HI6028 Taxation Case Study: Capital Gains, Fringe Benefits Analysis

VerifiedAdded on 2019/09/23

|14

|2517

|69

Case Study

AI Summary

This assignment analyzes two case studies related to Australian taxation. The first case study focuses on capital gains tax, examining the sale of a holiday home, calculating taxable income using both discount and indexation methods, and addressing the treatment of capital losses and the impact of the Income Tax Assessment Act. The second case study delves into fringe benefits tax, exploring the tax implications of company cars and employee loans. It covers the computation of fringe benefits for car usage and interest-free loans, and the application of relevant provisions from the Income Tax Assessment Act. The analysis includes calculations, considerations for tax planning, and emphasizes the importance of maintaining proper documentation for tax purposes. The assignment provides a detailed overview of these complex tax scenarios.

HI6028_Taxation_Assignment

[Type the document subtitle]

Student

[Pick the date]

[Type the document subtitle]

Student

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Case study 1: Capital Gain Taxation..........................................................................................................2

Case study 2: Fringe Benefits.......................................................................................................................8

References.................................................................................................................................................13

1

Case study 1: Capital Gain Taxation..........................................................................................................2

Case study 2: Fringe Benefits.......................................................................................................................8

References.................................................................................................................................................13

1

Case study 1: Capital Gain Taxation

Facts of the case:

Fred is a resident assessee

Assessee has sold Holiday home. That means, the assessee has a Main residence

where he resides

Holiday home is located in Blue Mountain

Agreement to sale happened in August 2015

Actual sales consideration received in February 2016

Sale consideration $8,00,000

Cost incurred for selling the house property $ 1100 (legal fees inclusive of Goods

and Service Tax) plus $9900 (Sale agent’s commission inclusive of Goods and

Service Tax)

Year of Purchase 1987. Month March

Cost of purchasing the House property $100000

Stamp duty paid on purchase of the said property $2000 (2% of consideration)

Legal fees paid $2000

Fred has other Capital Loss of $10000

The capital loss has arose due to Sale of Shares

Assumptions:

The house property is located within the Taxation Authorities

2

Facts of the case:

Fred is a resident assessee

Assessee has sold Holiday home. That means, the assessee has a Main residence

where he resides

Holiday home is located in Blue Mountain

Agreement to sale happened in August 2015

Actual sales consideration received in February 2016

Sale consideration $8,00,000

Cost incurred for selling the house property $ 1100 (legal fees inclusive of Goods

and Service Tax) plus $9900 (Sale agent’s commission inclusive of Goods and

Service Tax)

Year of Purchase 1987. Month March

Cost of purchasing the House property $100000

Stamp duty paid on purchase of the said property $2000 (2% of consideration)

Legal fees paid $2000

Fred has other Capital Loss of $10000

The capital loss has arose due to Sale of Shares

Assumptions:

The house property is located within the Taxation Authorities

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assessment year as per the Revenue authorities begin from 1st July and ends

30th June

Assessee resides in his Main Residence which is different than Holiday home.

Assessee has not made any investment further out of the sales consideration for

the purpose of Tax saving

Answer

Point of Taxation – August 2015. As per the Income Tax Assessment Act 1937, the

point of taxation in case of Sale of real estate properties other than those which are held

for personal use is the time when the contract agreement is registered with local

authorities (Smith, 2004).

It becomes crucial for the assessee Fred to identify the point of taxation of a Capital Gain

taxation event. It has implication in calculation of Tax Liability.

In this case, the contract for sale was registered in August 2015. And hence Capital Gain

Taxation liability starts from Assessment Year 2016-17. i.e. Financial year 2015-16.

However, Liability shall be paid in the year, settlement happens. In this case, the

settlement is done in February 2016 and hence the payment of Capital Gain Tax (if any)

shall be subject to payment in AY 16-17 only.

3

30th June

Assessee resides in his Main Residence which is different than Holiday home.

Assessee has not made any investment further out of the sales consideration for

the purpose of Tax saving

Answer

Point of Taxation – August 2015. As per the Income Tax Assessment Act 1937, the

point of taxation in case of Sale of real estate properties other than those which are held

for personal use is the time when the contract agreement is registered with local

authorities (Smith, 2004).

It becomes crucial for the assessee Fred to identify the point of taxation of a Capital Gain

taxation event. It has implication in calculation of Tax Liability.

In this case, the contract for sale was registered in August 2015. And hence Capital Gain

Taxation liability starts from Assessment Year 2016-17. i.e. Financial year 2015-16.

However, Liability shall be paid in the year, settlement happens. In this case, the

settlement is done in February 2016 and hence the payment of Capital Gain Tax (if any)

shall be subject to payment in AY 16-17 only.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

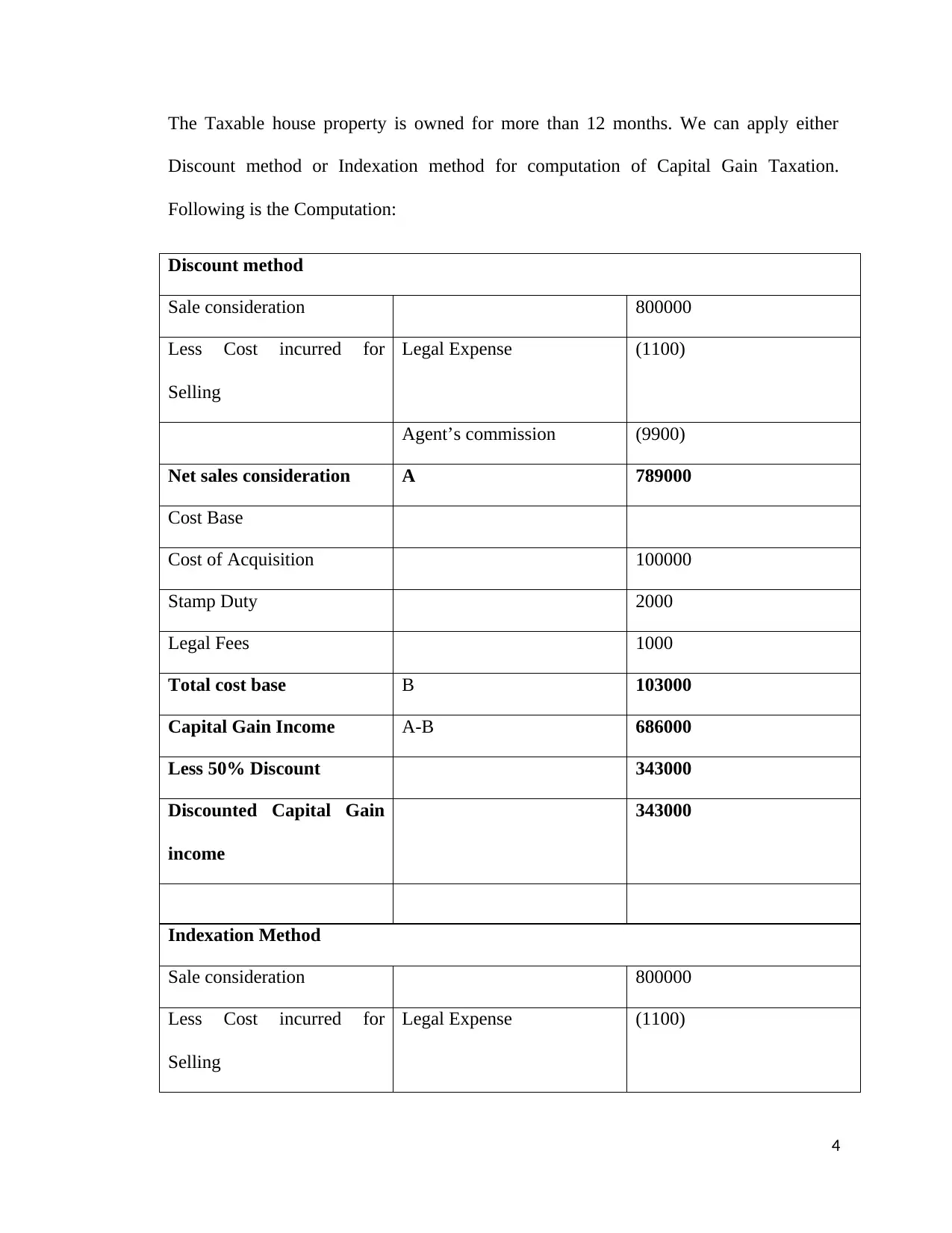

The Taxable house property is owned for more than 12 months. We can apply either

Discount method or Indexation method for computation of Capital Gain Taxation.

Following is the Computation:

Discount method

Sale consideration 800000

Less Cost incurred for

Selling

Legal Expense (1100)

Agent’s commission (9900)

Net sales consideration A 789000

Cost Base

Cost of Acquisition 100000

Stamp Duty 2000

Legal Fees 1000

Total cost base B 103000

Capital Gain Income A-B 686000

Less 50% Discount 343000

Discounted Capital Gain

income

343000

Indexation Method

Sale consideration 800000

Less Cost incurred for

Selling

Legal Expense (1100)

4

Discount method or Indexation method for computation of Capital Gain Taxation.

Following is the Computation:

Discount method

Sale consideration 800000

Less Cost incurred for

Selling

Legal Expense (1100)

Agent’s commission (9900)

Net sales consideration A 789000

Cost Base

Cost of Acquisition 100000

Stamp Duty 2000

Legal Fees 1000

Total cost base B 103000

Capital Gain Income A-B 686000

Less 50% Discount 343000

Discounted Capital Gain

income

343000

Indexation Method

Sale consideration 800000

Less Cost incurred for

Selling

Legal Expense (1100)

4

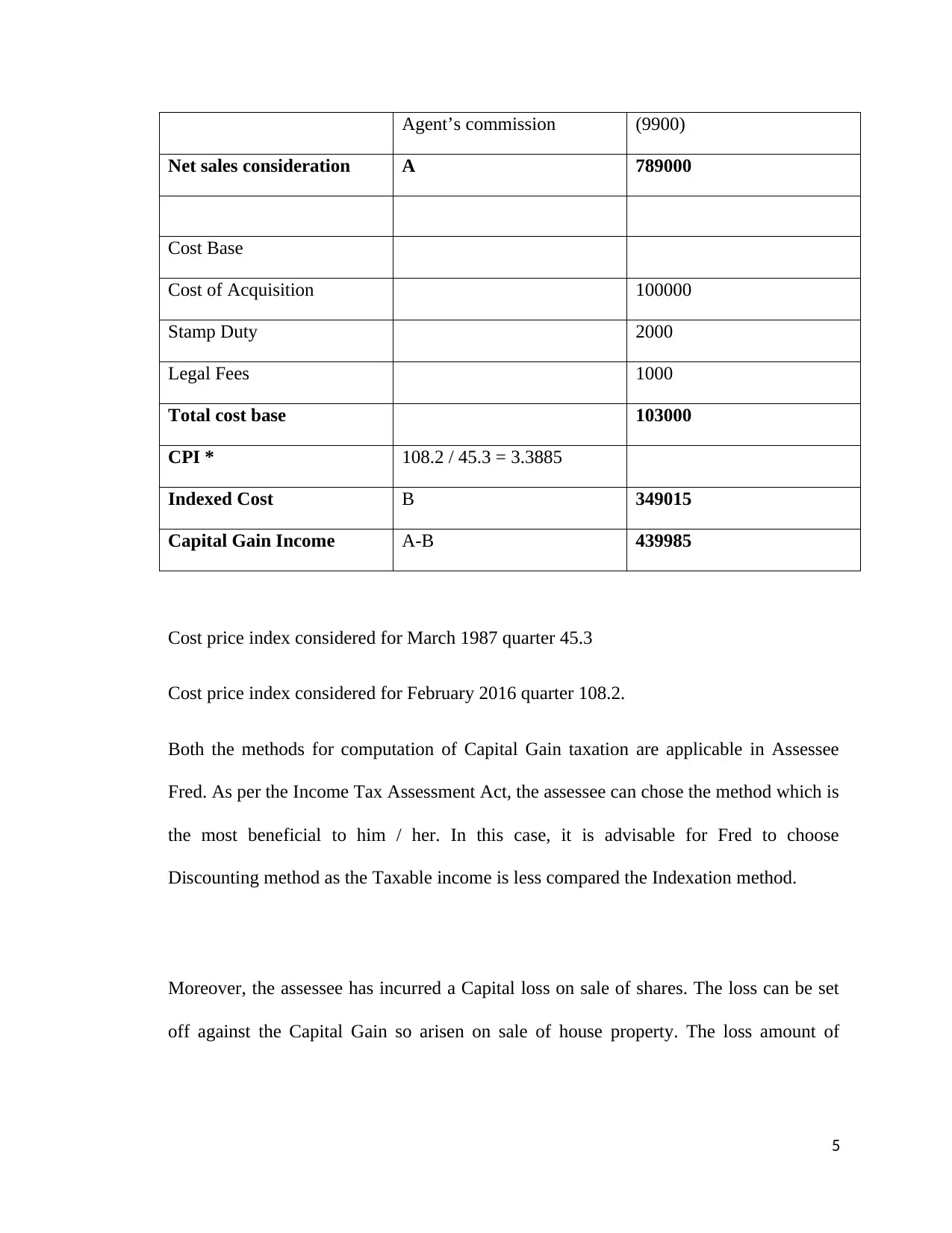

Agent’s commission (9900)

Net sales consideration A 789000

Cost Base

Cost of Acquisition 100000

Stamp Duty 2000

Legal Fees 1000

Total cost base 103000

CPI * 108.2 / 45.3 = 3.3885

Indexed Cost B 349015

Capital Gain Income A-B 439985

Cost price index considered for March 1987 quarter 45.3

Cost price index considered for February 2016 quarter 108.2.

Both the methods for computation of Capital Gain taxation are applicable in Assessee

Fred. As per the Income Tax Assessment Act, the assessee can chose the method which is

the most beneficial to him / her. In this case, it is advisable for Fred to choose

Discounting method as the Taxable income is less compared the Indexation method.

Moreover, the assessee has incurred a Capital loss on sale of shares. The loss can be set

off against the Capital Gain so arisen on sale of house property. The loss amount of

5

Net sales consideration A 789000

Cost Base

Cost of Acquisition 100000

Stamp Duty 2000

Legal Fees 1000

Total cost base 103000

CPI * 108.2 / 45.3 = 3.3885

Indexed Cost B 349015

Capital Gain Income A-B 439985

Cost price index considered for March 1987 quarter 45.3

Cost price index considered for February 2016 quarter 108.2.

Both the methods for computation of Capital Gain taxation are applicable in Assessee

Fred. As per the Income Tax Assessment Act, the assessee can chose the method which is

the most beneficial to him / her. In this case, it is advisable for Fred to choose

Discounting method as the Taxable income is less compared the Indexation method.

Moreover, the assessee has incurred a Capital loss on sale of shares. The loss can be set

off against the Capital Gain so arisen on sale of house property. The loss amount of

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

$10000 can be adjusted against the Capital gain income of $343000. Next Capital gain

income works out to be $333000.

Instead of loss from sale of shares, the assessee had incurred loss on sale of antique vase.

Antiques are part of collectables. As per the Income Tax Assessment Act, assets which

are of personal use incuding collectables are exempted assets and hence capital gain

chapter does not apply. But, there is a condition of asset value $10000 in case of

collectable. As per the relevant provisions of the act, items which are of value less than

$10000 are exempt from Capital Gain purview. In the given case, the Assessee, Fred has

incurred a loss of $10000 in Collectables, which means the actual value or the actual cost

of purchasing the Antique was more than $10000. This is an exception to the exemption

clause. Hence the consumable item does not fall in the exempted category and hence

liable to Capital Gain Tax. It shall be noted that Capital Gain income includes loss also.

In the given case, the loss can be set off against the capital gain of $343000.

The loss on sale of antique vase will not create any difference in Capital gain income

because the same is taxable in the eyes of law.

In case the revenue authorities scrutinize the case, the assessee, Fred in this case is liable

to produce all necessary documents which justify the Sales consideration / Purchase cost

of the Capital Gain Asset. If he fails to do so, the revenue department can raise demand

which shall be paid along with necessary penalty and interest. It is rather advisable to

6

income works out to be $333000.

Instead of loss from sale of shares, the assessee had incurred loss on sale of antique vase.

Antiques are part of collectables. As per the Income Tax Assessment Act, assets which

are of personal use incuding collectables are exempted assets and hence capital gain

chapter does not apply. But, there is a condition of asset value $10000 in case of

collectable. As per the relevant provisions of the act, items which are of value less than

$10000 are exempt from Capital Gain purview. In the given case, the Assessee, Fred has

incurred a loss of $10000 in Collectables, which means the actual value or the actual cost

of purchasing the Antique was more than $10000. This is an exception to the exemption

clause. Hence the consumable item does not fall in the exempted category and hence

liable to Capital Gain Tax. It shall be noted that Capital Gain income includes loss also.

In the given case, the loss can be set off against the capital gain of $343000.

The loss on sale of antique vase will not create any difference in Capital gain income

because the same is taxable in the eyes of law.

In case the revenue authorities scrutinize the case, the assessee, Fred in this case is liable

to produce all necessary documents which justify the Sales consideration / Purchase cost

of the Capital Gain Asset. If he fails to do so, the revenue department can raise demand

which shall be paid along with necessary penalty and interest. It is rather advisable to

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

keep a regular file which has all the relevant documents in original for the purpose of

justifying what is shown in the return of income at the end of the year. It is also stated in

law that the records should be maintained in English language or which are easily

translable to English.

Following are some of the records required to be maintained by the assessee in the

Capital Gain Taxation

Acknowledgement receipts of purchase of property or transfer of properties

Borrowing of money. Interest expended related to the asset sold in the Capital

Gain Working

Bills / supportive papers justifying the payment to the professionals like agents,

Book keeper, Legal advisors and other miscellaneous cost for advertising

Insurance premium paid receipts and other rates and taxes

Valuation reports by Income tax recognized and registered valuers

Job card of the repairing work / maintanence contracts etc

Bank statements which support all above transactions

7

justifying what is shown in the return of income at the end of the year. It is also stated in

law that the records should be maintained in English language or which are easily

translable to English.

Following are some of the records required to be maintained by the assessee in the

Capital Gain Taxation

Acknowledgement receipts of purchase of property or transfer of properties

Borrowing of money. Interest expended related to the asset sold in the Capital

Gain Working

Bills / supportive papers justifying the payment to the professionals like agents,

Book keeper, Legal advisors and other miscellaneous cost for advertising

Insurance premium paid receipts and other rates and taxes

Valuation reports by Income tax recognized and registered valuers

Job card of the repairing work / maintanence contracts etc

Bank statements which support all above transactions

7

Case study 2: Fringe Benefits

Salary income is taxable when there is a transaction of payment between Employer and

employee. Any sum paid directly or indirectly by employer to employee is to be treated as salary

income in the hands of employee (ATO, 2015). At times, in big companies and multi- nationals,

in order to keep the reputation of the concerns, the employer, apart from Salary package offers,

many facilities which otherwise the employee would have done as a part of his / her living. For

eg Car, house. These are considered to be fringe benefits which form essential Salary taxable

income. In other words it can be understood that it is a complete salary package which the

employer has offered in terms of company car medical insurance, hospitalisation schemes,

holiday schemes, pension plans, interest free loans, etc. It is not necessary that there has to be an

establishment of Employer and employee relation (ATO, 2015). The fringe benefits could be

passed on between two independent contractors also the recipient of such benefits must consider

fair market value of the benefits so availed as part of their taxable income. Difference countries

have different law framework for taxability of fringe benefit taxation. For eg in India, Fringe

Benefit taxation has been abolished. Some of the exempt category benefits are social security,

medical facilities – hospitalization, Federal unemployment taxes etc.

In Australian republic, Fringe Benefit tax is borne by the employer (ATO, 2015). The Income

Tax Assessment Act has established various provisions relating the chargeability and taxability

of Fringe Benefit Taxation.

In the given case study, the employer has given Car to employee for office to home commuting

or for official purpose.

8

Salary income is taxable when there is a transaction of payment between Employer and

employee. Any sum paid directly or indirectly by employer to employee is to be treated as salary

income in the hands of employee (ATO, 2015). At times, in big companies and multi- nationals,

in order to keep the reputation of the concerns, the employer, apart from Salary package offers,

many facilities which otherwise the employee would have done as a part of his / her living. For

eg Car, house. These are considered to be fringe benefits which form essential Salary taxable

income. In other words it can be understood that it is a complete salary package which the

employer has offered in terms of company car medical insurance, hospitalisation schemes,

holiday schemes, pension plans, interest free loans, etc. It is not necessary that there has to be an

establishment of Employer and employee relation (ATO, 2015). The fringe benefits could be

passed on between two independent contractors also the recipient of such benefits must consider

fair market value of the benefits so availed as part of their taxable income. Difference countries

have different law framework for taxability of fringe benefit taxation. For eg in India, Fringe

Benefit taxation has been abolished. Some of the exempt category benefits are social security,

medical facilities – hospitalization, Federal unemployment taxes etc.

In Australian republic, Fringe Benefit tax is borne by the employer (ATO, 2015). The Income

Tax Assessment Act has established various provisions relating the chargeability and taxability

of Fringe Benefit Taxation.

In the given case study, the employer has given Car to employee for office to home commuting

or for official purpose.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Assuming the car is from the following category:

Sedan / Hatch back car

Utility vehicle which are four wheelers

Passenger car – which can carry fewer than Nine passengers

In certain cases, the Income Tax Assessment Act provides exemption to Fringe Benefit Taxation.

In case the employee uses the vehicle for travelling between home and work; Marketing related

travelling; official tour utility; used for minors

Any usage of car other than the specified purpose amounts to Fringe Benefit (Austaxpbr, 2001).

It is therefore necessary to compute the Fringe benefit. If the employer maintains adequate

records, it can compute fringe benefit on Operating cost method.

Cost of Car = $33000

Repairing Expense= $550 (including GST)

Time when the car was not used for official purpose. 15 days.

Fringe benefit applicable for the 15 days.

Total days in the year when the car was put in use = 336 days. As per the Australian Taxation

office, the year of computation of Fringe benefit is from 1st April to 31st March.

Fringe Benefit (33000+550) x 15 / 336 = $1498

9

Sedan / Hatch back car

Utility vehicle which are four wheelers

Passenger car – which can carry fewer than Nine passengers

In certain cases, the Income Tax Assessment Act provides exemption to Fringe Benefit Taxation.

In case the employee uses the vehicle for travelling between home and work; Marketing related

travelling; official tour utility; used for minors

Any usage of car other than the specified purpose amounts to Fringe Benefit (Austaxpbr, 2001).

It is therefore necessary to compute the Fringe benefit. If the employer maintains adequate

records, it can compute fringe benefit on Operating cost method.

Cost of Car = $33000

Repairing Expense= $550 (including GST)

Time when the car was not used for official purpose. 15 days.

Fringe benefit applicable for the 15 days.

Total days in the year when the car was put in use = 336 days. As per the Australian Taxation

office, the year of computation of Fringe benefit is from 1st April to 31st March.

Fringe Benefit (33000+550) x 15 / 336 = $1498

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fringe benefit taxation is attracted in case an employer disburses a loan to employee and charges

lower rate of interest or no interest. Lower rate of interest can be construed as that rate which is

lower than the statutory pre-defined rate of interest. i.e. Bank rate which can be termed as

Benchmark rate.

It is necessary to understand the nature and purpose of usage of loan. An advance salary forms

part of Loan to employee and falls under the purview of Fringe benefit taxation.

Fringe benefit can be computed as under

Difference between statutory interest rate as prevailing in the market which could be fixed by the

Apex Bank or the Prime lending rate offered by nationalized bank; and the Actual interest that

will be accrued from the employee.

Employer has given a loan of $500000 to Emma which is used to purchase private asset for

$450000 and shares $50000 by husband. Both are solely used for the personal use. Fringe benefit

can be extended to the family of the employee also. Hence the benefit in this case was easily

diverted to the husband of the employee. This forms part of taxation to the employer. Had the

shares been purchased by Emma (Employee) the same would have been included in Income

Generating Asset. Hence in this case, no interest on loan benefit can be allowed as deduction to

the Fringe Benefit.

Fringe Benefit for Loan = $500000 x 213 / 366 = $290984

10

lower rate of interest or no interest. Lower rate of interest can be construed as that rate which is

lower than the statutory pre-defined rate of interest. i.e. Bank rate which can be termed as

Benchmark rate.

It is necessary to understand the nature and purpose of usage of loan. An advance salary forms

part of Loan to employee and falls under the purview of Fringe benefit taxation.

Fringe benefit can be computed as under

Difference between statutory interest rate as prevailing in the market which could be fixed by the

Apex Bank or the Prime lending rate offered by nationalized bank; and the Actual interest that

will be accrued from the employee.

Employer has given a loan of $500000 to Emma which is used to purchase private asset for

$450000 and shares $50000 by husband. Both are solely used for the personal use. Fringe benefit

can be extended to the family of the employee also. Hence the benefit in this case was easily

diverted to the husband of the employee. This forms part of taxation to the employer. Had the

shares been purchased by Emma (Employee) the same would have been included in Income

Generating Asset. Hence in this case, no interest on loan benefit can be allowed as deduction to

the Fringe Benefit.

Fringe Benefit for Loan = $500000 x 213 / 366 = $290984

10

Employer deals in Trading of Bathtubs. Trade price of bath tub for general public is $2600.

Discount given to Emma (Employee) is $1300. Cost price is not to be considered. The

opportunity lost is the benefit provided to the employer.

Fringe Benefit in this case is $1300

Had the shares purchased by Emma herself. The Interest cost (500000 x 4.5% * 213/366) x

50000/500000 shall be deductible from the Fringe Benefit.

i.e. $13094

Net Fringe Benefit = 290984 – 13094 = $277890.

The taxation of fringe benefit was started to compensate the revenue authorities from the Tax

planning done by big companies. The companies used to offer salary packaging which included

less of a Salary and more of Fringe Benefits. The Fringe benefits were owned by the Company

and the same were claimed as Depreciation. Whereas the Employee received less salary and filed

lower Return of income. The Government, identified the revenue leakage and introduced the

Fringe Benefit taxation which was imposed on the Employer for administrative convenience. It is

a kind of Tax deduction at source. On non compliance of the provisions, the company is liable

for all interests and penal provisions. It is essential for all the employers and employees to

document the bills and supportive which shall form relevant records for filing the fringe benefit

return. In case the company wants to claim any allowable deduction in payment of fringe benefit,

11

Discount given to Emma (Employee) is $1300. Cost price is not to be considered. The

opportunity lost is the benefit provided to the employer.

Fringe Benefit in this case is $1300

Had the shares purchased by Emma herself. The Interest cost (500000 x 4.5% * 213/366) x

50000/500000 shall be deductible from the Fringe Benefit.

i.e. $13094

Net Fringe Benefit = 290984 – 13094 = $277890.

The taxation of fringe benefit was started to compensate the revenue authorities from the Tax

planning done by big companies. The companies used to offer salary packaging which included

less of a Salary and more of Fringe Benefits. The Fringe benefits were owned by the Company

and the same were claimed as Depreciation. Whereas the Employee received less salary and filed

lower Return of income. The Government, identified the revenue leakage and introduced the

Fringe Benefit taxation which was imposed on the Employer for administrative convenience. It is

a kind of Tax deduction at source. On non compliance of the provisions, the company is liable

for all interests and penal provisions. It is essential for all the employers and employees to

document the bills and supportive which shall form relevant records for filing the fringe benefit

return. In case the company wants to claim any allowable deduction in payment of fringe benefit,

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.