LAW505 Taxation Assignment: Compensatory Damages and Capital Gains

VerifiedAdded on 2022/12/22

|17

|5056

|54

Report

AI Summary

This report examines the taxation implications for Our Earth Pty Ltd, an Australian company, concerning compensatory damages received for patent infringement and lost revenue, as well as the tax treatment of legal expenses. The analysis covers the application of "Division 6" and "Section 25 (1) of ITAA 1936" to determine the assessability of the damages received. The report delves into whether the compensatory damages are considered capital receipts or ordinary income, referencing relevant case law such as "CT (Vic) v Phillips (1936)" and "FC of T v Spedley Securities Ltd (1988)". Furthermore, it considers the treatment of interest received as part of the damages and the tax deductibility of legal expenses, referencing "Section 8 (1) of ITAA 1997" and "Subdivision 20 (A)". The second part of the report analyzes the capital gains tax implications of subdivided land sales, examining the applicability of "Section 26 (A)" and "Section 25 (1)", and considering whether the taxpayer has engaged in a simple realization of a capital asset. The report provides a detailed analysis of the facts, relevant legislation, and case law to arrive at conclusions regarding the tax liabilities of Our Earth Pty Ltd. The report also provides guidance on the application of capital gains tax to assets and the circumstances under which land subdivision may result in assessable income.

Running head: TAXATION

Taxation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Taxation

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION

Table of Contents

Question 1:.................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Question 2:.................................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

Table of Contents

Question 1:.................................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................4

Conclusion:............................................................................................................................6

Question 2:.................................................................................................................................7

Issues:.....................................................................................................................................7

Laws:......................................................................................................................................7

Application:..........................................................................................................................10

Conclusion:..........................................................................................................................13

References:...............................................................................................................................14

2TAXATION

Question 1:

Issues:

The main issue in this case is to find out whether the taxpayer would be obliged for

tax in terms of receipt of compensatory damages in accordance with “Division 6” or “Section

25 (1) of ITAA 1936”. The other issues include interest receipt from the payout of damages

and deciding whether to incorporate the same in assessable income of Our Earth Private

Limited and the liability of the taxpayer for assessment purpose to reimburse the legal

expenditure made by the organisation.

Laws:

The taxpayer often receives receipts of typical compensation, which comprise of

business receipts from external parties not able to meet contractual obligations, insurance

payments, payments obtained to enter into restrictive covenants and loss of monetary usage

and they are generally deemed to be in the form of income by nature (Auerbach & Hassett,

2015). An organisation often receives compensation receipts in the form of right to seek

compensation or any kind of partnership that it has introduced or the cause of action or with

respect to the underlying assets, which are considered as compensatory receipts. The

compensation obtained from damages would be incorporated into assessable income in

relation to the general meaning mentioned in “Division 6 of ITAA 1997” or it would be

included in the form of statutory income.

“Section 25 (1) of ITAA 1997” states that the received compensatory payments are

deemed to be taxable. However, it is estimated that the payments received are associated with

loss of income, especially, the interest or profit from past years (Baliamoune-Lutz & Garello,

2014). For instance, in the case of “Mclaurin v FC of T (1961)”, it has been found that the

Question 1:

Issues:

The main issue in this case is to find out whether the taxpayer would be obliged for

tax in terms of receipt of compensatory damages in accordance with “Division 6” or “Section

25 (1) of ITAA 1936”. The other issues include interest receipt from the payout of damages

and deciding whether to incorporate the same in assessable income of Our Earth Private

Limited and the liability of the taxpayer for assessment purpose to reimburse the legal

expenditure made by the organisation.

Laws:

The taxpayer often receives receipts of typical compensation, which comprise of

business receipts from external parties not able to meet contractual obligations, insurance

payments, payments obtained to enter into restrictive covenants and loss of monetary usage

and they are generally deemed to be in the form of income by nature (Auerbach & Hassett,

2015). An organisation often receives compensation receipts in the form of right to seek

compensation or any kind of partnership that it has introduced or the cause of action or with

respect to the underlying assets, which are considered as compensatory receipts. The

compensation obtained from damages would be incorporated into assessable income in

relation to the general meaning mentioned in “Division 6 of ITAA 1997” or it would be

included in the form of statutory income.

“Section 25 (1) of ITAA 1997” states that the received compensatory payments are

deemed to be taxable. However, it is estimated that the payments received are associated with

loss of income, especially, the interest or profit from past years (Baliamoune-Lutz & Garello,

2014). For instance, in the case of “Mclaurin v FC of T (1961)”, it has been found that the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION

compensation receipt was taxable within the statutory provision of “Section 25 (1) of ITAA

1936” until the part of payment obtained could be recognised and it had to be assessable in

the form of income.

For determining whether the compensation receipts amount to capital receipts or

ordinary income rely largely on the nature of payment. The application of “Section 6 (5) of

ITAA 1997” could be made when a compensation payment has the nature of income in

relation to ordinary concepts (Barkoczy, 2016). For instance, compensatory payments are

deemed to be assessable income at the time they are obtained in the form of either periodic or

recurrent payments and they need not be in the form of lump sum instalments.

For instance, in the case of “Californian Oil Products Limited v Federal

Commissioner of Taxation (1934)”, amounts incurred in the form of compensation, damages

or covering income loss taken place during the business course have to be treated in the form

of taxable income (Bevacqua, 2015). The fundamental reason is that it is a portion of profit

obtained from conduction of the business operations although it us a outcome of

extraordinary or unusual situations or occasions.

In the case of “CT (Vic) v Phillips (1936)”, the Taxation Commissioner has provided

a verdict by stating that if the taxpayer obtains a compensation associated with the loss of

commercial scheme or business income forming the element of business operations, the

compensation would be adjudged in the form of loss of capital asset (Braithwaite,

2017). Since there was no countervailing investigation, the receipts are treated in the form of

capital receipts. In the case of “FC of T v Spedley Securities Ltd (1988)”, according to the

statement of the Federal Court, compensatory damages in relation to goodwill were treated in

the form of capital item, while the compensation receipt was treated in the form of injury to

capital asset.

compensation receipt was taxable within the statutory provision of “Section 25 (1) of ITAA

1936” until the part of payment obtained could be recognised and it had to be assessable in

the form of income.

For determining whether the compensation receipts amount to capital receipts or

ordinary income rely largely on the nature of payment. The application of “Section 6 (5) of

ITAA 1997” could be made when a compensation payment has the nature of income in

relation to ordinary concepts (Barkoczy, 2016). For instance, compensatory payments are

deemed to be assessable income at the time they are obtained in the form of either periodic or

recurrent payments and they need not be in the form of lump sum instalments.

For instance, in the case of “Californian Oil Products Limited v Federal

Commissioner of Taxation (1934)”, amounts incurred in the form of compensation, damages

or covering income loss taken place during the business course have to be treated in the form

of taxable income (Bevacqua, 2015). The fundamental reason is that it is a portion of profit

obtained from conduction of the business operations although it us a outcome of

extraordinary or unusual situations or occasions.

In the case of “CT (Vic) v Phillips (1936)”, the Taxation Commissioner has provided

a verdict by stating that if the taxpayer obtains a compensation associated with the loss of

commercial scheme or business income forming the element of business operations, the

compensation would be adjudged in the form of loss of capital asset (Braithwaite,

2017). Since there was no countervailing investigation, the receipts are treated in the form of

capital receipts. In the case of “FC of T v Spedley Securities Ltd (1988)”, according to the

statement of the Federal Court, compensatory damages in relation to goodwill were treated in

the form of capital item, while the compensation receipt was treated in the form of injury to

capital asset.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION

When any taxpayer obtains interest in the form of compensatory amount, the amount

is considered in the form of taxable income for the taxpayer under the ordinary income

provision. As explained in the case “Whitaker v FCT (1998)”, post-judgement interests are

deemed to possess the nature of interest and they are adjudged as income in accordance with

the ordinary concept (Braunerhjelm & Eklund, 2014). In this regard, it is to be borne in mind

that under ordinary concepts, interest receipts are considered as income, in which there is

relationship with the compensation for lost income by considering that the claimant has not

faced any losses obtained from the awarded interest.

On the contrary, when the taxpayers are allowed to gain deduction for the available

legal expenses in accordance with “Section 8 (1) of ITAA 1997”, the award or payment in

relation to the legal expenses would be incorporated into the taxable income of the taxpayers

as recovery under “Subdivision 20 (A)”. The awarded legal expenditures are incurred to the

taxpayers so that they could be identified or the successful party is the recipient in relation to

the lawsuit cost (Chardon, Freudenberg & Brimble, 2016). According to “Subsection 20-20

(2)”, legal expenses are treated as taxable recoupment of expense or loss. This is a taxable

recoupment when the taxpayer has obtained the amount in the form of indemnity and the

amount to be deductible for the purpose of tax, as per “ITAA 1936 or ITAA 1997”

(Dharmapala, 2016).

Application:

The information collected from the provided case of Our Earth Private Limited

denotes that the organisation manufactures bio-degradable coffee cups that are designed

specially and they are prepared out of sustainable materials. However, the organisation has

identified that the cup design has been stolen by Coffee Beans Private Limited and the latter

is selling the cups to foreign customers at lower prices. This has compelled Our Earth Private

Limited to undertake legal action against Coffee Beans Private Limited, from which the

When any taxpayer obtains interest in the form of compensatory amount, the amount

is considered in the form of taxable income for the taxpayer under the ordinary income

provision. As explained in the case “Whitaker v FCT (1998)”, post-judgement interests are

deemed to possess the nature of interest and they are adjudged as income in accordance with

the ordinary concept (Braunerhjelm & Eklund, 2014). In this regard, it is to be borne in mind

that under ordinary concepts, interest receipts are considered as income, in which there is

relationship with the compensation for lost income by considering that the claimant has not

faced any losses obtained from the awarded interest.

On the contrary, when the taxpayers are allowed to gain deduction for the available

legal expenses in accordance with “Section 8 (1) of ITAA 1997”, the award or payment in

relation to the legal expenses would be incorporated into the taxable income of the taxpayers

as recovery under “Subdivision 20 (A)”. The awarded legal expenditures are incurred to the

taxpayers so that they could be identified or the successful party is the recipient in relation to

the lawsuit cost (Chardon, Freudenberg & Brimble, 2016). According to “Subsection 20-20

(2)”, legal expenses are treated as taxable recoupment of expense or loss. This is a taxable

recoupment when the taxpayer has obtained the amount in the form of indemnity and the

amount to be deductible for the purpose of tax, as per “ITAA 1936 or ITAA 1997”

(Dharmapala, 2016).

Application:

The information collected from the provided case of Our Earth Private Limited

denotes that the organisation manufactures bio-degradable coffee cups that are designed

specially and they are prepared out of sustainable materials. However, the organisation has

identified that the cup design has been stolen by Coffee Beans Private Limited and the latter

is selling the cups to foreign customers at lower prices. This has compelled Our Earth Private

Limited to undertake legal action against Coffee Beans Private Limited, from which the

5TAXATION

former has obtained $300,000 in the form of damages incurred to the patent infringement

design. The amount received as compensation by Our Earth Private Limited is related to

patent infringement and thus, it has to be considered as compensation obtained in relation to

the right to seek compensation for causing an infringement violation to the patent.

For determining whether compensatory damages are deemed to be capital receipts or

ordinary income, the decision relies on the nature of receipts obtained by Our Earth Private

Limited. By taking into consideration the decision made in “CT (Vic) v Phillips (1936)”,

$300,000 incurred to Our Earth Private Limited in the form of compensatory damages are

related to foundations of business operations or business loss (Eccleston & Warrnen, 2015).

Moreover, the damages amounting to $300,000 have to be considered in the form of

compensation payment due to loss incurred to the capital asset. Along with this, owing to no

countervailing investigation, the receipts or damages are considered to be capital in nature.

In accordance with the decision undertaken in the case of “FC of T v Spedley

Securities Ltd (1988)”, Our Earth Private Limited has received $300,000 as compensation to

recompense the damage caused to its patent, which was capital in nature (Faccio & Xu,

2015). Hence, the amount of $300,000 is not taken into account for assessment purpose, since

it is an ordinary income and compensation amounts for incurring injury to the capital asset.

Later on, it has been found that Our Earth Private Limited has obtained another

$200,000 from Coffee Beans Private Limited, since the former has suffered considerable loss

of profit during the past year. In accordance with the decision undertaken in the case of

“Californian Oil Products Ltd v Federal Commissioner of Taxation (1934)”, it could be

cited that the additional amount obtained by Our Earth Private Limited as a result of

compensating the loss incurred in the past year to the ordinary course of business is definitely

former has obtained $300,000 in the form of damages incurred to the patent infringement

design. The amount received as compensation by Our Earth Private Limited is related to

patent infringement and thus, it has to be considered as compensation obtained in relation to

the right to seek compensation for causing an infringement violation to the patent.

For determining whether compensatory damages are deemed to be capital receipts or

ordinary income, the decision relies on the nature of receipts obtained by Our Earth Private

Limited. By taking into consideration the decision made in “CT (Vic) v Phillips (1936)”,

$300,000 incurred to Our Earth Private Limited in the form of compensatory damages are

related to foundations of business operations or business loss (Eccleston & Warrnen, 2015).

Moreover, the damages amounting to $300,000 have to be considered in the form of

compensation payment due to loss incurred to the capital asset. Along with this, owing to no

countervailing investigation, the receipts or damages are considered to be capital in nature.

In accordance with the decision undertaken in the case of “FC of T v Spedley

Securities Ltd (1988)”, Our Earth Private Limited has received $300,000 as compensation to

recompense the damage caused to its patent, which was capital in nature (Faccio & Xu,

2015). Hence, the amount of $300,000 is not taken into account for assessment purpose, since

it is an ordinary income and compensation amounts for incurring injury to the capital asset.

Later on, it has been found that Our Earth Private Limited has obtained another

$200,000 from Coffee Beans Private Limited, since the former has suffered considerable loss

of profit during the past year. In accordance with the decision undertaken in the case of

“Californian Oil Products Ltd v Federal Commissioner of Taxation (1934)”, it could be

cited that the additional amount obtained by Our Earth Private Limited as a result of

compensating the loss incurred in the past year to the ordinary course of business is definitely

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION

an income amount by adhering to the general concepts mentioned in “Section 6 (5) of ITAA

1997” (Frecknall-Hughes & Kirchler, 2015).

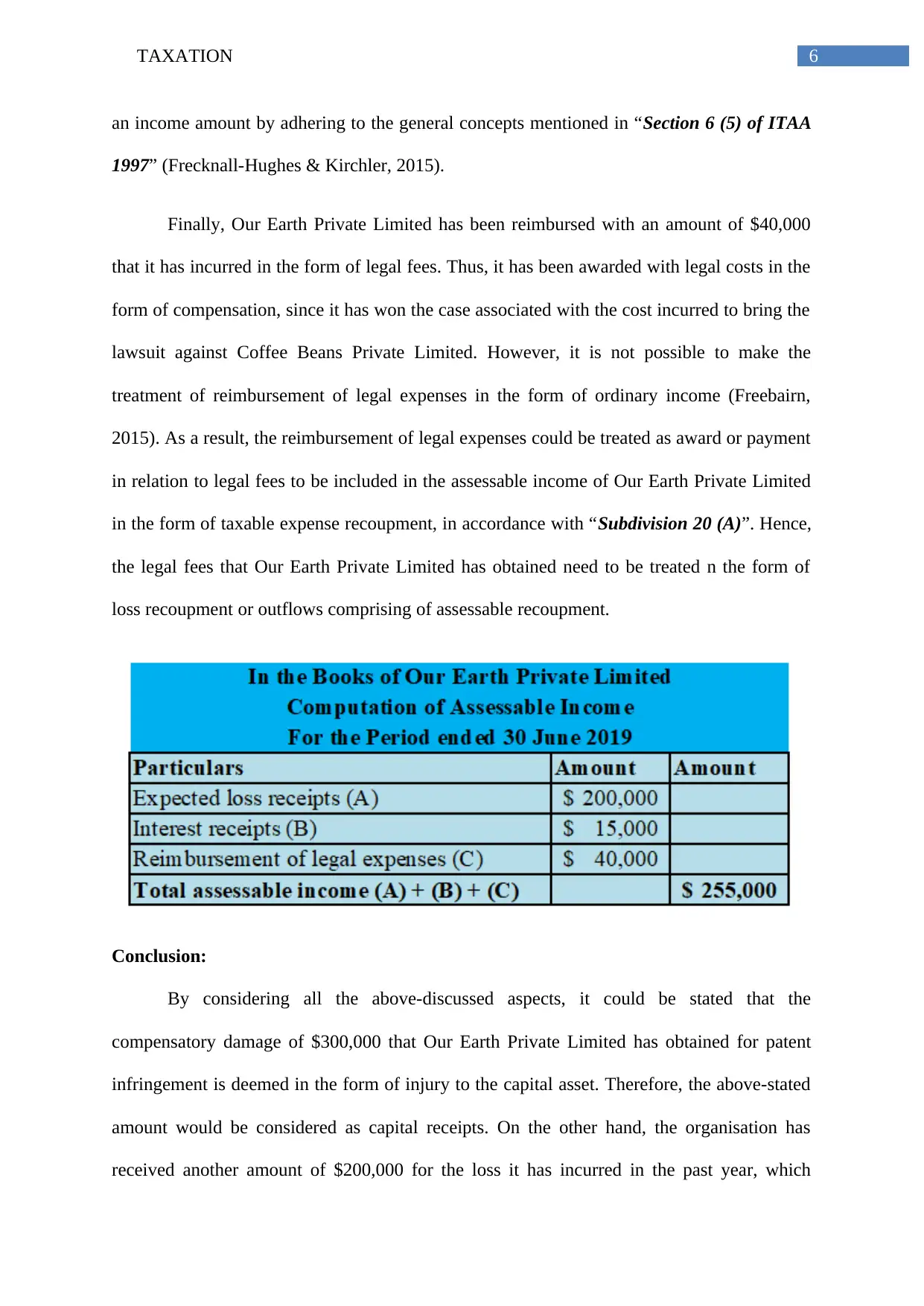

Finally, Our Earth Private Limited has been reimbursed with an amount of $40,000

that it has incurred in the form of legal fees. Thus, it has been awarded with legal costs in the

form of compensation, since it has won the case associated with the cost incurred to bring the

lawsuit against Coffee Beans Private Limited. However, it is not possible to make the

treatment of reimbursement of legal expenses in the form of ordinary income (Freebairn,

2015). As a result, the reimbursement of legal expenses could be treated as award or payment

in relation to legal fees to be included in the assessable income of Our Earth Private Limited

in the form of taxable expense recoupment, in accordance with “Subdivision 20 (A)”. Hence,

the legal fees that Our Earth Private Limited has obtained need to be treated n the form of

loss recoupment or outflows comprising of assessable recoupment.

Conclusion:

By considering all the above-discussed aspects, it could be stated that the

compensatory damage of $300,000 that Our Earth Private Limited has obtained for patent

infringement is deemed in the form of injury to the capital asset. Therefore, the above-stated

amount would be considered as capital receipts. On the other hand, the organisation has

received another amount of $200,000 for the loss it has incurred in the past year, which

an income amount by adhering to the general concepts mentioned in “Section 6 (5) of ITAA

1997” (Frecknall-Hughes & Kirchler, 2015).

Finally, Our Earth Private Limited has been reimbursed with an amount of $40,000

that it has incurred in the form of legal fees. Thus, it has been awarded with legal costs in the

form of compensation, since it has won the case associated with the cost incurred to bring the

lawsuit against Coffee Beans Private Limited. However, it is not possible to make the

treatment of reimbursement of legal expenses in the form of ordinary income (Freebairn,

2015). As a result, the reimbursement of legal expenses could be treated as award or payment

in relation to legal fees to be included in the assessable income of Our Earth Private Limited

in the form of taxable expense recoupment, in accordance with “Subdivision 20 (A)”. Hence,

the legal fees that Our Earth Private Limited has obtained need to be treated n the form of

loss recoupment or outflows comprising of assessable recoupment.

Conclusion:

By considering all the above-discussed aspects, it could be stated that the

compensatory damage of $300,000 that Our Earth Private Limited has obtained for patent

infringement is deemed in the form of injury to the capital asset. Therefore, the above-stated

amount would be considered as capital receipts. On the other hand, the organisation has

received another amount of $200,000 for the loss it has incurred in the past year, which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

would be considered as income in accordance with the ordinary concepts of “Section 6 (5) of

ITAA 1997”. In addition, the interest collected from damages is classified as income under

normal meaning of “Section 6 (5) of ITAA 1997” that draws tax liability. Finally, for

reimbursing legal expenses to Our Earth Private Limited, the same would be incorporated for

assessment purpose in the form of taxable recoupment under “Subdivision 20 (A)”.

Question 2:

Issues:

The issue here is to identify whether the liability of the taxpayer in relation to the

capital gains tax associated with the gains made from the disposal of subdivided land either

under “Section 26 (A)” or “Section 25 (1)” or there has been simple realisation of the capital

asset by the taxpayer.

Laws:

The application of capital gains tax is made generally to the assets, which are bought,

or events taking place before or after 20th September 1985. Therefore, the two terms, pre-

CGT and post-CGT are used regularly for representing the assets purchased or events

occurring before or after the date (Graetz & Warren, 2016). The application of the system of

capital gains tax is made on the recognised capital gain amount, which arises from asset sale

or from other particular events. The initial step to ascertain whether the events or transactions

that take place makes the subject of CGT along with determining whether there has been

occurrence of the CGT event.

Generally, capital gains tax acts in a prospective manner and it could be applied only

when the CGT events occur for the assets bought on or after 20th September 1985. There are a

number of exceptions for maximum CGT events. In case, the CGT asset is bought before 20th

would be considered as income in accordance with the ordinary concepts of “Section 6 (5) of

ITAA 1997”. In addition, the interest collected from damages is classified as income under

normal meaning of “Section 6 (5) of ITAA 1997” that draws tax liability. Finally, for

reimbursing legal expenses to Our Earth Private Limited, the same would be incorporated for

assessment purpose in the form of taxable recoupment under “Subdivision 20 (A)”.

Question 2:

Issues:

The issue here is to identify whether the liability of the taxpayer in relation to the

capital gains tax associated with the gains made from the disposal of subdivided land either

under “Section 26 (A)” or “Section 25 (1)” or there has been simple realisation of the capital

asset by the taxpayer.

Laws:

The application of capital gains tax is made generally to the assets, which are bought,

or events taking place before or after 20th September 1985. Therefore, the two terms, pre-

CGT and post-CGT are used regularly for representing the assets purchased or events

occurring before or after the date (Graetz & Warren, 2016). The application of the system of

capital gains tax is made on the recognised capital gain amount, which arises from asset sale

or from other particular events. The initial step to ascertain whether the events or transactions

that take place makes the subject of CGT along with determining whether there has been

occurrence of the CGT event.

Generally, capital gains tax acts in a prospective manner and it could be applied only

when the CGT events occur for the assets bought on or after 20th September 1985. There are a

number of exceptions for maximum CGT events. In case, the CGT asset is bought before 20th

8TAXATION

September 1985, the treatment would be like pre-CGT asset, which is exempted from capital

gains tax (Hauptman, Horvat & Korez-Vide, 2014). There is occurrence of capital gains or

loss in case of occurrence of the CGT event and it involves the capital asset. The occurrence

of CGT event A1 takes place in compliance with “Section 104 (10) of ITAA 1997” to the

CGT asset at the time the taxpayer is involved in selling the asset. A CGT asset could be

explained as any form of legal, property or equitable right, which is not deemed to be

property.

There are a number of events, in which the taxpayers have the opportunity of

segregating and selling the land, which are preserved primarily for ample amount of time.

These circumstances occurred, in which the primary producers own the land situated in urban

outskirts as well as residential development; imply that effective use of land could be made

by developing houses, instead of using the same for agricultural purpose (Herault &

Azpitarte, 2015). In few circumstances, this type of property development could be treated as

adequate, in which greater amount of profit could be made from land. This raises the concern

regarding the way through which profits are generated from segregation and treatment of sale

of land. Generally, three alternatives are available:

The segregation and sale of land might be qualified in the form of multiple

recognition of capital asset.

The extent of land development would be in a manner that it includes conducting the

land development business.

The development of land might move beyond the simple recognition of land;

however, the same might fall short of requirement related to conduction of business

operations in such a manner that it would be taken into account in the form of profit

deriving activities or arrangements.

September 1985, the treatment would be like pre-CGT asset, which is exempted from capital

gains tax (Hauptman, Horvat & Korez-Vide, 2014). There is occurrence of capital gains or

loss in case of occurrence of the CGT event and it involves the capital asset. The occurrence

of CGT event A1 takes place in compliance with “Section 104 (10) of ITAA 1997” to the

CGT asset at the time the taxpayer is involved in selling the asset. A CGT asset could be

explained as any form of legal, property or equitable right, which is not deemed to be

property.

There are a number of events, in which the taxpayers have the opportunity of

segregating and selling the land, which are preserved primarily for ample amount of time.

These circumstances occurred, in which the primary producers own the land situated in urban

outskirts as well as residential development; imply that effective use of land could be made

by developing houses, instead of using the same for agricultural purpose (Herault &

Azpitarte, 2015). In few circumstances, this type of property development could be treated as

adequate, in which greater amount of profit could be made from land. This raises the concern

regarding the way through which profits are generated from segregation and treatment of sale

of land. Generally, three alternatives are available:

The segregation and sale of land might be qualified in the form of multiple

recognition of capital asset.

The extent of land development would be in a manner that it includes conducting the

land development business.

The development of land might move beyond the simple recognition of land;

however, the same might fall short of requirement related to conduction of business

operations in such a manner that it would be taken into account in the form of profit

deriving activities or arrangements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION

“Taxation Determination TD 97/3” states that simple land segregation could be

considered in the form of land sale falling within “Section 104 (10) of ITAA 1997”. This

ruling is involved in providing guidance about whether the proceeds generated from selling

isolated transactions would be considered as income and therefore, it would be assessable

under “Section 25 (1) of ITAA 1936” (Jaafar & Thornton, 2015). It is crucial to determine

whether the development of land would be treated in the form of simple recognition before

depending on the full study. However, it needs to be appreciated that in case; the land was

bought actually for earning profit on resale or development purpose, the income or gains

made from land development and sale would be considered in the form of ordinary assessable

income regardless of the land sale (James, Sawyer & Budak, 2016).

The profit origination from conducting or performing the profit deriving plan or

scheme related to the property bought from the initiation of CGT or pre-CGT asset is

incorporated primarily within “Section 15 (15) of ITAA 1997”. The capital improvements

that the taxpayer has made on the capital gains tax asset are subject to CGT (Woellner et al.,

2014). On the other hand, if the taxpayer at the time of buying the land undertakes

considerable capital improvement after the date of purchase, it would be included in the

asset’s cost base for the purpose of capital gains tax.

In the case of “Scottish Australian Mining Company Limited v FC of T (1950)”,

verdict has been passed by the Federal Court by citing that the taxpayer obtained considerable

profit by disposing off subdivided lots (McGee, Devos & Benk, 2016). The taxpayer was

held assessable in relation to the gains obtained from selling various land lots. From the

viewpoint of the Commissioner of Taxation, the profits were considered as taxable income

either within “Section 25 (1) of ITAA 1936”, as gains earned from conducting the land

development business or within the provision in legislation of “Section 26 (a)”, since the

profits are generated from undertaking revenue generation (Merz & Overesch, 2016).

“Taxation Determination TD 97/3” states that simple land segregation could be

considered in the form of land sale falling within “Section 104 (10) of ITAA 1997”. This

ruling is involved in providing guidance about whether the proceeds generated from selling

isolated transactions would be considered as income and therefore, it would be assessable

under “Section 25 (1) of ITAA 1936” (Jaafar & Thornton, 2015). It is crucial to determine

whether the development of land would be treated in the form of simple recognition before

depending on the full study. However, it needs to be appreciated that in case; the land was

bought actually for earning profit on resale or development purpose, the income or gains

made from land development and sale would be considered in the form of ordinary assessable

income regardless of the land sale (James, Sawyer & Budak, 2016).

The profit origination from conducting or performing the profit deriving plan or

scheme related to the property bought from the initiation of CGT or pre-CGT asset is

incorporated primarily within “Section 15 (15) of ITAA 1997”. The capital improvements

that the taxpayer has made on the capital gains tax asset are subject to CGT (Woellner et al.,

2014). On the other hand, if the taxpayer at the time of buying the land undertakes

considerable capital improvement after the date of purchase, it would be included in the

asset’s cost base for the purpose of capital gains tax.

In the case of “Scottish Australian Mining Company Limited v FC of T (1950)”,

verdict has been passed by the Federal Court by citing that the taxpayer obtained considerable

profit by disposing off subdivided lots (McGee, Devos & Benk, 2016). The taxpayer was

held assessable in relation to the gains obtained from selling various land lots. From the

viewpoint of the Commissioner of Taxation, the profits were considered as taxable income

either within “Section 25 (1) of ITAA 1936”, as gains earned from conducting the land

development business or within the provision in legislation of “Section 26 (a)”, since the

profits are generated from undertaking revenue generation (Merz & Overesch, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION

Another case of “Federal Commissioner of Taxation v Whitfords Beach Private

Limited (1982)” reveals that the taxpayer was held taxable by the Federal Court owing to the

gains generated from sale of various land plots (Annuar, Salihu & Obid, 2014). From the

perspective of the Taxation Officer, the profits were considered as taxable income either

within “Section 25 (1) of ITAA 1936”, as gains earned from conducting the land

development business or within the provision in legislation of “Section 26 (a)”, since the

profits are generated from undertaking revenue generation.

After understanding the fact that land acquisition and its sale result in profit

generation not falling within the ordinary business course or subject of ordinary business

operations, the income needs to be considered in the form of assessable earnings of the

taxpayer within the normal meaning. However, it is assumed that the intention of the taxpayer

is to earn profit at the time of buying the land.

Application:

From the provided case of Sam, it has been identified that the individual has

purchased two lands of 80 acres and 20 acres. The 20 acres of land has been purchased

primarily for diversifying the business operations. However, over time, Sam was not

interested in conducting the agriculture business owing to the prevailing drought conditions,

which had adversely affected the business operations. Therefore, Sam undertook the decision

of selling the land and eventually took retirement from the business. After taking the service

of real estate agent, advice was provided to Sam that it would be beneficial to subdivide the

land for obtaining the maximum price. Sam accepted this advice and he decided to subdivide

the land for accommodating residential development rather than conducting farming

operations.

Another case of “Federal Commissioner of Taxation v Whitfords Beach Private

Limited (1982)” reveals that the taxpayer was held taxable by the Federal Court owing to the

gains generated from sale of various land plots (Annuar, Salihu & Obid, 2014). From the

perspective of the Taxation Officer, the profits were considered as taxable income either

within “Section 25 (1) of ITAA 1936”, as gains earned from conducting the land

development business or within the provision in legislation of “Section 26 (a)”, since the

profits are generated from undertaking revenue generation.

After understanding the fact that land acquisition and its sale result in profit

generation not falling within the ordinary business course or subject of ordinary business

operations, the income needs to be considered in the form of assessable earnings of the

taxpayer within the normal meaning. However, it is assumed that the intention of the taxpayer

is to earn profit at the time of buying the land.

Application:

From the provided case of Sam, it has been identified that the individual has

purchased two lands of 80 acres and 20 acres. The 20 acres of land has been purchased

primarily for diversifying the business operations. However, over time, Sam was not

interested in conducting the agriculture business owing to the prevailing drought conditions,

which had adversely affected the business operations. Therefore, Sam undertook the decision

of selling the land and eventually took retirement from the business. After taking the service

of real estate agent, advice was provided to Sam that it would be beneficial to subdivide the

land for obtaining the maximum price. Sam accepted this advice and he decided to subdivide

the land for accommodating residential development rather than conducting farming

operations.

11TAXATION

Initially, for the ascertainment of capital gains tax, it is essential to consider the

buying date of the asset for the purpose of capital gains tax. The 80-acre land was bought by

Sam in 1984. Hence, with relation to the CGT provision, 80 acres of land would be

considered in the form of pre-CGT asset. Therefore, as the land is identified as pre-CGT

asset, there would be no application of capital gains tax (Akhtar, 2018). The capital gains tax

generated from selling the land would be taken into account in the form of an exemption for

the purpose of tax.

On the contrary, Sam purchased 20 acres of land, which was close to the farm land on

February 1995. Therefore, it mandates the need to treat the land in the form of pre-CGT asset

owing to the fact that it is purchased after the initiation of regimes related to capital gains tax

(Woellner et al., 2016). There was commencement of the subdivision in 2017 and the sale of

land was made finally in April 2018. Thus, capital gains earned from the sale of 20-acre land

are subject to capital gains tax in the form of post-CGT asset.

Based on the current scenario of Sam, the development of land would be treated

adequate with the intention of earning significant profits from the project. With reference to

the “Taxation Determination TD 97/3”, it could be cited that for ascertaining the gains made

from the subdivided land sale, they have to be taken into account as income and hence, it us

taxable in compliance with “Section 25 (1) of ITAA 1936” (Zucman, 2015). Before involving

in detailed analysis, it is to be noted that the property was not bought actually for resale to

earn profit or for development. The profit intention arrived in the later stage.

In the case of “Scottish Australian Mining Company Limited v FC of T (1950)”, the

taxpayer earned significant profit by selling the subdivided allotments (Miller & Oats,

2016). Therefore, Sam would be considered as assessable for the purpose of capital gains tax

in such circumstance for the gains earned from sale of land in compliance with “Section 25

Initially, for the ascertainment of capital gains tax, it is essential to consider the

buying date of the asset for the purpose of capital gains tax. The 80-acre land was bought by

Sam in 1984. Hence, with relation to the CGT provision, 80 acres of land would be

considered in the form of pre-CGT asset. Therefore, as the land is identified as pre-CGT

asset, there would be no application of capital gains tax (Akhtar, 2018). The capital gains tax

generated from selling the land would be taken into account in the form of an exemption for

the purpose of tax.

On the contrary, Sam purchased 20 acres of land, which was close to the farm land on

February 1995. Therefore, it mandates the need to treat the land in the form of pre-CGT asset

owing to the fact that it is purchased after the initiation of regimes related to capital gains tax

(Woellner et al., 2016). There was commencement of the subdivision in 2017 and the sale of

land was made finally in April 2018. Thus, capital gains earned from the sale of 20-acre land

are subject to capital gains tax in the form of post-CGT asset.

Based on the current scenario of Sam, the development of land would be treated

adequate with the intention of earning significant profits from the project. With reference to

the “Taxation Determination TD 97/3”, it could be cited that for ascertaining the gains made

from the subdivided land sale, they have to be taken into account as income and hence, it us

taxable in compliance with “Section 25 (1) of ITAA 1936” (Zucman, 2015). Before involving

in detailed analysis, it is to be noted that the property was not bought actually for resale to

earn profit or for development. The profit intention arrived in the later stage.

In the case of “Scottish Australian Mining Company Limited v FC of T (1950)”, the

taxpayer earned significant profit by selling the subdivided allotments (Miller & Oats,

2016). Therefore, Sam would be considered as assessable for the purpose of capital gains tax

in such circumstance for the gains earned from sale of land in compliance with “Section 25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.