Capital Gains and Fringe Benefits: A Case Study Analysis

VerifiedAdded on 2023/06/05

|13

|2728

|97

Case Study

AI Summary

This case study analyzes the capital gains tax (CGT) implications of disposing of various assets, including land, shares, an antique bed, a painting, and a violin, in the 2017/18 income year. It discusses pre-CGT assets, CGT events, cost base calculations, capital loss adjustments, and strategies for reducing CGT liability. The analysis covers the disposal of each asset, determining whether CGT applies and how to calculate any gains or losses. Additionally, the case study examines fringe benefits tax (FBT) implications for an employee, Jasmine, focusing on car fringe benefits, loan fringe benefits, and internal expense fringe benefits, detailing how these benefits are assessed and taxed, with reference to relevant sections of the Income Tax Assessment Act and Fringe Benefit Tax Assessment Act. Desklib provides access to similar solved assignments and past papers for students.

a ation heory ractice awT x T , P & L

S D DTU ENT I

[Pick the date]

S D DTU ENT I

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

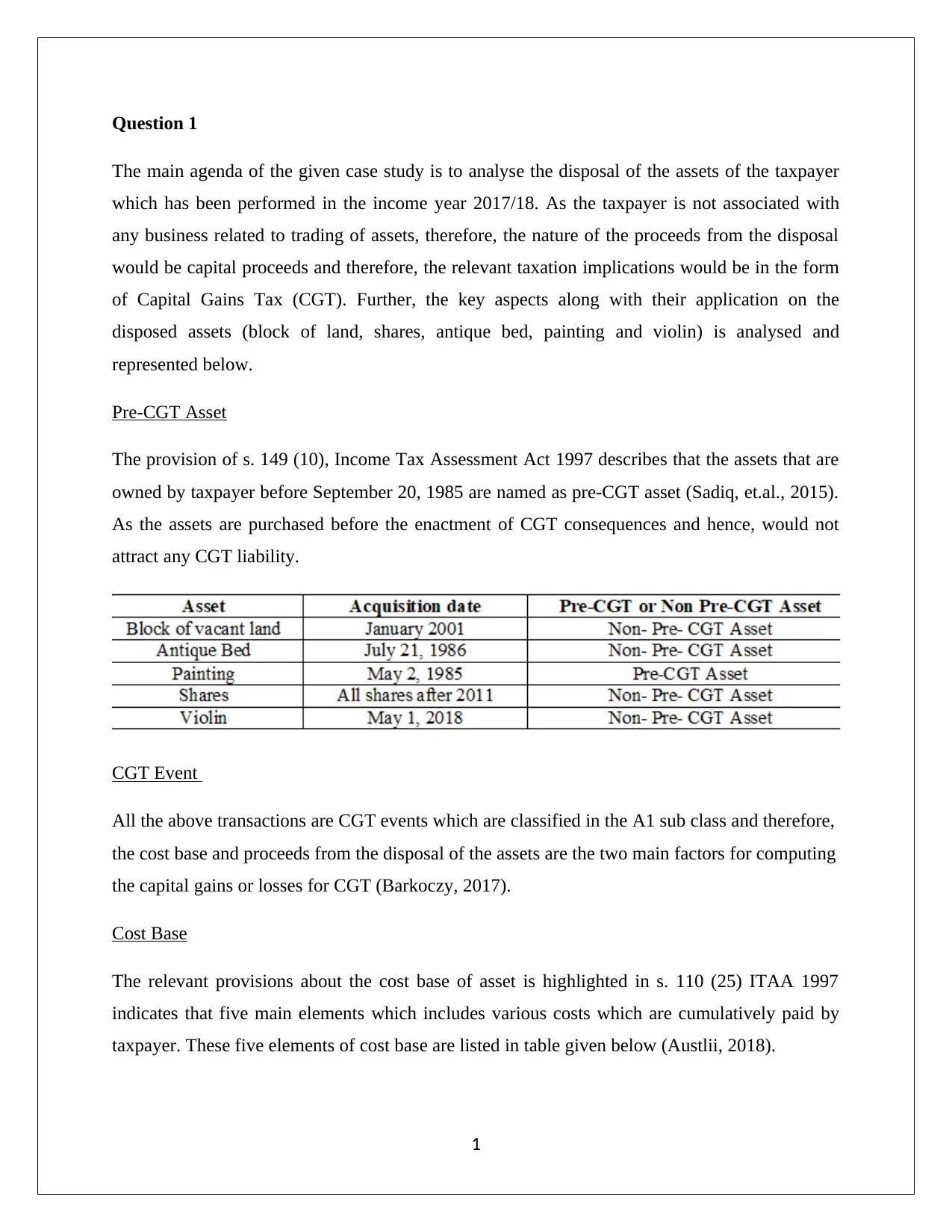

The main agenda of the given case study is to analyse the disposal of the assets of the taxpayer

which has been performed in the income year 2017/18. As the taxpayer is not associated with

any business related to trading of assets, therefore, the nature of the proceeds from the disposal

would be capital proceeds and therefore, the relevant taxation implications would be in the form

of Capital Gains Tax (CGT). Further, the key aspects along with their application on the

disposed assets (block of land, shares, antique bed, painting and violin) is analysed and

represented below.

Pre-CGT Asset

The provision of s. 149 (10), Income Tax Assessment Act 1997 describes that the assets that are

owned by taxpayer before September 20, 1985 are named as pre-CGT asset (Sadiq, et.al., 2015).

As the assets are purchased before the enactment of CGT consequences and hence, would not

attract any CGT liability.

CGT Event

All the above transactions are CGT events which are classified in the A1 sub class and therefore,

the cost base and proceeds from the disposal of the assets are the two main factors for computing

the capital gains or losses for CGT (Barkoczy, 2017).

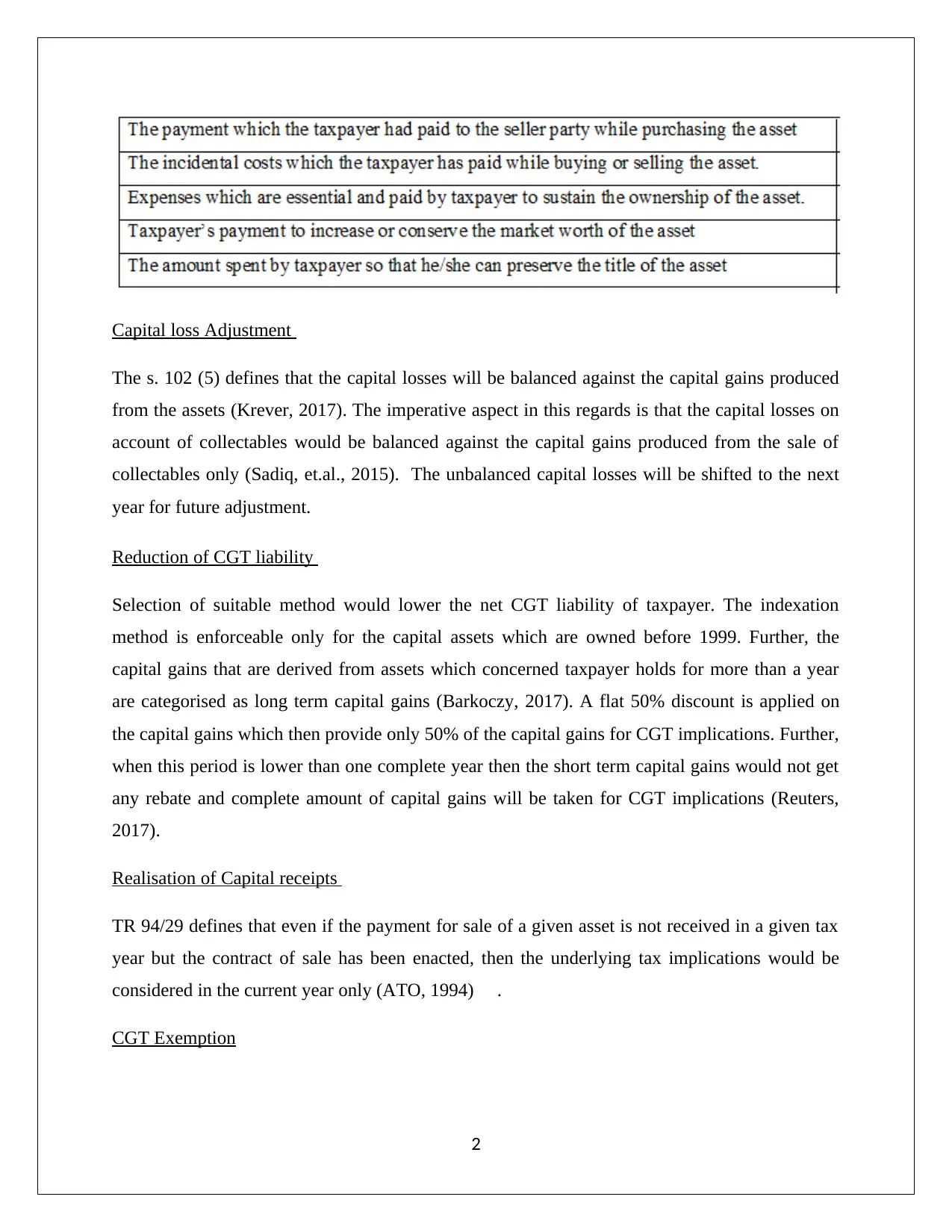

Cost Base

The relevant provisions about the cost base of asset is highlighted in s. 110 (25) ITAA 1997

indicates that five main elements which includes various costs which are cumulatively paid by

taxpayer. These five elements of cost base are listed in table given below (Austlii, 2018).

1

The main agenda of the given case study is to analyse the disposal of the assets of the taxpayer

which has been performed in the income year 2017/18. As the taxpayer is not associated with

any business related to trading of assets, therefore, the nature of the proceeds from the disposal

would be capital proceeds and therefore, the relevant taxation implications would be in the form

of Capital Gains Tax (CGT). Further, the key aspects along with their application on the

disposed assets (block of land, shares, antique bed, painting and violin) is analysed and

represented below.

Pre-CGT Asset

The provision of s. 149 (10), Income Tax Assessment Act 1997 describes that the assets that are

owned by taxpayer before September 20, 1985 are named as pre-CGT asset (Sadiq, et.al., 2015).

As the assets are purchased before the enactment of CGT consequences and hence, would not

attract any CGT liability.

CGT Event

All the above transactions are CGT events which are classified in the A1 sub class and therefore,

the cost base and proceeds from the disposal of the assets are the two main factors for computing

the capital gains or losses for CGT (Barkoczy, 2017).

Cost Base

The relevant provisions about the cost base of asset is highlighted in s. 110 (25) ITAA 1997

indicates that five main elements which includes various costs which are cumulatively paid by

taxpayer. These five elements of cost base are listed in table given below (Austlii, 2018).

1

Capital loss Adjustment

The s. 102 (5) defines that the capital losses will be balanced against the capital gains produced

from the assets (Krever, 2017). The imperative aspect in this regards is that the capital losses on

account of collectables would be balanced against the capital gains produced from the sale of

collectables only (Sadiq, et.al., 2015). The unbalanced capital losses will be shifted to the next

year for future adjustment.

Reduction of CGT liability

Selection of suitable method would lower the net CGT liability of taxpayer. The indexation

method is enforceable only for the capital assets which are owned before 1999. Further, the

capital gains that are derived from assets which concerned taxpayer holds for more than a year

are categorised as long term capital gains (Barkoczy, 2017). A flat 50% discount is applied on

the capital gains which then provide only 50% of the capital gains for CGT implications. Further,

when this period is lower than one complete year then the short term capital gains would not get

any rebate and complete amount of capital gains will be taken for CGT implications (Reuters,

2017).

Realisation of Capital receipts

TR 94/29 defines that even if the payment for sale of a given asset is not received in a given tax

year but the contract of sale has been enacted, then the underlying tax implications would be

considered in the current year only (ATO, 1994) .

CGT Exemption

2

The s. 102 (5) defines that the capital losses will be balanced against the capital gains produced

from the assets (Krever, 2017). The imperative aspect in this regards is that the capital losses on

account of collectables would be balanced against the capital gains produced from the sale of

collectables only (Sadiq, et.al., 2015). The unbalanced capital losses will be shifted to the next

year for future adjustment.

Reduction of CGT liability

Selection of suitable method would lower the net CGT liability of taxpayer. The indexation

method is enforceable only for the capital assets which are owned before 1999. Further, the

capital gains that are derived from assets which concerned taxpayer holds for more than a year

are categorised as long term capital gains (Barkoczy, 2017). A flat 50% discount is applied on

the capital gains which then provide only 50% of the capital gains for CGT implications. Further,

when this period is lower than one complete year then the short term capital gains would not get

any rebate and complete amount of capital gains will be taken for CGT implications (Reuters,

2017).

Realisation of Capital receipts

TR 94/29 defines that even if the payment for sale of a given asset is not received in a given tax

year but the contract of sale has been enacted, then the underlying tax implications would be

considered in the current year only (ATO, 1994) .

CGT Exemption

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CGT will not be imposed on the capital gains received when the following factors are incurred

(Deutsch, et.al., 2015).

When taxpayer has sold a pre-CGT capital asset then CGT is exempted

When the personal use asset has been acquired at lesser than $10,000 then also CGT is

exempted.

When any collectable has been acquired lesser than $500 then CGT is exempted

Disposal of Block of Vacant Land

The CGT liability will be linked to the capital gains or losses computed in case of sale of land

block because the transaction is not related to a pre-CGT. Further, the nature of transaction for

selling the asset is CGT event of A1 subclass. The proceeds from the sale of the land will

actually be received in FY2019 while the sale contract has been made in FY2018 and hence, as

per the applicability of TR 94/29, the proceeds will be used for capital gains/losses computation

in FY 2018 only (Deutsch, et.al., 2015). Further, the losses from the previous years will also be

counterbalanced against the capital gains generated. Ownership period for land has exceeded one

year and therefore, 50% will be chargeable on the capital gains received so as to minimize the

net CGT liability for taxpayer.

Disposal of Antique Bed

Antique bed is classified as collectable (s. 118-10) and the CGT liability will be applied on the

capital gains/loss received from the disposal income because the owning amount is $3,500

whereas the threshold cut-off limit is more than $500 which is satisfied and hence, CGT will be

applicable. It is apparent that taxpayer has not voluntarily sold the antique bed and rather it has

3

(Deutsch, et.al., 2015).

When taxpayer has sold a pre-CGT capital asset then CGT is exempted

When the personal use asset has been acquired at lesser than $10,000 then also CGT is

exempted.

When any collectable has been acquired lesser than $500 then CGT is exempted

Disposal of Block of Vacant Land

The CGT liability will be linked to the capital gains or losses computed in case of sale of land

block because the transaction is not related to a pre-CGT. Further, the nature of transaction for

selling the asset is CGT event of A1 subclass. The proceeds from the sale of the land will

actually be received in FY2019 while the sale contract has been made in FY2018 and hence, as

per the applicability of TR 94/29, the proceeds will be used for capital gains/losses computation

in FY 2018 only (Deutsch, et.al., 2015). Further, the losses from the previous years will also be

counterbalanced against the capital gains generated. Ownership period for land has exceeded one

year and therefore, 50% will be chargeable on the capital gains received so as to minimize the

net CGT liability for taxpayer.

Disposal of Antique Bed

Antique bed is classified as collectable (s. 118-10) and the CGT liability will be applied on the

capital gains/loss received from the disposal income because the owning amount is $3,500

whereas the threshold cut-off limit is more than $500 which is satisfied and hence, CGT will be

applicable. It is apparent that taxpayer has not voluntarily sold the antique bed and rather it has

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

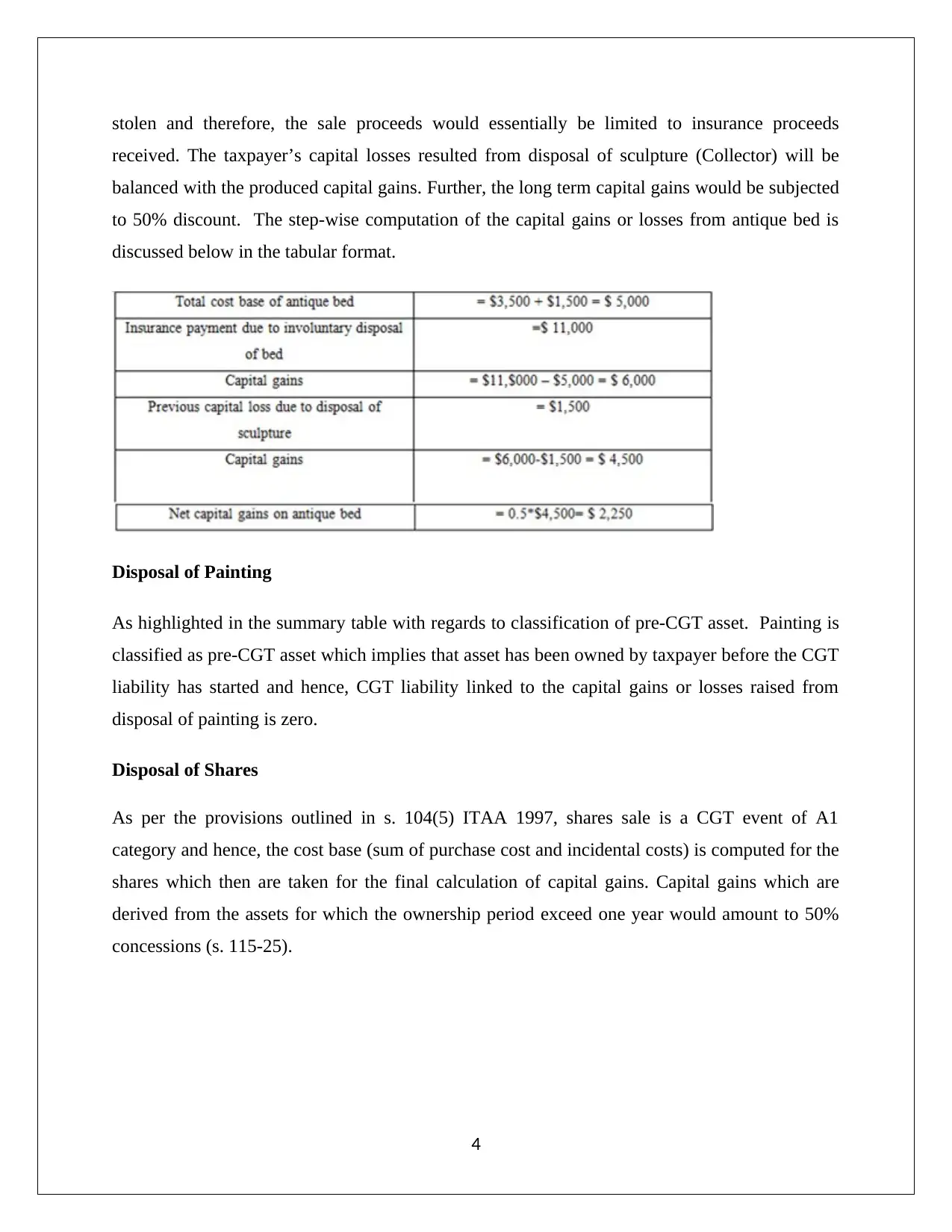

stolen and therefore, the sale proceeds would essentially be limited to insurance proceeds

received. The taxpayer’s capital losses resulted from disposal of sculpture (Collector) will be

balanced with the produced capital gains. Further, the long term capital gains would be subjected

to 50% discount. The step-wise computation of the capital gains or losses from antique bed is

discussed below in the tabular format.

Disposal of Painting

As highlighted in the summary table with regards to classification of pre-CGT asset. Painting is

classified as pre-CGT asset which implies that asset has been owned by taxpayer before the CGT

liability has started and hence, CGT liability linked to the capital gains or losses raised from

disposal of painting is zero.

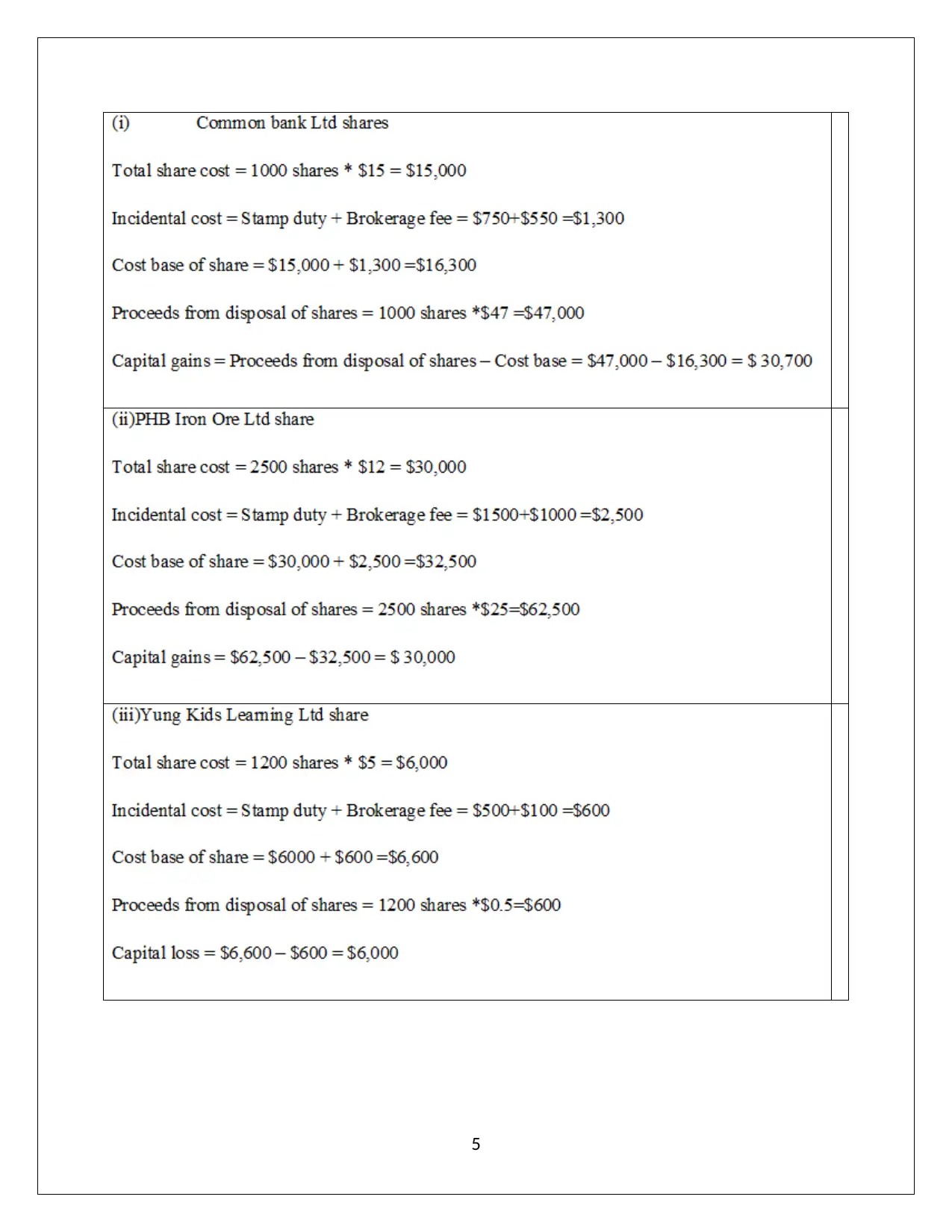

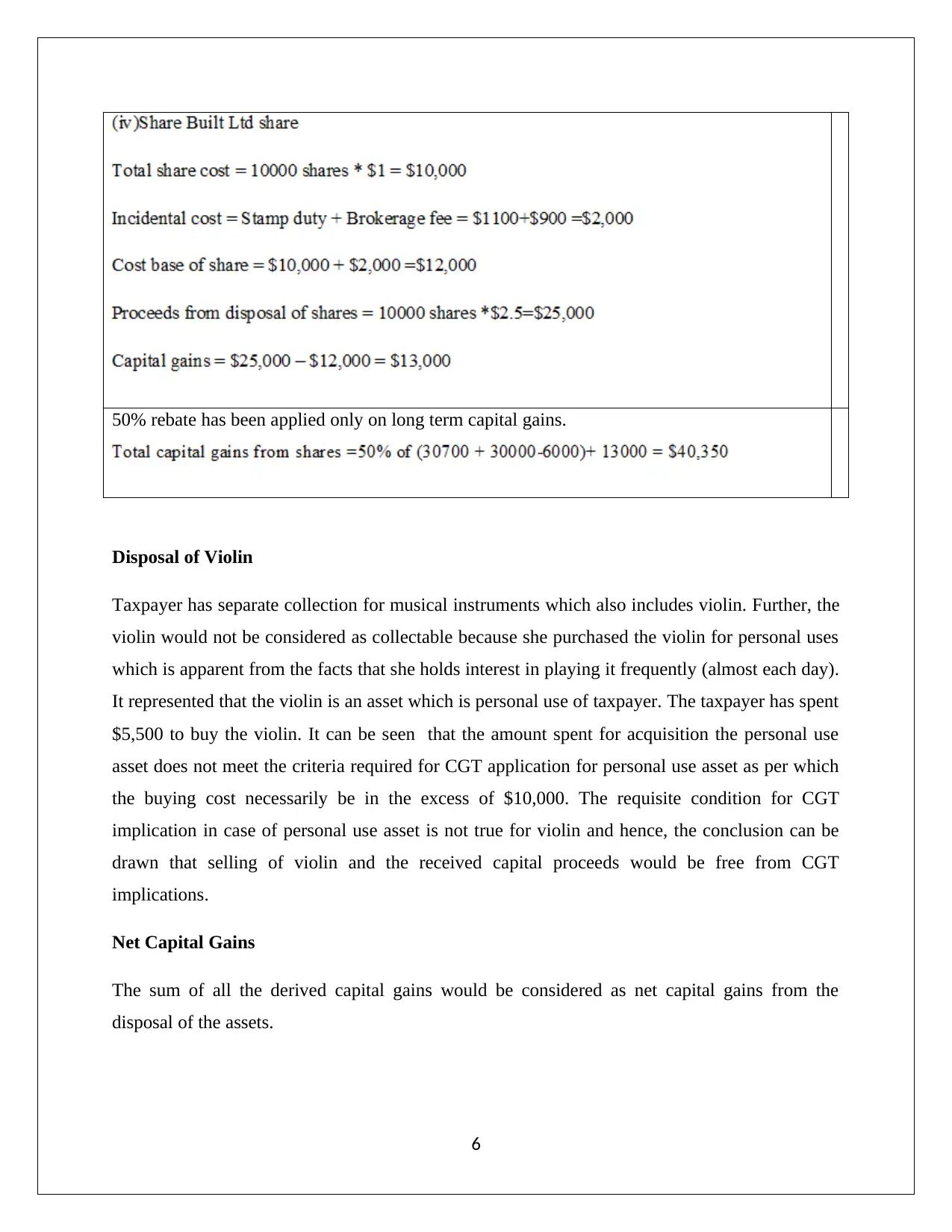

Disposal of Shares

As per the provisions outlined in s. 104(5) ITAA 1997, shares sale is a CGT event of A1

category and hence, the cost base (sum of purchase cost and incidental costs) is computed for the

shares which then are taken for the final calculation of capital gains. Capital gains which are

derived from the assets for which the ownership period exceed one year would amount to 50%

concessions (s. 115-25).

4

received. The taxpayer’s capital losses resulted from disposal of sculpture (Collector) will be

balanced with the produced capital gains. Further, the long term capital gains would be subjected

to 50% discount. The step-wise computation of the capital gains or losses from antique bed is

discussed below in the tabular format.

Disposal of Painting

As highlighted in the summary table with regards to classification of pre-CGT asset. Painting is

classified as pre-CGT asset which implies that asset has been owned by taxpayer before the CGT

liability has started and hence, CGT liability linked to the capital gains or losses raised from

disposal of painting is zero.

Disposal of Shares

As per the provisions outlined in s. 104(5) ITAA 1997, shares sale is a CGT event of A1

category and hence, the cost base (sum of purchase cost and incidental costs) is computed for the

shares which then are taken for the final calculation of capital gains. Capital gains which are

derived from the assets for which the ownership period exceed one year would amount to 50%

concessions (s. 115-25).

4

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

50% rebate has been applied only on long term capital gains.

Disposal of Violin

Taxpayer has separate collection for musical instruments which also includes violin. Further, the

violin would not be considered as collectable because she purchased the violin for personal uses

which is apparent from the facts that she holds interest in playing it frequently (almost each day).

It represented that the violin is an asset which is personal use of taxpayer. The taxpayer has spent

$5,500 to buy the violin. It can be seen that the amount spent for acquisition the personal use

asset does not meet the criteria required for CGT application for personal use asset as per which

the buying cost necessarily be in the excess of $10,000. The requisite condition for CGT

implication in case of personal use asset is not true for violin and hence, the conclusion can be

drawn that selling of violin and the received capital proceeds would be free from CGT

implications.

Net Capital Gains

The sum of all the derived capital gains would be considered as net capital gains from the

disposal of the assets.

6

Disposal of Violin

Taxpayer has separate collection for musical instruments which also includes violin. Further, the

violin would not be considered as collectable because she purchased the violin for personal uses

which is apparent from the facts that she holds interest in playing it frequently (almost each day).

It represented that the violin is an asset which is personal use of taxpayer. The taxpayer has spent

$5,500 to buy the violin. It can be seen that the amount spent for acquisition the personal use

asset does not meet the criteria required for CGT application for personal use asset as per which

the buying cost necessarily be in the excess of $10,000. The requisite condition for CGT

implication in case of personal use asset is not true for violin and hence, the conclusion can be

drawn that selling of violin and the received capital proceeds would be free from CGT

implications.

Net Capital Gains

The sum of all the derived capital gains would be considered as net capital gains from the

disposal of the assets.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2

(a) There are specific benefits that employers provide to employees which are named fringe

benefits. There are two key characteristics associated with these.

These would not be presented in cash form and limited to non-cash form only.

The benefits are not professional but rather personal in nature.

Another unique feature of fringe benefit which segregates it from other kind of employee

benefits is the unique pattern of taxation. For normal employee benefits (both cash and non-

cash), the employee would be levied personal income tax and employer would be able to gain

deduction on the expense. However, in case of fringe benefits, the beneficiary (i.e. employee)

is exempt from all concerned tax liabilities and only the benefit provider would be taxed. As

a result, the applicable statute for these benefits is “Fringe Benefit Tax Assessment Act

1986”(Wilmot, 2014). The discussion in regards to various applicable fringe benefits for

Jasmine is carried in the manner exhibited as follows.

Car Fringe Benefit

A common benefit that is often extended to employee is car fringe benefit. If the employer

provides conveyance in the form of car to the employee for conducting job duties, then it does

not lead to any fringe benefit since the car is only used for completing office work. However,

benefit is extended to employee only when the employee can use the car for personal use which

is indeed a benefit enjoyed by the employee (Sadiq, et.al., 2015).

The given case facts highlight that employer purchases a brand new car and hands it to the

employee (Jasmine). The usage of this car is not limited to professional reasons as the car also

remains with Jasmine on weekends and holidays when the office is closed. Owing to the

7

(a) There are specific benefits that employers provide to employees which are named fringe

benefits. There are two key characteristics associated with these.

These would not be presented in cash form and limited to non-cash form only.

The benefits are not professional but rather personal in nature.

Another unique feature of fringe benefit which segregates it from other kind of employee

benefits is the unique pattern of taxation. For normal employee benefits (both cash and non-

cash), the employee would be levied personal income tax and employer would be able to gain

deduction on the expense. However, in case of fringe benefits, the beneficiary (i.e. employee)

is exempt from all concerned tax liabilities and only the benefit provider would be taxed. As

a result, the applicable statute for these benefits is “Fringe Benefit Tax Assessment Act

1986”(Wilmot, 2014). The discussion in regards to various applicable fringe benefits for

Jasmine is carried in the manner exhibited as follows.

Car Fringe Benefit

A common benefit that is often extended to employee is car fringe benefit. If the employer

provides conveyance in the form of car to the employee for conducting job duties, then it does

not lead to any fringe benefit since the car is only used for completing office work. However,

benefit is extended to employee only when the employee can use the car for personal use which

is indeed a benefit enjoyed by the employee (Sadiq, et.al., 2015).

The given case facts highlight that employer purchases a brand new car and hands it to the

employee (Jasmine). The usage of this car is not limited to professional reasons as the car also

remains with Jasmine on weekends and holidays when the office is closed. Owing to the

7

arrangement indicated above, it becomes evident that Jasmine has been the recipient of car fringe

benefits and resultant FBT would be payable by the employer (Rapid Heat).

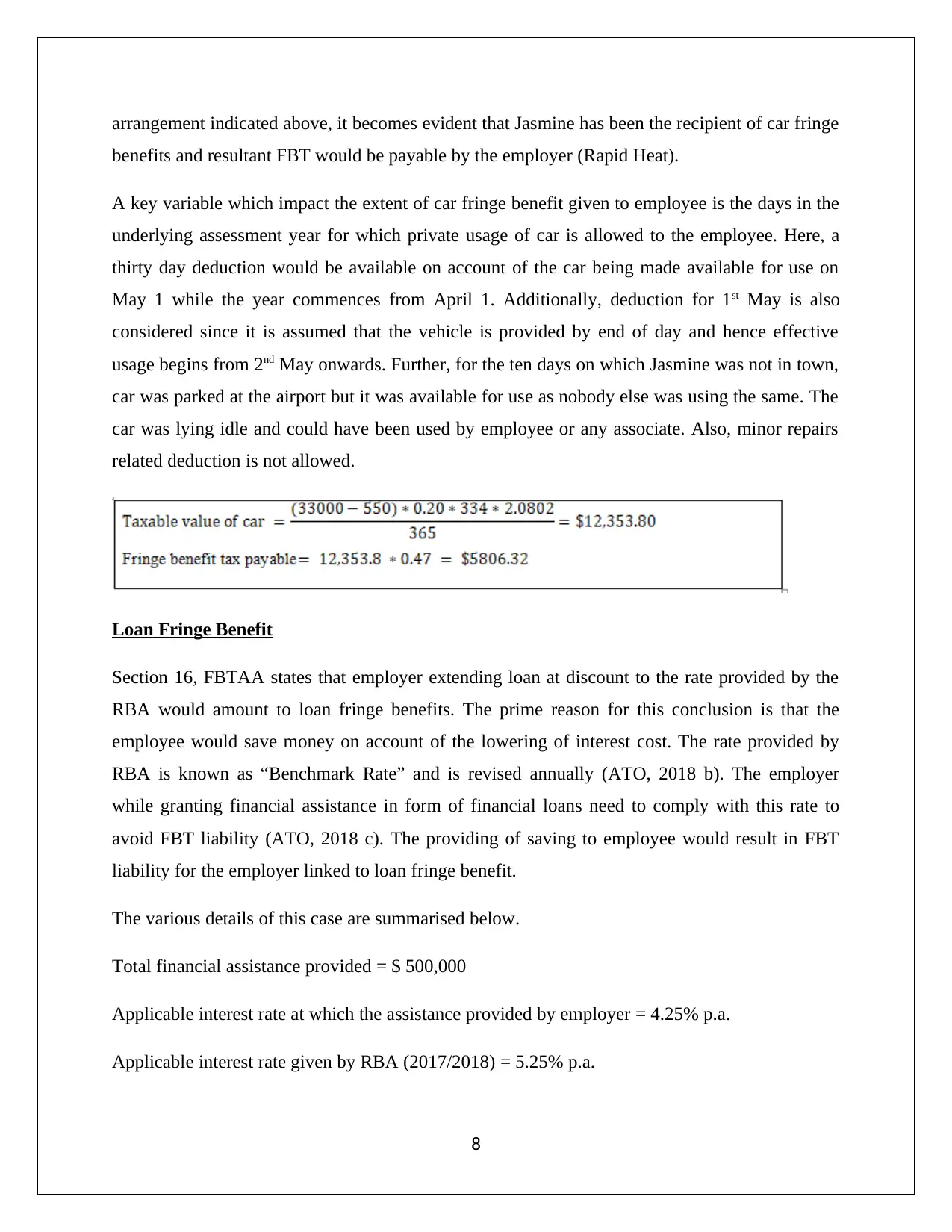

A key variable which impact the extent of car fringe benefit given to employee is the days in the

underlying assessment year for which private usage of car is allowed to the employee. Here, a

thirty day deduction would be available on account of the car being made available for use on

May 1 while the year commences from April 1. Additionally, deduction for 1st May is also

considered since it is assumed that the vehicle is provided by end of day and hence effective

usage begins from 2nd May onwards. Further, for the ten days on which Jasmine was not in town,

car was parked at the airport but it was available for use as nobody else was using the same. The

car was lying idle and could have been used by employee or any associate. Also, minor repairs

related deduction is not allowed.

Loan Fringe Benefit

Section 16, FBTAA states that employer extending loan at discount to the rate provided by the

RBA would amount to loan fringe benefits. The prime reason for this conclusion is that the

employee would save money on account of the lowering of interest cost. The rate provided by

RBA is known as “Benchmark Rate” and is revised annually (ATO, 2018 b). The employer

while granting financial assistance in form of financial loans need to comply with this rate to

avoid FBT liability (ATO, 2018 c). The providing of saving to employee would result in FBT

liability for the employer linked to loan fringe benefit.

The various details of this case are summarised below.

Total financial assistance provided = $ 500,000

Applicable interest rate at which the assistance provided by employer = 4.25% p.a.

Applicable interest rate given by RBA (2017/2018) = 5.25% p.a.

8

benefits and resultant FBT would be payable by the employer (Rapid Heat).

A key variable which impact the extent of car fringe benefit given to employee is the days in the

underlying assessment year for which private usage of car is allowed to the employee. Here, a

thirty day deduction would be available on account of the car being made available for use on

May 1 while the year commences from April 1. Additionally, deduction for 1st May is also

considered since it is assumed that the vehicle is provided by end of day and hence effective

usage begins from 2nd May onwards. Further, for the ten days on which Jasmine was not in town,

car was parked at the airport but it was available for use as nobody else was using the same. The

car was lying idle and could have been used by employee or any associate. Also, minor repairs

related deduction is not allowed.

Loan Fringe Benefit

Section 16, FBTAA states that employer extending loan at discount to the rate provided by the

RBA would amount to loan fringe benefits. The prime reason for this conclusion is that the

employee would save money on account of the lowering of interest cost. The rate provided by

RBA is known as “Benchmark Rate” and is revised annually (ATO, 2018 b). The employer

while granting financial assistance in form of financial loans need to comply with this rate to

avoid FBT liability (ATO, 2018 c). The providing of saving to employee would result in FBT

liability for the employer linked to loan fringe benefit.

The various details of this case are summarised below.

Total financial assistance provided = $ 500,000

Applicable interest rate at which the assistance provided by employer = 4.25% p.a.

Applicable interest rate given by RBA (2017/2018) = 5.25% p.a.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The application of discount on the RBA rate to the extent of 1% is clear evidence of the loan

fringe benefit being extended to Jasmine.

The deduction rule outlined in section 18, FBTAA 1986 highlights that FBT reduction may be

possible for employer depending upon the utilisation of the loan and obtaining assessable income

by employer from the usage of loan proceeds (ATO, 2018 c). In this regards, a key aspect is that

possible deduction is available when the money is used by employee and not any associate.

Taking into consideration the usage of the loan proceeds, no deduction on $ 50,000 loan amount

would be available for Rapid Heat since this has been extended to Jasmine’s husband. The

possibility of FBT deduction for the employer depends on whether the holiday home that jasmine

has bought would generate taxable income probably in form of rent or not for Jasmine.

Internal Expenses Fringe Benefit

The private expenses of employees are not the responsibility of employer. However, if the

employer provides any contribution in this regards, then the underlying benefit would be called

as expense fringe benefit. One particular case which may arise in this regards is when the

employer lower the quote of a self-made product when the employer intends to purchase the

same. It is equivalent of the employer paying the discount amount while employee bearing the

remaining price (ATO, 2018 a).

In the given instance, Rapid Heater is a manufacturer of electric heater and Jasmine is interested

in buying one of these. The price to consumers is $ 2,600 but when Jasmine expresses her desire

to make purchase, the employer only takes $ 1,300 from her and thereby making the remaining

payment on her behalf.

9

fringe benefit being extended to Jasmine.

The deduction rule outlined in section 18, FBTAA 1986 highlights that FBT reduction may be

possible for employer depending upon the utilisation of the loan and obtaining assessable income

by employer from the usage of loan proceeds (ATO, 2018 c). In this regards, a key aspect is that

possible deduction is available when the money is used by employee and not any associate.

Taking into consideration the usage of the loan proceeds, no deduction on $ 50,000 loan amount

would be available for Rapid Heat since this has been extended to Jasmine’s husband. The

possibility of FBT deduction for the employer depends on whether the holiday home that jasmine

has bought would generate taxable income probably in form of rent or not for Jasmine.

Internal Expenses Fringe Benefit

The private expenses of employees are not the responsibility of employer. However, if the

employer provides any contribution in this regards, then the underlying benefit would be called

as expense fringe benefit. One particular case which may arise in this regards is when the

employer lower the quote of a self-made product when the employer intends to purchase the

same. It is equivalent of the employer paying the discount amount while employee bearing the

remaining price (ATO, 2018 a).

In the given instance, Rapid Heater is a manufacturer of electric heater and Jasmine is interested

in buying one of these. The price to consumers is $ 2,600 but when Jasmine expresses her desire

to make purchase, the employer only takes $ 1,300 from her and thereby making the remaining

payment on her behalf.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(b) Now, there has been a change in the loan proceed utilisation with 100% of the amount being

used by Jasmine only. This would be useful for the employer since the share related income

as dividends would ensure that deduction rule would be applicable. As a result, the employer

would be able to extract extra FBT deduction to the following extent.

10

used by Jasmine only. This would be useful for the employer since the share related income

as dividends would ensure that deduction rule would be applicable. As a result, the employer

would be able to extract extra FBT deduction to the following extent.

10

References

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 30 September 2018)

ATO, (2018 a) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 30

September 2018)

ATO, (2018 b) Loan Fringe Benefits https://www.ato.gov.au/General/Fringe-benefits-tax-

(FBT)/Types-of-fringe-benefits/Loan-fringe-benefits/ (Accessed: 30 September 2018)

ATO, (2018 c) Fringe Benefits Tax- Exemptions and Concessions.

https://www.ato.gov.au/general/fringe-benefits-tax-(fbt)/in-detail/getting-started/fbt-for-small-

business/?page=21 (Accessed: 24 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 30

September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 115.25 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.25.html (Accessed: 30

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

11

ATO, (1994) Taxation Ruling –TR 94/29 [Online]. Available at: Income tax: capital gains tax

consequences of a contract for the sale of land falling through.

https://www.ato.gov.au/law/view/document?DocID=TXR/TR9429/NAT/ATO/

00001&PiT=99991231235958 (Accessed: 30 September 2018)

ATO, (2018 a) Fringe Benefits Tax- A Guide For Employers.

http://law.ato.gov.au/atolaw/view.htm?DocID=SAV%2FFBTGEMP%2F00010 (Accessed: 30

September 2018)

ATO, (2018 b) Loan Fringe Benefits https://www.ato.gov.au/General/Fringe-benefits-tax-

(FBT)/Types-of-fringe-benefits/Loan-fringe-benefits/ (Accessed: 30 September 2018)

ATO, (2018 c) Fringe Benefits Tax- Exemptions and Concessions.

https://www.ato.gov.au/general/fringe-benefits-tax-(fbt)/in-detail/getting-started/fbt-for-small-

business/?page=21 (Accessed: 24 September 2018)

Austlii, (2018 a) Income Tax Assessment Act 1997- SECT 110.25.General Rules About Cost

Base [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html (Accessed: 30

September 2018)

Austlii, (2018) Income Tax Assessment Act 1997- SECT 115.25 [Online]. Available at:

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.25.html (Accessed: 30

September 2018)

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.