Taxation Theory, Practice & Law: Capital Gains and FBT Analysis

VerifiedAdded on 2020/11/12

|21

|3285

|273

Homework Assignment

AI Summary

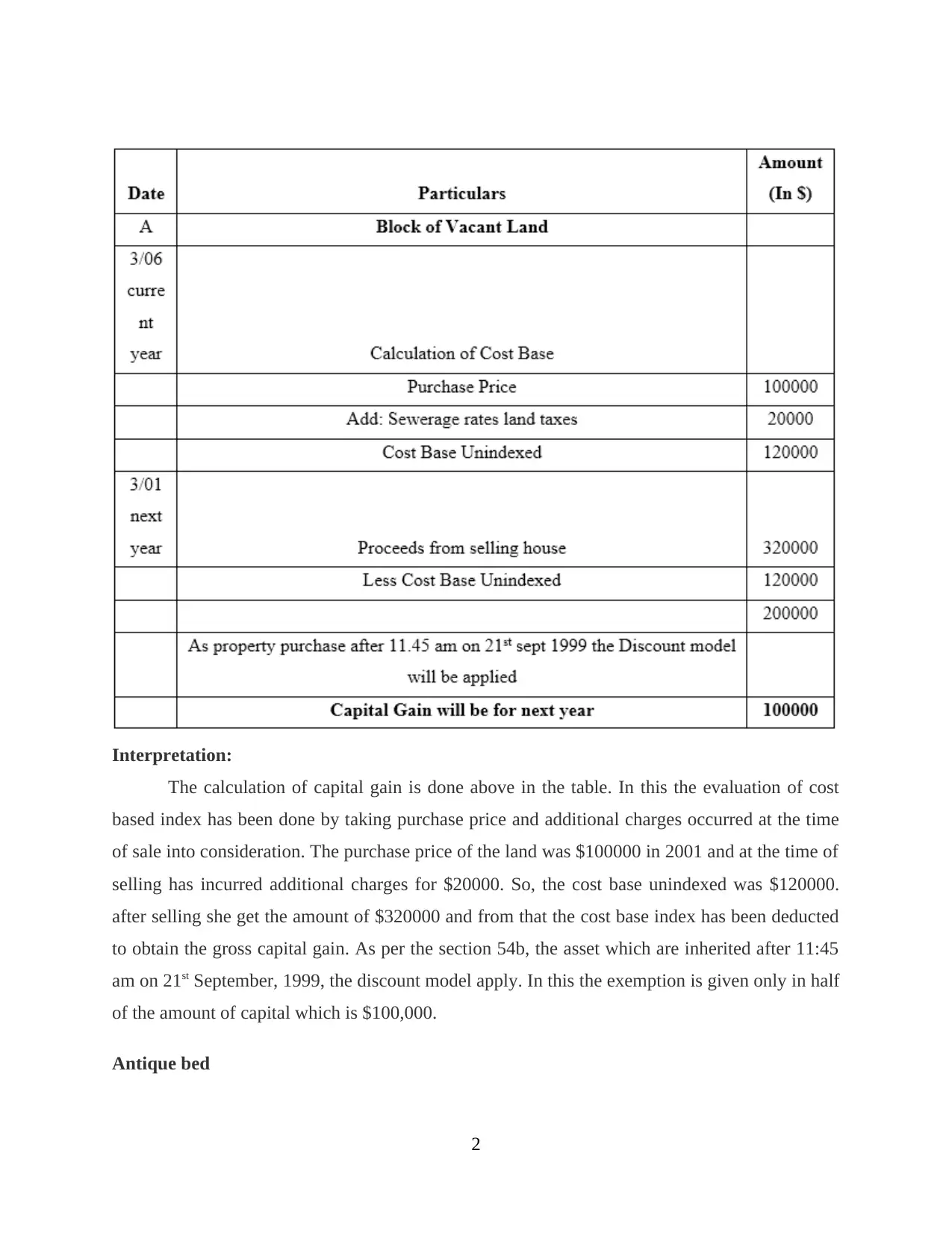

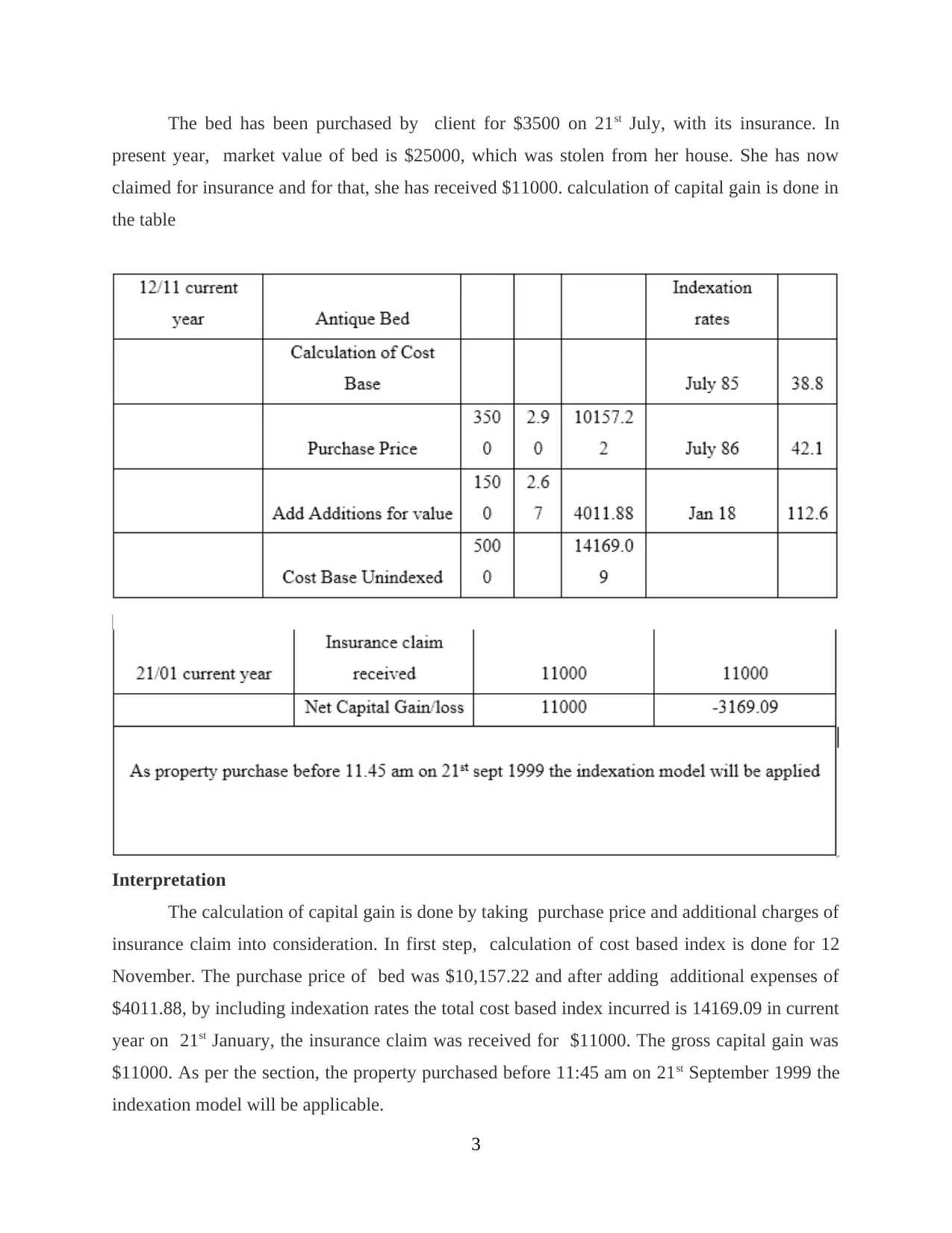

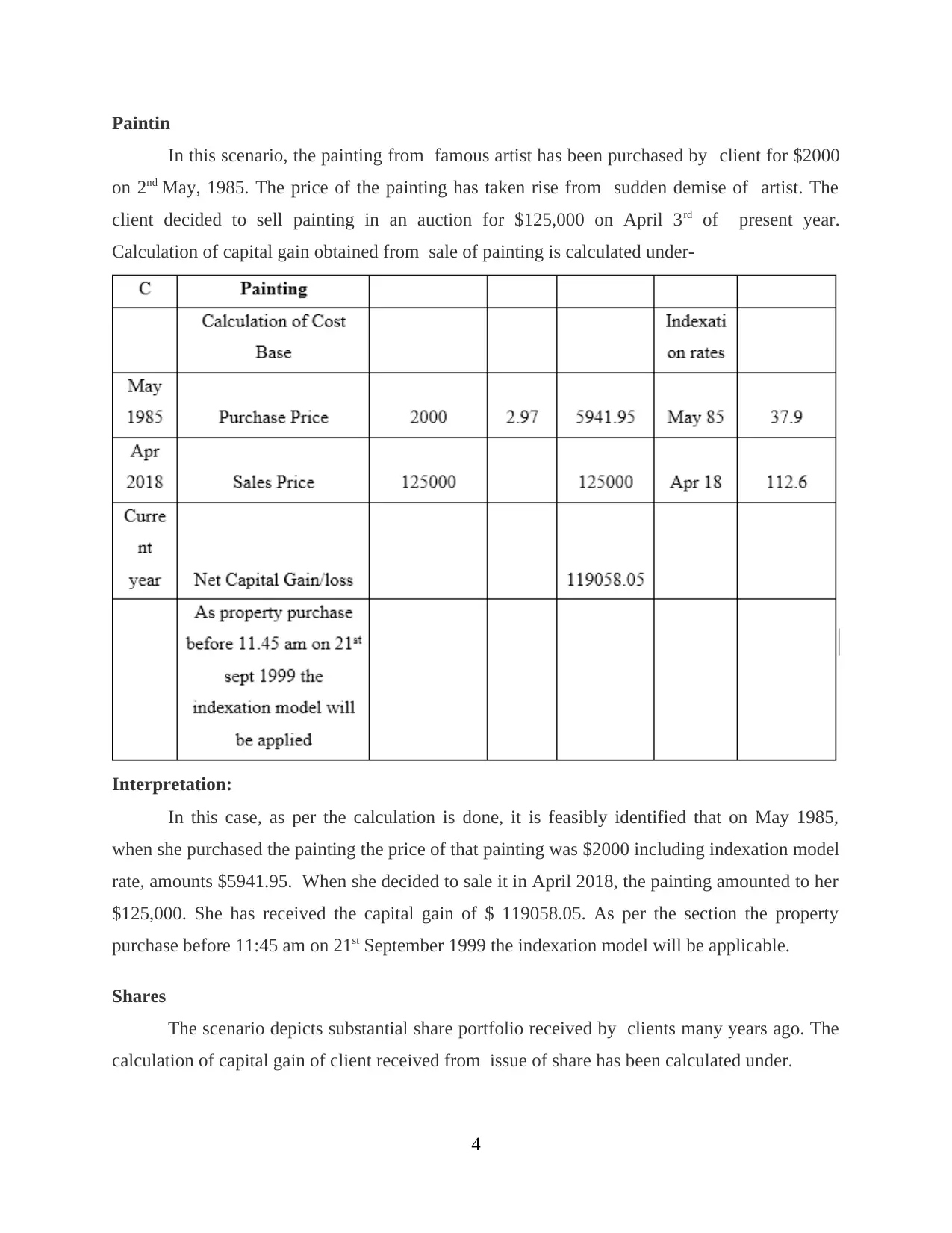

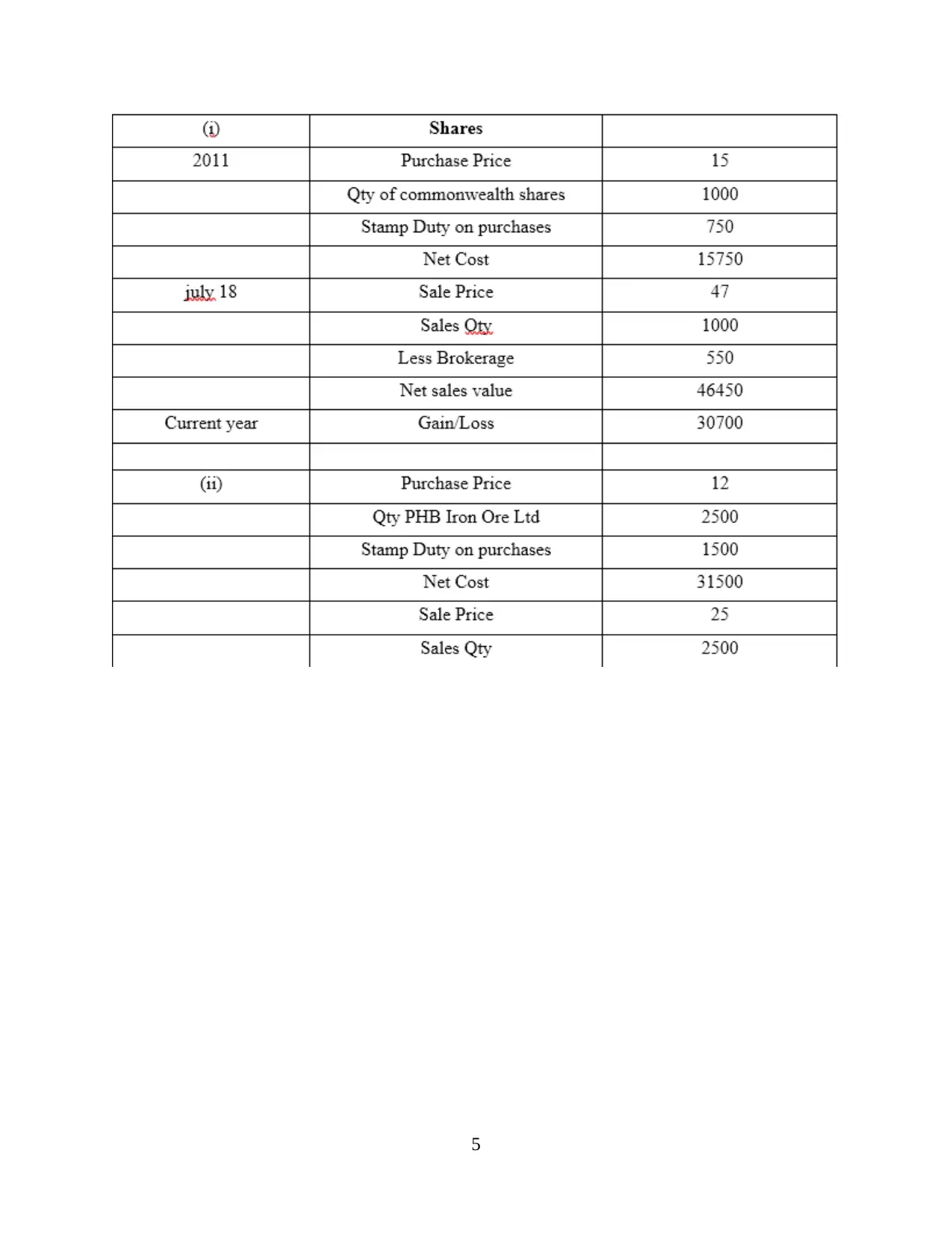

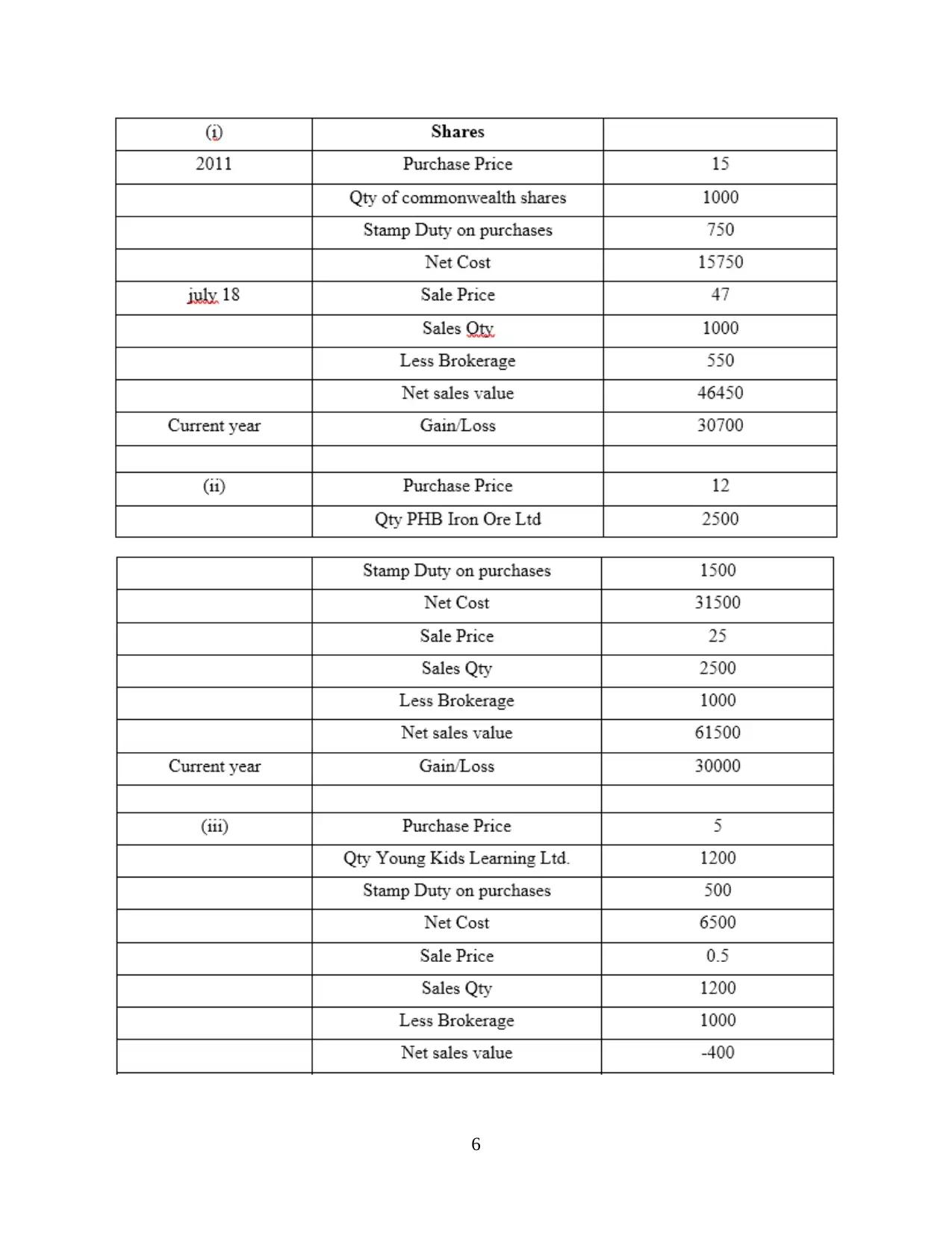

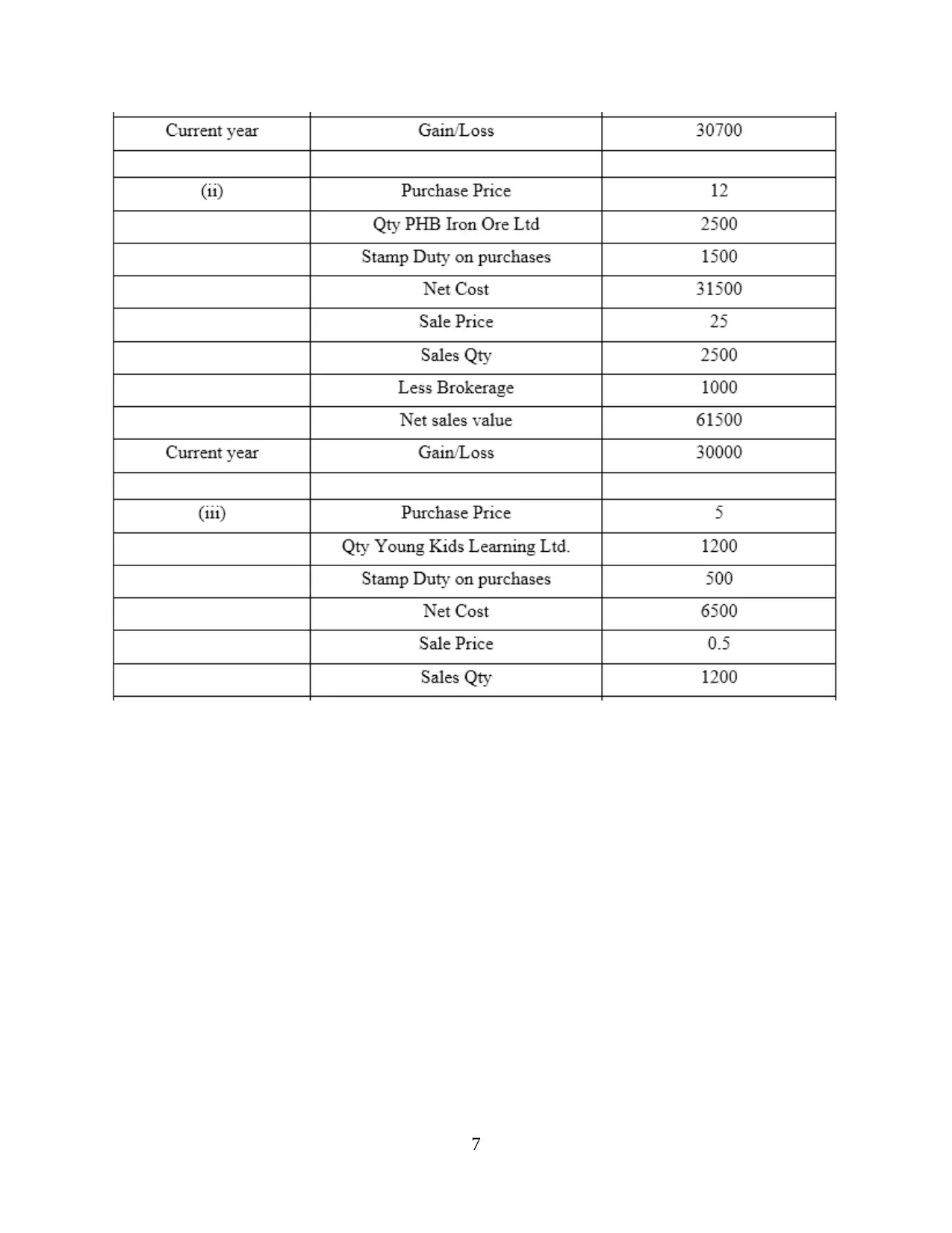

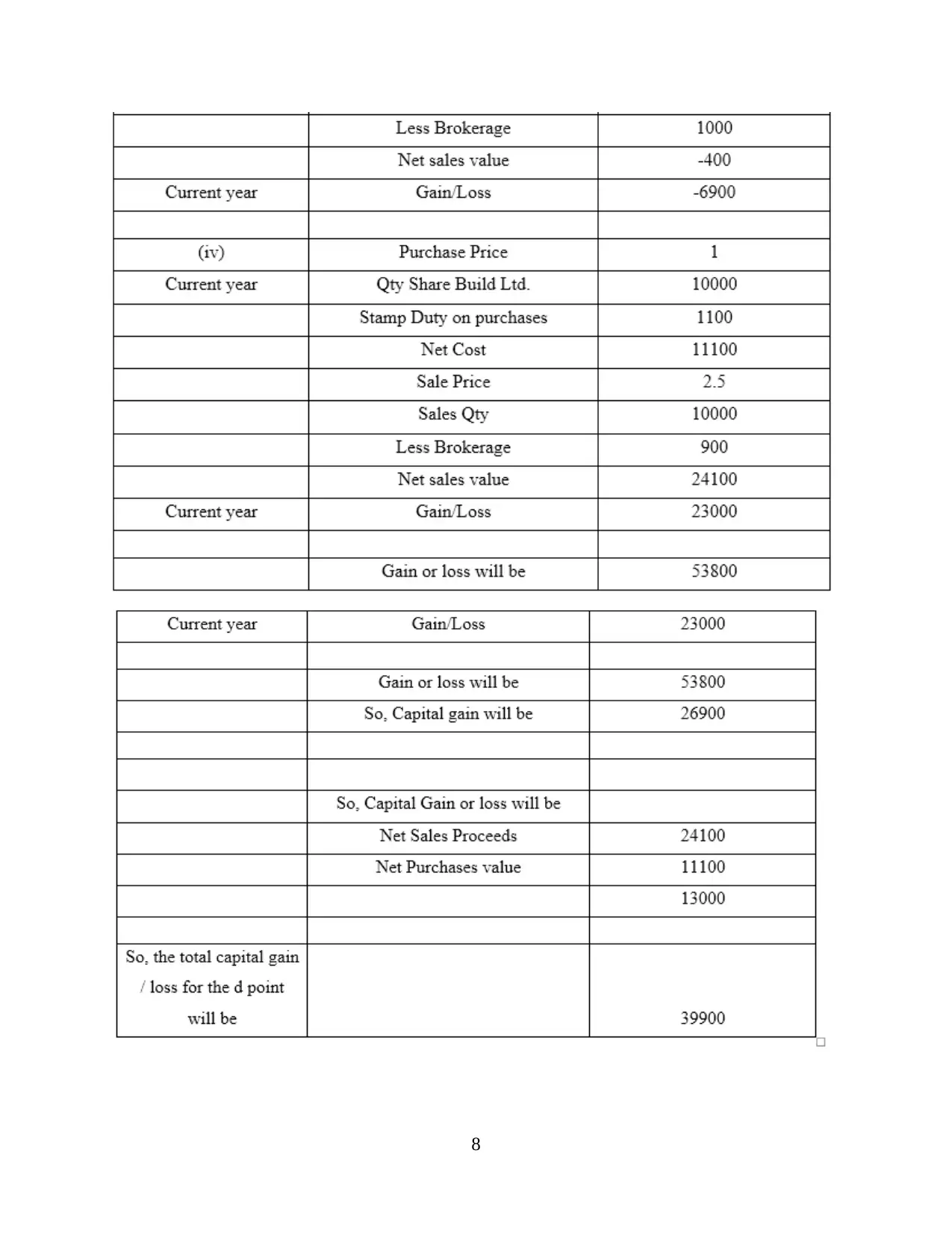

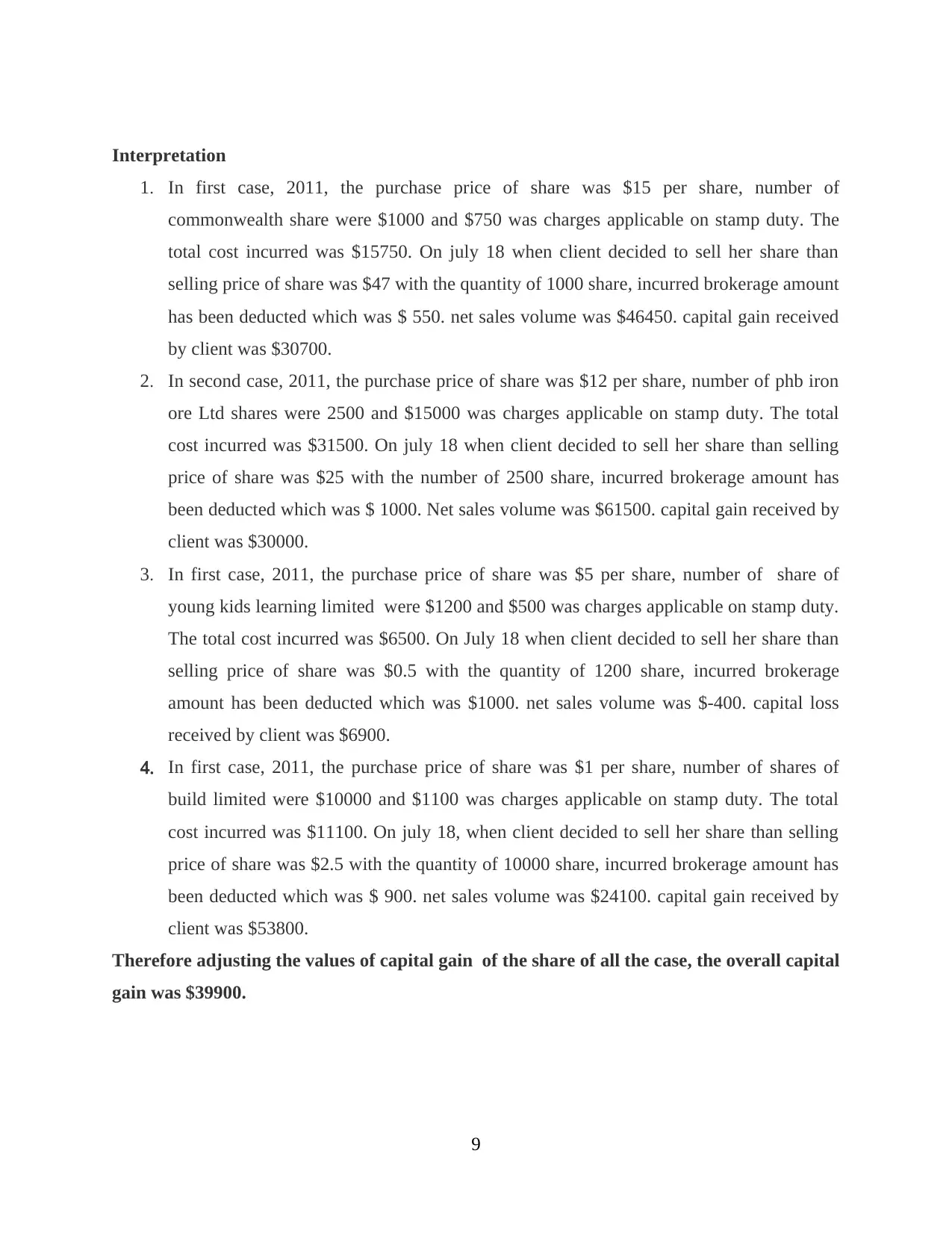

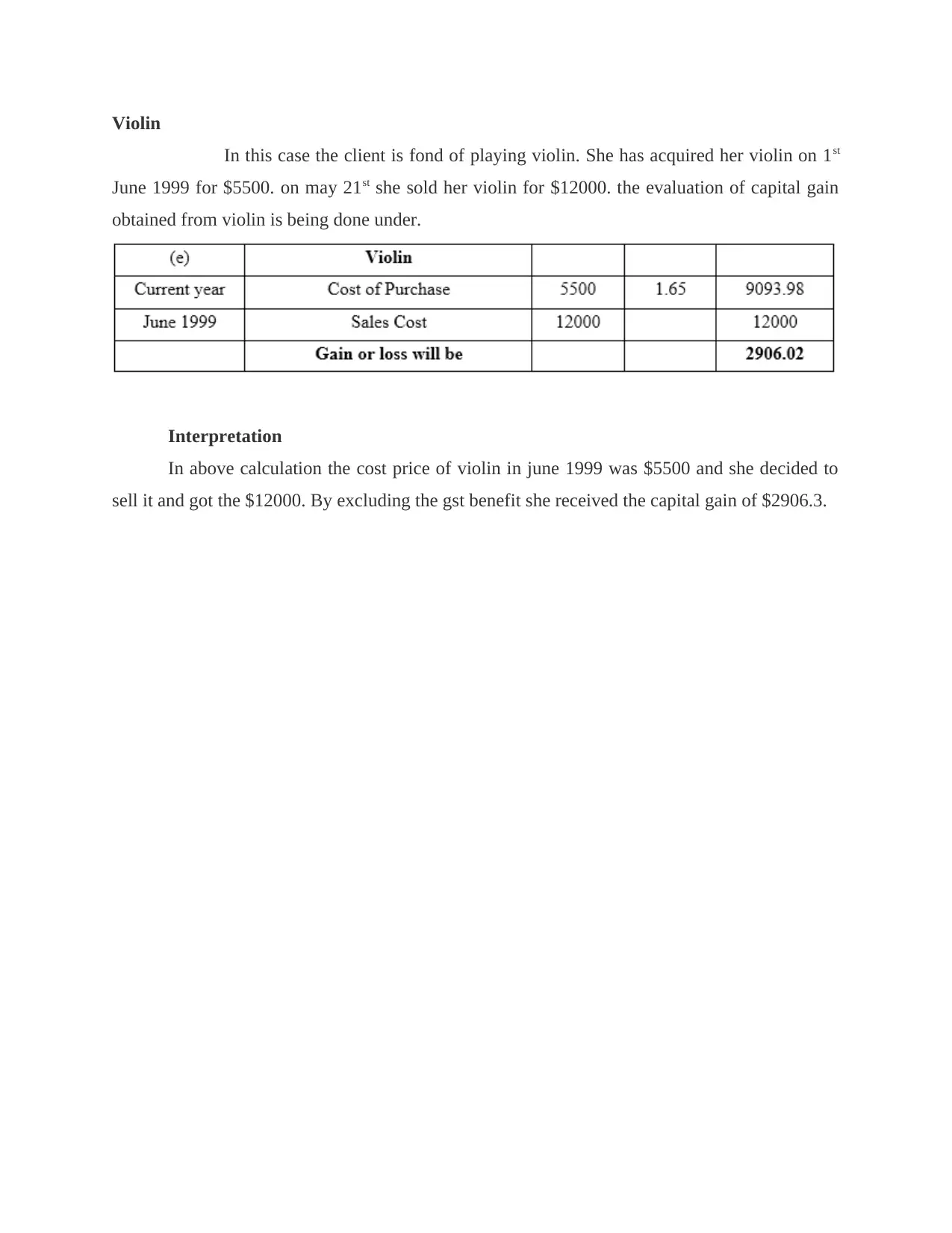

This assignment addresses key concepts in taxation, focusing on capital gains and fringe benefits tax (FBT). It begins by determining the net capital gain of a client, analyzing various assets like vacant land, an antique bed, a painting, shares, and a violin. The calculations consider purchase prices, selling prices, and additional expenses, applying relevant tax models like the discount and indexation models. The second part of the assignment advises on analyzing FBT for an employee named Jasmine, considering car usage, and calculating the taxable value of fringe benefits. It details the steps for FBT calculation, including statutory formula and operating cost methods, along with a discussion of the pros and cons of offering fringe benefits. The assignment also analyzes the tax consequences of a loan used by Jasmine for purchasing securities, providing a comprehensive overview of taxation principles and their practical application.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.