Taxation Case Studies: Analysis and Application of Tax Laws

VerifiedAdded on 2020/04/01

|11

|2247

|52

Homework Assignment

AI Summary

This taxation assignment provides a detailed analysis of several case studies related to Australian taxation law. The assignment examines issues such as calculating capital gains and losses from the sale of assets, determining fringe benefit tax (FBT) liabilities for bank employees, and the division of profits and losses from jointly held rental properties. It also explores the legal case of IRC v Duke of Westminster regarding tax avoidance and analyzes income derived from the sale of timber. The assignment references relevant taxation directives and case law, including the ITAA, TR 93/6, TR 93/32, and the case of F.C. of T. v McDonald, to support its conclusions. Overall, the assignment provides a comprehensive overview of key taxation principles and their application to real-world scenarios.

Running head: TAXATION

Taxation

University Name

Student Name

Authors’ Note

Taxation

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2TAXATION

Assignment Question 1:

Issues that can be hereby recognized from the case analysis:

The present segment elucidates in detail regarding ascertainment of capital gain otherwise

loss from Eric’s transaction of antique vase. The current scenario mentioned in the case helps

in knowing the fact that Eric got possession of various resource counting antique vase as well

as chair, sound system for home, paintings as well as shares of particular listed business

corporations. Nonetheless, Eric marketed all the above mentioned resources only after

acquisition of the stated ones. Essentially, this case aims to establish the accurate capital gain

otherwise loss from the said trade. Yet, this process of establishment of the right capital gain

else wise loss can be correlated to specific bylaws of tax that is 108-20 decree asserted by

ITAA. Plainly this issue mentioned herein the case can be understood after proper orientation

to the tax diktat (108-20) articulated by ITAA (Woellner et al., 2016).

Taxation dictates that is pertinent to the current case under deliberation

Taxation bylaws that can be referred to in the present section involve the following

mentioned ones:

Assignment Question 1:

Issues that can be hereby recognized from the case analysis:

The present segment elucidates in detail regarding ascertainment of capital gain otherwise

loss from Eric’s transaction of antique vase. The current scenario mentioned in the case helps

in knowing the fact that Eric got possession of various resource counting antique vase as well

as chair, sound system for home, paintings as well as shares of particular listed business

corporations. Nonetheless, Eric marketed all the above mentioned resources only after

acquisition of the stated ones. Essentially, this case aims to establish the accurate capital gain

otherwise loss from the said trade. Yet, this process of establishment of the right capital gain

else wise loss can be correlated to specific bylaws of tax that is 108-20 decree asserted by

ITAA. Plainly this issue mentioned herein the case can be understood after proper orientation

to the tax diktat (108-20) articulated by ITAA (Woellner et al., 2016).

Taxation dictates that is pertinent to the current case under deliberation

Taxation bylaws that can be referred to in the present section involve the following

mentioned ones:

3TAXATION

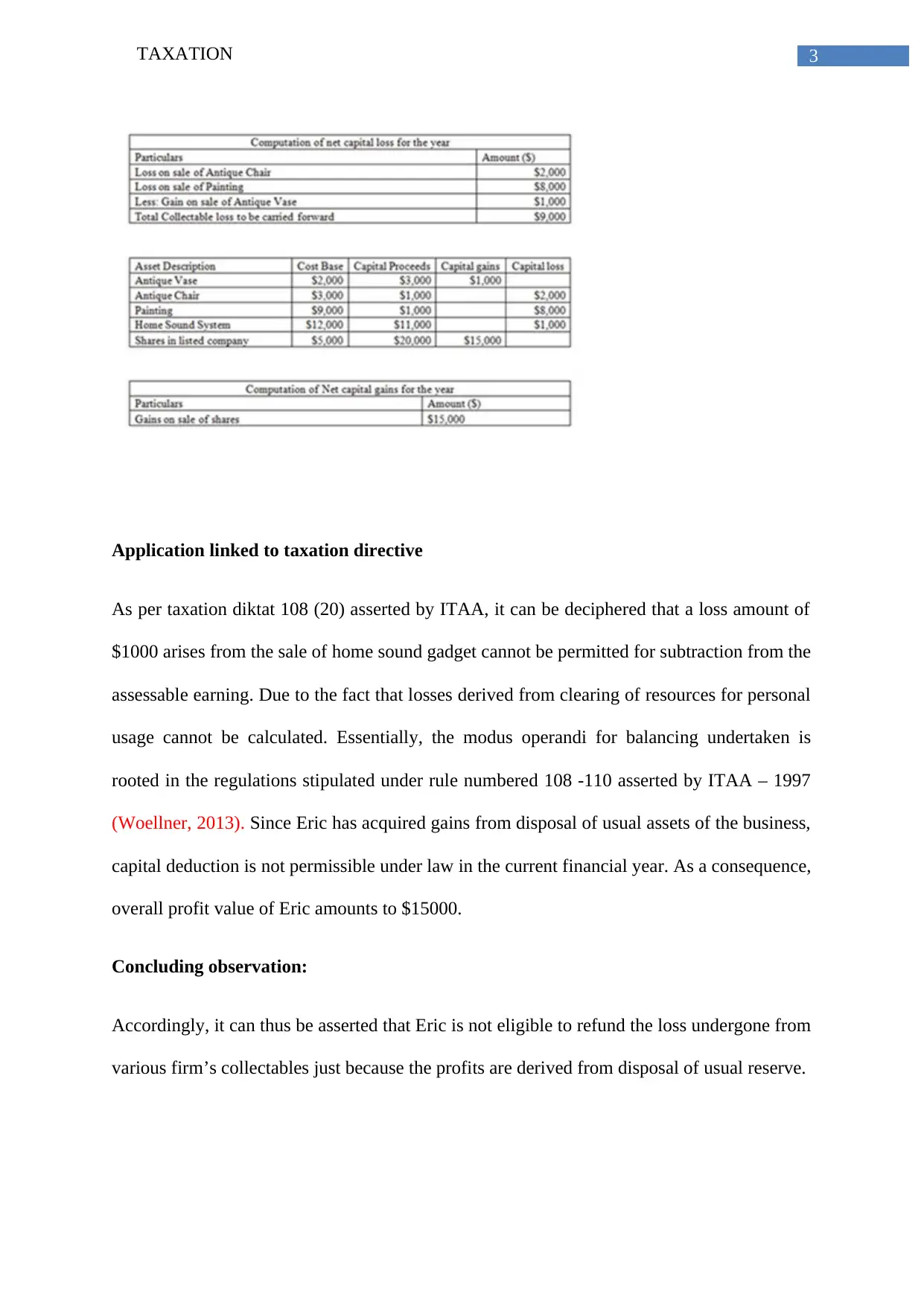

Application linked to taxation directive

As per taxation diktat 108 (20) asserted by ITAA, it can be deciphered that a loss amount of

$1000 arises from the sale of home sound gadget cannot be permitted for subtraction from the

assessable earning. Due to the fact that losses derived from clearing of resources for personal

usage cannot be calculated. Essentially, the modus operandi for balancing undertaken is

rooted in the regulations stipulated under rule numbered 108 -110 asserted by ITAA – 1997

(Woellner, 2013). Since Eric has acquired gains from disposal of usual assets of the business,

capital deduction is not permissible under law in the current financial year. As a consequence,

overall profit value of Eric amounts to $15000.

Concluding observation:

Accordingly, it can thus be asserted that Eric is not eligible to refund the loss undergone from

various firm’s collectables just because the profits are derived from disposal of usual reserve.

Application linked to taxation directive

As per taxation diktat 108 (20) asserted by ITAA, it can be deciphered that a loss amount of

$1000 arises from the sale of home sound gadget cannot be permitted for subtraction from the

assessable earning. Due to the fact that losses derived from clearing of resources for personal

usage cannot be calculated. Essentially, the modus operandi for balancing undertaken is

rooted in the regulations stipulated under rule numbered 108 -110 asserted by ITAA – 1997

(Woellner, 2013). Since Eric has acquired gains from disposal of usual assets of the business,

capital deduction is not permissible under law in the current financial year. As a consequence,

overall profit value of Eric amounts to $15000.

Concluding observation:

Accordingly, it can thus be asserted that Eric is not eligible to refund the loss undergone from

various firm’s collectables just because the profits are derived from disposal of usual reserve.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4TAXATION

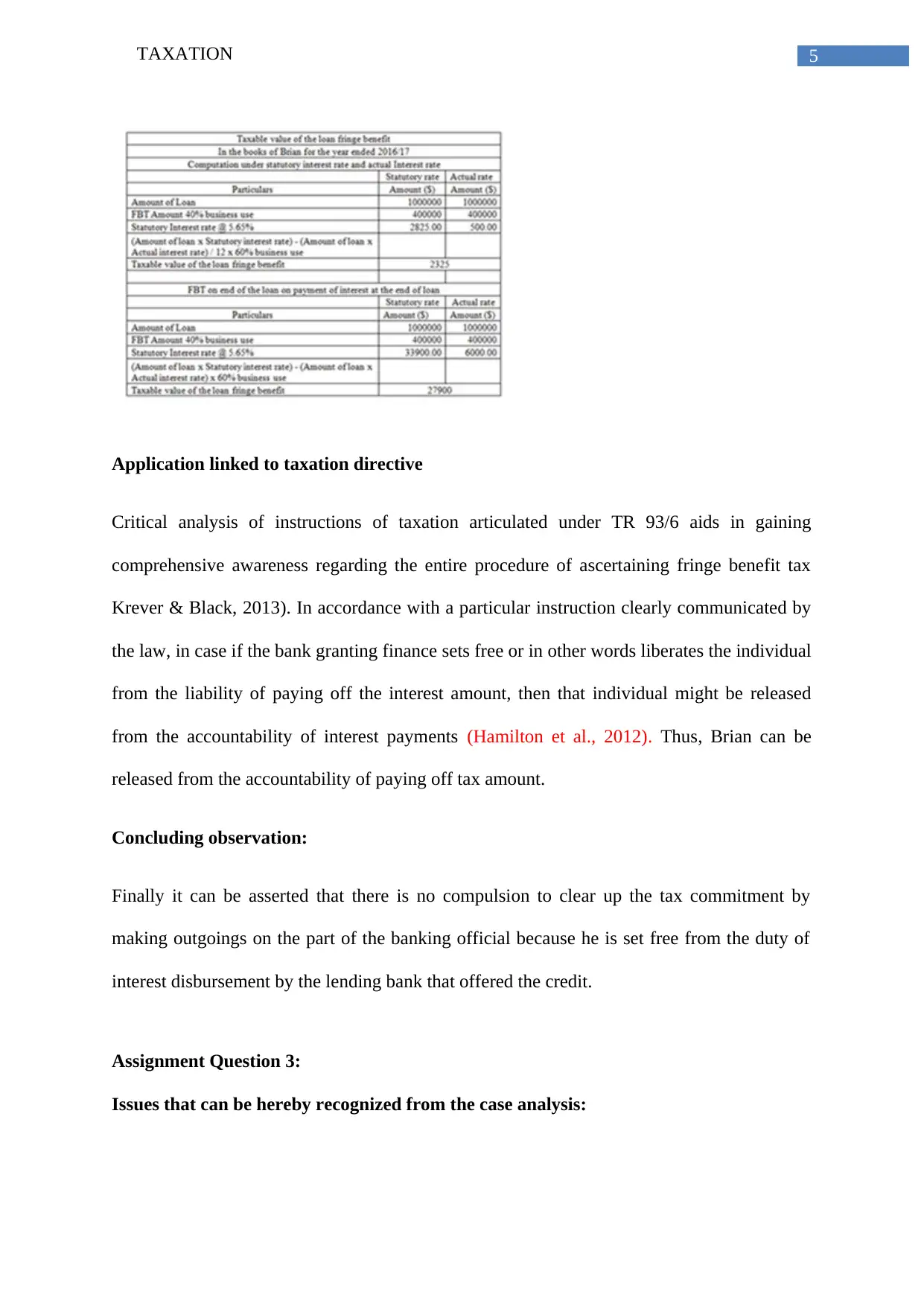

Assignment Question 2:

Issues that can be hereby recognized from the case analysis:

The study refers to a case on business dealings connected to a particular bank official named

as Brian. The case illustrates that the employer of the specific granted Brian a loan amounting

to $1 million with attached interest rate of nearly 1% every year. Nevertheless, the present

set-up also divulges the fact that the banking official employed 40% of this lent amount for

making income and met all the loan obligations concerning the interest expense. The current

question is to spell out the measurable value of fringe benefit enumerated for the year 2016 as

well as 2017. In addition to this, this present section also intends to assess whether the answer

derived might possibly be completely in case of payment of interest on lent amount at the

termination period of the loan agreement instead of monthly disbursements of interests.

However, it is vital to comprehend if the bank sets frees Brian from paying back the amount

of interest on borrowed funds. Therefore, the current case study under deliberation can be

attached to the resolving of concerns in the process of ascertainment of FBT-taxation (fringe

benefit). Essentially, this again can be connected to taxation decree asserted under bylaw TR

93/6 (Wallschutzky, 2012).

Taxation dictates that is pertinent to the current case under deliberation

Calculation of Fringe Benefit Tax (FBT)

Assignment Question 2:

Issues that can be hereby recognized from the case analysis:

The study refers to a case on business dealings connected to a particular bank official named

as Brian. The case illustrates that the employer of the specific granted Brian a loan amounting

to $1 million with attached interest rate of nearly 1% every year. Nevertheless, the present

set-up also divulges the fact that the banking official employed 40% of this lent amount for

making income and met all the loan obligations concerning the interest expense. The current

question is to spell out the measurable value of fringe benefit enumerated for the year 2016 as

well as 2017. In addition to this, this present section also intends to assess whether the answer

derived might possibly be completely in case of payment of interest on lent amount at the

termination period of the loan agreement instead of monthly disbursements of interests.

However, it is vital to comprehend if the bank sets frees Brian from paying back the amount

of interest on borrowed funds. Therefore, the current case study under deliberation can be

attached to the resolving of concerns in the process of ascertainment of FBT-taxation (fringe

benefit). Essentially, this again can be connected to taxation decree asserted under bylaw TR

93/6 (Wallschutzky, 2012).

Taxation dictates that is pertinent to the current case under deliberation

Calculation of Fringe Benefit Tax (FBT)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5TAXATION

Application linked to taxation directive

Critical analysis of instructions of taxation articulated under TR 93/6 aids in gaining

comprehensive awareness regarding the entire procedure of ascertaining fringe benefit tax

Krever & Black, 2013). In accordance with a particular instruction clearly communicated by

the law, in case if the bank granting finance sets free or in other words liberates the individual

from the liability of paying off the interest amount, then that individual might be released

from the accountability of interest payments (Hamilton et al., 2012). Thus, Brian can be

released from the accountability of paying off tax amount.

Concluding observation:

Finally it can be asserted that there is no compulsion to clear up the tax commitment by

making outgoings on the part of the banking official because he is set free from the duty of

interest disbursement by the lending bank that offered the credit.

Assignment Question 3:

Issues that can be hereby recognized from the case analysis:

Application linked to taxation directive

Critical analysis of instructions of taxation articulated under TR 93/6 aids in gaining

comprehensive awareness regarding the entire procedure of ascertaining fringe benefit tax

Krever & Black, 2013). In accordance with a particular instruction clearly communicated by

the law, in case if the bank granting finance sets free or in other words liberates the individual

from the liability of paying off the interest amount, then that individual might be released

from the accountability of interest payments (Hamilton et al., 2012). Thus, Brian can be

released from the accountability of paying off tax amount.

Concluding observation:

Finally it can be asserted that there is no compulsion to clear up the tax commitment by

making outgoings on the part of the banking official because he is set free from the duty of

interest disbursement by the lending bank that offered the credit.

Assignment Question 3:

Issues that can be hereby recognized from the case analysis:

6TAXATION

The concern in the given case can be related to proper terms of division of profit otherwise

loss among two different co-carrier of rental assets (property) (Halligan, 2015).

Taxation dictates that is pertinent to the current case under deliberation

Application linked to taxation directive

As rightly indicated by Ganghof & Eccleston (2014), taxation instruction articulated under

TR 93/32 presents ways of treating profits otherwise losses arising from jointly holding rental

properties. As per the instructions articulated under by law TR 93/32, rental possessions

jointly held cannot be referred to as partnerships in the process of tax assessment (Eccleston,

2014). The relevant guideline as cited under this ruling explicates the fact that partnership

accord that includes both either in written format or by word of mouth is said to exert any

impact on the overall process of distributing proceeds derived from the jointly held rental

property. Moreover, the diktat under this bylaw also stresses the fact that co-owners of a

specific rental possession under contemplation cannot be viewed as partners particularly

under common circumstances of the ruling. Fundamentally, treaties of joint venture cannot

have any effect on the combined amount of either profit or else loss divided between the co-

possessors of the property. As per the given case study, proportion s of liability of Jack as

well as his wife is essentially 90% and 10% respectively. The verdicts of the case on F.C. of

T. v McDonald (1987) 18 ATR 957 can be referred to in this regard. This law case verdict

states that partner of the spender of tax laid hands on two diverse title in a specific shared

venture (Eccleston, 2012). Based on this it can be said that the treaty helped in validating that

two different holders of assets (in this case Jack and Jill) can acquire earnings in the specific

The concern in the given case can be related to proper terms of division of profit otherwise

loss among two different co-carrier of rental assets (property) (Halligan, 2015).

Taxation dictates that is pertinent to the current case under deliberation

Application linked to taxation directive

As rightly indicated by Ganghof & Eccleston (2014), taxation instruction articulated under

TR 93/32 presents ways of treating profits otherwise losses arising from jointly holding rental

properties. As per the instructions articulated under by law TR 93/32, rental possessions

jointly held cannot be referred to as partnerships in the process of tax assessment (Eccleston,

2014). The relevant guideline as cited under this ruling explicates the fact that partnership

accord that includes both either in written format or by word of mouth is said to exert any

impact on the overall process of distributing proceeds derived from the jointly held rental

property. Moreover, the diktat under this bylaw also stresses the fact that co-owners of a

specific rental possession under contemplation cannot be viewed as partners particularly

under common circumstances of the ruling. Fundamentally, treaties of joint venture cannot

have any effect on the combined amount of either profit or else loss divided between the co-

possessors of the property. As per the given case study, proportion s of liability of Jack as

well as his wife is essentially 90% and 10% respectively. The verdicts of the case on F.C. of

T. v McDonald (1987) 18 ATR 957 can be referred to in this regard. This law case verdict

states that partner of the spender of tax laid hands on two diverse title in a specific shared

venture (Eccleston, 2012). Based on this it can be said that the treaty helped in validating that

two different holders of assets (in this case Jack and Jill) can acquire earnings in the specific

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7TAXATION

percentage fraction of particularly 75% and 25% respectively. In the light of the instructions

mentioned herein, both the co-owners that is Jack along with wife Jill have the right on the

proceeds of the property as joint renters.

Concluding observation:

In conjunction with the instruction articulated in the bylaws TR 93/32, it can thus be made

out that in cases of joint holders of rental possessions, loss undergone can be justifiably

scattered among the two different possessors, despite the fact that joint holding of rented

possessions cannot be considered to be treated in the similar manner as the dealings carried

out in partnerships.

Assignment Question4:

Case on “IRC v Duke of Westminster [1936] AC 1” narrates about tax shirking. This

particular instance bears mention about the fact that all individuals have the permission to

direct specific state of affairs for allowing deductions from the measured obligation of tax

(Eccleston, 2014). Necessarily, this legal case speaks about the “Duke of Westminster” who

deployed a gardener and paid compensation from the substantial earnings derived post tax

from essentially the Dike. However, for the purpose of lessening the overall taxed value, the

Duke also discontinued to provide wage to that specific gardener and instead developed a

pact to carry out disbursements that is of equal value. Nevertheless, the decrees of tax gave

Duke the authority to claim for a deduction in the process of his tax assessment (Ganghof &

Eccleston, 2014). Essentially, this subsequently decreased the overall liability of the payer of

tax as both the income tax as well as the surtax got lessened. As such, the Inland Revenue as

a matter of fact lost in the legal case that was against the Duke. This case talks about the

individuals seeking for ways of evading tax legally by generation of specific circumstances.

However, in the present circumstances, the principle in Australia explicates that if a specific

percentage fraction of particularly 75% and 25% respectively. In the light of the instructions

mentioned herein, both the co-owners that is Jack along with wife Jill have the right on the

proceeds of the property as joint renters.

Concluding observation:

In conjunction with the instruction articulated in the bylaws TR 93/32, it can thus be made

out that in cases of joint holders of rental possessions, loss undergone can be justifiably

scattered among the two different possessors, despite the fact that joint holding of rented

possessions cannot be considered to be treated in the similar manner as the dealings carried

out in partnerships.

Assignment Question4:

Case on “IRC v Duke of Westminster [1936] AC 1” narrates about tax shirking. This

particular instance bears mention about the fact that all individuals have the permission to

direct specific state of affairs for allowing deductions from the measured obligation of tax

(Eccleston, 2014). Necessarily, this legal case speaks about the “Duke of Westminster” who

deployed a gardener and paid compensation from the substantial earnings derived post tax

from essentially the Dike. However, for the purpose of lessening the overall taxed value, the

Duke also discontinued to provide wage to that specific gardener and instead developed a

pact to carry out disbursements that is of equal value. Nevertheless, the decrees of tax gave

Duke the authority to claim for a deduction in the process of his tax assessment (Ganghof &

Eccleston, 2014). Essentially, this subsequently decreased the overall liability of the payer of

tax as both the income tax as well as the surtax got lessened. As such, the Inland Revenue as

a matter of fact lost in the legal case that was against the Duke. This case talks about the

individuals seeking for ways of evading tax legally by generation of specific circumstances.

However, in the present circumstances, the principle in Australia explicates that if a specific

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8TAXATION

individual can attain success for getting to the conclusion, the entire Inland Revenue in such

case might possibly be subjugated for their format (Halligan, 2015).

Assignment Question5:

Issues that can be hereby recognized from the case analysis:

The recognized matter in the present state revolves around analysis of earnings arising from

the takings of the company from the sales of felled timber. Basically, this particular amount

can be observed under taxation bylaw articulated under 6-1 of the rule for Assessment of

Income (that is to say, Income Tax Assessment Act-1936) (Eccleston, 2014).

Taxation dictates that is pertinent to the current case under deliberation

Application linked to taxation directive

Detailed evaluation of the case reflects that Bill necessarily possesses a particular land that

has pine trees. Moving further, the case under reflection also asserts that Bill has the intention

to put the land to use for the purpose of grazing by sheep and get it cleaned. Over and above

this, Bill got the impression that a logging entity is all set to pay $1000 for timber. Setting

apart all the matters of concern related to the taxation attached to capital gains, Bill is given

recommendations concerning the takings from the specific scheme.

Essentially, decree of taxation articulated under TR 95/6 indicates towards upshots of

taxation that necessarily crop up from the productions with works on plantation and forestry

works (Keating, 2015). In addition to this, this specific ruling dictates divulges the bindings

or else limitations as regards takings from the business that arise out of the sales of the timber

individual can attain success for getting to the conclusion, the entire Inland Revenue in such

case might possibly be subjugated for their format (Halligan, 2015).

Assignment Question5:

Issues that can be hereby recognized from the case analysis:

The recognized matter in the present state revolves around analysis of earnings arising from

the takings of the company from the sales of felled timber. Basically, this particular amount

can be observed under taxation bylaw articulated under 6-1 of the rule for Assessment of

Income (that is to say, Income Tax Assessment Act-1936) (Eccleston, 2014).

Taxation dictates that is pertinent to the current case under deliberation

Application linked to taxation directive

Detailed evaluation of the case reflects that Bill necessarily possesses a particular land that

has pine trees. Moving further, the case under reflection also asserts that Bill has the intention

to put the land to use for the purpose of grazing by sheep and get it cleaned. Over and above

this, Bill got the impression that a logging entity is all set to pay $1000 for timber. Setting

apart all the matters of concern related to the taxation attached to capital gains, Bill is given

recommendations concerning the takings from the specific scheme.

Essentially, decree of taxation articulated under TR 95/6 indicates towards upshots of

taxation that necessarily crop up from the productions with works on plantation and forestry

works (Keating, 2015). In addition to this, this specific ruling dictates divulges the bindings

or else limitations as regards takings from the business that arise out of the sales of the timber

9TAXATION

derived from the land. Fundamentally, this requires enquiry regarding the fact that whether

the person paying the tax is in any way in a partaker in the forestry works. 6-1 stipulated

under taxation act -1936, manufacturing can be linked to activities of plantation (Krever &

Black, 2013). Detailed assessment of the case of Bill reveals that Bill did not carry out any

kind of plantation work. However, Bill received the takings derived from selling the felled

timber. Therefore, this can be observed as a measurable income of the person paying the tax.

Concluding observation:

Finally, it can be hereby ascertained that acceptance of different takings that are generated

from sales that is in this specific case obtained from sales of timber can be viewed as

measurable income as per directive articulated under 6 –(1) pronounced by ITAA.

derived from the land. Fundamentally, this requires enquiry regarding the fact that whether

the person paying the tax is in any way in a partaker in the forestry works. 6-1 stipulated

under taxation act -1936, manufacturing can be linked to activities of plantation (Krever &

Black, 2013). Detailed assessment of the case of Bill reveals that Bill did not carry out any

kind of plantation work. However, Bill received the takings derived from selling the felled

timber. Therefore, this can be observed as a measurable income of the person paying the tax.

Concluding observation:

Finally, it can be hereby ascertained that acceptance of different takings that are generated

from sales that is in this specific case obtained from sales of timber can be viewed as

measurable income as per directive articulated under 6 –(1) pronounced by ITAA.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10TAXATION

References

Eccleston, R. (2012). Taxing times: a political retrospective. Austl. Tax F., 17, 287.

Eccleston, R. (2014). Thirty year problem: the politics of Australian tax reform,

The. Australian Tax Research Foundation Research Studies, 206.

Ganghof, S., & Eccleston, R. (2014). Globalisation and the dilemmas of income taxation in

Australia. Australian Journal of Political Science, 39(3), 519-534.

Halligan, J. (2015). Learning from experience in Australian reform: balancing principle and

pragmatism. Learning from Reform.

Hamilton, R., Deutsch, R., & Raneri, J. (2012). Guidebook to Australian international

taxation. St Leonards, N.S.W.: Prospect Media.

Keating, P. (2015). Reform of the Australian taxation system: Statement by the treasurer (No.

315). Australian Government Publishing Service.

Krever, R., & Black, C. (2013). Australian taxation law cases 2007. Pyrmont, N.S.W.:

Thomson ATP.

Wallschutzky, I. G. (2012). The effects of tax reform on tax evasion (No. 8). Australian Tax

Research Foundation.

Woellner, R. (2013). Australian taxation law 2012. North Ryde [N.S.W.]: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. Melbourne, Vic.: Oxford University Press.

References

Eccleston, R. (2012). Taxing times: a political retrospective. Austl. Tax F., 17, 287.

Eccleston, R. (2014). Thirty year problem: the politics of Australian tax reform,

The. Australian Tax Research Foundation Research Studies, 206.

Ganghof, S., & Eccleston, R. (2014). Globalisation and the dilemmas of income taxation in

Australia. Australian Journal of Political Science, 39(3), 519-534.

Halligan, J. (2015). Learning from experience in Australian reform: balancing principle and

pragmatism. Learning from Reform.

Hamilton, R., Deutsch, R., & Raneri, J. (2012). Guidebook to Australian international

taxation. St Leonards, N.S.W.: Prospect Media.

Keating, P. (2015). Reform of the Australian taxation system: Statement by the treasurer (No.

315). Australian Government Publishing Service.

Krever, R., & Black, C. (2013). Australian taxation law cases 2007. Pyrmont, N.S.W.:

Thomson ATP.

Wallschutzky, I. G. (2012). The effects of tax reform on tax evasion (No. 8). Australian Tax

Research Foundation.

Woellner, R. (2013). Australian taxation law 2012. North Ryde [N.S.W.]: CCH Australia.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. Melbourne, Vic.: Oxford University Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11TAXATION

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.