40% = $22,600

Fourth step:

Since forty percent of the loan has been utilized for meeting future obligations, Brian must

compute his tax-deductible interest expense (real figure) as $10000 * 40% = $4,000

4

Answer to 2

Brian’s employer has offered him a three-year loan with a special one percent rate of interest that

must be repaid to him in monthly installments. Such loan of $1 million comes under the purview

of loan fringe benefits that are offered by an employer to their employees with an interest rate

lesser than the prevailing market rate of interest on the loan. Furthermore, in order to compute

the taxability of such benefit, such prevailing statutory interest rate must also be taken into

account. Based on the given question, the statutory interest rate will be 5.65% because the loan

was offered on April 1, 2016.

First step:

In this step, such loan fringe benefit must be computed after discarding the deductible rule and

for such purpose; the interest on the loan based on the actual rate of interest must be subtracted

from interest on the loan based on the statutory rate of interest.

Therefore, interest based on statutory interest= $1000000 * 5.65% = $56,500

Similarly, interest based on actual interest= $1000000 * 1% = $10000

The taxable value shall be the difference betwixt both that is $56,500 - $10,000 = $46,500

Second step:

Brian must compute the interest based on statutory interest rate after assuming that such amount

is the real amount payable.

Therefore, interest based on such rate = $1000000 * 5.65% = $56,500

Third step:

Since forty percent of the loan has been utilized for meeting future obligations, Brian must

compute his tax-deductible interest expense (hypothetical) as $56,500 * 40% = $22,600

Fourth step:

Since forty percent of the loan has been utilized for meeting future obligations, Brian must

compute his tax-deductible interest expense (real figure) as $10000 * 40% = $4,000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

Fifth step:

After all the above steps, the actual amount must be subtracted from the hypothetical figure to

arrive at a conclusion.

Hence, $22,600 - $4,000 = $18,600

Sixth step:

The final amount must be computed by subtracting the amount determined in the fifth step from

that of the amount in the first step.

Therefore, $46,500 - $18,600 = $27,900

Nevertheless, if such interest had been payable at the termination of the loan instead of usual

monthly repayments, then the deemed period of such loan would be assumed from the time when

such interest will become payable or is paid respectively (Sadiq et. al,, 2014). Besides, if there is

no obligation on the part of Brian to repay the interests, then the computation must be done in the

same way but by considering the actual interest rate to be zero.

5

Fifth step:

After all the above steps, the actual amount must be subtracted from the hypothetical figure to

arrive at a conclusion.

Hence, $22,600 - $4,000 = $18,600

Sixth step:

The final amount must be computed by subtracting the amount determined in the fifth step from

that of the amount in the first step.

Therefore, $46,500 - $18,600 = $27,900

Nevertheless, if such interest had been payable at the termination of the loan instead of usual

monthly repayments, then the deemed period of such loan would be assumed from the time when

such interest will become payable or is paid respectively (Sadiq et. al,, 2014). Besides, if there is

no obligation on the part of Brian to repay the interests, then the computation must be done in the

same way but by considering the actual interest rate to be zero.

5

Taxation

Answer to 3

Both Jack and Jill agreed to borrow some money in order to rent a property wherein Jack also

agreed to only 10% of the profits in contrast to 90% of the same to his wife Jill. Besides, Jack

also agreed to bear the entire loss and Jill was freed of such burden. Therefore, the loss of $1000

that incurred in the last year must be borne by Jack himself and Jill has no other obligation in

respect of the same. Besides, such loss can be set off with other incomes of Jack so that he can

arrive at a net income or loss for the year. In addition, Jack also has a right to carry forward these

losses for subsequent years. In the event of a decision to sell the property, either gain or loss can

arrive for Jack and Jill.

If there is a loss, the entire amount must be borne by Jack and he has full right to carry forward

the same in subsequent years or utilize the same in the current year to ascertain his net income or

loss (Saunders, 2015). On the other hand, if there is a gain, the amount must be apportioned

betwixt Jack and Jill in the ratio of 10:90, and Jack has complete right to set off such loss of

$1000 that may arise from the gain after selling the property. On a whole, the conclusion is that

Jack is able to set off the losses of last year in the present year if there is some income arriving

from the sale of the property (Kobestky, 2005). Besides, if Jack does not have any gain in the

current year, such loss must be borne by him and Jill is free of such responsibility. Therefore, the

tax treatment cannot affect Jill in any circumstances whereas Jack is under an obligation to bear

such losses in his books.

6

Answer to 3

Both Jack and Jill agreed to borrow some money in order to rent a property wherein Jack also

agreed to only 10% of the profits in contrast to 90% of the same to his wife Jill. Besides, Jack

also agreed to bear the entire loss and Jill was freed of such burden. Therefore, the loss of $1000

that incurred in the last year must be borne by Jack himself and Jill has no other obligation in

respect of the same. Besides, such loss can be set off with other incomes of Jack so that he can

arrive at a net income or loss for the year. In addition, Jack also has a right to carry forward these

losses for subsequent years. In the event of a decision to sell the property, either gain or loss can

arrive for Jack and Jill.

If there is a loss, the entire amount must be borne by Jack and he has full right to carry forward

the same in subsequent years or utilize the same in the current year to ascertain his net income or

loss (Saunders, 2015). On the other hand, if there is a gain, the amount must be apportioned

betwixt Jack and Jill in the ratio of 10:90, and Jack has complete right to set off such loss of

$1000 that may arise from the gain after selling the property. On a whole, the conclusion is that

Jack is able to set off the losses of last year in the present year if there is some income arriving

from the sale of the property (Kobestky, 2005). Besides, if Jack does not have any gain in the

current year, such loss must be borne by him and Jill is free of such responsibility. Therefore, the

tax treatment cannot affect Jill in any circumstances whereas Jack is under an obligation to bear

such losses in his books.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

Answer to 4

It can be witnessed from the case of IRC v Duke of Westminster [1936] AC 1 that every

individual has full right to make use of legal means and strategies in a way that can assist them in

decreasing their total income at the end of the year. This means that if an individual succeeds in

doing so, the Commissioners of Inland Revenue are under no authority to question the same and

exert pressure upon the person to enhance his payable tax (Kenny, 2016). On a whole, such rule

can be allowed only when the individual utilizes fair means to decrease his total income at the

year-end, thereby decrease his total tax payable to the authority.

This clearly signifies that the case accommodates the following principles:

a. Every individual has complete right to make use of strategic measures in order to manage

their accounts in a way that can assist them in decreasing their total income (Kenny,

2016).

b. If no immoral or unethical procedures are adopted, then no further taxes shall be

implemented upon that individual.

c. Besides, if legal means are adopted for decreasing the total tax payable to the authority,

then no one can question the validity of the same and force the person to pay an increased

amount of tax.

The previously mentioned rule was valid somehow until the appearance of new case laws in the

current scenario. As a result, the ideology of observing accounts has become different from what

was before. The significance of the rule in the current situation can be stated in the following

manner (Latimer, 2012):

The given rule holds true even in the present environment because it prevents organizations to

influence their accounts in a way that can grant additional advantage to them. Besides, the rule

also offers a legal right to operate the business affairs in a genuine way. For example, if a

business enterprise is encountering immense losses in a year that restricts it to address its

obligations; such business can alter its balance sheet amounts and write off their fixed assets to

their respective carrying values (Greene, 2013). Further, if the businesses do not pursue properly

authenticated documents to justify the transaction, they can still do so. However, if unethical

means are adopted by the businesses to alter their accounts, then the rule prevents them from

7

Answer to 4

It can be witnessed from the case of IRC v Duke of Westminster [1936] AC 1 that every

individual has full right to make use of legal means and strategies in a way that can assist them in

decreasing their total income at the end of the year. This means that if an individual succeeds in

doing so, the Commissioners of Inland Revenue are under no authority to question the same and

exert pressure upon the person to enhance his payable tax (Kenny, 2016). On a whole, such rule

can be allowed only when the individual utilizes fair means to decrease his total income at the

year-end, thereby decrease his total tax payable to the authority.

This clearly signifies that the case accommodates the following principles:

a. Every individual has complete right to make use of strategic measures in order to manage

their accounts in a way that can assist them in decreasing their total income (Kenny,

2016).

b. If no immoral or unethical procedures are adopted, then no further taxes shall be

implemented upon that individual.

c. Besides, if legal means are adopted for decreasing the total tax payable to the authority,

then no one can question the validity of the same and force the person to pay an increased

amount of tax.

The previously mentioned rule was valid somehow until the appearance of new case laws in the

current scenario. As a result, the ideology of observing accounts has become different from what

was before. The significance of the rule in the current situation can be stated in the following

manner (Latimer, 2012):

The given rule holds true even in the present environment because it prevents organizations to

influence their accounts in a way that can grant additional advantage to them. Besides, the rule

also offers a legal right to operate the business affairs in a genuine way. For example, if a

business enterprise is encountering immense losses in a year that restricts it to address its

obligations; such business can alter its balance sheet amounts and write off their fixed assets to

their respective carrying values (Greene, 2013). Further, if the businesses do not pursue properly

authenticated documents to justify the transaction, they can still do so. However, if unethical

means are adopted by the businesses to alter their accounts, then the rule prevents them from

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

doing so. On a whole, any transaction that assists a business in operating effectively is valid in

the eyes of law and must not be questioned upon by any authority.

8

doing so. On a whole, any transaction that assists a business in operating effectively is valid in

the eyes of law and must not be questioned upon by any authority.

8

Taxation

Answer to 5

There are various big pine trees in a piece of land that is owned by Bill and he intends to use the

same for grazing sheep. However, for complying with such desire, the clearance of such trees is

vital. Therefore, he hires a logging company who shall offer him $1000 for every 100 meters of

timber. The main question behind such ideology is that whether the tax is applicable on Bill for

the amount obtained by the logging company. Besides, since the given question does not clarify

the fact what is the exact amount of receipts obtained after clearing such trees, it can be

considered a revenue receipt in the hands of Bill (Woellner et. al, 2017). This means that capital

gain tax does not accrue upon Bill in this regard.

If Bill attains a lump sum amount of $50000 for allowing the logging company to remove the

timber from his land, the same amount must be regarded as a capital receipt in the hands of Bill.

The reason behind this can be attributed to the fact that this payment is lump sum in nature and

there is no recurring receipt. Further, this transaction also occurs because of the offering of the

right to a party to remove the trees from the land. Therefore, on a whole, since it is a case of

lump sum receipt, the same must be considered a capital receipt and hence, taxable under capital

gain in the hands of Bill (Barcokzy, 2010).

In both the above scenarios, Bill is attaining the money. In the first given case, the receipt in the

hands of Bill is recurring and small in nature while in the second case, the receipt in the hands of

Bill is not recurring in nature and there is an offering of the right to the party to comply with the

requirement of clearing the trees. Moreover, the same receipt is a bigger one and is also a one-

time receipt because once the trees are terminated from the land; it will consume some amount of

time to grow once again. Therefore, as Bill in the second case is receiving enormous amount

after giving a right to the opposite party, this transaction can be considered as selling an asset to a

company for a lump sum consideration. Besides, in taxation law, when one party sells an asset to

another party for a consideration, the same shall be considered a capital receipt and taxable in his

hands (Fullerton et.al, 2017). In contrast to this, since the first case does not attract any capital

gain tax, it must be treated under normal tax rates and not capital gains.

9

Answer to 5

There are various big pine trees in a piece of land that is owned by Bill and he intends to use the

same for grazing sheep. However, for complying with such desire, the clearance of such trees is

vital. Therefore, he hires a logging company who shall offer him $1000 for every 100 meters of

timber. The main question behind such ideology is that whether the tax is applicable on Bill for

the amount obtained by the logging company. Besides, since the given question does not clarify

the fact what is the exact amount of receipts obtained after clearing such trees, it can be

considered a revenue receipt in the hands of Bill (Woellner et. al, 2017). This means that capital

gain tax does not accrue upon Bill in this regard.

If Bill attains a lump sum amount of $50000 for allowing the logging company to remove the

timber from his land, the same amount must be regarded as a capital receipt in the hands of Bill.

The reason behind this can be attributed to the fact that this payment is lump sum in nature and

there is no recurring receipt. Further, this transaction also occurs because of the offering of the

right to a party to remove the trees from the land. Therefore, on a whole, since it is a case of

lump sum receipt, the same must be considered a capital receipt and hence, taxable under capital

gain in the hands of Bill (Barcokzy, 2010).

In both the above scenarios, Bill is attaining the money. In the first given case, the receipt in the

hands of Bill is recurring and small in nature while in the second case, the receipt in the hands of

Bill is not recurring in nature and there is an offering of the right to the party to comply with the

requirement of clearing the trees. Moreover, the same receipt is a bigger one and is also a one-

time receipt because once the trees are terminated from the land; it will consume some amount of

time to grow once again. Therefore, as Bill in the second case is receiving enormous amount

after giving a right to the opposite party, this transaction can be considered as selling an asset to a

company for a lump sum consideration. Besides, in taxation law, when one party sells an asset to

another party for a consideration, the same shall be considered a capital receipt and taxable in his

hands (Fullerton et.al, 2017). In contrast to this, since the first case does not attract any capital

gain tax, it must be treated under normal tax rates and not capital gains.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Taxation

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Greene, B 2013, Course Notes: Tort Law, Oxon: Routledge.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Latimer, P 2012, Australian Business Law 2012, 31st ed. Sydney, NSW: CCH Australia Limited.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

10

References

Barcokzy, S 2010, Australian Tax Casebook, CCH Australia Ltd

Fullerton, I.G, Deutsch, R, Friezer, M.L, Hanley,P & Snape, T 2017, The Australian Tax

Handbook Tax Return Edition 2017, Thomson Reuters: Australia

Greene, B 2013, Course Notes: Tort Law, Oxon: Routledge.

Kenny, B. V 2016, Australian Tax 2016, Thomson Reuters (Professional) Australia Limited

Kenny, P, Blissenden, M, & Villios, S 2017, Australian Tax 2017, Thomson Reuters: Australia

Kobestky, M 2005, Income Tax: Text, Materials and Essential Cases, Sydney: The Federation

Press

Latimer, P 2012, Australian Business Law 2012, 31st ed. Sydney, NSW: CCH Australia Limited.

Renton N.E 2005, Income Tax and Investment, 2nd edition, Sydney

Sadiq, K, Coleman, C, Hanegbi, R., Jogarajan,S, Krever, R.,Obst, W.,& Ting, A 2014,

Principles of Taxation Law, Sydney.

Saunders, C 2015, The Australian Constitution, Carlton: Constitutional Centenary Foundation

Woellner, R, Barkoczy, S, Murphy, S, Evans, C & Pinto, D 2017, Australian taxation law 2017,

Oxford University Press Australia

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.