Taxation Report: Capital Gains, Fringe Benefits, and Tax Strategies

VerifiedAdded on 2020/12/29

|14

|3597

|167

Report

AI Summary

This report provides a comprehensive analysis of taxation in Australia, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). It examines the CGT implications of various assets, including vacant land, an antique bed, paintings, shares, and a violin, detailing purchase prices, sales prices, and the application of indexation and discount models to determine taxable gains or losses. The report also discusses the FBT implications and suggests strategies to minimize taxation costs. The analysis includes specific calculations for each asset, considering relevant legislation and tax provisions, and offers insights into how different asset types are treated under CGT. The report concludes with a summary of the net capital gain for the period, considering both gains and losses from various assets and the offset of capital losses.

TAXATION THEORY, PRCATICE

& LAW

& LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determining the net capital gain of client as on 30 June 2018...............................................1

QUESTION 2...................................................................................................................................2

Advising Jasmine in analysing FBT on various assets...........................................................2

Analysing the tax consequences as per loan amount will be used by Jasmine in purchasing

securities.................................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Determining the net capital gain of client as on 30 June 2018...............................................1

QUESTION 2...................................................................................................................................2

Advising Jasmine in analysing FBT on various assets...........................................................2

Analysing the tax consequences as per loan amount will be used by Jasmine in purchasing

securities.................................................................................................................................4

CONCLUSION................................................................................................................................5

REFERENCES................................................................................................................................6

INTRODUCTION

Taxation law and practices imposed by the legislative authorities in Australia to bring fair

tax operations. There are various taxes, norms and regulation which are imposed on various

segmentation of activities. In the present report, there will be an analysis of capital gains or

losses on different assets on which client will suggest solutions to analyse their taxable income.

Along with this, there will be a discussion based on analysing fringe benefit tax with influence of

FBTA Act, 1986. Moreover, individual will be suggested various ways of reducing taxation costs

and implicate alternative solutions for resolving taxable issues for smooth functioning and

overall impact on the company’s growth.

QUESTION 1

Determining the net capital gain of client as on 30 June 2018

For analysing gains obtained by client on the basis of selling various assets. Thus, there has

been legislation based on Capital Gain Tax (CGT). These are taxes which were being levied on

assets at a time of their purchase and sale. Thus, gains retained by owner were analysed on the

basis of period of utilising such asset (Capital Gains Tax, 2018).

In case of selling real estate property and shares, on which capital gains and losses are

listed in income tax return were determined. Therefore, there will be determination of all taxes

that will be helpful in making proper administration of gains and losses. Moreover, with

influence of provision made in 20th September, 1985 which insists that, there will not be any

charges levied on personal assets. Thus, these are exempted in the CGT like, car, Home and

furniture for personal use (McCormack, 2017). There will be no allowances awarded on

depreciation of assets as well as on fittings, or furniture in a rental property (Jacob, 2018).

Similarly, below listed assets and various analysis on the CGT tax has been determined on

several assets including land, shares, bed, violin etc.

Block of Vacant Land

Date Particulars

Amount

(In $)

A Block of Vacant Land

3/06

curre

nt

Calculation of Cost Base

1

Taxation law and practices imposed by the legislative authorities in Australia to bring fair

tax operations. There are various taxes, norms and regulation which are imposed on various

segmentation of activities. In the present report, there will be an analysis of capital gains or

losses on different assets on which client will suggest solutions to analyse their taxable income.

Along with this, there will be a discussion based on analysing fringe benefit tax with influence of

FBTA Act, 1986. Moreover, individual will be suggested various ways of reducing taxation costs

and implicate alternative solutions for resolving taxable issues for smooth functioning and

overall impact on the company’s growth.

QUESTION 1

Determining the net capital gain of client as on 30 June 2018

For analysing gains obtained by client on the basis of selling various assets. Thus, there has

been legislation based on Capital Gain Tax (CGT). These are taxes which were being levied on

assets at a time of their purchase and sale. Thus, gains retained by owner were analysed on the

basis of period of utilising such asset (Capital Gains Tax, 2018).

In case of selling real estate property and shares, on which capital gains and losses are

listed in income tax return were determined. Therefore, there will be determination of all taxes

that will be helpful in making proper administration of gains and losses. Moreover, with

influence of provision made in 20th September, 1985 which insists that, there will not be any

charges levied on personal assets. Thus, these are exempted in the CGT like, car, Home and

furniture for personal use (McCormack, 2017). There will be no allowances awarded on

depreciation of assets as well as on fittings, or furniture in a rental property (Jacob, 2018).

Similarly, below listed assets and various analysis on the CGT tax has been determined on

several assets including land, shares, bed, violin etc.

Block of Vacant Land

Date Particulars

Amount

(In $)

A Block of Vacant Land

3/06

curre

nt

Calculation of Cost Base

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

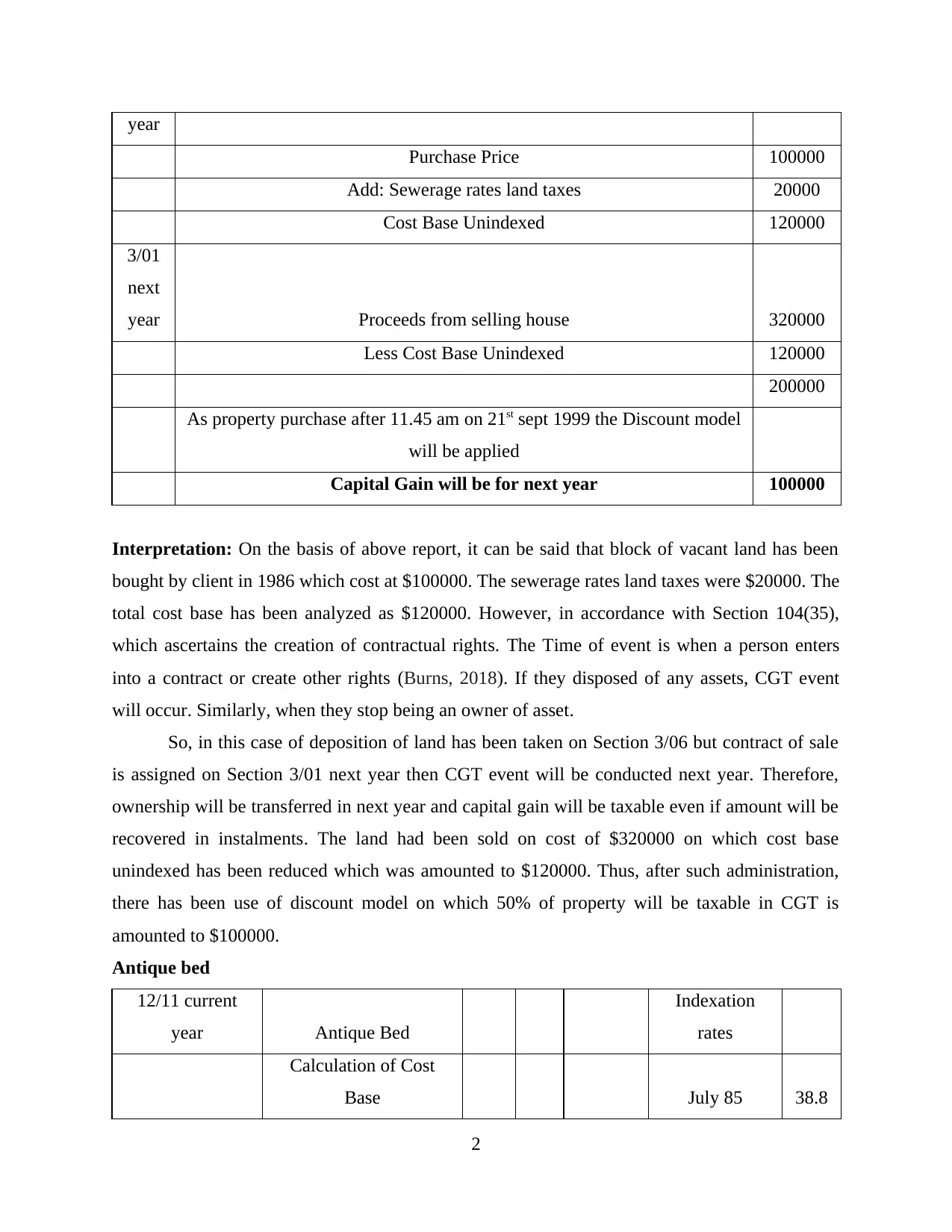

year

Purchase Price 100000

Add: Sewerage rates land taxes 20000

Cost Base Unindexed 120000

3/01

next

year Proceeds from selling house 320000

Less Cost Base Unindexed 120000

200000

As property purchase after 11.45 am on 21st sept 1999 the Discount model

will be applied

Capital Gain will be for next year 100000

Interpretation: On the basis of above report, it can be said that block of vacant land has been

bought by client in 1986 which cost at $100000. The sewerage rates land taxes were $20000. The

total cost base has been analyzed as $120000. However, in accordance with Section 104(35),

which ascertains the creation of contractual rights. The Time of event is when a person enters

into a contract or create other rights (Burns, 2018). If they disposed of any assets, CGT event

will occur. Similarly, when they stop being an owner of asset.

So, in this case of deposition of land has been taken on Section 3/06 but contract of sale

is assigned on Section 3/01 next year then CGT event will be conducted next year. Therefore,

ownership will be transferred in next year and capital gain will be taxable even if amount will be

recovered in instalments. The land had been sold on cost of $320000 on which cost base

unindexed has been reduced which was amounted to $120000. Thus, after such administration,

there has been use of discount model on which 50% of property will be taxable in CGT is

amounted to $100000.

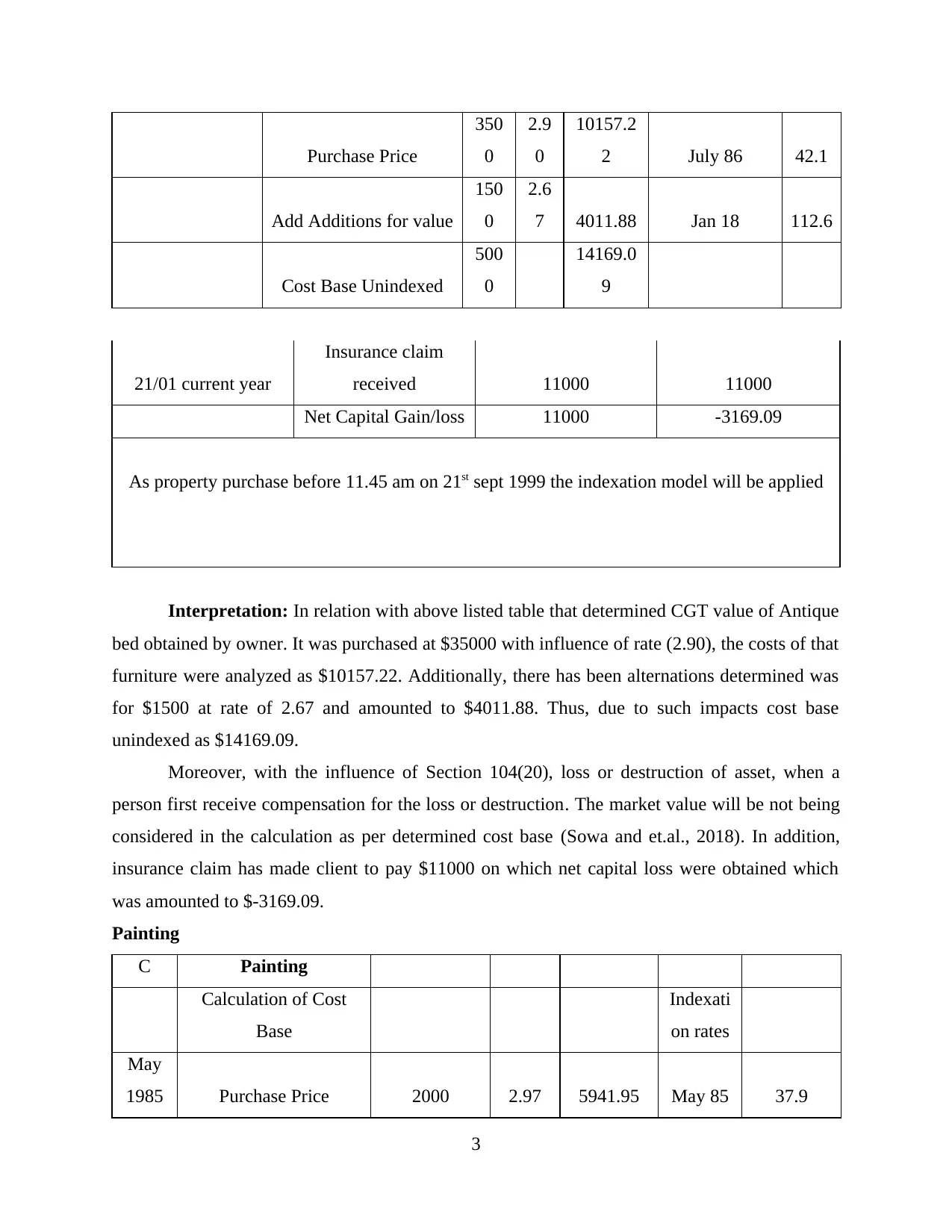

Antique bed

12/11 current

year Antique Bed

Indexation

rates

Calculation of Cost

Base July 85 38.8

2

Purchase Price 100000

Add: Sewerage rates land taxes 20000

Cost Base Unindexed 120000

3/01

next

year Proceeds from selling house 320000

Less Cost Base Unindexed 120000

200000

As property purchase after 11.45 am on 21st sept 1999 the Discount model

will be applied

Capital Gain will be for next year 100000

Interpretation: On the basis of above report, it can be said that block of vacant land has been

bought by client in 1986 which cost at $100000. The sewerage rates land taxes were $20000. The

total cost base has been analyzed as $120000. However, in accordance with Section 104(35),

which ascertains the creation of contractual rights. The Time of event is when a person enters

into a contract or create other rights (Burns, 2018). If they disposed of any assets, CGT event

will occur. Similarly, when they stop being an owner of asset.

So, in this case of deposition of land has been taken on Section 3/06 but contract of sale

is assigned on Section 3/01 next year then CGT event will be conducted next year. Therefore,

ownership will be transferred in next year and capital gain will be taxable even if amount will be

recovered in instalments. The land had been sold on cost of $320000 on which cost base

unindexed has been reduced which was amounted to $120000. Thus, after such administration,

there has been use of discount model on which 50% of property will be taxable in CGT is

amounted to $100000.

Antique bed

12/11 current

year Antique Bed

Indexation

rates

Calculation of Cost

Base July 85 38.8

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Purchase Price

350

0

2.9

0

10157.2

2 July 86 42.1

Add Additions for value

150

0

2.6

7 4011.88 Jan 18 112.6

Cost Base Unindexed

500

0

14169.0

9

21/01 current year

Insurance claim

received 11000 11000

Net Capital Gain/loss 11000 -3169.09

As property purchase before 11.45 am on 21st sept 1999 the indexation model will be applied

Interpretation: In relation with above listed table that determined CGT value of Antique

bed obtained by owner. It was purchased at $35000 with influence of rate (2.90), the costs of that

furniture were analyzed as $10157.22. Additionally, there has been alternations determined was

for $1500 at rate of 2.67 and amounted to $4011.88. Thus, due to such impacts cost base

unindexed as $14169.09.

Moreover, with the influence of Section 104(20), loss or destruction of asset, when a

person first receive compensation for the loss or destruction. The market value will be not being

considered in the calculation as per determined cost base (Sowa and et.al., 2018). In addition,

insurance claim has made client to pay $11000 on which net capital loss were obtained which

was amounted to $-3169.09.

Painting

C Painting

Calculation of Cost

Base

Indexati

on rates

May

1985 Purchase Price 2000 2.97 5941.95 May 85 37.9

3

350

0

2.9

0

10157.2

2 July 86 42.1

Add Additions for value

150

0

2.6

7 4011.88 Jan 18 112.6

Cost Base Unindexed

500

0

14169.0

9

21/01 current year

Insurance claim

received 11000 11000

Net Capital Gain/loss 11000 -3169.09

As property purchase before 11.45 am on 21st sept 1999 the indexation model will be applied

Interpretation: In relation with above listed table that determined CGT value of Antique

bed obtained by owner. It was purchased at $35000 with influence of rate (2.90), the costs of that

furniture were analyzed as $10157.22. Additionally, there has been alternations determined was

for $1500 at rate of 2.67 and amounted to $4011.88. Thus, due to such impacts cost base

unindexed as $14169.09.

Moreover, with the influence of Section 104(20), loss or destruction of asset, when a

person first receive compensation for the loss or destruction. The market value will be not being

considered in the calculation as per determined cost base (Sowa and et.al., 2018). In addition,

insurance claim has made client to pay $11000 on which net capital loss were obtained which

was amounted to $-3169.09.

Painting

C Painting

Calculation of Cost

Base

Indexati

on rates

May

1985 Purchase Price 2000 2.97 5941.95 May 85 37.9

3

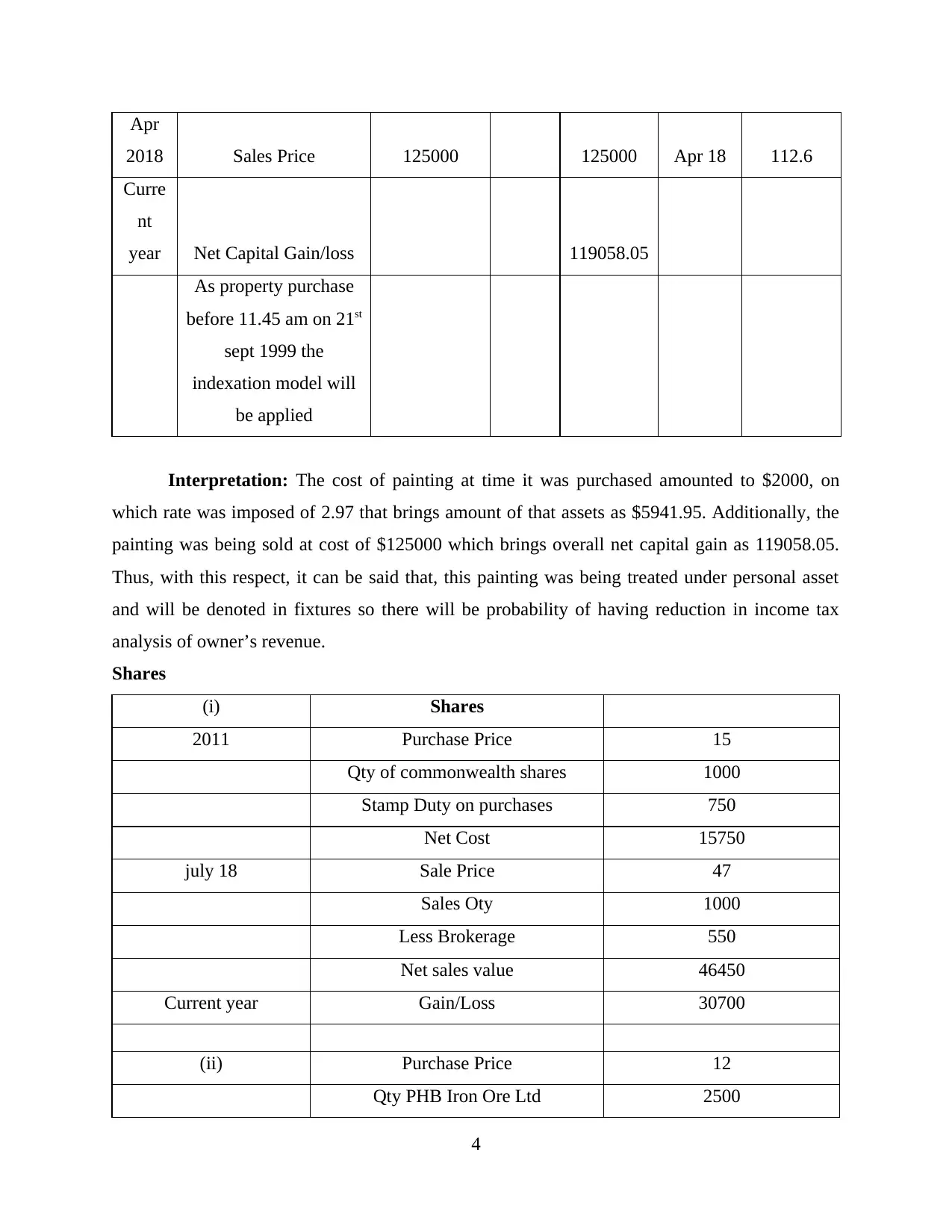

Apr

2018 Sales Price 125000 125000 Apr 18 112.6

Curre

nt

year Net Capital Gain/loss 119058.05

As property purchase

before 11.45 am on 21st

sept 1999 the

indexation model will

be applied

Interpretation: The cost of painting at time it was purchased amounted to $2000, on

which rate was imposed of 2.97 that brings amount of that assets as $5941.95. Additionally, the

painting was being sold at cost of $125000 which brings overall net capital gain as 119058.05.

Thus, with this respect, it can be said that, this painting was being treated under personal asset

and will be denoted in fixtures so there will be probability of having reduction in income tax

analysis of owner’s revenue.

Shares

(i) Shares

2011 Purchase Price 15

Qty of commonwealth shares 1000

Stamp Duty on purchases 750

Net Cost 15750

july 18 Sale Price 47

Sales Oty 1000

Less Brokerage 550

Net sales value 46450

Current year Gain/Loss 30700

(ii) Purchase Price 12

Qty PHB Iron Ore Ltd 2500

4

2018 Sales Price 125000 125000 Apr 18 112.6

Curre

nt

year Net Capital Gain/loss 119058.05

As property purchase

before 11.45 am on 21st

sept 1999 the

indexation model will

be applied

Interpretation: The cost of painting at time it was purchased amounted to $2000, on

which rate was imposed of 2.97 that brings amount of that assets as $5941.95. Additionally, the

painting was being sold at cost of $125000 which brings overall net capital gain as 119058.05.

Thus, with this respect, it can be said that, this painting was being treated under personal asset

and will be denoted in fixtures so there will be probability of having reduction in income tax

analysis of owner’s revenue.

Shares

(i) Shares

2011 Purchase Price 15

Qty of commonwealth shares 1000

Stamp Duty on purchases 750

Net Cost 15750

july 18 Sale Price 47

Sales Oty 1000

Less Brokerage 550

Net sales value 46450

Current year Gain/Loss 30700

(ii) Purchase Price 12

Qty PHB Iron Ore Ltd 2500

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

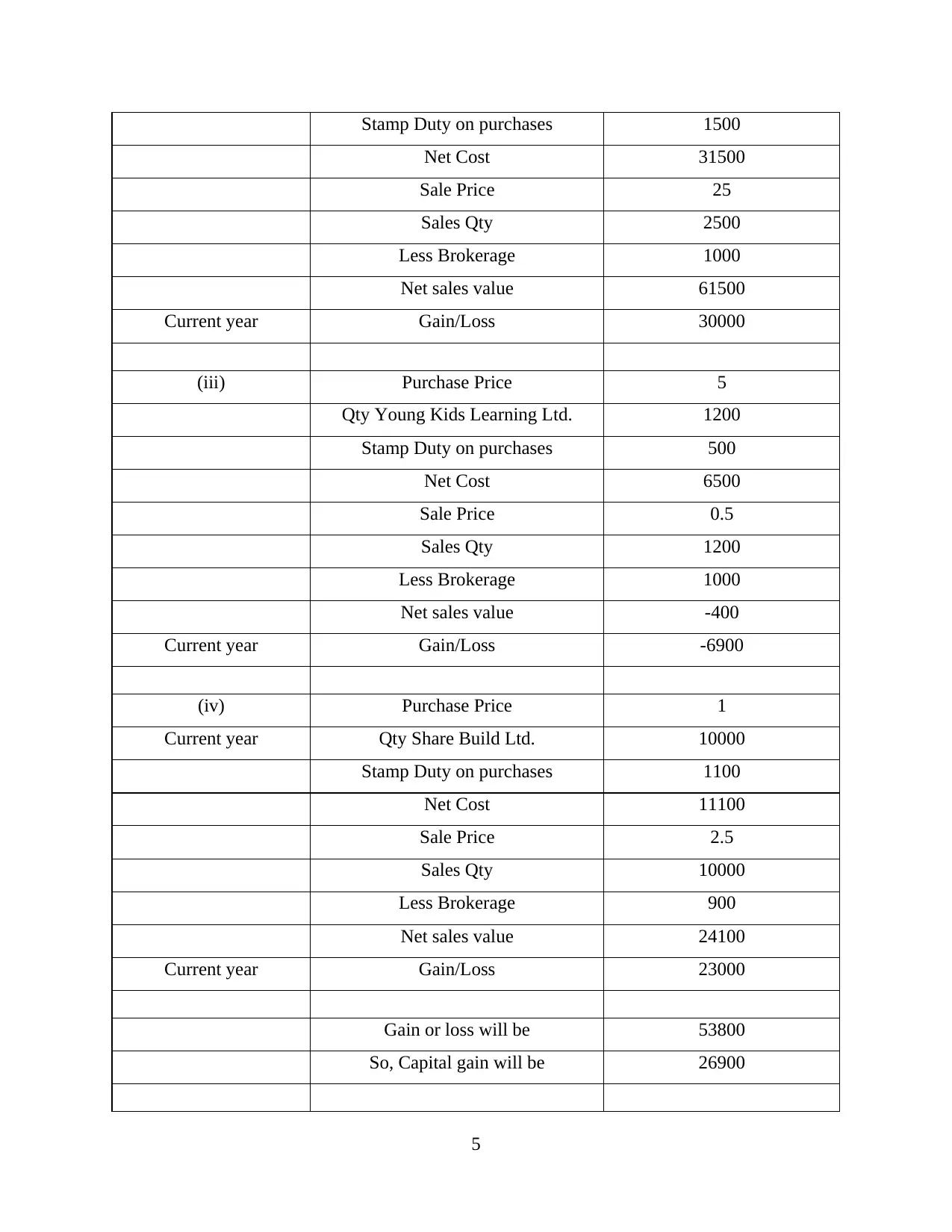

Stamp Duty on purchases 1500

Net Cost 31500

Sale Price 25

Sales Qty 2500

Less Brokerage 1000

Net sales value 61500

Current year Gain/Loss 30000

(iii) Purchase Price 5

Qty Young Kids Learning Ltd. 1200

Stamp Duty on purchases 500

Net Cost 6500

Sale Price 0.5

Sales Qty 1200

Less Brokerage 1000

Net sales value -400

Current year Gain/Loss -6900

(iv) Purchase Price 1

Current year Qty Share Build Ltd. 10000

Stamp Duty on purchases 1100

Net Cost 11100

Sale Price 2.5

Sales Qty 10000

Less Brokerage 900

Net sales value 24100

Current year Gain/Loss 23000

Gain or loss will be 53800

So, Capital gain will be 26900

5

Net Cost 31500

Sale Price 25

Sales Qty 2500

Less Brokerage 1000

Net sales value 61500

Current year Gain/Loss 30000

(iii) Purchase Price 5

Qty Young Kids Learning Ltd. 1200

Stamp Duty on purchases 500

Net Cost 6500

Sale Price 0.5

Sales Qty 1200

Less Brokerage 1000

Net sales value -400

Current year Gain/Loss -6900

(iv) Purchase Price 1

Current year Qty Share Build Ltd. 10000

Stamp Duty on purchases 1100

Net Cost 11100

Sale Price 2.5

Sales Qty 10000

Less Brokerage 900

Net sales value 24100

Current year Gain/Loss 23000

Gain or loss will be 53800

So, Capital gain will be 26900

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

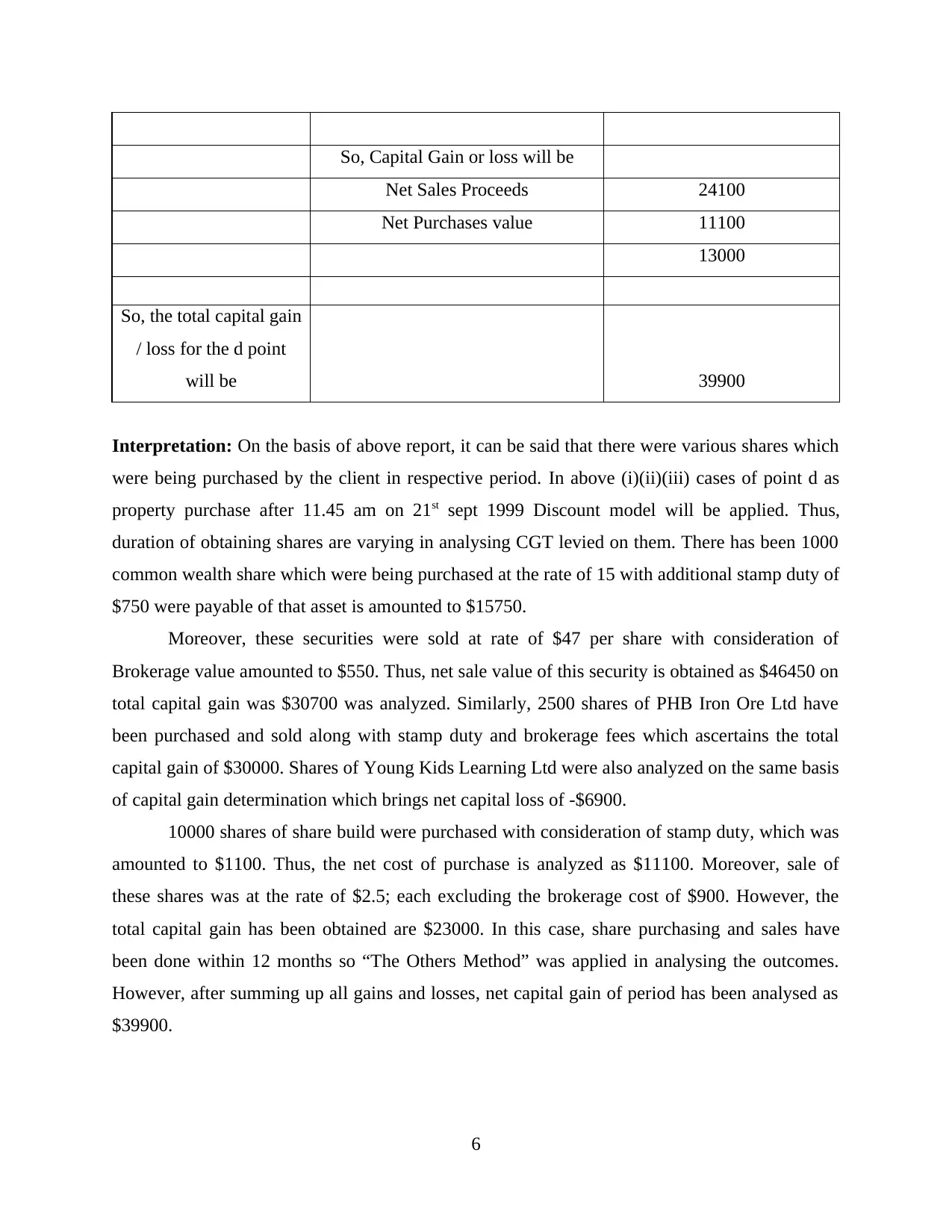

So, Capital Gain or loss will be

Net Sales Proceeds 24100

Net Purchases value 11100

13000

So, the total capital gain

/ loss for the d point

will be 39900

Interpretation: On the basis of above report, it can be said that there were various shares which

were being purchased by the client in respective period. In above (i)(ii)(iii) cases of point d as

property purchase after 11.45 am on 21st sept 1999 Discount model will be applied. Thus,

duration of obtaining shares are varying in analysing CGT levied on them. There has been 1000

common wealth share which were being purchased at the rate of 15 with additional stamp duty of

$750 were payable of that asset is amounted to $15750.

Moreover, these securities were sold at rate of $47 per share with consideration of

Brokerage value amounted to $550. Thus, net sale value of this security is obtained as $46450 on

total capital gain was $30700 was analyzed. Similarly, 2500 shares of PHB Iron Ore Ltd have

been purchased and sold along with stamp duty and brokerage fees which ascertains the total

capital gain of $30000. Shares of Young Kids Learning Ltd were also analyzed on the same basis

of capital gain determination which brings net capital loss of -$6900.

10000 shares of share build were purchased with consideration of stamp duty, which was

amounted to $1100. Thus, the net cost of purchase is analyzed as $11100. Moreover, sale of

these shares was at the rate of $2.5; each excluding the brokerage cost of $900. However, the

total capital gain has been obtained are $23000. In this case, share purchasing and sales have

been done within 12 months so “The Others Method” was applied in analysing the outcomes.

However, after summing up all gains and losses, net capital gain of period has been analysed as

$39900.

6

Net Sales Proceeds 24100

Net Purchases value 11100

13000

So, the total capital gain

/ loss for the d point

will be 39900

Interpretation: On the basis of above report, it can be said that there were various shares which

were being purchased by the client in respective period. In above (i)(ii)(iii) cases of point d as

property purchase after 11.45 am on 21st sept 1999 Discount model will be applied. Thus,

duration of obtaining shares are varying in analysing CGT levied on them. There has been 1000

common wealth share which were being purchased at the rate of 15 with additional stamp duty of

$750 were payable of that asset is amounted to $15750.

Moreover, these securities were sold at rate of $47 per share with consideration of

Brokerage value amounted to $550. Thus, net sale value of this security is obtained as $46450 on

total capital gain was $30700 was analyzed. Similarly, 2500 shares of PHB Iron Ore Ltd have

been purchased and sold along with stamp duty and brokerage fees which ascertains the total

capital gain of $30000. Shares of Young Kids Learning Ltd were also analyzed on the same basis

of capital gain determination which brings net capital loss of -$6900.

10000 shares of share build were purchased with consideration of stamp duty, which was

amounted to $1100. Thus, the net cost of purchase is analyzed as $11100. Moreover, sale of

these shares was at the rate of $2.5; each excluding the brokerage cost of $900. However, the

total capital gain has been obtained are $23000. In this case, share purchasing and sales have

been done within 12 months so “The Others Method” was applied in analysing the outcomes.

However, after summing up all gains and losses, net capital gain of period has been analysed as

$39900.

6

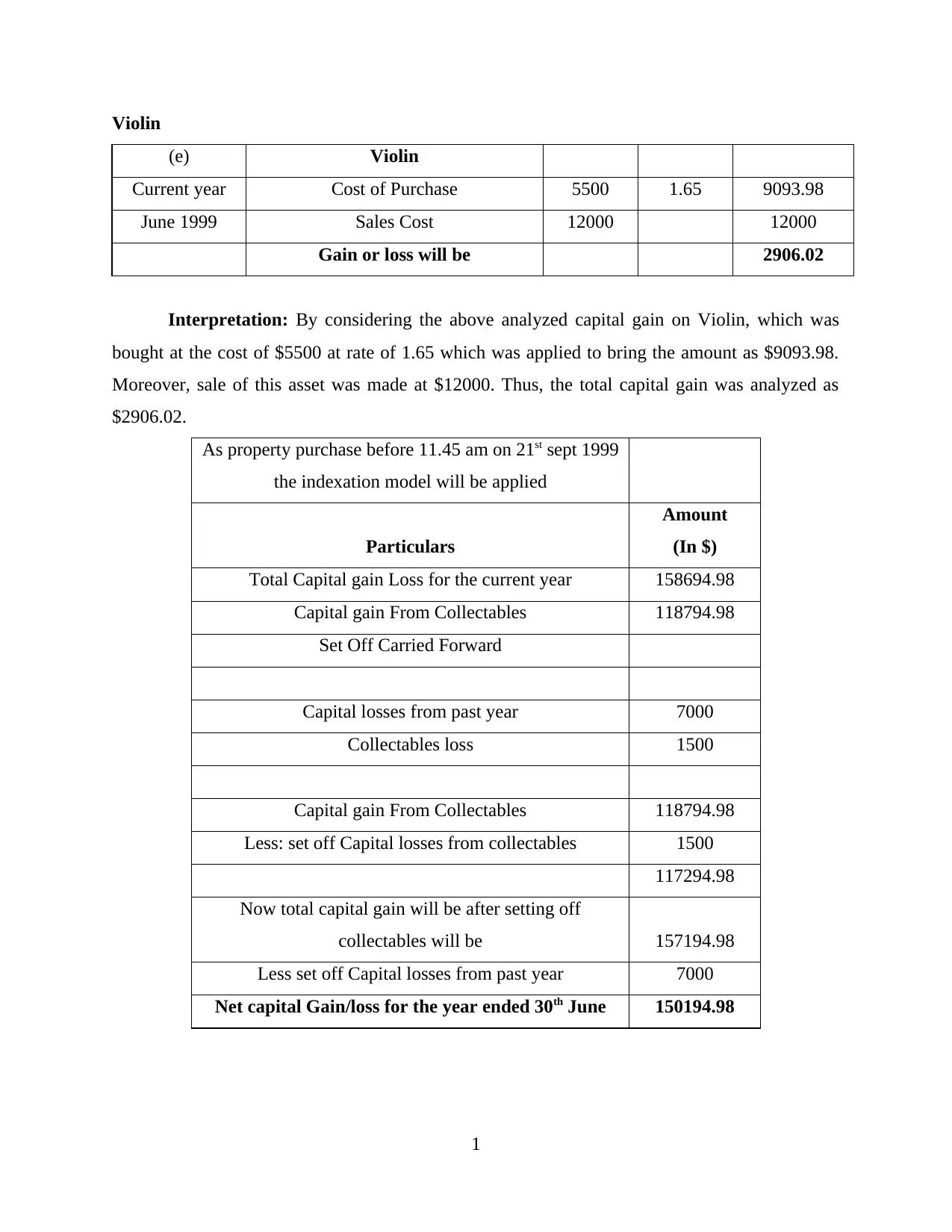

Violin

(e) Violin

Current year Cost of Purchase 5500 1.65 9093.98

June 1999 Sales Cost 12000 12000

Gain or loss will be 2906.02

Interpretation: By considering the above analyzed capital gain on Violin, which was

bought at the cost of $5500 at rate of 1.65 which was applied to bring the amount as $9093.98.

Moreover, sale of this asset was made at $12000. Thus, the total capital gain was analyzed as

$2906.02.

As property purchase before 11.45 am on 21st sept 1999

the indexation model will be applied

Particulars

Amount

(In $)

Total Capital gain Loss for the current year 158694.98

Capital gain From Collectables 118794.98

Set Off Carried Forward

Capital losses from past year 7000

Collectables loss 1500

Capital gain From Collectables 118794.98

Less: set off Capital losses from collectables 1500

117294.98

Now total capital gain will be after setting off

collectables will be 157194.98

Less set off Capital losses from past year 7000

Net capital Gain/loss for the year ended 30th June 150194.98

1

(e) Violin

Current year Cost of Purchase 5500 1.65 9093.98

June 1999 Sales Cost 12000 12000

Gain or loss will be 2906.02

Interpretation: By considering the above analyzed capital gain on Violin, which was

bought at the cost of $5500 at rate of 1.65 which was applied to bring the amount as $9093.98.

Moreover, sale of this asset was made at $12000. Thus, the total capital gain was analyzed as

$2906.02.

As property purchase before 11.45 am on 21st sept 1999

the indexation model will be applied

Particulars

Amount

(In $)

Total Capital gain Loss for the current year 158694.98

Capital gain From Collectables 118794.98

Set Off Carried Forward

Capital losses from past year 7000

Collectables loss 1500

Capital gain From Collectables 118794.98

Less: set off Capital losses from collectables 1500

117294.98

Now total capital gain will be after setting off

collectables will be 157194.98

Less set off Capital losses from past year 7000

Net capital Gain/loss for the year ended 30th June 150194.98

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The total capital gain loss for current year has been analyzed as $158694.98

additionally, gains from collectables as $118794.98 had also been obtained. Moreover, capital

losses from past year are $7000 along with collectable loss as $1500.

However, as per Section 102, losses of collectables will be set of by collectables capital gain

profits so, the capital gains from them were $118794.98 will be deducted from set off capital

losses from these variables as $1500. Thus, it brings an amount as $117294.98 on which the net

capital gain was demonstrated after setting off all collectables were amounted to $157194.98.

Further, there will be reduction of previous year’s set off capital loss of $7000 that brings an

overall net capital gain as $150194.98.

QUESTION 2

Advising Jasmine in analysing FBT on various assets

Car

Rapid Head Pty provided Jasmine a car for traveling purposes. So, it will be calculated

with reference to Fringe Benefit Tax Assessment Act 1986.

As per Section 7 of the FBTA Act where at any time car provided to employee is applied

for private use (Fringe benefits tax, 2018). Section 7(3) of the act suggests that a car will be

treated as private use, when not in premises and parked at employee’s home.

The car has been defined by the act as:

Motor cars, station wagons, vans or any utilities

Other Goods carrying vehicle capacity of less than 1 tone.

Other passengers carrying vehicle carrying less than 9 occupants

As per Section 9 of Act, FBT can be calculated by using two methods:

1. Statutory Method-: Where a person does not show the actual value of cars in gross

taxable value.

2. Cost Method-: Where a person shows the actual value of cars in gross taxable value.

Section 9 also states that any amount paid as an expense with respect to fuel of car, and

repairs if documentary evidence given by the employee in vacant period will be barred by

employer. The car for repairs and maintenance will not be treated under private or personal use

(McLaren, 2017).

2

additionally, gains from collectables as $118794.98 had also been obtained. Moreover, capital

losses from past year are $7000 along with collectable loss as $1500.

However, as per Section 102, losses of collectables will be set of by collectables capital gain

profits so, the capital gains from them were $118794.98 will be deducted from set off capital

losses from these variables as $1500. Thus, it brings an amount as $117294.98 on which the net

capital gain was demonstrated after setting off all collectables were amounted to $157194.98.

Further, there will be reduction of previous year’s set off capital loss of $7000 that brings an

overall net capital gain as $150194.98.

QUESTION 2

Advising Jasmine in analysing FBT on various assets

Car

Rapid Head Pty provided Jasmine a car for traveling purposes. So, it will be calculated

with reference to Fringe Benefit Tax Assessment Act 1986.

As per Section 7 of the FBTA Act where at any time car provided to employee is applied

for private use (Fringe benefits tax, 2018). Section 7(3) of the act suggests that a car will be

treated as private use, when not in premises and parked at employee’s home.

The car has been defined by the act as:

Motor cars, station wagons, vans or any utilities

Other Goods carrying vehicle capacity of less than 1 tone.

Other passengers carrying vehicle carrying less than 9 occupants

As per Section 9 of Act, FBT can be calculated by using two methods:

1. Statutory Method-: Where a person does not show the actual value of cars in gross

taxable value.

2. Cost Method-: Where a person shows the actual value of cars in gross taxable value.

Section 9 also states that any amount paid as an expense with respect to fuel of car, and

repairs if documentary evidence given by the employee in vacant period will be barred by

employer. The car for repairs and maintenance will not be treated under private or personal use

(McLaren, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

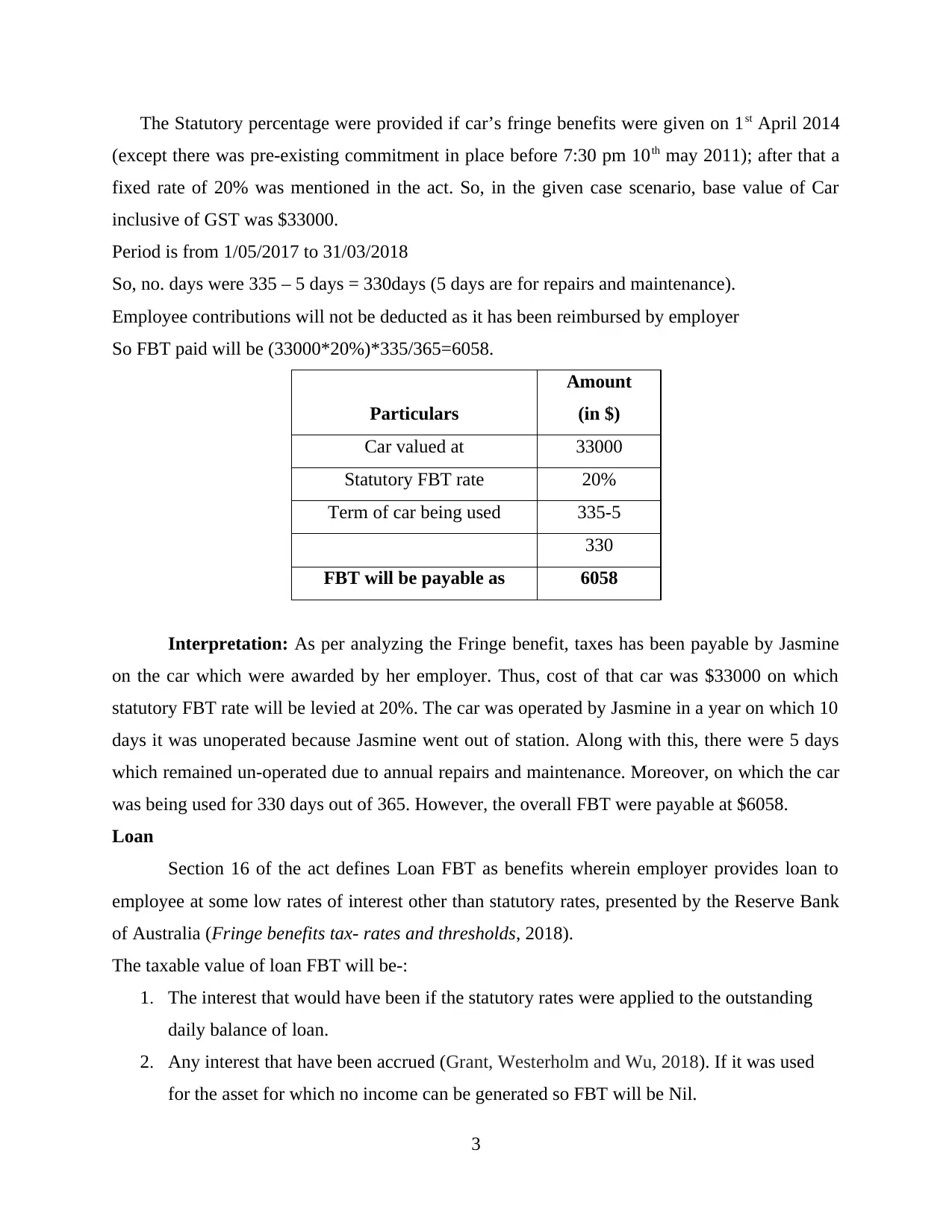

The Statutory percentage were provided if car’s fringe benefits were given on 1st April 2014

(except there was pre-existing commitment in place before 7:30 pm 10th may 2011); after that a

fixed rate of 20% was mentioned in the act. So, in the given case scenario, base value of Car

inclusive of GST was $33000.

Period is from 1/05/2017 to 31/03/2018

So, no. days were 335 – 5 days = 330days (5 days are for repairs and maintenance).

Employee contributions will not be deducted as it has been reimbursed by employer

So FBT paid will be (33000*20%)*335/365=6058.

Particulars

Amount

(in $)

Car valued at 33000

Statutory FBT rate 20%

Term of car being used 335-5

330

FBT will be payable as 6058

Interpretation: As per analyzing the Fringe benefit, taxes has been payable by Jasmine

on the car which were awarded by her employer. Thus, cost of that car was $33000 on which

statutory FBT rate will be levied at 20%. The car was operated by Jasmine in a year on which 10

days it was unoperated because Jasmine went out of station. Along with this, there were 5 days

which remained un-operated due to annual repairs and maintenance. Moreover, on which the car

was being used for 330 days out of 365. However, the overall FBT were payable at $6058.

Loan

Section 16 of the act defines Loan FBT as benefits wherein employer provides loan to

employee at some low rates of interest other than statutory rates, presented by the Reserve Bank

of Australia (Fringe benefits tax- rates and thresholds, 2018).

The taxable value of loan FBT will be-:

1. The interest that would have been if the statutory rates were applied to the outstanding

daily balance of loan.

2. Any interest that have been accrued (Grant, Westerholm and Wu, 2018). If it was used

for the asset for which no income can be generated so FBT will be Nil.

3

(except there was pre-existing commitment in place before 7:30 pm 10th may 2011); after that a

fixed rate of 20% was mentioned in the act. So, in the given case scenario, base value of Car

inclusive of GST was $33000.

Period is from 1/05/2017 to 31/03/2018

So, no. days were 335 – 5 days = 330days (5 days are for repairs and maintenance).

Employee contributions will not be deducted as it has been reimbursed by employer

So FBT paid will be (33000*20%)*335/365=6058.

Particulars

Amount

(in $)

Car valued at 33000

Statutory FBT rate 20%

Term of car being used 335-5

330

FBT will be payable as 6058

Interpretation: As per analyzing the Fringe benefit, taxes has been payable by Jasmine

on the car which were awarded by her employer. Thus, cost of that car was $33000 on which

statutory FBT rate will be levied at 20%. The car was operated by Jasmine in a year on which 10

days it was unoperated because Jasmine went out of station. Along with this, there were 5 days

which remained un-operated due to annual repairs and maintenance. Moreover, on which the car

was being used for 330 days out of 365. However, the overall FBT were payable at $6058.

Loan

Section 16 of the act defines Loan FBT as benefits wherein employer provides loan to

employee at some low rates of interest other than statutory rates, presented by the Reserve Bank

of Australia (Fringe benefits tax- rates and thresholds, 2018).

The taxable value of loan FBT will be-:

1. The interest that would have been if the statutory rates were applied to the outstanding

daily balance of loan.

2. Any interest that have been accrued (Grant, Westerholm and Wu, 2018). If it was used

for the asset for which no income can be generated so FBT will be Nil.

3

GST Act 1999 defines that input tax credit will be available for things that are used for

business (Story, 2017). So here in the given question, car that was purchased for employee and

the expenses made on that car was also for business purpose so, company claimed Input credit in

both cases.

Electric Heater

Interpretation: As per considering the above listed table on which it can be said that costs

of purchasing an electric heater of $1300 with additional manufacturing cost of $700. Thus,

overall purchase costs of that heater were $2000. Thus, it has been sold for $2600 on which

overall gain was of $600. The FBT had been levied on asset on rate of $282.

Analysing the tax consequences as per loan amount will be used by Jasmine in purchasing

securities.

In this Case, where the loan is used for income bearing investments. So taxable FBT will

be 4.25%-5.5% (assumed) from 1st Sept 2017 to 31st March 2018 will be

=50000*1.25%*212/365=363

Particulars Amount

(In $)

FBT tax rate will be 4.25%-5.5%

estimates 1.25%

50000*1.25%*212/365 363

4

business (Story, 2017). So here in the given question, car that was purchased for employee and

the expenses made on that car was also for business purpose so, company claimed Input credit in

both cases.

Electric Heater

Interpretation: As per considering the above listed table on which it can be said that costs

of purchasing an electric heater of $1300 with additional manufacturing cost of $700. Thus,

overall purchase costs of that heater were $2000. Thus, it has been sold for $2600 on which

overall gain was of $600. The FBT had been levied on asset on rate of $282.

Analysing the tax consequences as per loan amount will be used by Jasmine in purchasing

securities.

In this Case, where the loan is used for income bearing investments. So taxable FBT will

be 4.25%-5.5% (assumed) from 1st Sept 2017 to 31st March 2018 will be

=50000*1.25%*212/365=363

Particulars Amount

(In $)

FBT tax rate will be 4.25%-5.5%

estimates 1.25%

50000*1.25%*212/365 363

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.