Taxation Theory, Practice, and Law: Capital Gains Tax Analysis Report

VerifiedAdded on 2020/10/23

|12

|3527

|254

Report

AI Summary

This report delves into Australian taxation practices, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). It begins with a detailed analysis of CGT, examining the purchase and sale of various assets including land, an antique bed, a painting, shares, and a violin, providing calculations to determine the taxable capital gains for each. The report then explores the FBT implications of a company-provided car. The analysis includes relevant tax rulings, acts, and regulations from the Australian Taxation Office (ATO), offering a clear framework for understanding and calculating tax liabilities. The report also touches upon assessing the income of a couple residing in Australia. The report concludes with a summary of findings and references used.

TAXATION THEORY, PRACTICE &

LAW

LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Measuring the capital gain tax in the income tax...................................................................1

QUESTION 2...................................................................................................................................7

Measuring the liabilities if FBT in respects with relevant information..................................7

Analysing income of husband and wife.................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Measuring the capital gain tax in the income tax...................................................................1

QUESTION 2...................................................................................................................................7

Measuring the liabilities if FBT in respects with relevant information..................................7

Analysing income of husband and wife.................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

Taxation practices in analysing the assessable income and net tax will be payable by an

industry or an individual is necessary. Thus, net worth of any concern has to be taxed with

proper analysis and measurements. In the present report, there will be discussion based on capital

gain tax analysis as well as assessment income of couple resident in Australia. However, this

report will bring various measurement and determination of taxes on the basis of tax rulings, acts

and regulations enacted by Australian Taxation Office (ATO). A clear demonstration of all

calculations and analysis will bring information relevant with authentic framework of such

regulatory.

QUESTION 1

Measuring the capital gain tax in the income tax

Capital Gain Tax: The purchase and sale of any asset is basically reflecting differences in

amount. Thus, such variations will reflect positive or negative outcomes determines capital gain

of loss incurred on such property (Sowa and et.al., 2018). However, it will be measured and

analysed in income tax returns of an individual. It will directly add in assessable income of a

person which will significantly raises tax (Lawrence and Bennett, 2017). Moreover, in the below

listed analysis there have been various assets which were being bought and sold by an individual.

Thus, there will be measurement of capital gain tax to analyse the taxes which are needed to be

payable by them (White and Townsend, 2018). The analysis of CGT on various assets such as

Block of vacant land, Antique bed, Painting, shares and Violin is as follows.

Particulars Amount in($)

Vacant block of land

Purchase price of vacant block 100000

add: local council 20000

cost base unindexed 120000

Sale of land 320000

less: cost base unindexed 120000

440000

With provision of 1 sept. 1999 discount will be

applicable as per reducing the 50% cost of asset in

taxation 220000

Capital gain 220000

1

Taxation practices in analysing the assessable income and net tax will be payable by an

industry or an individual is necessary. Thus, net worth of any concern has to be taxed with

proper analysis and measurements. In the present report, there will be discussion based on capital

gain tax analysis as well as assessment income of couple resident in Australia. However, this

report will bring various measurement and determination of taxes on the basis of tax rulings, acts

and regulations enacted by Australian Taxation Office (ATO). A clear demonstration of all

calculations and analysis will bring information relevant with authentic framework of such

regulatory.

QUESTION 1

Measuring the capital gain tax in the income tax

Capital Gain Tax: The purchase and sale of any asset is basically reflecting differences in

amount. Thus, such variations will reflect positive or negative outcomes determines capital gain

of loss incurred on such property (Sowa and et.al., 2018). However, it will be measured and

analysed in income tax returns of an individual. It will directly add in assessable income of a

person which will significantly raises tax (Lawrence and Bennett, 2017). Moreover, in the below

listed analysis there have been various assets which were being bought and sold by an individual.

Thus, there will be measurement of capital gain tax to analyse the taxes which are needed to be

payable by them (White and Townsend, 2018). The analysis of CGT on various assets such as

Block of vacant land, Antique bed, Painting, shares and Violin is as follows.

Particulars Amount in($)

Vacant block of land

Purchase price of vacant block 100000

add: local council 20000

cost base unindexed 120000

Sale of land 320000

less: cost base unindexed 120000

440000

With provision of 1 sept. 1999 discount will be

applicable as per reducing the 50% cost of asset in

taxation 220000

Capital gain 220000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: In analyzing the profitability retained by individual in context with the

purchase and sale of various assets. Thus, Block of vacant land has been bought by him in 2001.

Similarly, it has been sold at the cost of $320000. To determine the effective capital gain tax

amount, there will be determination of various techniques and implication of such aspects will be

helpful in bringing the qualitative analysis. However, as per considering the three norms which

are being enacted in CGT analysis such as after 1985, 1999 and within 12 months. Therefore,

land was purchased in 2001 on which discounting technique were has to be implicated that states

50% of the Capital gain or loss will be charged. Moreover, there capital gain taxable here will

be$220000.

Antique Bed:

Particulars Amount in($)

Antique bed

Purchase price of antique bed 3500

Add: alteration cost 1500

Add: amount of household content 11000

cost base unindexed 16000

sale of bed 25000

less: cost base unindexed 16000

9000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 4500

Interpretation: As per analyzing the above listed determination of operation which

ascertains that there has been measurement of capital gain tax on Antique Bed which were

bought by an individual. The purchase costs of the bed in 1986 was $3500 on which a minor

alternation has been made amounted to $1500. Similarly, the insurance claim has been made by

owner with respect with the bed on which they have agreed on bringing $11000 as an insurance

claim. Moreover, here the cost base unindexed has been measured as $16000. The bed was sold

for $25000 which in total brings the total capital gain of $9000. As per considering the

discounting technique on which there have been charges levied on 50% of the total gains such as

$4500 will be taxable.

2

purchase and sale of various assets. Thus, Block of vacant land has been bought by him in 2001.

Similarly, it has been sold at the cost of $320000. To determine the effective capital gain tax

amount, there will be determination of various techniques and implication of such aspects will be

helpful in bringing the qualitative analysis. However, as per considering the three norms which

are being enacted in CGT analysis such as after 1985, 1999 and within 12 months. Therefore,

land was purchased in 2001 on which discounting technique were has to be implicated that states

50% of the Capital gain or loss will be charged. Moreover, there capital gain taxable here will

be$220000.

Antique Bed:

Particulars Amount in($)

Antique bed

Purchase price of antique bed 3500

Add: alteration cost 1500

Add: amount of household content 11000

cost base unindexed 16000

sale of bed 25000

less: cost base unindexed 16000

9000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 4500

Interpretation: As per analyzing the above listed determination of operation which

ascertains that there has been measurement of capital gain tax on Antique Bed which were

bought by an individual. The purchase costs of the bed in 1986 was $3500 on which a minor

alternation has been made amounted to $1500. Similarly, the insurance claim has been made by

owner with respect with the bed on which they have agreed on bringing $11000 as an insurance

claim. Moreover, here the cost base unindexed has been measured as $16000. The bed was sold

for $25000 which in total brings the total capital gain of $9000. As per considering the

discounting technique on which there have been charges levied on 50% of the total gains such as

$4500 will be taxable.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Painting:

Painting

Particulars Amount in($)

Purchase price of Painting 2000

Cost base unindexed 2000

Sale of painting 125000

Less: cost base unindexed 2000

123000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 61500

Interpretation: In consideration with the above listed analysis which insist capital gain

tax will be charged on painting there have been obtained by an individual for $2000. However,

the cost base unindexed will be same as there has been no additional cost incurred in purchase of

painting. On the other side, it was sold for $125000 on which unindexed cost base has been

reduces which determines that total capital gain of $123000. Thus, with reference to the CGT

provision of 1st September, 1999 that determines discount of 50% for CGT which brings the

outcomes as $61500.

Share:

Shares

Particulars

Details

(In $)

Amount

(In $)

Common bank shares purchased 1000*15 15000

Add: Stamp duty on cost of purchase 750

cost base unindexed 15750

Sale of shares 1000*47 47000

Add: Brokerage fees on sales 550

less: Cost base Unindexed 15750

31800

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 15900

PHB share purchased 2500*12 30000

Add: Stamp duty on cost of purchase 500

cost base unindexed 30500

Sale of shares 2500*25 62500

3

Painting

Particulars Amount in($)

Purchase price of Painting 2000

Cost base unindexed 2000

Sale of painting 125000

Less: cost base unindexed 2000

123000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 61500

Interpretation: In consideration with the above listed analysis which insist capital gain

tax will be charged on painting there have been obtained by an individual for $2000. However,

the cost base unindexed will be same as there has been no additional cost incurred in purchase of

painting. On the other side, it was sold for $125000 on which unindexed cost base has been

reduces which determines that total capital gain of $123000. Thus, with reference to the CGT

provision of 1st September, 1999 that determines discount of 50% for CGT which brings the

outcomes as $61500.

Share:

Shares

Particulars

Details

(In $)

Amount

(In $)

Common bank shares purchased 1000*15 15000

Add: Stamp duty on cost of purchase 750

cost base unindexed 15750

Sale of shares 1000*47 47000

Add: Brokerage fees on sales 550

less: Cost base Unindexed 15750

31800

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 15900

PHB share purchased 2500*12 30000

Add: Stamp duty on cost of purchase 500

cost base unindexed 30500

Sale of shares 2500*25 62500

3

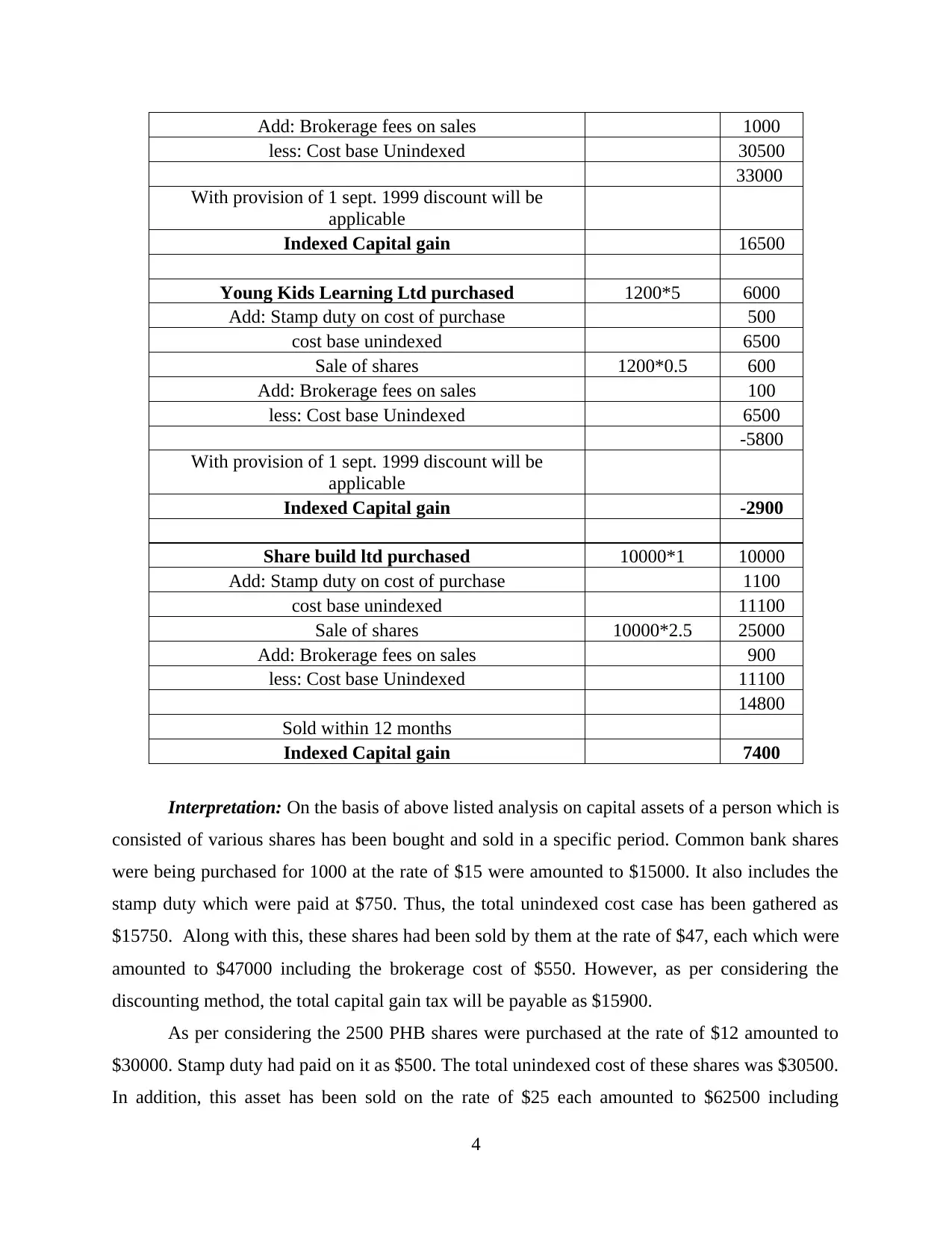

Add: Brokerage fees on sales 1000

less: Cost base Unindexed 30500

33000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 16500

Young Kids Learning Ltd purchased 1200*5 6000

Add: Stamp duty on cost of purchase 500

cost base unindexed 6500

Sale of shares 1200*0.5 600

Add: Brokerage fees on sales 100

less: Cost base Unindexed 6500

-5800

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain -2900

Share build ltd purchased 10000*1 10000

Add: Stamp duty on cost of purchase 1100

cost base unindexed 11100

Sale of shares 10000*2.5 25000

Add: Brokerage fees on sales 900

less: Cost base Unindexed 11100

14800

Sold within 12 months

Indexed Capital gain 7400

Interpretation: On the basis of above listed analysis on capital assets of a person which is

consisted of various shares has been bought and sold in a specific period. Common bank shares

were being purchased for 1000 at the rate of $15 were amounted to $15000. It also includes the

stamp duty which were paid at $750. Thus, the total unindexed cost case has been gathered as

$15750. Along with this, these shares had been sold by them at the rate of $47, each which were

amounted to $47000 including the brokerage cost of $550. However, as per considering the

discounting method, the total capital gain tax will be payable as $15900.

As per considering the 2500 PHB shares were purchased at the rate of $12 amounted to

$30000. Stamp duty had paid on it as $500. The total unindexed cost of these shares was $30500.

In addition, this asset has been sold on the rate of $25 each amounted to $62500 including

4

less: Cost base Unindexed 30500

33000

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 16500

Young Kids Learning Ltd purchased 1200*5 6000

Add: Stamp duty on cost of purchase 500

cost base unindexed 6500

Sale of shares 1200*0.5 600

Add: Brokerage fees on sales 100

less: Cost base Unindexed 6500

-5800

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain -2900

Share build ltd purchased 10000*1 10000

Add: Stamp duty on cost of purchase 1100

cost base unindexed 11100

Sale of shares 10000*2.5 25000

Add: Brokerage fees on sales 900

less: Cost base Unindexed 11100

14800

Sold within 12 months

Indexed Capital gain 7400

Interpretation: On the basis of above listed analysis on capital assets of a person which is

consisted of various shares has been bought and sold in a specific period. Common bank shares

were being purchased for 1000 at the rate of $15 were amounted to $15000. It also includes the

stamp duty which were paid at $750. Thus, the total unindexed cost case has been gathered as

$15750. Along with this, these shares had been sold by them at the rate of $47, each which were

amounted to $47000 including the brokerage cost of $550. However, as per considering the

discounting method, the total capital gain tax will be payable as $15900.

As per considering the 2500 PHB shares were purchased at the rate of $12 amounted to

$30000. Stamp duty had paid on it as $500. The total unindexed cost of these shares was $30500.

In addition, this asset has been sold on the rate of $25 each amounted to $62500 including

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

brokerage fees of $1000. Moreover, there have been reduction of cost base unindexed amount of

$30500 which were reduced to have the total capital of asset as $33000. Considering discounting

approach in it which will ascertains that 50% of asset will be taxed in capital gain tax such as

$16500.

In relation with 1200 shares of Young Kids Learning Ltd which were being purchased for

$5 each amounted to $6000. Therefore, it includes the stamp duty of $500 which presents the

total cost based unindexed as $6500. On the other side, these shares were sold at the rate of $0.5

which can be demonstrated as a loss in this capital asset. These shares amounted to $600 along

with the brokerage fees of $100. However, the total capital loss has been analyzed as -$5800 on

which 50% will be taxable such as $2900.

By considering the capital asset bought by individual such as 10000 marketable securities

of Share Build Ltd at $1 of rate which is amounted to $10000 along with its stamp duty as a cost

on purchase amounted to $1100. Therefore, unindexed cost base of data base is $11100. Thus,

sales of these shares were at the rate of $2.5 each which has been amounted to $25000 including

brokerage fee of $900 on sales has been charged which brings the total capital gain of $14800.

Thus, these are the shares which have been sold within 12 months of period it includes the stamp

duty paid by client on the purchase of these shares such as $1100. This together ascertains the

Cost base unindexed as $11100. Moreover, there have been sale of these securities at the rate of

$2.5 with additional brokerage fees of 900. In addition, there has been reduction of Unindexed

cost base which brings the total gains as $14800. The overall capital gain on this security was

$7400.

Violin

Particulars

Amount

(in $)

Violin Purchased 5500

cost base unindexed 5500

Sale of Violin 12000

less: Cost base unindexed 5500

6500

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 3250

5

$30500 which were reduced to have the total capital of asset as $33000. Considering discounting

approach in it which will ascertains that 50% of asset will be taxed in capital gain tax such as

$16500.

In relation with 1200 shares of Young Kids Learning Ltd which were being purchased for

$5 each amounted to $6000. Therefore, it includes the stamp duty of $500 which presents the

total cost based unindexed as $6500. On the other side, these shares were sold at the rate of $0.5

which can be demonstrated as a loss in this capital asset. These shares amounted to $600 along

with the brokerage fees of $100. However, the total capital loss has been analyzed as -$5800 on

which 50% will be taxable such as $2900.

By considering the capital asset bought by individual such as 10000 marketable securities

of Share Build Ltd at $1 of rate which is amounted to $10000 along with its stamp duty as a cost

on purchase amounted to $1100. Therefore, unindexed cost base of data base is $11100. Thus,

sales of these shares were at the rate of $2.5 each which has been amounted to $25000 including

brokerage fee of $900 on sales has been charged which brings the total capital gain of $14800.

Thus, these are the shares which have been sold within 12 months of period it includes the stamp

duty paid by client on the purchase of these shares such as $1100. This together ascertains the

Cost base unindexed as $11100. Moreover, there have been sale of these securities at the rate of

$2.5 with additional brokerage fees of 900. In addition, there has been reduction of Unindexed

cost base which brings the total gains as $14800. The overall capital gain on this security was

$7400.

Violin

Particulars

Amount

(in $)

Violin Purchased 5500

cost base unindexed 5500

Sale of Violin 12000

less: Cost base unindexed 5500

6500

With provision of 1 sept. 1999 discount will be

applicable

Indexed Capital gain 3250

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: On the basis of above listed table which insist that, Violin was being

purchased on cost of 5500 and sold for 12000. There has been a capital gain of 6500 which was

discounted at 50%. Thus, capital gain tax will be levied on $3250 of total gains.

Particulars

Amount

(in$)

Block Vacant land 220000

Antique bed 4500

Painting 61500

shares

Common bank shares 15900

PHB Iron Ore 16500

Young Kids Learning Ltd -2900

share build ltd 7400

Violin 3250

Total capital gains 326150

Less: Provision of previous year's capital loss 8500

Less: Attribute to the sale of sculpture 1500

Net capital gain 316150

Marginal tax rate 45% 142268

Tax payable on Regime 142268

Interpretation: The above listed table demonstrates overall capital gains and losses were

obtained by the owner in a period. Block of vacant land was at $220000, Antique bed as $4500,

Painting as $61500, Common Bank shares as $15900, PHB as $16500, Young Kids learning Ltd

as -$2900, share build ltd as $74000, Violin as $3250. Therefore, the total capital gains after

reducing the loss was $326150. In addition, there was a previous year balance which was

negative as -$8500 along with the attribute of amount based on sales of a sculpture amounted to

$1500. As per adjusting previous year arrears, net capital gain has been obtained by owner as

$316150. The marginal rate of tax at 45% was being charged on these assets which brings total

tax will be payable by owner is $142268.

QUESTION 2

Measuring the liabilities if FBT in respects with relevant information

Car:

6

purchased on cost of 5500 and sold for 12000. There has been a capital gain of 6500 which was

discounted at 50%. Thus, capital gain tax will be levied on $3250 of total gains.

Particulars

Amount

(in$)

Block Vacant land 220000

Antique bed 4500

Painting 61500

shares

Common bank shares 15900

PHB Iron Ore 16500

Young Kids Learning Ltd -2900

share build ltd 7400

Violin 3250

Total capital gains 326150

Less: Provision of previous year's capital loss 8500

Less: Attribute to the sale of sculpture 1500

Net capital gain 316150

Marginal tax rate 45% 142268

Tax payable on Regime 142268

Interpretation: The above listed table demonstrates overall capital gains and losses were

obtained by the owner in a period. Block of vacant land was at $220000, Antique bed as $4500,

Painting as $61500, Common Bank shares as $15900, PHB as $16500, Young Kids learning Ltd

as -$2900, share build ltd as $74000, Violin as $3250. Therefore, the total capital gains after

reducing the loss was $326150. In addition, there was a previous year balance which was

negative as -$8500 along with the attribute of amount based on sales of a sculpture amounted to

$1500. As per adjusting previous year arrears, net capital gain has been obtained by owner as

$316150. The marginal rate of tax at 45% was being charged on these assets which brings total

tax will be payable by owner is $142268.

QUESTION 2

Measuring the liabilities if FBT in respects with relevant information

Car:

6

As per considering the consequences incurred that, Jasmin was awarded a car for travelling

by Rapid heat Pty Ltd. It will come under legislative influences of Fringe benefits tax

Assessment act, 1986 (Burkhauser, Hahn and Wilkins, 2018). Therefore, with the influences of

the section 7 of this act, which ascertains the time of purchasing the car, cost and total kilometres

it was travelled (Burns, 2018). Moreover, in analysing the FBT benefits will be awarded to

Jasmine which were analysed as per the travel made by car in period and rate is proposed in

norms of FBT act.

Particulars

Amount

(in $)

Car valued at 33000

Statutory FBT rate which

were being implied on car 26%

Period of car using 335-5

330

FBT will be payable as 7757.26

Interpretation: By considering the above listed analysis of FBT benefits of Jasmine on the

car has been determined. Car was valued at $33000. Thus, the car was being travelled only

10000 km which insist the rate of 26%. This rate has been levied on cost on the basis of tax

threshold presented by FBTA, such as vehicle which was travelled less than 15000 km will be

charged on 26%. Moreover, in a year the total days are 365 on which 10 days the car is not in use

as it Jasmin moves out of station. Along with this 5 days were deducted as the car is being

unused due to annual repairs etc. In analysing the FBT will be payable By Jasmine on the car is

$7757.26 which will be charged in her taxable income for the year.

Loan:

Fringe benefits which were being levied with respect of loan provided to Jasmine for

personal use. However, the loan of $500000 was taken by her on which 450000 was used for

purchasing the holiday home (Harding and Marten, 2018). Additionally, the $50000 was being

lent by her to her husband on which he had purchased some shares of Telstra. With respect to

FBTA act, that determines the amount of loan that will be used in purchasing securities which in

turn bring the dividend gain to a person will be deductible and exempted. However, these are

gains which are being allowed to a person in the income tax assessment act of Australia (Loan

Fringe Benefits Tax (FBT) Policy, 2018). It is because of interest on loan will be charged on

7

by Rapid heat Pty Ltd. It will come under legislative influences of Fringe benefits tax

Assessment act, 1986 (Burkhauser, Hahn and Wilkins, 2018). Therefore, with the influences of

the section 7 of this act, which ascertains the time of purchasing the car, cost and total kilometres

it was travelled (Burns, 2018). Moreover, in analysing the FBT benefits will be awarded to

Jasmine which were analysed as per the travel made by car in period and rate is proposed in

norms of FBT act.

Particulars

Amount

(in $)

Car valued at 33000

Statutory FBT rate which

were being implied on car 26%

Period of car using 335-5

330

FBT will be payable as 7757.26

Interpretation: By considering the above listed analysis of FBT benefits of Jasmine on the

car has been determined. Car was valued at $33000. Thus, the car was being travelled only

10000 km which insist the rate of 26%. This rate has been levied on cost on the basis of tax

threshold presented by FBTA, such as vehicle which was travelled less than 15000 km will be

charged on 26%. Moreover, in a year the total days are 365 on which 10 days the car is not in use

as it Jasmin moves out of station. Along with this 5 days were deducted as the car is being

unused due to annual repairs etc. In analysing the FBT will be payable By Jasmine on the car is

$7757.26 which will be charged in her taxable income for the year.

Loan:

Fringe benefits which were being levied with respect of loan provided to Jasmine for

personal use. However, the loan of $500000 was taken by her on which 450000 was used for

purchasing the holiday home (Harding and Marten, 2018). Additionally, the $50000 was being

lent by her to her husband on which he had purchased some shares of Telstra. With respect to

FBTA act, that determines the amount of loan that will be used in purchasing securities which in

turn bring the dividend gain to a person will be deductible and exempted. However, these are

gains which are being allowed to a person in the income tax assessment act of Australia (Loan

Fringe Benefits Tax (FBT) Policy, 2018). It is because of interest on loan will be charged on

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amount which were being obtained by a person. Similarly, with this respect, it can be said that

Jasmine’s husband will use amount of loan in purchasing equity assets. In respect with the same,

the loan was awarded to her by her employer on which it is required that the employee must

provide a document of declaration which will bring the clear analysis on the loan is being

obtained for personal use (Fettes and Butler, 2017).

Considering the operational requirement on which it can be said that, securities obtained by

her husband will be deductible in the analysis as there will not be any taxable charges on such

amount. Along with this, she is paying 4.25% of amount as interest on such loan, which are the

payments already made by her in respect with the loan cannot be charged in income tax

assessment. Thus, in this respect, there will be not any other taxable payment made by her on the

loan.

Electric heaters:

Particulars

Amount

(in $)

Electric heaters manufactured by

Rapid heat 1300

Manufacture cost 700

Sold for 2600

Cots base unindexed 2000

Sale 2600

Less: Cost base unindexed 2000

Total gains 600

FBT rate 47% 282

Interpretation: On the basis of above table where, Jasmine had purchased Electric heaters

from Rapid Heat amounted to $1300 along with the manufacturing cost of $700. Therefore, the

total cost of that heater was $2000 that sold by Jasmine at price of $2600. Thus, $600 has been

gained by her. In consideration with the current charges and tax rates imposed by ATO on FBT

is 47% on goods. Thus, Jasmine has to pay tax on this heater as $282.

Analysing income of husband and wife

Particulars Amount

8

Jasmine’s husband will use amount of loan in purchasing equity assets. In respect with the same,

the loan was awarded to her by her employer on which it is required that the employee must

provide a document of declaration which will bring the clear analysis on the loan is being

obtained for personal use (Fettes and Butler, 2017).

Considering the operational requirement on which it can be said that, securities obtained by

her husband will be deductible in the analysis as there will not be any taxable charges on such

amount. Along with this, she is paying 4.25% of amount as interest on such loan, which are the

payments already made by her in respect with the loan cannot be charged in income tax

assessment. Thus, in this respect, there will be not any other taxable payment made by her on the

loan.

Electric heaters:

Particulars

Amount

(in $)

Electric heaters manufactured by

Rapid heat 1300

Manufacture cost 700

Sold for 2600

Cots base unindexed 2000

Sale 2600

Less: Cost base unindexed 2000

Total gains 600

FBT rate 47% 282

Interpretation: On the basis of above table where, Jasmine had purchased Electric heaters

from Rapid Heat amounted to $1300 along with the manufacturing cost of $700. Therefore, the

total cost of that heater was $2000 that sold by Jasmine at price of $2600. Thus, $600 has been

gained by her. In consideration with the current charges and tax rates imposed by ATO on FBT

is 47% on goods. Thus, Jasmine has to pay tax on this heater as $282.

Analysing income of husband and wife

Particulars Amount

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(In $)

FBT tax rate will be 4.25%-3.5%

estimates 0.75

50000*0.75%*212/365 217.81

Interpretation: In relation with the proposed case on which it can be said that, the

amount $50000 will be used by Jasmine for purchasing shares. Thus, as per considering the

norms where she need to make any taxable payment in the income tax payments made by her.

Thus, with this respect, there will be estimated that the rate of 3.5% will be charged in against

interest rate of loan of 4.25%. Moreover, rate has been analysed as 0.75. Thus, the overall FBT

will be payable by her in this respect is $217.81.

CONCLUSION

On the basis of above report, it can be said that, implication of various law, acts, norms

and regulation will be beneficial in soothing the taxation system in a country. This report is

consisted, with CGT application on various assets that were being obtained by an owner and had

been sold in the relevant period. Along with this, there were adjustments on loans taken by

Jasmine from her employer on which FBT taxes were analysed. Further, the analysis of all taxes

were on the basis of making proper operational determination.

9

FBT tax rate will be 4.25%-3.5%

estimates 0.75

50000*0.75%*212/365 217.81

Interpretation: In relation with the proposed case on which it can be said that, the

amount $50000 will be used by Jasmine for purchasing shares. Thus, as per considering the

norms where she need to make any taxable payment in the income tax payments made by her.

Thus, with this respect, there will be estimated that the rate of 3.5% will be charged in against

interest rate of loan of 4.25%. Moreover, rate has been analysed as 0.75. Thus, the overall FBT

will be payable by her in this respect is $217.81.

CONCLUSION

On the basis of above report, it can be said that, implication of various law, acts, norms

and regulation will be beneficial in soothing the taxation system in a country. This report is

consisted, with CGT application on various assets that were being obtained by an owner and had

been sold in the relevant period. Along with this, there were adjustments on loans taken by

Jasmine from her employer on which FBT taxes were analysed. Further, the analysis of all taxes

were on the basis of making proper operational determination.

9

REFERENCES

Books and Journals

Burkhauser, R. V., Hahn, M. H. and Wilkins, R., 2018. Transitioning from an Historical to a

Contemporary Use of Tax Record Data for Measuring Top Incomes in

Australia.Economic Papers: A journal of applied economics and policy. 37(2). pp.113-

145.

Burns, A., 2018. Options in succession planning for a family business. Taxation in

Australia. 52(10). p.543.

Fettes, W. and Butler, D., 2017. Superanuation: Understanding ECPI in view of super

reforms. Taxation in Australia. 51(11). p.626.

Harding, M. and Marten, M., 2018. Statutory tax rates on dividends, interest and capital gains.

Lawrence, S. and Bennett, M., 2017. Image rights in Australia: Fair game or foul ball? Taxation

in Australia. 51(9). p.487.

Sowa, P. M. and et.al., 2018. Private health insurance incentives in Australia: in search of cost-

effective adjustments. Applied health economics and health policy. 16(1). pp.31-41.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia. 52(11). p.608.

Online

Loan Fringe Benefits Tax (FBT) Policy. 2018. [Online]. Available through: <

http://www.finserv.uwa.edu.au/tax/fbt/policy/loan>.

10

Books and Journals

Burkhauser, R. V., Hahn, M. H. and Wilkins, R., 2018. Transitioning from an Historical to a

Contemporary Use of Tax Record Data for Measuring Top Incomes in

Australia.Economic Papers: A journal of applied economics and policy. 37(2). pp.113-

145.

Burns, A., 2018. Options in succession planning for a family business. Taxation in

Australia. 52(10). p.543.

Fettes, W. and Butler, D., 2017. Superanuation: Understanding ECPI in view of super

reforms. Taxation in Australia. 51(11). p.626.

Harding, M. and Marten, M., 2018. Statutory tax rates on dividends, interest and capital gains.

Lawrence, S. and Bennett, M., 2017. Image rights in Australia: Fair game or foul ball? Taxation

in Australia. 51(9). p.487.

Sowa, P. M. and et.al., 2018. Private health insurance incentives in Australia: in search of cost-

effective adjustments. Applied health economics and health policy. 16(1). pp.31-41.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia. 52(11). p.608.

Online

Loan Fringe Benefits Tax (FBT) Policy. 2018. [Online]. Available through: <

http://www.finserv.uwa.edu.au/tax/fbt/policy/loan>.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.