HI6028 Taxation Theory, Practice & Law Assignment: Taxation Analysis

VerifiedAdded on 2023/06/04

|23

|3602

|207

Homework Assignment

AI Summary

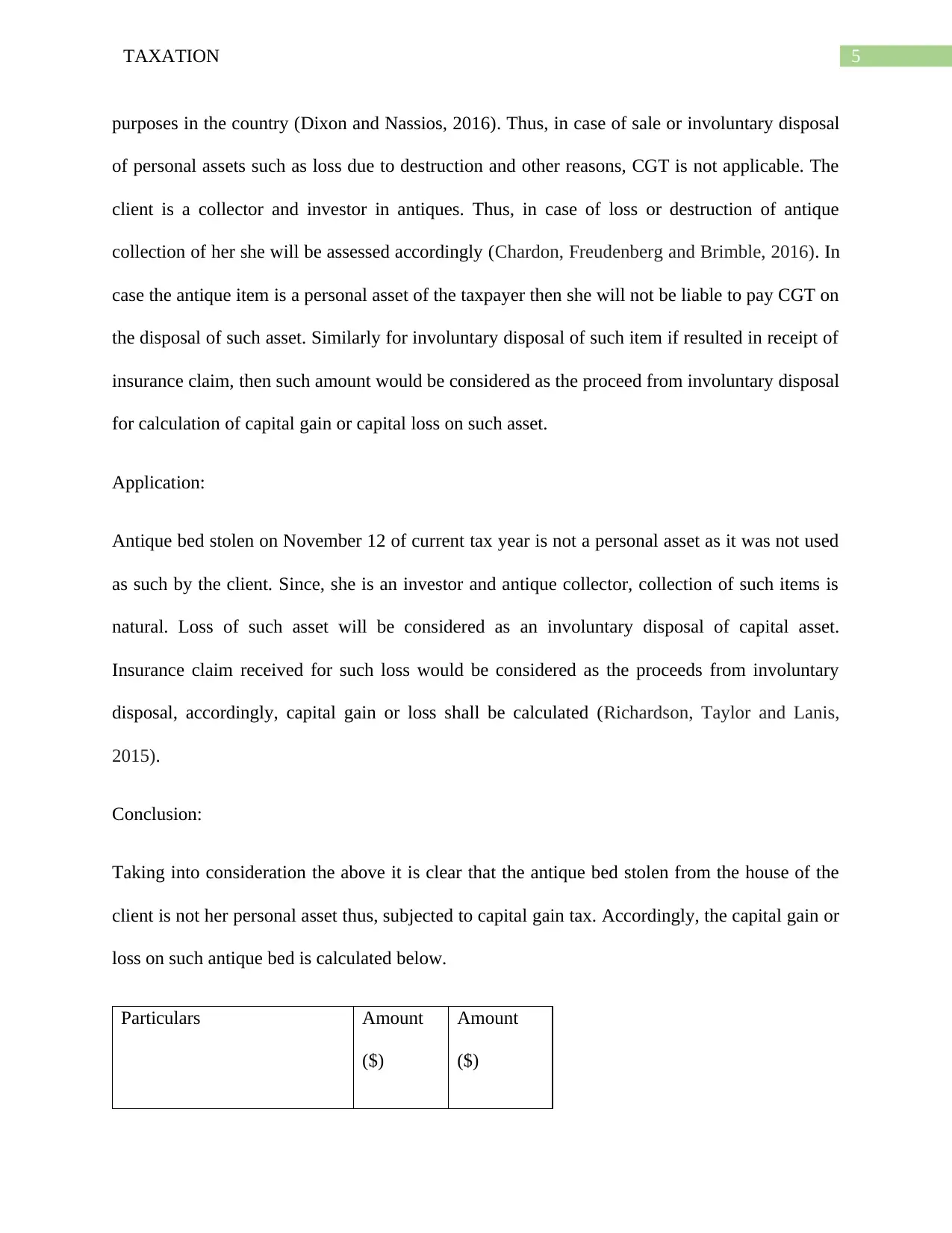

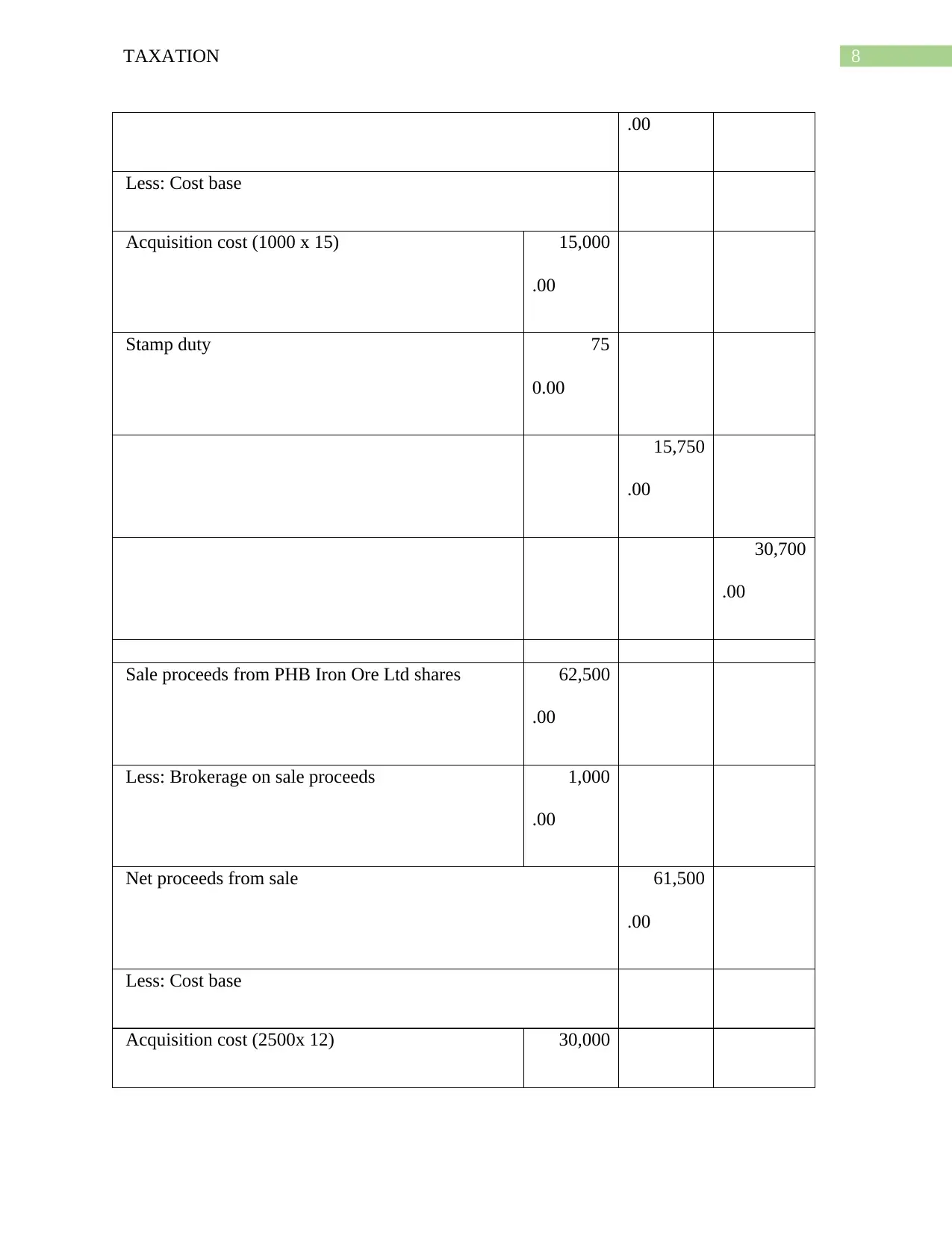

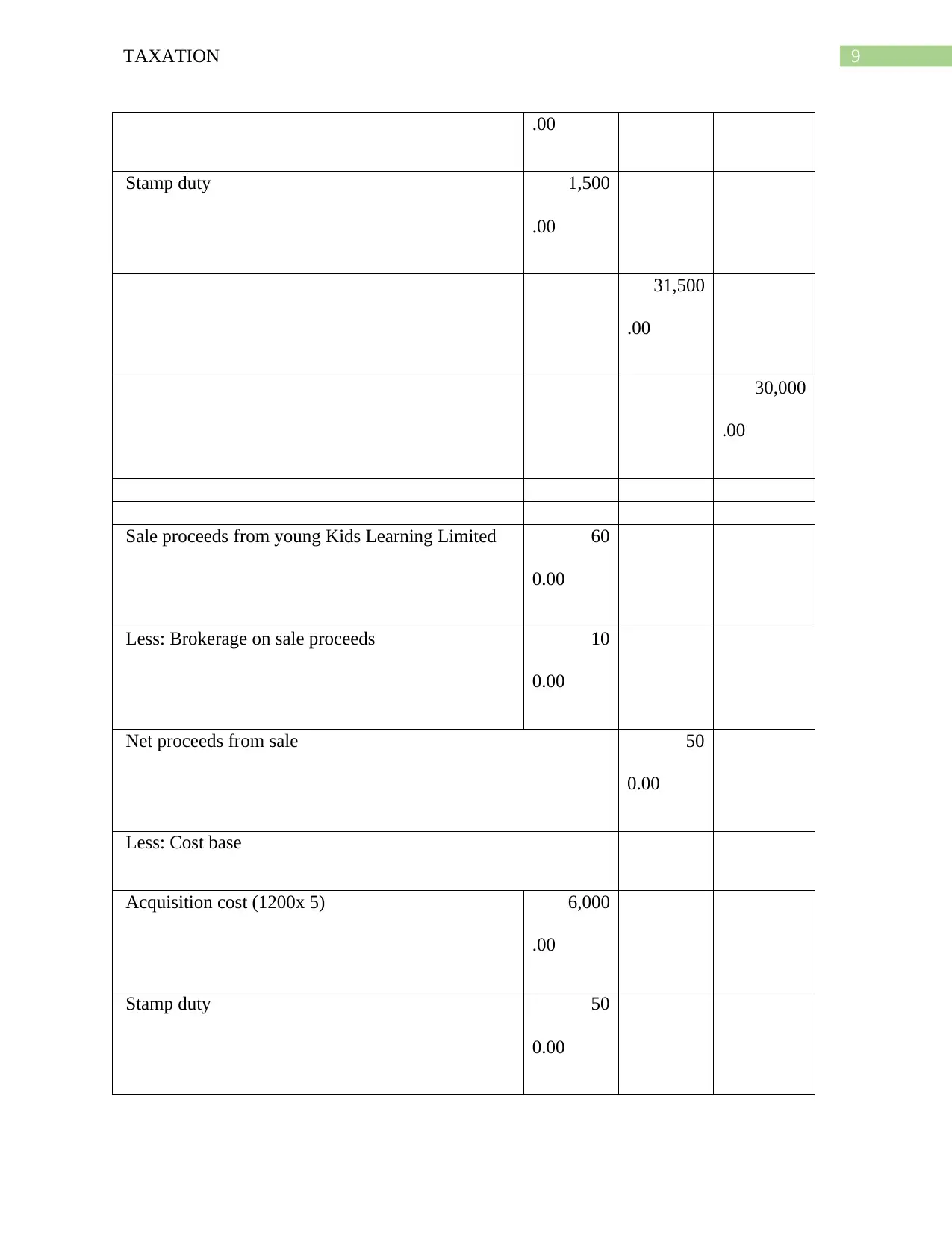

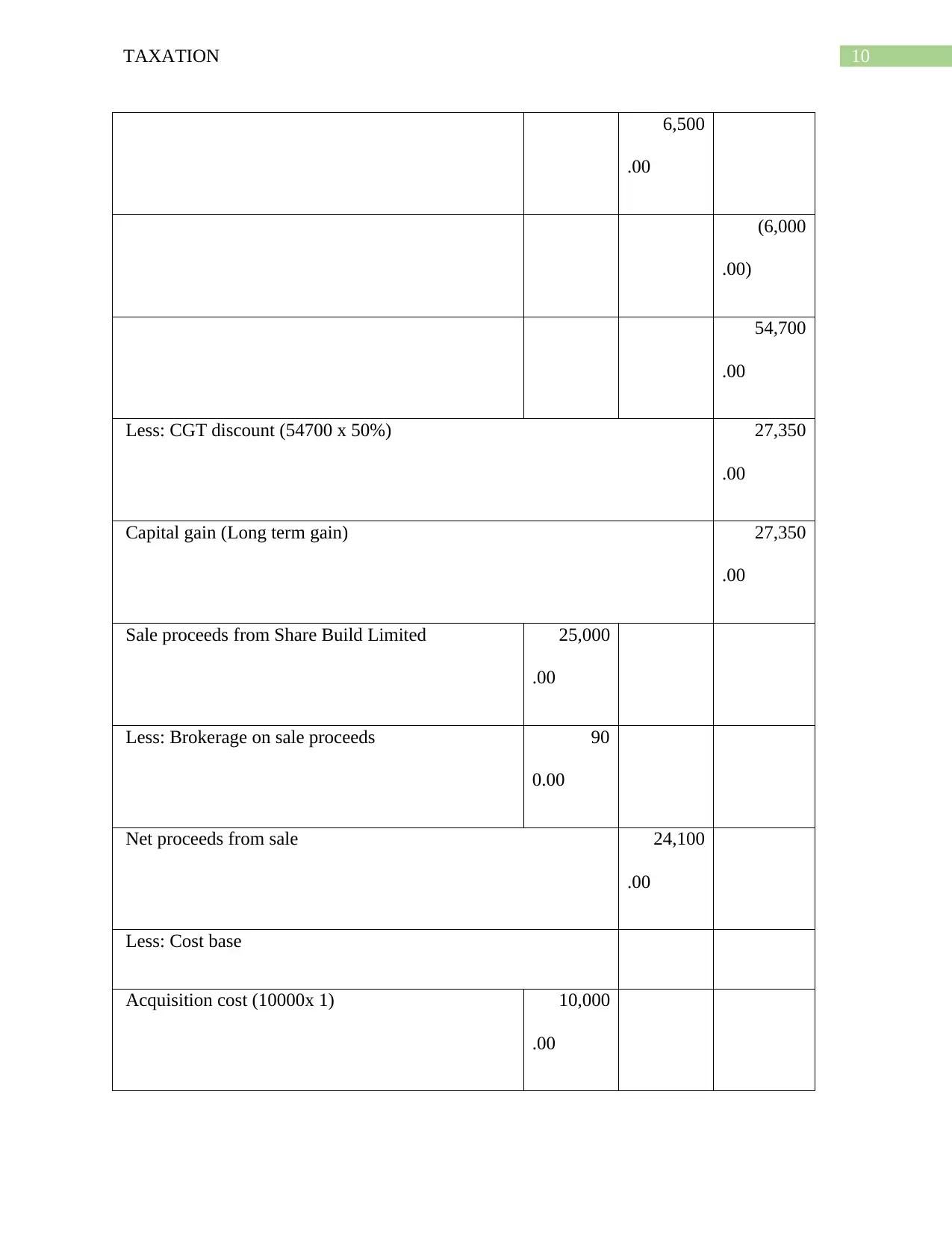

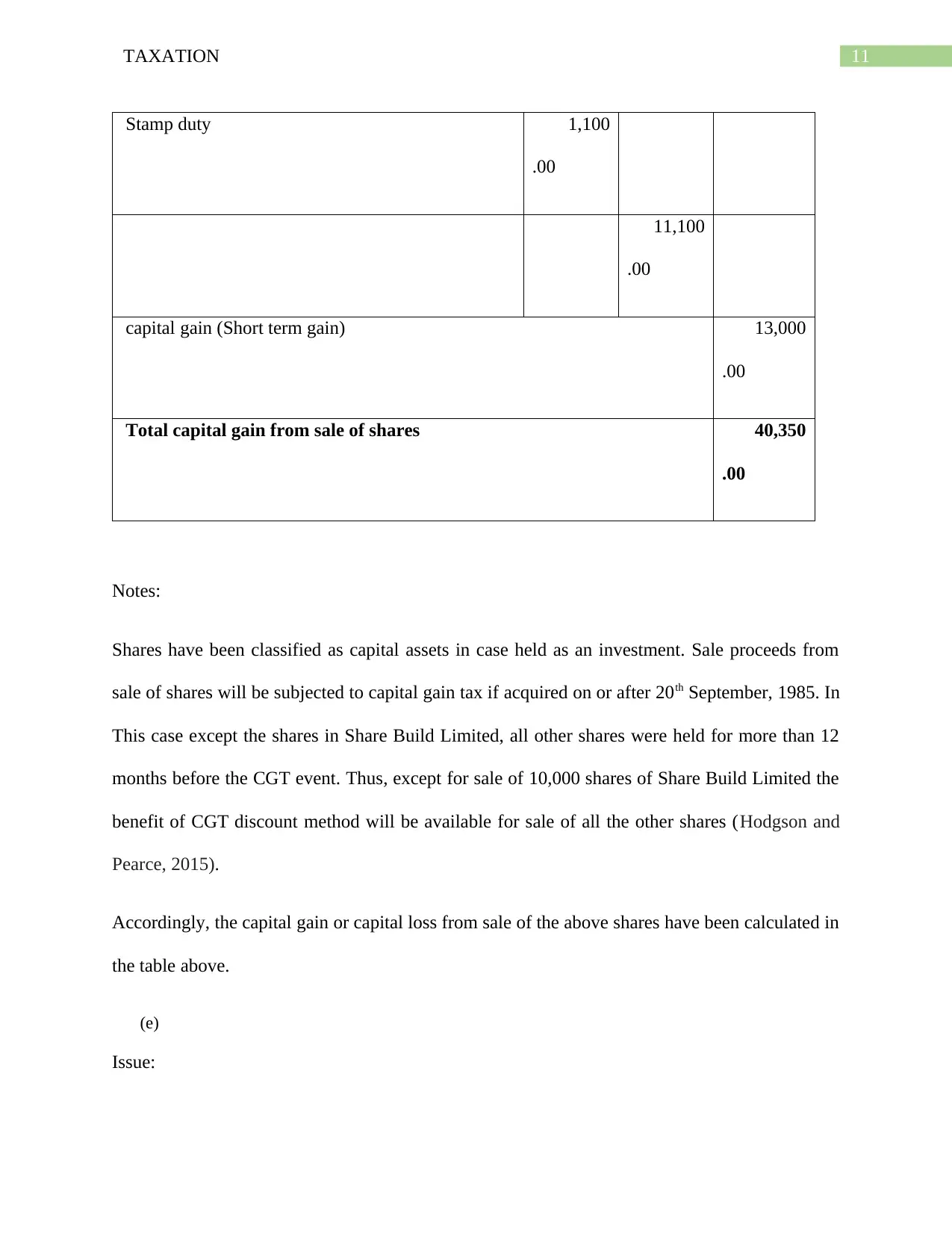

This assignment analyzes various taxation scenarios for a tax consultant's client, covering capital gains tax (CGT) and fringe benefits tax (FBT). The assignment addresses the tax implications of selling vacant land, the loss of an antique bed, the sale of a painting acquired before CGT introduction, and the sale of shares, including the calculation of capital gains and losses. It also examines whether the sale of a violin attracts CGT. Furthermore, the assignment delves into fringe benefits tax, specifically assessing whether a car provided to an employee constitutes a fringe benefit and the employer's FBT liability. The document includes detailed calculations and explanations based on Australian taxation laws.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.