HI6028 Taxation Theory, Practice & Law: Analyzing Key Tax Concepts

VerifiedAdded on 2020/04/07

|8

|2435

|402

Homework Assignment

AI Summary

This assignment solution for HI6028 Taxation Theory, Practice & Law T2 2017 covers several key areas of taxation. It includes calculating net capital gains and losses from asset sales, determining the taxable value of fringe benefits related to low-interest loans, and analyzing the allocation of rental property losses between co-owners. The assignment also discusses a landmark case concerning tax avoidance schemes and addresses the tax implications of selling timber from a piece of land, referencing relevant tax regulations and legal precedents to support its conclusions. The document is a valuable resource for students studying taxation, offering detailed explanations and practical applications of complex tax concepts, and is available on Desklib, a platform offering a wide array of study tools.

HI6028 Taxation Theory, Practice & Law

T2 2017 Individual Assignment

T2 2017 Individual Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Question 2..................................................................................................................................3

Question 3..................................................................................................................................3

Question 4..................................................................................................................................4

Question 5..................................................................................................................................4

References..................................................................................................................................5

Question 1..................................................................................................................................3

Question 2..................................................................................................................................3

Question 3..................................................................................................................................3

Question 4..................................................................................................................................4

Question 5..................................................................................................................................4

References..................................................................................................................................5

QUESTION 1

Issue Calculating the net capital loss or gain from the assets bought and sold by

Eric.

An antique vase

$2,000

An antique chair

$3,000

A painting

$9,000

A home sound system

$12,000

Shares in a listed company

$5,000

The assets sold were as follows-

antique vase-

$3,000

antique chair- $1,000

painting- $1,000

sound system- $11,000

shares- $20,000

Regulatory

provisions

For the purpose of determining capital gain or loss, as per the Australian

Tax provisions, the holding period of an asset is the critical point to be

considered. According to the provisions stated thereto, if the asset holding

period is more than a year, indexation or discounting method is applied for

this purpose of determining capital loss or gain (AO, 2015). On the other

hand, if the defined period is less than a year then the taxable amount is

calculated as-

Sales price - purchase price

The loss arising from one transaction is compensated by the other.

Applicability

of cited

provisions in

In the present scenario, the assets have been held by Eric for less than

twelve months, and due to the same reason, the other method in which gain

is ascertained through reducing purchase price from selling price will be

applied. The capital gain or capital will be calculated in the following

Issue Calculating the net capital loss or gain from the assets bought and sold by

Eric.

An antique vase

$2,000

An antique chair

$3,000

A painting

$9,000

A home sound system

$12,000

Shares in a listed company

$5,000

The assets sold were as follows-

antique vase-

$3,000

antique chair- $1,000

painting- $1,000

sound system- $11,000

shares- $20,000

Regulatory

provisions

For the purpose of determining capital gain or loss, as per the Australian

Tax provisions, the holding period of an asset is the critical point to be

considered. According to the provisions stated thereto, if the asset holding

period is more than a year, indexation or discounting method is applied for

this purpose of determining capital loss or gain (AO, 2015). On the other

hand, if the defined period is less than a year then the taxable amount is

calculated as-

Sales price - purchase price

The loss arising from one transaction is compensated by the other.

Applicability

of cited

provisions in

In the present scenario, the assets have been held by Eric for less than

twelve months, and due to the same reason, the other method in which gain

is ascertained through reducing purchase price from selling price will be

applied. The capital gain or capital will be calculated in the following

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

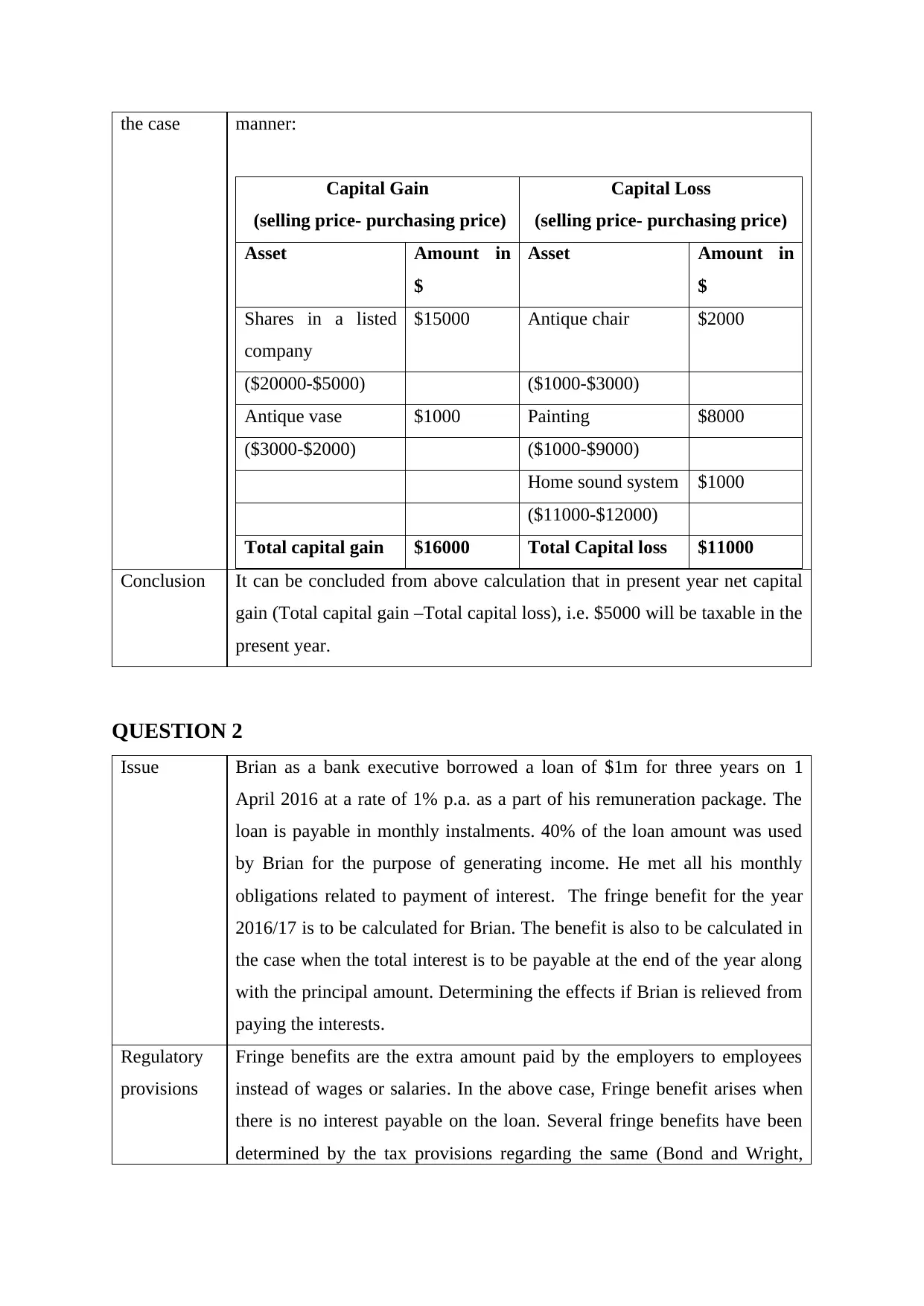

the case manner:

Capital Gain

(selling price- purchasing price)

Capital Loss

(selling price- purchasing price)

Asset Amount in

$

Asset Amount in

$

Shares in a listed

company

$15000 Antique chair $2000

($20000-$5000) ($1000-$3000)

Antique vase $1000 Painting $8000

($3000-$2000) ($1000-$9000)

Home sound system $1000

($11000-$12000)

Total capital gain $16000 Total Capital loss $11000

Conclusion It can be concluded from above calculation that in present year net capital

gain (Total capital gain –Total capital loss), i.e. $5000 will be taxable in the

present year.

QUESTION 2

Issue Brian as a bank executive borrowed a loan of $1m for three years on 1

April 2016 at a rate of 1% p.a. as a part of his remuneration package. The

loan is payable in monthly instalments. 40% of the loan amount was used

by Brian for the purpose of generating income. He met all his monthly

obligations related to payment of interest. The fringe benefit for the year

2016/17 is to be calculated for Brian. The benefit is also to be calculated in

the case when the total interest is to be payable at the end of the year along

with the principal amount. Determining the effects if Brian is relieved from

paying the interests.

Regulatory

provisions

Fringe benefits are the extra amount paid by the employers to employees

instead of wages or salaries. In the above case, Fringe benefit arises when

there is no interest payable on the loan. Several fringe benefits have been

determined by the tax provisions regarding the same (Bond and Wright,

Capital Gain

(selling price- purchasing price)

Capital Loss

(selling price- purchasing price)

Asset Amount in

$

Asset Amount in

$

Shares in a listed

company

$15000 Antique chair $2000

($20000-$5000) ($1000-$3000)

Antique vase $1000 Painting $8000

($3000-$2000) ($1000-$9000)

Home sound system $1000

($11000-$12000)

Total capital gain $16000 Total Capital loss $11000

Conclusion It can be concluded from above calculation that in present year net capital

gain (Total capital gain –Total capital loss), i.e. $5000 will be taxable in the

present year.

QUESTION 2

Issue Brian as a bank executive borrowed a loan of $1m for three years on 1

April 2016 at a rate of 1% p.a. as a part of his remuneration package. The

loan is payable in monthly instalments. 40% of the loan amount was used

by Brian for the purpose of generating income. He met all his monthly

obligations related to payment of interest. The fringe benefit for the year

2016/17 is to be calculated for Brian. The benefit is also to be calculated in

the case when the total interest is to be payable at the end of the year along

with the principal amount. Determining the effects if Brian is relieved from

paying the interests.

Regulatory

provisions

Fringe benefits are the extra amount paid by the employers to employees

instead of wages or salaries. In the above case, Fringe benefit arises when

there is no interest payable on the loan. Several fringe benefits have been

determined by the tax provisions regarding the same (Bond and Wright,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2017). These provisions also contain specific rules of valuation for each

benefit. The taxable value of fringe benefits is calculated by the measuring

the difference in the interest rate payable by the borrower with that of the

statutory interest rate. The statutory tax rate for the year 2016 and 2017

were 5.65%.

Applicability

of cited

provisions in

the case

The taxable value of fringe benefit

= Amount of interest in accordance with statutory rate (working note 1) –

The amount of interest actually paid by the assessee (working note-2) *

proportion of loan applied for producing income

=$56500-$10000

=$46500 *40%

=$18600

Working Note :1

Amount of loan * rate at will loan provided by bank

=$1000000*1%

=$10000

Working Note: 2

Amount of loan * statutory rate of interest

=$1000000*5.65%

=$56500

Conclusion In the present case as only 40% of the total amount of loan taken has been

applied for producing income; the same will be the taxable amount of

fringe benefits tax. The fact that whether interest is paid on monthly or

yearly basis does not have any effect on the amount of fringe benefits tax.

Moreover, if in a situation Brain is not liable to pay any amount of interest

and released from whole liability that the entire amount of interest will be

taxable. The same will be further proportioned to the extent amount has

been applied for producing income.

QUESTION 3

Issue Determining the allocation of loss for the purpose of tax for Jack and Jill.

They both have borrowed money for the purpose of purchasing a rental

benefit. The taxable value of fringe benefits is calculated by the measuring

the difference in the interest rate payable by the borrower with that of the

statutory interest rate. The statutory tax rate for the year 2016 and 2017

were 5.65%.

Applicability

of cited

provisions in

the case

The taxable value of fringe benefit

= Amount of interest in accordance with statutory rate (working note 1) –

The amount of interest actually paid by the assessee (working note-2) *

proportion of loan applied for producing income

=$56500-$10000

=$46500 *40%

=$18600

Working Note :1

Amount of loan * rate at will loan provided by bank

=$1000000*1%

=$10000

Working Note: 2

Amount of loan * statutory rate of interest

=$1000000*5.65%

=$56500

Conclusion In the present case as only 40% of the total amount of loan taken has been

applied for producing income; the same will be the taxable amount of

fringe benefits tax. The fact that whether interest is paid on monthly or

yearly basis does not have any effect on the amount of fringe benefits tax.

Moreover, if in a situation Brain is not liable to pay any amount of interest

and released from whole liability that the entire amount of interest will be

taxable. The same will be further proportioned to the extent amount has

been applied for producing income.

QUESTION 3

Issue Determining the allocation of loss for the purpose of tax for Jack and Jill.

They both have borrowed money for the purpose of purchasing a rental

property as joint tenants.

As per the written agreement executed between them for the profit

entitlement, Jack is allowed 10% share in profit and Jill is allowed to have

the rest that is 90%. Jack is entitled to loss, if any, by 100%. There was a

loss of $10,000 arose in the past year. Calculating capital gain or loss that

will arise on their part if they decide to sell the property.

Regulatory

provisions

The tax provision applicable for the purpose would be TR 93/32-

distribution of net profit and loss among co-owners. The co-owners of the

rental property are not to be considered as partners as per the law unless the

partnership is for the purpose of carrying on some business. If they are

considered as a partner, this would be irrelevant since it is an unreal

partnership and not according to the provisions for partnership

(Braithwaite, 2017). This form of unreal partnership would entail many

other implications and not just share of profit and loss. In partnership, any

event of loss does not mean the loss of their interest. Hence, their mutual

interest in their rented place is retained even after the loss.

Applicability

of cited

provisions in

the case

In the present case as Jack and Jill both are co-tenants, and as per the

agreement of partnership, it has been provided that the ratio of profit

between them is 1:9 (Jack : Jill) and in case of loss the ratio is 1:0 (Jack :

Jill). However, in accordance with above provision no partnership existed

among the respondent and their spouse as per the general law. Further,

renting single premises cannot be said as conducting business; thus their

partnership will not be treated as a partnership for income tax purposes.

Further, profit and loss should be apportioned on an equal basis, i.e. 50: 50

as they both have equal right in business. The same result was concluded in

case of FCT v Whiting (1943), 68 CLR 199 at 204; 2 AITR 421.

Conclusion From above analysis, it can be assessed that it is necessary to ascertain

whether both the responder and the wife are notional partners for presenting

the same in the eyes of the law or they are actually partners in accordance

with general law. Thus, they will be liable for equal profit and loss and not

in accordance with the ratio provided in the partnership agreement for

income tax purposes.

As per the written agreement executed between them for the profit

entitlement, Jack is allowed 10% share in profit and Jill is allowed to have

the rest that is 90%. Jack is entitled to loss, if any, by 100%. There was a

loss of $10,000 arose in the past year. Calculating capital gain or loss that

will arise on their part if they decide to sell the property.

Regulatory

provisions

The tax provision applicable for the purpose would be TR 93/32-

distribution of net profit and loss among co-owners. The co-owners of the

rental property are not to be considered as partners as per the law unless the

partnership is for the purpose of carrying on some business. If they are

considered as a partner, this would be irrelevant since it is an unreal

partnership and not according to the provisions for partnership

(Braithwaite, 2017). This form of unreal partnership would entail many

other implications and not just share of profit and loss. In partnership, any

event of loss does not mean the loss of their interest. Hence, their mutual

interest in their rented place is retained even after the loss.

Applicability

of cited

provisions in

the case

In the present case as Jack and Jill both are co-tenants, and as per the

agreement of partnership, it has been provided that the ratio of profit

between them is 1:9 (Jack : Jill) and in case of loss the ratio is 1:0 (Jack :

Jill). However, in accordance with above provision no partnership existed

among the respondent and their spouse as per the general law. Further,

renting single premises cannot be said as conducting business; thus their

partnership will not be treated as a partnership for income tax purposes.

Further, profit and loss should be apportioned on an equal basis, i.e. 50: 50

as they both have equal right in business. The same result was concluded in

case of FCT v Whiting (1943), 68 CLR 199 at 204; 2 AITR 421.

Conclusion From above analysis, it can be assessed that it is necessary to ascertain

whether both the responder and the wife are notional partners for presenting

the same in the eyes of the law or they are actually partners in accordance

with general law. Thus, they will be liable for equal profit and loss and not

in accordance with the ratio provided in the partnership agreement for

income tax purposes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 4

Issue An agreement was carried out between IRC and Duke of Westminster

regarding its associates which comprise gardener, house helpers and other

servants. As per the agreement, Duke was liable to pay additional money, and

in return, same was liable to pay money as a reward for the same. Further,

affidavit relating to payment of additional wages was submitted in which it

was declared that additional sum would be paid by Duke in case they provide

extra services. Even after the agreement, some servants received wages as

they received before and on the other hand, Duke received a benefit in tax

liability due to the agreement which he submitted that he will pay additional

charges to his servants.

Regulator

y

provisions

The decision was made by Lord Tomlin which declared that every individual

is having the right to order his affairs in a way that liability of tax in

accordance with appropriate Acts is less in any other case it would have

actually been (Woellner and et.al. 2016). Further, if he succeeds in ordering

them to secure this result. In that case, it does not matter the manner

unappreciative Commissioner of Inland revenue of other authorities may be

his ingenuity. Moreover, he cannot be compelled to pay an increased tax.

Relevance

in present

scenario

Provisions have been made by the constitution in the recent year which

requires the advisors to inform the HRMC regarding any scheme which

results into the evasion of tax liability. Further, it would not be assessed by

the board and the action which is taken after receiving notifications relating to

the scheme of tax evasion. It was assessed by Lord Wilberforce that the

decision of the case of Westminster prevented the court from noticing the

actual transaction to some alleged basis substance (Long, Campbell and

Kelshaw, 2016). However, the court should identify the facts relating to the

case and make decisions relating to same. Further, it can be said that the

existing scheme was encouraging tax avoidance in the absence of any

commercial justification. Thus, the Tomlin Westminster ruling specifies that

taxpayer never had a right to abuse in that way in first place, this means that

he does not suggest for avoiding tax but assist for non-right to have not had

tax avoided.

Issue An agreement was carried out between IRC and Duke of Westminster

regarding its associates which comprise gardener, house helpers and other

servants. As per the agreement, Duke was liable to pay additional money, and

in return, same was liable to pay money as a reward for the same. Further,

affidavit relating to payment of additional wages was submitted in which it

was declared that additional sum would be paid by Duke in case they provide

extra services. Even after the agreement, some servants received wages as

they received before and on the other hand, Duke received a benefit in tax

liability due to the agreement which he submitted that he will pay additional

charges to his servants.

Regulator

y

provisions

The decision was made by Lord Tomlin which declared that every individual

is having the right to order his affairs in a way that liability of tax in

accordance with appropriate Acts is less in any other case it would have

actually been (Woellner and et.al. 2016). Further, if he succeeds in ordering

them to secure this result. In that case, it does not matter the manner

unappreciative Commissioner of Inland revenue of other authorities may be

his ingenuity. Moreover, he cannot be compelled to pay an increased tax.

Relevance

in present

scenario

Provisions have been made by the constitution in the recent year which

requires the advisors to inform the HRMC regarding any scheme which

results into the evasion of tax liability. Further, it would not be assessed by

the board and the action which is taken after receiving notifications relating to

the scheme of tax evasion. It was assessed by Lord Wilberforce that the

decision of the case of Westminster prevented the court from noticing the

actual transaction to some alleged basis substance (Long, Campbell and

Kelshaw, 2016). However, the court should identify the facts relating to the

case and make decisions relating to same. Further, it can be said that the

existing scheme was encouraging tax avoidance in the absence of any

commercial justification. Thus, the Tomlin Westminster ruling specifies that

taxpayer never had a right to abuse in that way in first place, this means that

he does not suggest for avoiding tax but assist for non-right to have not had

tax avoided.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 5

Issue Bill, an owner if a piece of land, which he intends to use for the purpose of

grazing. The land has pine trees which when sold to a company in the form

of timber is expected to generate $1,000 for every 100 metres. Bill is to be

advised that would these receipts be considered for the purpose of taxation.

Measuring the implications if he receives a lump sum amount of $50,000

by the logging company against the right to any amount of timer collected

from his land.

Regulatory

provisions

According to TR 95/6- point 22- subsection 36(1)- The section deals with

the provision of disposing of standing timer, not in ordinary course of

business. As per the provision of this section, the sale price arising as a

result of the disposal of planted trees is a taxable income during the year in

which the disposal arises. It does not matter if the person if the person is

carrying a business related to forest or not and also when the tree disposal is

not as a part of normal course of business (Barkoczy, 2016). The point to

be considered here is that the tress must be the subject matter of business or

just a part of it. The value of trees is to be valued on the market rate on the

date of disposal- TR 95/6.

Point 25 of TR 95/6: The point deals with disposal of rights to standing

timber. It has been provided in the provisions of the specified section that a

taxpayer engaged in forest operations may put the timber to sale. The

income produced thereon is taxable as per this subsection. Moreover, the

royalty obtained by the taxpayer pertaining to the right given for the

purpose of procuring timber on the taxpayer’s land would be considered for

the purpose of taxation (Barkoczy, 2017). This rule would be applicable

even if the selling of right is not a part of normal course of business of the

taxpayer.

In this regard, the judge Lord Tomlin said that it is allowed for each and

every person to arrange their business affairs in such a way so as to reduce

the tax implications. If the person succeeds in the same, then they can

safeguard their interest.

Applicability

of cited

In the first scenario, the transactions are relating to disposal of standing

timber which is not in ordinary course of business. Thus, the income which

Issue Bill, an owner if a piece of land, which he intends to use for the purpose of

grazing. The land has pine trees which when sold to a company in the form

of timber is expected to generate $1,000 for every 100 metres. Bill is to be

advised that would these receipts be considered for the purpose of taxation.

Measuring the implications if he receives a lump sum amount of $50,000

by the logging company against the right to any amount of timer collected

from his land.

Regulatory

provisions

According to TR 95/6- point 22- subsection 36(1)- The section deals with

the provision of disposing of standing timer, not in ordinary course of

business. As per the provision of this section, the sale price arising as a

result of the disposal of planted trees is a taxable income during the year in

which the disposal arises. It does not matter if the person if the person is

carrying a business related to forest or not and also when the tree disposal is

not as a part of normal course of business (Barkoczy, 2016). The point to

be considered here is that the tress must be the subject matter of business or

just a part of it. The value of trees is to be valued on the market rate on the

date of disposal- TR 95/6.

Point 25 of TR 95/6: The point deals with disposal of rights to standing

timber. It has been provided in the provisions of the specified section that a

taxpayer engaged in forest operations may put the timber to sale. The

income produced thereon is taxable as per this subsection. Moreover, the

royalty obtained by the taxpayer pertaining to the right given for the

purpose of procuring timber on the taxpayer’s land would be considered for

the purpose of taxation (Barkoczy, 2017). This rule would be applicable

even if the selling of right is not a part of normal course of business of the

taxpayer.

In this regard, the judge Lord Tomlin said that it is allowed for each and

every person to arrange their business affairs in such a way so as to reduce

the tax implications. If the person succeeds in the same, then they can

safeguard their interest.

Applicability

of cited

In the first scenario, the transactions are relating to disposal of standing

timber which is not in ordinary course of business. Thus, the income which

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.